Quick Answer

Use a letter of credit for international project deals when non-payment would materially hurt delivery and you can present exact milestone documents. Build document requirements before issuance, then dry-run the draft with your bank and client to remove mismatch risk. Confirm fee ownership, whether confirmation is required, and which governing rules are written into the credit text, including UCP 600 when intended, before work begins.

The Letter of Credit, Reimagined: Securing High-Value Service Contracts#

A letter of credit for international project work can protect payment, but document compliance is often the make-or-break issue. Banks examine what you present against the credit terms, and even a small mismatch can force correction and resubmission before payment moves. That delay can hit cash flow at the worst possible moment.

Treat the LC as a separate payment contract before kickoff, not as a footnote to your services agreement. UCP 600 is a common baseline for documentary credits, but it applies only if the credit text says it does. The examination window is commonly up to 5 banking days after presentation, so build that into your timing if milestone cash funds the next phase of delivery.

| Party | What they are obligated to do | Verify before kickoff | Common misunderstanding |

|---|---|---|---|

| Applicant | Requests the credit from its bank | Your client can support terms that match your real delivery evidence | "We can clean up the wording later." |

| Beneficiary (you) | Presents complying documents to draw | You can produce every required item exactly as written | "Proof of delivery alone is enough." |

| Issuing bank | Issues the credit and honors a complying presentation | The documentary conditions are clear enough to be checked without interpretation | "The bank will read vague service language in our favor." |

| Advising or confirming bank | Advises the credit; a confirmer adds its own undertaking | Whether you only have advice or an added payment undertaking | "If a bank advises it, that bank is automatically paying." |

The right instrument depends on the payment trigger, not the label.

| Decision point | Commercial LC | SBLC |

|---|---|---|

| Payment trigger | Planned documentary draw in normal payment flow | Default-triggered backstop |

| Workflow burden | Higher in day-to-day operations because routine draws depend on compliant presentation | Lighter in normal operations, heavier if invoked |

| Margin impact | Ongoing bank fees and admin can compress margin | Bank appetite and pricing posture can shift during negotiation |

| Best fit | Milestone-based work with clean, objective acceptance artifacts | Mostly trusted invoicing flow where you still want fallback security |

Before the contract is locked, define an evidence pack the bank can actually examine under the draft LC terms: document names, signing role, acceptance wording, and presentation format. A practical draft line can look like this: "Milestone Acceptance Certificate, signed by [role per LC wording], dated [DD/MM/YYYY], presented as [format accepted by bank], subject to [rule set stated in the credit]." If acceptance language is subjective or signing authority is unclear, pause before issuance. Use this pre-issuance checkpoint:

- Go if the draft credit mirrors documents you can produce without interpretation.

- Go if fee ownership, confirmation need, and expiry timing are explicit.

- Pause if the advising bank is being treated as the payer.

- Pause if your margin cannot absorb LC overhead. If that is the issue, read The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

We covered related payment-routing mechanics in A Guide to the 'For Further Credit' (FFC) Instruction in Wire Transfers.

How to Secure a Letter of Credit: A Four-Step Process#

If you decide an LC is the right tool, the order matters: qualify fit early, design the evidence pack, stress-test the draft, then run a final go or pause gate before kickoff.

| Step | Primary owner | What you do | Handoff point | Expected output |

|---|---|---|---|---|

| 1. Qualify fit early | You, client, your bank | Raise LC terms during negotiation and get your bank's view before application | Client agrees in principle and proceeds as applicant | Early go/no-go on LC fit |

| 2. Design the document pack | You | Convert each payment condition into bank-checkable documents | Client uses that set in the sales agreement and LC application | Draft-ready evidence checklist |

| 3. Stress-test the draft | You, then client, then issuing bank | Simulate presentation and send one consolidated redline pass | Client pushes revisions to issuing bank before issuance | Operationally executable LC draft |

| 4. Run a go/pause gate | You | Confirm fee ownership, workload, and fallback path | Project starts only after internal approval | Margin-protected launch decision |

Qualify fit before contract language hardens#

Raise the LC before the contract is locked, not after. Talk to your bank before the client applies so the document requirements are workable before the LC is issued.

