Quick Answer

Remote freelancers and independent contractors usually are not covered by a client's workers' compensation policy. Because you are treated as a separate business entity, you generally need your own protection, often through Occupational Accident Insurance or, in some cases, a formal workers' comp policy through your own business structure. Strong contracts also help limit liability and clarify responsibility.

The shift from anxiety to advantage starts with dismantling one dangerous assumption many remote professionals make: that in a crisis, a client's insurance will protect them. That belief creates a serious risk hiding in plain sight. To build a resilient career, you first need to understand the legal and financial wall that separates you from a traditional employee.

The Critical Distinction: You Are a Business, Not an Employee#

Let's be direct. The law does not see you as an extension of your client's team; it sees you as a separate business entity. This is the core principle behind your classification as a 1099 independent contractor versus a W-2 employee.

- A W-2 employee operates under the direct control of the company. The employer dictates their hours, manages their workflow, provides their tools, and, importantly, withholds taxes and pays for protections like unemployment and workers' compensation insurance. They are inside the company's protective bubble.

- A 1099 independent contractor is a "Business-of-One." You provide services to clients, control how and when you perform the work, and are responsible for your own taxes, tools, and benefits. You are a vendor, operating outside that bubble.

Thinking you are covered by a client's workers' compensation policy is like expecting their health insurance to cover your doctor's visits - it is a structural impossibility.

Your Client's Policy is Not Your Safety Net#

State laws do not require businesses to provide workers' compensation for independent contractors. These policies are designed to cover a company's legal responsibility to its employees. Premiums are calculated based on W-2 payroll and the associated risks of those jobs. Including a vendor like you would violate the terms of the policy and misrepresent the risk to the insurer. In practice, relying on a client's coverage means being left unprotected when something goes wrong.

The Catastrophic Risk Scenario#

Imagine this: you're a software developer working for a San Francisco-based client from your apartment in Lisbon. After months of intense coding, you develop a severe case of carpal tunnel syndrome. Your doctor says you need surgery and months of physical therapy, making it impossible to type - and therefore impossible to work.

Suddenly, you have no income. Medical bills are piling up. Who pays?

- Your client? No. Their workers' compensation explicitly excludes you. They will express sympathy, but legally, your injury is not their liability.

- Your personal health insurance? Probably not. Many health insurance policies explicitly exclude work-related injuries, expecting workers' comp to cover those costs. Even if they initially cover some medical bills, they may later seek reimbursement from you once the injury is determined to be work-related. Personal health insurance will also do nothing to replace your lost income during recovery.

You are left to face a career-threatening injury with devastating financial consequences. That is the stark reality of personal liability for a remote "Business-of-One."

The Misclassification Minefield#

"But my client treats me like an employee," you might argue. This is a common and dangerous gray area. While worker misclassification exposes your client to significant legal and financial penalties - like back taxes, fines, and liability for unpaid insurance premiums - it is not a safety net you can depend on. For the contractor, being misclassified can mean you are denied critical protections like minimum wage, overtime pay, and anti-discrimination laws.

A legal battle to prove you were a de facto employee is costly, slow, and uncertain - exactly what you do not need in the middle of a medical crisis. If the relationship is already blurry, What to Do If You've Been Misclassified as an Independent Contractor is the next issue to sort before you assume any client policy will protect you. Securing your own coverage early draws a bright, unambiguous line that reinforces your independent contractor status. It protects you and shows clients that you are a low-risk, professional partner.

Your Personal Shield: Choosing the Right Insurance for Your 'Business-of-One'#

Once you accept that you need your own coverage, the next question is practical: what policy actually fits your business? This is not just about buying insurance. It is about choosing coverage that protects your income and health without taking on the complexity or cost built for traditional companies.

The Contractor's Go-To: Occupational Accident Insurance (OAI)#

For the vast majority of independent contractors, the answer is Occupational Accident Insurance (OAI). Think of OAI as a workers' compensation equivalent built specifically for the "Business-of-One." It's a personal, portable safety net that you own and control, and it moves with you from one client project to the next.

A strong OAI policy typically covers the essentials that keep an injury from turning into a financial crisis:

- Medical Expenses: Covers the costs of hospital visits, surgeries, and medication resulting from a work-related injury.

- Disability Benefits: This is the most important component. If an injury prevents you from working, OAI provides income replacement to cover your bills while you recover.

- Death Benefits: In a worst-case scenario, it provides compensation to your designated beneficiaries.

