Quick Answer

Start by drafting one written multi-member llc operating agreement that fixes governing law, member authority, and tax handling before work begins in new locations. Define who collects Form W-9 records, who manages IRC 1446 withholding and Form 8813 payments, and who checks foreign state registration triggers. Then add deadlock, transfer, and buyout procedures with written notice and documentation rules so exits and disputes follow a preset process.

Why Standard Agreements Sabotage Global Partnerships#

If your partners live, work, or get paid across countries, a generic multi-member LLC operating agreement can fail on three assumptions: shared legal framework, shared tax exposure, and shared operating context. Templates are not automatically invalid, but they are often too generic for how the business actually runs.

| Assumption | Watch for this signal | Fix next |

|---|---|---|

| Shared legal framework | Your real rules live partly in Slack, email, or side conversations instead of one controlled agreement. | Align formation jurisdiction, governing-law language, and actual operating practice in one place. |

| Shared tax exposure | Incomplete partner tax documentation. | Assign who collects member tax forms, who handles withholding, and who files Form 8813 payments. |

| Shared operating context | Your agreement says you can operate anywhere but names no owner for registration checks. | Define where members can bind the company and who monitors foreign-registration obligations by state. |

Shared legal framework#

A one-size-fits-all legal setup is risky from day one because an LLC is created under state statute. Delaware gives broad freedom of contract in LLC agreements and treats an agreement broadly enough to include written, oral, or implied terms. Watch for this signal: your real rules live partly in Slack, email, or side conversations instead of one controlled agreement. Fix next: align formation jurisdiction, governing-law language, and actual operating practice in one place.

Shared tax exposure#

Tax treatment and withholding do not sort themselves out just because members agree on economics. A domestic LLC with two or more members defaults to partnership tax treatment unless it elects otherwise on Form 8832. If partnership income is effectively connected taxable income allocable to foreign partners, IRC 1446 withholding applies. Missing a Form W-9 or similar documentation means you must presume the partner is foreign for withholding purposes. Watch for this signal: incomplete partner tax documentation. Fix next: assign who collects member tax forms, who handles withholding, and who files Form 8813 payments.

Shared operating context#

Operating across states creates a gap that generic language often misses. State registration triggers are not identical. California requires qualification before transacting intrastate business, Delaware requires registration before doing business there, and New York provides an Application for Authority path for foreign LLCs. Watch for this signal: your agreement says you can operate "anywhere" but names no owner for registration checks. Fix next: define where members can bind the company and who monitors foreign-registration obligations by state.

| Generic template language | Cross-border-ready clause intent |

|---|---|

| "This agreement is governed by one state's law." | Name governing law, then assign responsibility for checking where additional state registration or local compliance may be triggered. |

| "Profits and losses are shared equally." | State tax classification, required partner documentation, withholding responsibility, and tax-distribution handling. |

| "The company may do business anywhere." | Define where members manage, sign, sell, or perform work, and who reviews registration requirements in those locations. |

Handle these three assumptions first. Then draft the agreement so those decisions hold up in real operations.

For a step-by-step walkthrough, see How to Create a Service Agreement for a SaaS Product.

The Foundational Architecture: Core Clauses for a Borderless Business#

Use one written operating agreement as the reference point for how the LLC is run. Keep it with the company records and use it in practice. If key rules stay in chat threads or verbal understandings, enforceability can weaken and dispute risk can rise over time.

Choose one written legal reference point#

Pick one written agreement and make it the document people actually use. Document the framework members will use for internal interpretation, and document where the records are maintained. This does not override every rule in every place you operate, but it gives everyone one shared starting point when interpretations conflict across jurisdictions.

If your LLC is formed in California, keep this explicit and in writing. The California materials provided here say LLCs must maintain a written operating agreement at formation. They also say written terms are needed to modify key statutory provisions like fiduciary duties, and that the agreement is kept internally rather than filed with the state. Without a properly drafted agreement, default California rules can apply.

Ask yourself: if a third party reviewed your file, would they find one current written agreement and know which terms control?

Define member authority, not just member roles#

Titles alone may not resolve who can act when a decision is contested. Use the written agreement to document authority and keep a clear internal record of key decisions.