A simple script works well here: "Because this is cross-border and the payment exposure is material, I want a bank payment commitment tied to defined milestone documents. Before application, let's align on document requirements, fee ownership, and whether my bank is advising only or also confirming."

Move forward only if three checks pass: your client accepts LC use in principle, your bank can support the transaction, and milestone acceptance can be evidenced with objective documents. If the response is "we'll sort documents later," treat that as a pause signal.

Design documents the bank can actually examine#

This step determines whether payment will move smoothly. Banks examine documents, not the underlying service performance, so build the evidence pack before the applicant submits the LC request.

| Element | Define | Check |

|---|---|---|

| Artifact name | Exact artifact name, such as "Milestone Acceptance Certificate" | Document labels match what you can actually issue. |

| Signer or issuer | Whether applicant issuance or countersignature is required | Confirm signer authority. |

| Acceptance wording | Document-checkable, not subjective | Pause if acceptance language is subjective. |

| Presentation route and format | Channel and file format required by the credit and the receiving bank | Confirm the presentation route. |

| Rule set and timing | If UCP 600 is intended, make sure the LC text expressly incorporates it; raise presentation timing before issuance if the document set may take longer to assemble | UCP 600 applies only if the credit text says it does. |

For each milestone, define four things:

- Exact artifact name, such as "Milestone Acceptance Certificate."

- Signer or issuer, including whether applicant issuance or countersignature is required.

- Acceptance wording that is document-checkable, not subjective.

- Presentation channel and file format required by the credit and the receiving bank.

Before handoff, add two controls: confirm signer authority and confirm the presentation route. Unless the credit says otherwise, presentation can be made to a nominated bank or directly to the issuing bank, so specify your preferred route if operations depend on it.

If UCP 600 is intended, make sure the LC text expressly incorporates it. If your document set may take longer to assemble, raise presentation timing before issuance.

Stress-test the draft before issuance#

Once the buyer applies and the issuing bank drafts the credit, switch into review mode. This is not a quick read; it is your chance to catch discrepancies while they are still fixable.

Run one full stress test before issuance:

- Verify applicant and beneficiary names and addresses.

- Verify document labels match what you can actually issue.

- Check for internal contradictions in the terms.

- Simulate a live presentation. Can you submit every required document exactly as written, with the stated signer, format, and channel?

Escalate the predictable problem areas early: subjective acceptance language, unclear countersignature responsibility, conflicting timing language, or unconfirmed submission instructions. Send one consolidated redline set to the client for issuing-bank revision. Keeping it to one pass helps keep the decision binary: workable in practice, or not.