Because independent contractors are generally not eligible for state-mandated workers' comp, OAI fills that dangerous protection gap.

OAI vs. Traditional Workers' Comp#

Choosing between OAI and a traditional workers' compensation policy requires understanding their different purposes. OAI is often more affordable and accessible for a solo professional, while traditional workers' comp may be required by certain enterprise clients or state laws.

Here's a direct comparison to guide your decision:

| Feature | Occupational Accident Insurance (OAI) | Traditional Workers' Compensation |

|---|---|---|

| Primary User | Independent Contractors (1099) & Gig Workers. | W-2 Employees of a Company. |

| Cost | Generally more affordable, often with flexible payment options. | More expensive; premiums are based on company payroll and risk codes. |

| Coverage | Covers medical, disability, and death benefits up to a set policy limit. | Coverage is mandated by state law and is typically more comprehensive, with fewer limits on medical care. |

| Legal Status | An optional, private insurance product. | A state-regulated, legally mandated insurance for employers. |

| Portability | Fully portable; it belongs to you regardless of your current client. | Tied to the employer; coverage ends when employment terminates. |

The Strategic S-Corp Option#

For high-earning remote professionals, forming an S-Corporation can be a strategic move. By structuring your business as an S-Corp, you can legally classify yourself as an "employee" and pay yourself a formal salary.

That change can materially affect your insurance options. As an employee of your own company, you become eligible to purchase a formal workers' compensation policy for yourself. While it may be more expensive than OAI, it solves a major compliance headache. Many large enterprise clients, bound by strict internal risk-management protocols, will not engage contractors who cannot provide a Certificate of Insurance for a state-recognized workers' comp policy. Adopting this structure signals that you run a low-risk business and can open the door to corporate contracts.