Keep it practical:

- Who can act on behalf of the LLC

- What requires group approval

- Where final decisions are recorded

For cross-border operations, coordination across jurisdictions can still create interpretation and enforcement challenges, so do not rely on unwritten understandings for core authority decisions.

Make money rules explicit if multiple currencies are involved#

The materials here do not establish a universally required base currency, exchange-rate source, or conversion timing. If multiple currencies are involved, treat those items as internal policy choices, document them clearly, and apply them consistently.

Record contributions in one consistent format#

Use one consistent written format for contribution records and keep supporting documents with company records. The materials here do not establish one required valuation method for cash, IP, or services, so avoid vague or memory-based tracking.

Final check: can you match each recorded contribution to supporting documentation and a clear entry in company records without relying on memory?

The Decision-Making Engine: Architecting Operations Across Time Zones#

Your agreement should make routine decisions fast and major decisions explicit, even when members are spread across time zones. In practice, that means one clear governance section for management, meetings, and voting, plus a separate escalation path for transfer restrictions and push-pull provisions if an operating dispute becomes an ownership dispute.

Choose the management model you can run in real life#

Choose the model your team can actually run, not the one that only sounds sophisticated. A member-managed structure can fit when all members are active and decision volume is manageable. If you go that route, define guardrails up front: who can sign ordinary contracts, what requires a vote, and what happens when a member is unavailable.

A manager-managed structure can fit when execution needs speed, involvement is uneven, or overlap is limited. Treat this as a structural choice, not a wording tweak. Manager-managed and member-managed models are presented as separate agreement variants.

Two drafting checks help avoid predictable mistakes:

- Do not import corporate board logic by default. The commonly quoted Delaware Section 141(a) language is corporation-focused, not LLC authority language.

- Do not overbuild governance for a simple team. LLCs can support complex voting and succession terms, but many new LLCs are not complex in practice.

Quick test: could a bank, vendor, or counsel immediately identify who can bind the company on ordinary matters today?

Define the major-decision bucket before conflict#

A vague "members will vote" clause is not enough. Reserve formal voting for decisions that materially change ownership, risk, or control, then draft each category so real events map cleanly to the text.

| Reserved-matter element | What to specify |

|---|---|

| Trigger | Specify the trigger for each reserved matter. |

| Approval threshold | Define approval thresholds explicitly in your agreement. |

| Notice method | Specify the notice method for each reserved matter. |

| Decision record | State where the final written decision record is stored. |

Keep these drafting points open until the specific agreement and supporting records confirm the final terms:

- The excerpts do not provide a fixed list of major-decision categories or dollar limits.

- Define reserved matters and approval thresholds explicitly in your agreement.

- Where ownership disputes are possible, align escalation language with Article 8 transfer restrictions and push-pull provisions.

For each reserved matter, specify four items together: the trigger, approval threshold, notice method, and where the final written decision record is stored.

Match deadlock handling to trust level and dispute risk#

These materials do not identify one universally "best" deadlock method, and they do not provide state-by-state enforceability rules. Treat deadlock design as a drafting choice you should validate before finalizing.

| Mechanism | What this approach supports | What remains open |

|---|---|---|

| Push-pull under Article 8 | The model agreement outline includes transfer restrictions and push-pull provisions in Article 8. | Trigger design and enforcement specifics are not provided in the excerpts. |

| Any other tie-breaker process | No specific alternative method is prescribed in the excerpts. | Method selection and enforceability details are not provided in the excerpts. |

Use push-pull as an ownership-level backstop rather than an everyday operating tool. For more on exit mechanics, see How to Create a Buy-Sell Agreement for a Partnership.

Finalize mechanics and stress-test once#

Before you sign, test the agreement against one routine decision and one reserved matter. If you cannot answer who acts, how notice is sent, how long responses take, and what happens after silence or disagreement, the clause is still too abstract.

Implementation checklist:

- Authority map: who acts alone, who approves spend, who is backup.

- Vote workflow: how proposals are submitted, who can call votes, where final decisions are recorded.

- Notice method: accepted delivery channels for meetings and votes.

- Response window: the period stated in the specific agreement and checked against supporting records, not "promptly."