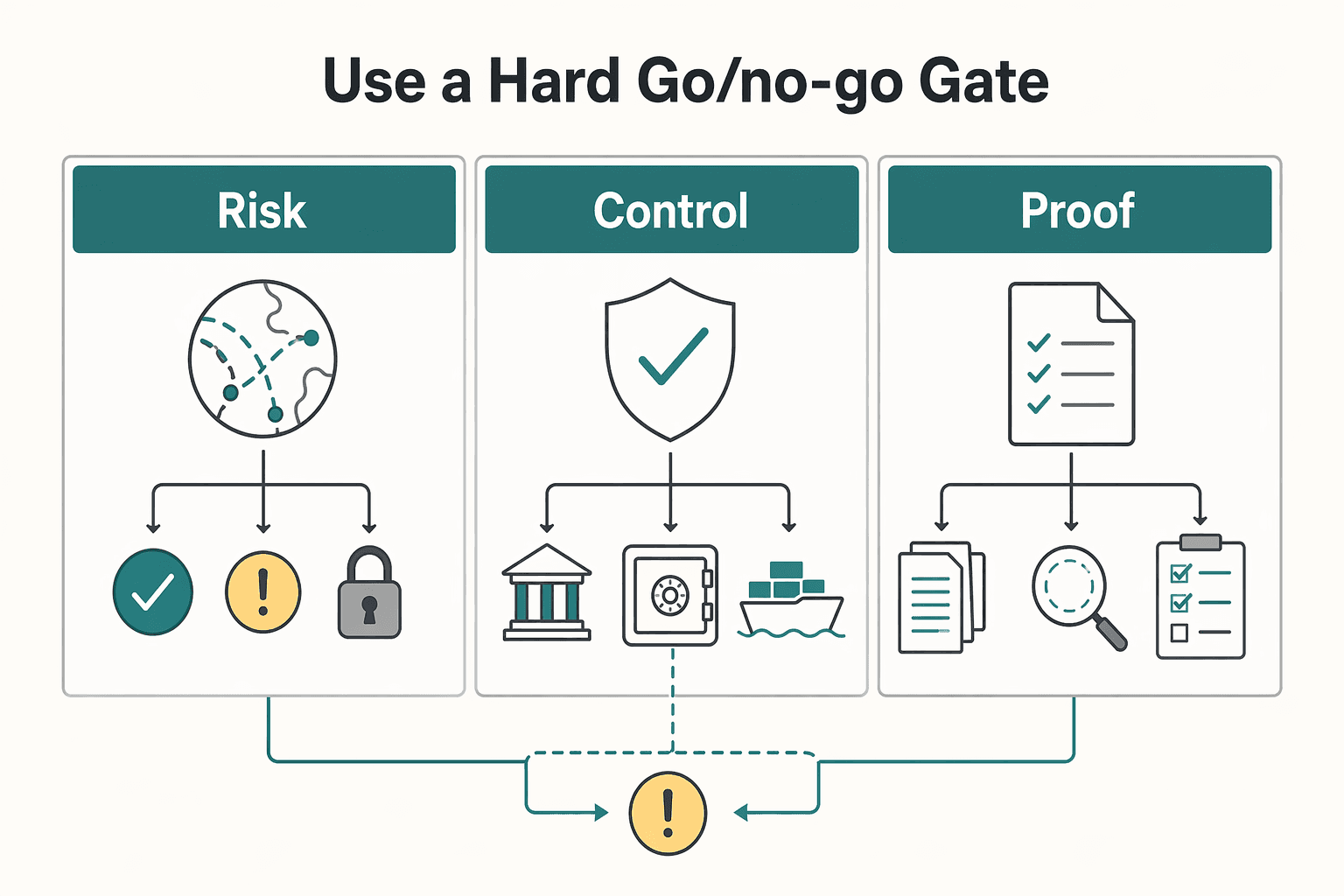

Run a real go/pause gate before kickoff#

An LC can improve payment security, but it still adds work and cost. The final decision should protect both execution and margin.

Go only if fee ownership is explicit, the process load is manageable for this deal, and the draft works without manual rescue. Pause if fees are unresolved, document terms are still subjective, or the admin burden is too high for the contract value.

If you still need a payment-control mechanism but the LC route is too heavy, switch early to A Guide to Using an Escrow Service for High-Value Projects. Related: How to use 'escrow' for a large freelance project payment.

When Does an LC Make Sense (And When Is It Overkill)?#

An LC makes sense when the downside is large enough to justify the extra process and fees. If trust risk is limited, the impact of a missed payment is manageable, or the payment trigger cannot be documented cleanly, it is usually more tool than you need.