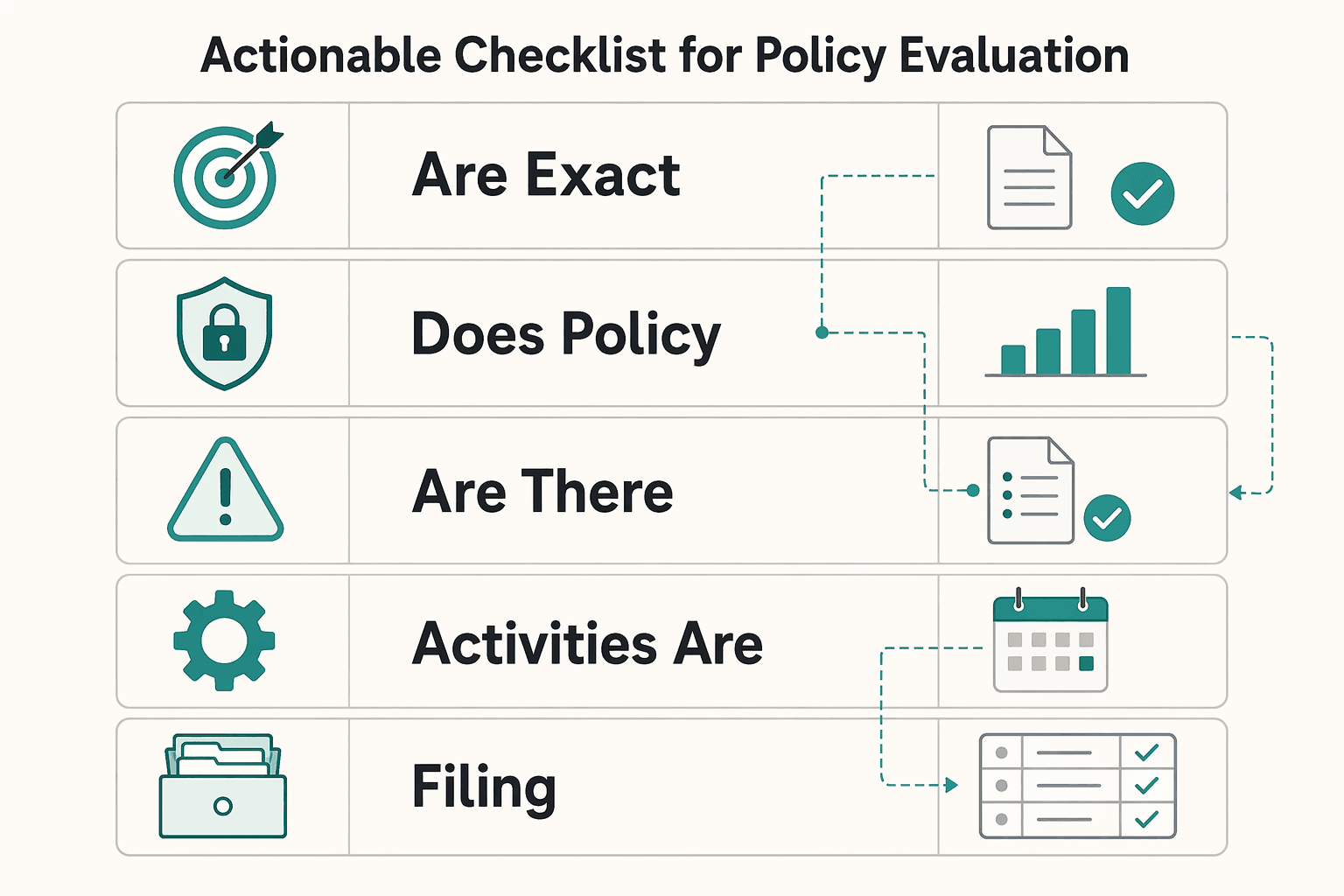

Actionable Checklist for Policy Evaluation#

Don't buy insurance blindly. The fine print matters. Use this checklist to evaluate any OAI or workers' comp policy before you commit:

| Check | Confirm | Detail |

|---|---|---|

| Disability coverage limits | Specific weekly or monthly payout amount | Maximum duration of payments |

| Home office injuries | Policy explicitly covers injuries in a home office | Addresses ergonomic injuries and common home-based accidents |

| Geographical restrictions | Coverage from your home base | Coverage from a temporary residence abroad |

| Excluded activities | Exclusions related to your specific profession | Exclusions related to your lifestyle |

| Claim process | Steps and required documentation | Expected timeline |

- What are the exact disability coverage limits? Ask for the specific weekly or monthly payout amount and, just as importantly, the maximum duration of those payments. Your income replacement is your lifeline.

- Does the policy explicitly cover injuries in a home office? Make sure the policy language addresses ergonomic injuries, like carpal tunnel, and common home-based accidents.

- Are there geographical restrictions? For the global professional, this is non-negotiable. Confirm that you are covered whether you're working from your home base or a temporary residence abroad.

- What activities are excluded? Scrutinize the policy for any exclusions related to your specific profession or lifestyle that could render your coverage useless.

- What is the process for filing a claim? Understand the steps, required documentation, and expected timeline. In a crisis, you need clarity, not confusion.

Beyond Insurance: Fortifying Your Contracts to Limit Liability#

Insurance helps after something goes wrong. Your client contract helps keep disputes from starting in the first place. Treat the Master Service Agreement as more than a formality; it is a core risk-management document.

The Power of an Indemnification Clause#

Start by assigning responsibility clearly. A well-drafted indemnification clause, sometimes called a "hold harmless" clause, is a cornerstone of professional contracting. In plain terms, it clarifies that you are responsible for your own work and actions. It also legally obligates your client to cover costs if their negligence, faulty equipment, or bad instructions cause harm. This helps prevent you from being held liable for a crisis you didn't create, providing a critical layer of protection that works in tandem with your own insurance policy.

Capping Your Financial Risk#

Beyond assigning fault, you need to contain your total financial exposure. Without a specific contractual limit, a single client dispute - justified or not - could theoretically put all of your business and personal assets at risk. This is where the Limitation of Liability clause becomes one of the most important sentences in your entire agreement. It sets a sensible, absolute cap on the amount of money a client can seek in damages.

A limitation of liability clause caps the amount of money one party must pay the other if losses arise from a breach of contract or certain other events. Without such a clause, there may be no financial limit on the damages a party can seek. For a "Business-of-One," this is not just legalese; it's a financial firewall.

Defining the "Scope of Work" to Mitigate Injury Risk#

One of the most overlooked tools for managing liability is the Scope of Work (SOW) section. A vague SOW is a breeding ground for disputes. You should use it to clearly define not just your deliverables, but also the boundaries of your work environment and duties.

- Specify Your Environment: State that work will be performed from your home office, using your own equipment.

- Outline Your Duties: Be specific about the tasks included. This creates a clear record of what is officially "work-related."

- Establish Boundaries: This detail helps legally distinguish between a legitimate work injury and a personal accident that happens to occur at home. If you trip in your kitchen outside of defined work activities, a precise SOW helps make it clear that it's not a work-related incident, protecting both you and your client from ambiguity.