- Escalation path: order from internal vote to neutral process to Article 8 remedies.

With that in place, your governance terms start working like operating rules instead of theory. The next step is compliance, because authorization language and compliance obligations are separate. Related: What Happens to an LLC When a Member Dies?.

The Cross-Border Compliance Shield: Mitigating Your #1 Hidden Risk#

A clean vote and a valid signature may not protect you if the action creates tax or filing exposure in another country. Your operating agreement should treat cross-border compliance as a pre-action control, not cleanup after someone has already traveled, negotiated, signed, or started work abroad.

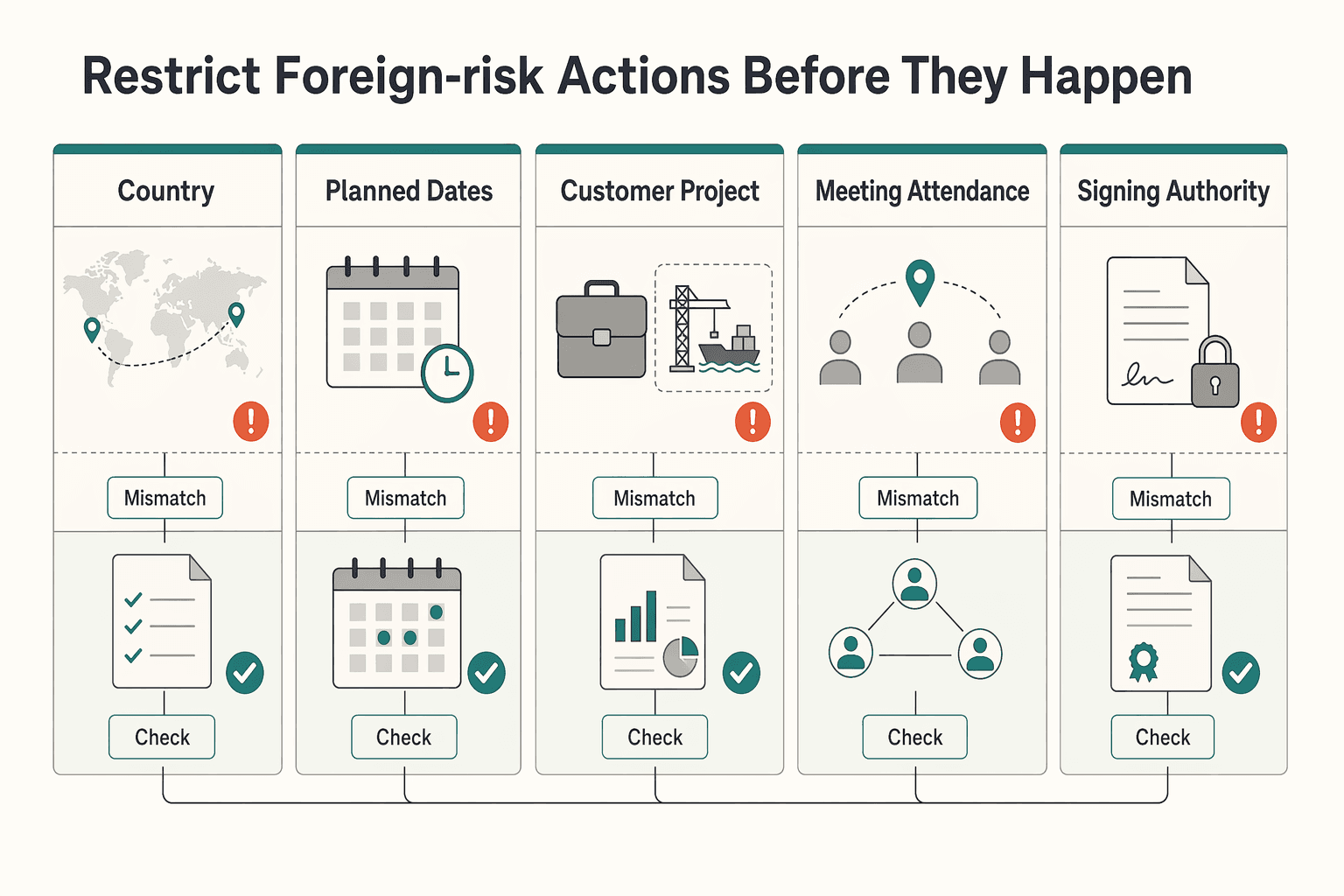

Restrict foreign-risk actions before they happen#

Treat potential cross-border tax exposure as an operating-control issue, not a legal memo pulled out after the fact. Draft the clause as a practical checklist that pauses actions that may create foreign nexus, registration, or PE exposure until the facts are reviewed.