Run this decision flow before proposal sign-off#

| Factor | What to ask | Article cue |

|---|---|---|

| Trust risk | Is buyer credit weak, unavailable, or unproven? Is the issuing-bank or country exposure a concern? | LCs are commonly used in higher-risk situations; a confirmed LC can add a second bank payment promise. |

| Downside severity | Would one missed payment materially disrupt payroll, reserves, or delivery capacity? | Use LC only if the downside is large enough to justify the extra process and fees. |

| Documentability | Can you prove the first milestone with exact document names, clear signer authority, and objective wording? | Payment turns on documents that comply on their face, not on a later performance debate. |

| Enforcement complexity | If a dispute happens, would cross-border enforcement be slow or impractical enough that a bank payment commitment materially changes your risk? | A bank payment commitment matters when enforcement is slow or impractical. |

| Timeline tolerance | Can the project plan absorb document examination time? | If the credit text expressly incorporates UCP 600, examination can run up to five banking days. |

- Trust risk

Is buyer credit weak, unavailable, or unproven? Is the issuing-bank or country exposure a concern? LCs are commonly used in higher-risk situations, and a confirmed LC can add a second bank payment promise when that exposure is the issue.

- Downside severity

Would one missed payment materially disrupt payroll, reserves, or delivery capacity? Keep any internal value trigger pending until it has been checked against current project risk, bank-cost, admin-capacity, and margin records before use.

- Documentability

Can you prove the first milestone with exact document names, clear signer authority, and objective wording? Payment turns on documents that comply on their face, not on a later performance debate.

- Enforcement complexity

If a dispute happens, would cross-border enforcement be slow or impractical enough that a bank payment commitment materially changes your risk?

- Timeline tolerance

Can the project plan absorb document examination time? If the credit text expressly incorporates UCP 600, examination can run up to five banking days. Under other governing rules, timing can differ.

A useful minimum test is this: can you complete a first-milestone presentation pack before contract lock? If it still depends on side emails, subjective acceptance language, or assumed signer authority, expect discrepancy cycles and resubmission.

Match the instrument to the trigger#

| Instrument | Payment trigger clarity | Operational load | Choose this when |

|---|---|---|---|

| Commercial LC | High when milestone documents are precisely defined | High | You expect routine milestone draws and can present compliant documents each time |

| SBLC | High for default or non-payment events when default evidence is clearly defined | Varies | You want a backup payment commitment, not documentary draws on every milestone |

| Documentary Collections or cash in advance | Varies by terms; no LC-style payment guarantee in documentary collections | Lower | Buyer trust is stronger, speed matters, or LC cost and process are too heavy for this deal |

Quick overkill check#

Some patterns are good reasons to stop and reassess: strong payment history with the buyer, small ticket size, urgent launch timing, subjective acceptance criteria, or fee and admin burden that compresses margin. Run one last check on total bank cost, internal admin hours, and your fallback path before you commit. Keep the internal trigger pending until it has been verified against current project risk, bank-cost, admin-capacity, and margin records before use; if process overhead worsens margin erosion, skip the LC.

If you want a deeper dive, read Separating Business and Personal Finances: An Important Step for LLCs.

If you are deciding between LC, escrow, or upfront terms, run the numbers before locking terms with the Payment Fee Comparison tool.

Beyond the Bank: Faster, Smarter Alternatives#

If the bank route feels too heavy, do not ask what the next-best product is. Ask what event releases cash, what evidence controls that release, and who keeps the leftover risk. If you are not using a full bank instrument, the signed terms need to answer those questions before you sign.

An SBLC gives you a document-based payment path through banks. Payment is tied to documentary evidence, such as invoices or certificates, and governing rules are often stated as UCP 600 or ISP98. Bank guarantees are typically framed as a more direct trigger path, often used for local projects, with frameworks such as URDG 758 or UNCITRAL rules alongside local law. For escrow and Merchant of Record setups, treat release mechanics, dispute handling, reversals, and payout conditions as contract items to verify, not assumptions.