| Fact pack item | Article wording |

|---|---|

| Country | country |

| Planned dates | planned dates |

| Customer or project | customer or project |

| Meeting attendance | who will attend meetings |

| Signing authority | who may sign |

| Local setup | whether a local address, bank account, or service provider will be used |

| Local advice | any local advice already received |

Your clause should combine four controls in one place:

- Restricted activities

- Written pre-approval

- A short fact pack

- Escalation to qualified counsel when the answer is unclear

Define restricted activities functionally and tie them to a clear approval workflow. Keep the language broad enough to catch risk, but specific enough that members know when pre-approval is required.

Require the approval request to include country, planned dates, customer or project, who will attend meetings, who may sign, whether a local address, bank account, or service provider will be used, and any local advice already received. Before you approve, confirm the designated reviewer has the fact pack and has decided whether outside counsel is required.

Authorize tax distributions with a stated method#

If the agreement authorizes tax distributions, say how they work and who approves them. Avoid a clause that only says "tax distributions may be made" without a defined process.

State who calculates proposed amounts, when they are considered, and how they interact with ordinary distributions. If cross-border facts are involved, require advisor review before you finalize the method and any rates or reserves.

Then define governance. State whether payment is mandatory when cash is available, discretionary, or subject to approval above a stated threshold. Also state whether tax distributions are advances against later distributions and when the calculation must be revisited.

Assign compliance ownership and document the evidence trail#

Compliance drifts when ownership is vague. Name one role to track filing obligations and one approving member or manager to review advisor deliverables before submission.

| Generic compliance wording | Operationally enforceable wording |

|---|---|

| "Members will comply with applicable laws." | "The Compliance Owner maintains the filing calendar, circulates upcoming obligations, and confirms completion in writing." |

| "The company may hire advisors." | "Advisor drafts are reviewed by the designated reviewer before filing, with comments and approval stored in the company records folder." |

| "Records will be maintained." | "Final filings, advisor memos, approvals, and official-source copies are stored in the company records repository under a dated folder structure." |

| "Delays should be addressed promptly." | "A missed or threatened deadline is reported to all members within the response window stated in the agreement, with a remediation plan and counsel escalation if timing is uncertain." |

Two operating rules make this enforceable. First, if you rely on a federal rule or notice, keep the official version in your records. FederalRegister.gov's XML display is informational and not the official legal edition, and the page says legal research should be verified against an official Federal Register edition. Also confirm whether the document is proposed or final before you treat it as binding. Second, preserve written request-and-response records. A written request followed by dated submission materials is a concrete checkpoint, and timing uncertainty is exactly when you should escalate before a deadline passes.

Use this clause review point to test member movement scenarios with the Tax Residency Tracker before you lock your final draft.

The Resilient Exit Protocol: Planning a Seamless Buyout Across Continents#

Lock the exit process in writing before anyone needs to leave. In a cross-border LLC, disputes can start when a real-world trigger appears and the agreement does not clearly say what happens next. Treat buyouts like an operating process, not an emergency negotiation.

Define trigger events in usable categories#

Use trigger categories members can actually administer. Tie them to observable events and to the governing-law topics your documents already touch, such as transfer, exchange, merger, or dissolution.

Write each trigger as an observable event, then tie it to a process. Keep the standard specific enough that you can apply it without debating intent.

Set a process flow for each trigger#

Once the triggers are clear, use a consistent process so no one is inventing procedure mid-dispute. For each trigger category, document the same four controls:

- Notice: how notice is given and to whom

- Documentation: what records must be provided

- Confirmation: which named role confirms the trigger

- Interim authority: what voting, account, and signing authority applies while the buyout is pending

Use named roles and written records so the trigger decision is auditable. If an exit changes the LLC's location or registered agent in Minnesota, file the required change of address or agent update with the Secretary of State.

Also keep a legal guardrail in mind. Delaware Chancery has described tension between private ordering and fiduciary accountability, and in that cited corporate-law context fiduciary tailoring is limited. Do not rely on broad waiver language to fix an unclear or uneven exit process.

Choose valuation mechanics before a dispute#

Do not wait for conflict to decide how the business will be valued. The grounding sources here do not require one valuation method, so choose your method explicitly and align it with your governing documents and governing law.

| Valuation approach | When it fits | Tradeoff | State-law checkpoint to insert |

|---|---|---|---|

| Formula-based | Predictable economics and members want speed | Efficient, but may feel off in unusual periods | Add a clause requiring review against governing law plus transfer/dissolution rules in your formation documents |

| Independent appraisal | Value is disputed or hard to model with one formula | More neutral process, but slower and costlier | Name appraiser selection and confirm the process does not conflict with governing-law constraints |

| Hybrid | Members want speed with a fairness backstop | More drafting complexity, fewer deadlocks | Set formula as default, appraisal as escalation, then cross-check both steps against governing-law limits |

Minnesota materials emphasize that LLC formation and operation are governed by state law, that transfer and dissolution are core topics, and that formation documents may modify many default rules. Your valuation clause should be checked against all three layers.

Make cross-border payment execution explicit#

Payout logistics should not be left to later emails. The grounding sources do not provide default state-law rules on settlement currency, exchange-rate lock timing, payment-rail fallback, fee allocation, or withholding splits for LLC buyouts. If cross-border payments are part of your deal, define those terms explicitly in the agreement.

Use a short implementation checklist#

Before finalizing, confirm the following:

- Trigger events are objective and scoped

- Notice, documentation, confirmation, and interim authority are written for each trigger

- Valuation method and escalation path are defined

- Governing-law and formation-document checks are built into the clause

- If cross-border payment terms apply, they are explicitly defined in the agreement

If you need deeper drafting patterns for exit mechanics, continue with How to Create a Buy-Sell Agreement for a Partnership.

The Dynamic Agreement: Why Your Playbook Must Be a Living Document#

Your agreement should change when the business changes. Keeping it current reduces uncertainty, keeps member relationships professional, and reinforces that the LLC is run as a separate legal entity rather than an informal arrangement. Use these four trigger types as a practical amendment framework:

| Trigger type | Primary risk area | Update scope in the agreement | Jurisdiction check (insert local advice) |

|---|---|---|---|

| Ownership transfer or member change | Governance, ownership | ownership percentages, transfer restrictions, profit-sharing and distribution terms, voting rights | Confirm tax and filing impact in each relevant jurisdiction |

| Leadership transition | Governance, operations | management authority, approval rules, signing authority | Confirm local governance and compliance implications |

| Major financing or capital structure change | Financial, governance | capital accounts, voting rights, dilution terms, transfer restrictions | Confirm lender-document constraints and local law alignment |

| Multi-entity expansion or restructuring | Governance, compliance | coordination across operating agreements, decision rights, reporting responsibilities | Confirm separate agreement and tax-filing obligations for each entity |

For each trigger, pre-define the same workflow so you are not inventing process under pressure:

- Notification and approvals: document who is informed and who approves amendments.

- Review pack: pull the current signed agreement and related ownership, financing, and compliance records.

- Drafting owner: name who prepares and circulates amendment redlines.

- Interim decisions: state what can be approved temporarily and what is paused until signatures are complete.

Then make amendment control visible. Your operating agreement should define procedures for meetings, voting, amendments, and dispute resolution, so use those procedures every time and maintain a version log with adoption date, change summary, and reviewed documents.

Implementation checklist:

- Assign one agreement owner.

- Create a version log and file-naming rule.

- Add these trigger categories to your agreement or governance policy.

- Pre-build a review-pack folder for ownership, finance, and governance records.

- Name the drafting owner and interim decision approver.

- If a trigger also changes exit mechanics, update those terms alongside this section and cross-check with How to Create a Buy-Sell Agreement for a Partnership.