| Option | Control point | Retained liability | Dispute evidence path | Operational burden |

|---|---|---|---|---|

| SBLC | Bank action against documents named in the instrument | Documentary-compliance obligations follow the instrument and contract terms | Presentation requirements in the instrument text; evidence can include invoices/certificates | Higher documentation and review burden |

| Bank Guarantee (BG) | Demand process set by the guarantee wording | Scope follows guarantee text and applicable law | Often less complex documentation at trigger than SBLC, but exact evidence is text-dependent | Often quicker trigger path for local-project use cases |

| Escrow | Defined by signed escrow terms (verify exact clause) | Do not assume risk transfer unless terms assign it | Verify which records control outcomes in the contract | Contract-dependent |

| Merchant of Record | Defined by provider contract terms (verify exact clause) | Do not assume risk transfer unless terms assign it | Verify what records the contract treats as controlling evidence | Contract-dependent |

Contract review checklist before signing#

Before you rely on any alternative, make the contract do the heavy lifting. Check these points before you sign:

- Release trigger: Define the exact event that unlocks funds. If the terms say "approval," also define who approves, what counts as approval, and whether silence becomes acceptance after a stated period.

- Dispute evidence: Name which records decide disputes and the order of precedence if records conflict.

- Responsibility scope: State which party handles losses, fees, and response work when reversals or disputes occur.

- Payout timing and holds: Lock in payout windows, hold or reserve rights, and pause conditions.

Run the scope gap test#

Use this as a hard checkpoint before contract lock. If any answer is "no," the unresolved obligation is still yours.

- Can you point to one clause that states exactly when money is released?

- Can you point to one clause that states what evidence controls a dispute outcome?

- Can you point to one clause that assigns reversal/dispute responsibilities?

If acceptance language, evidence hierarchy, or release timing are vague, disputes are harder to resolve. Bank instruments can fail the same way when document requirements are vague, so confirm review timing in the governing text rather than assuming it. In the SBLC/BG comparison provided, guarantor demand examination is described as generally seven business days.

If you want the lighter route, make the contract carry the weight before kickoff. A short pre-mortem on release, evidence, and retained liability can save cleanup later. We covered that implementation approach in How to Conduct a 'Pre-Mortem' to De-Risk a Large Freelance Project.

For a step-by-step walkthrough, see A Guide to Stripe Radar for Fraud Protection.

Take Control: Your Playbook for Fearless International Growth#

The practical rule is simple: use the lightest control that still protects the one failure you cannot absorb, then verify it at document level before kickoff. If you cannot point to the exact trigger, required artifacts, and artifact owner, you do not have payment security yet.

Name the one loss that would break this project#

Start with the failure, not the product label. If your core risk is non-payment after delivery, an LC can be justified. If your core risk is unclear acceptance, escrow terms usually matter more. If your core risk is payment operations scope, a MoR may fit better.

Be realistic about execution. An LC setup works only if you can produce documents exactly as required. Banks examine documents against credit terms. They do not assess service quality or delivery quality.

Match the option to the control point#

Once you know the failure you are protecting against, compare options by what releases funds, what evidence is required, who keeps the residual risk, and who owns the work.

| Option | Control point | Evidence burden | Residual risk you still carry | Operational ownership |

|---|---|---|---|---|

| LC | Bank action on a complying presentation under the instrument | High: documents must conform to instrument terms and any named governing rules | Discrepancy risk, expiry risk, and obligations outside instrument text | Shared across you, the buyer, and banks in the LC flow |

| Escrow | Buyer acceptance or inspection-period expiry under escrow terms | Medium: acceptance records, milestone proof, and dispute artifacts | Delay risk if acceptance language is vague, plus unassigned obligations | Shared across you, the buyer, and the escrow provider |

| Merchant of Record | Provider-controlled payment flow under its contract terms | Medium: provider-specific onboarding, scope, and dispute evidence | Anything not expressly assumed in contract scope | Provider for covered payment operations; you for remaining obligations |

A MoR is legally responsible for processing customer payments, and covered scope can include tax calculation, collection, and remittance. A PayFac is a different model, so do not treat those labels as interchangeable.