Conclusion: From Legal Document to Strategic Asset#

An operating agreement becomes a strategic asset when you use it as a live governance document, not a one-time document. It controls how the LLC is organized, operated, and managed, including who can make decisions, how ownership transfers work, and how member disputes are handled.

In practice, the sections above work best together. Decision rules guide daily approvals, updates keep terms current as circumstances change, transfer terms cover ownership changes, and the review process keeps the agreement aligned with current reality. The point is not to predict every issue. It is to decide key rules before pressure makes decisions harder.

What to do next:

- Run a clause gap check using your latest signed agreement, written amendments, ownership records, and any joinder agreements for newer members.

- Assign one clear owner for agreement updates so changes do not stall.

- Schedule your next review check now, and if circumstances have changed, complete amendments in writing and have all members execute them.

Frequently Asked Questions

How does an operating agreement handle members in different countries?

Use the agreement as the written record for ownership, management roles, voting rights, and dispute resolution, then keep it aligned with how the business actually operates. Regularly verify stated ownership against reality and record member changes in meeting minutes or an amended agreement. If you include jurisdiction-specific legal or tax terms, validate them before relying on them. Cross-border friction can increase when written terms and day-to-day conduct stop matching.

What clauses are essential for a remote-first multi-member LLC?

Start with the clauses that control execution: management authority, voting process, and dispute process. Then add documentation controls, including ownership updates in minutes or amendments and capital account reconciliation before K-1 preparation. Remote teams often run into problems at handoffs and records, not at intent. Have local counsel and your tax advisor confirm the final language for your jurisdictions and filing setup.

Can a US citizen and a non-US citizen form a multi-member LLC?

A US citizen and a non-US citizen may be able to form a multi-member LLC, but the setup has to match the actual ownership, tax classification, and filing records. If a non-US member is involved, verify foreign-status details, withholding details, and the filing setup in the specific agreement and official/source records before use. Classification or documentation errors can create avoidable rework.

How do you structure a buy-sell agreement for nomadic partners?

Keep transfer terms tied to documented ownership mechanics. At minimum, define how transfers are approved and recorded, and make sure ownership records are updated in writing through minutes and/or an amended agreement. Unclear transfer paperwork can become a failure point during exits. Have local counsel and your tax advisor review enforceability and tax treatment before execution.

What is a tie-breaker clause and why do 50/50 partnerships need one?

A tie-breaker clause is a pre-agreed deadlock path so decisions do not stall when votes split evenly. Write down when it triggers, who initiates it, and what decisions it covers so the process stays usable under pressure. Unresolved deadlock can delay contracts, spending, and filings. Because procedure and enforceability vary by jurisdiction, have local counsel confirm the final tie-breaker structure.

How do you handle multiple currencies in an LLC operating agreement?

The provided materials do not set a required base currency, FX methodology, or rate source, so treat those items as jurisdiction- and advisor-dependent. Keep capital accounts reconcilable using one consistent documented method: beginning balance + contributions + income - losses - distributions = ending balance. Inconsistent conversion treatment can distort member balances, and distributions above basis are described as taxable gain. Confirm currency and tax treatment details with your accountant and local counsel before finalizing. When your agreement is finalized and you need compliant execution for cross-border member payments, explore Payouts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- courts.delaware.gov/Opinions/Download.aspxtrusted

- courts.delaware.gov/Opinions/Download.aspxtrusted

- delcode.delaware.gov/title6/c018/sc09/index.htmltrusted

- delcode.delaware.gov/title6/c018/sc01/index.htmltrusted

- dos.ny.gov/application-authority-foreign-limited-liabil...trusted

- downloads.regulations.gov/DOT-OST-2021-0046-0052/attachment_1.pdftrusted

- federalregister.gov/documents/2021/12/08/2021-26548/beneficial-o...trusted

- irs.gov/individuals/international-taxpayers/partners...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

How to Create a Buy-Sell Agreement for a Partnership

**Treat your buy-sell agreement for partnership as core operating infrastructure, not paperwork for later.** Freelancers and consultants move fast on client delivery, but shared ownership risk keeps running in the background until one partner leaves, becomes disabled, goes bankrupt, or goes through a divorce.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.