Verify execution details before you commit#

At this point, details decide whether the protection is real or only theoretical.

| Option | What to verify | Timing/mechanics |

|---|---|---|

| LC | The credit text controls; UCP 600 applies only if the credit expressly says so | Check that you can submit every required document as written before expiry; the UCP 600 five-banking-day period is an examination window after presentation, not a payment guarantee. |

| Escrow | Verify release and dispute clauses in the actual provider terms | In Escrow.com-style mechanics, release happens on buyer acceptance or inspection-period expiry; inspection periods can run 1 to 30 calendar days; disputes can include a 14-day negotiation period before arbitration steps. |

| Merchant of Record | Verify scope boundaries in the contract language | Reseller-style setups can involve two linked transactions, and the MoR name can appear on the customer statement; treat refunds, taxes, chargebacks, payout timing, and customer recourse as open items unless the contract clearly assigns them. |

For LC, the credit text controls. UCP 600 applies only if the credit expressly says so, and parties often reference the 2007 Revision (ICC Publication no. 600) when intended. Check that you can submit every required document as written before expiry, and run a pre-acceptance discrepancy check before you accept the LC. The UCP 600 five-banking-day period is an examination window after presentation, not a payment guarantee.

For escrow, verify release and dispute clauses in the actual provider terms. In Escrow.com-style mechanics, release happens on buyer acceptance or inspection-period expiry, and inspection periods can run 1 to 30 calendar days. Disputes can include a 14-day negotiation period before arbitration steps. Do not assume all providers use the same mechanics.

For MoR, verify scope boundaries in the contract language. In reseller-style setups, the flow can involve two linked transactions, and the MoR name can appear on the customer statement. Treat refunds, taxes, chargebacks, payout timing, and customer recourse as open items unless the contract clearly assigns them. A recent FTC settlement announcement is a reminder to scrutinize MoR boundary claims carefully.

Use a hard go/no-go gate#

Before kickoff, confirm all five items below:

- Trigger clause: Exact text that releases funds.

- Artifact list: Every required record, such as invoice, certificate, acceptance record, delivery log, or dispute evidence.

- Artifact owner: Who creates, signs, submits, and stores each artifact.

- Timing fit: Examination windows, expiry dates, inspection periods, and payout holds match your cash-flow reality.

- Residual-risk map: Unassigned obligations are explicitly identified as yours.

If any answer is no, pause. The best option is usually the one with the least process overhead that still controls your highest-impact failure. If escrow looks like the right middle path, read A Guide to Using an Escrow Service for High-Value Projects.

You might also find this useful: Using a Stability Report to apply for a UK mortgage as a freelancer with international clients. If you decide LC overhead is too high for this project, review a practical alternative workflow in Merchant of Record for freelancers.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- das.nebraska.gov/materiel/purchasing/6677/101867%20O4.pdftrusted

- ecfr.gov/current/title-12/chapter-III/subchapter-B/pa...trusted

- federalreserve.gov/frrs/regulations/section-20824-letters-of-cr...trusted

- ftc.gov/news-events/news/press-releases/2025/06/padd...trusted

- kitsap.gov/das/Documents/2024-012%20CKTP%20Solids%20and...trusted

- law.cornell.edu/ucc/5/5-108trusted

- legacy.export.gov/articletrusted

- trade.gov/letter-credittrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stop Freelance Profit Margin Erosion Before It Hits Cashflow

Revenue can hold steady while the business underneath it gets weaker. What comes in matters, but what you keep after the work is delivered is the clearer signal of health.

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

A Guide to Using an Escrow Service for High-Value Projects

**Treat escrow as your payment system, not a last-minute fix for overdue invoices.** On high-value projects, money risk usually shows up at handoff points like scope approval, milestone acceptance, and payout release. If you run a business of one, you need a get-paid system that works the same way on every deal, even when a client is in a hurry. This guide treats escrow as that repeatable system, so payment protection supports delivery, trust, and disciplined risk management from day one.