Negotiating Like a Professional, Not an Adversary#

Introducing these clauses to a client does not have to be confrontational. The key is to frame them as standard business practice that ensures mutual protection and clarity. This approach elevates your status from a simple freelancer to a professional business partner.

When you present your contract, use collaborative and confident language:

"My standard agreement includes a few clauses for mutual protection, like indemnification and a limitation of liability. This is typical for my business-to-business engagements and helps make sure we both have clear expectations and safeguards in place, so we can focus entirely on the great work we'll be doing together."

This positions you as a prudent, low-risk partner - someone who manages their business affairs with the same precision they bring to their client work.

How Proactive Risk Management Becomes Your Competitive Advantage#

Being seen as a prudent, low-risk partner is more than a negotiating tactic. It can become a real competitive advantage. Every step you take to manage your own liability - from tightening your contracts to securing the right insurance - sends a clear signal to the marketplace. You are not simply a talented individual for hire; you are a professional, resilient business entity. High-value clients, particularly enterprise-level organizations, are not just buying your skills. They are also buying peace of mind.

Weaponizing Your Certificate of Insurance (COI)#

One of the most useful tools you have is the Certificate of Insurance (COI). A COI is a simple, one-page document from your insurer that proves you have active coverage, detailing the policy type, coverage limits, and effective dates. While many contractors wait to be asked for this, the strategic move is to provide it early during the proposal or final negotiation stage.

Think about the message this sends. You are instantly answering a critical, often unasked, question for their legal and risk teams: "Is this contractor a potential liability?" By presenting your COI upfront, you demonstrate foresight and immediately differentiate yourself from competitors who may appear less prepared. It is tangible evidence that you manage your business professionally, turning a routine compliance document into an early trust signal.

Justifying Your Premium Rates#

When a potential client sees that you carry your own workers' compensation or occupational accident insurance, they see a partner who has taken financial responsibility for their own risk. It lowers the risk of the engagement for them. They do not have to worry about misclassification risks or the potential for liability claims stemming from your work.

That reduction in risk has real value. It gives you a solid basis for your premium rates. You are no longer just billing for hours or deliverables; you are billing for the added value of a safe, secure, and professional engagement. You can justify higher fees because the client is receiving more than just your expertise - they are receiving a partnership with a well-run, low-risk business.

Building a Resilient Career#

In the end, taking control of your own safety net severs your financial well-being from the ambiguity of any single client's policies. By building your own protection through strong contracts and personal insurance, you create a career that can withstand uncertainty. That is the goal of the "Business-of-One": a resilient career built on control, foresight, and clear boundaries.

Conclusion: From Compliance Anxiety to Professional Confidence#

That burden of proof is the core problem. If you wait until after an injury to sort out whether you are covered, you are already in a defensive, uncertain position. The better move is to build a business structure that answers those questions in advance. That is the shift: stop treating workers' compensation as a client's problem and start treating your own coverage as part of running your business.

Your insurance policy - whether it's a strong Occupational Accident plan or a formal workers' comp policy for your business of one - is the financial safety net underneath your work. It helps make sure that a slip in your home office or a repetitive strain injury does not lead to a catastrophic financial collapse, allowing you to focus on recovery instead of bills and lost income.

But insurance is only one layer. Your contracts matter just as much. By embedding precise indemnification and liability clauses, you are not creating conflict; you are creating clarity. You are defining the boundaries of the engagement, which protects both you and your client from ambiguity. In practice, that is what moves you from a simple freelancer to a low-risk, high-value business partner.

In the end, this process is an investment in career resilience. By taking deliberate control of your liability, you decouple your financial well-being from any single client's policies or interpretations. You build a "Business-of-One" that is durable, secure, and prepared for the unexpected.

Frequently Asked Questions

As a remote freelancer, am I covered by my client's workers' comp?

Almost certainly not. A client's workers' compensation policy is designed to cover that company's W-2 employees, not independent contractors. As a 1099 worker, you are treated as a separate business entity.

Do independent contractors need their own workers' compensation insurance?

Usually yes for practical reasons, even if the law may not require it for a self-employed person with no employees. Larger clients often require contractors to carry their own coverage. Your own policy also protects your income if you are injured and your personal health insurance excludes work-related injuries.

What is the difference between workers' comp for employees vs. contractors?

For employees, the employer buys and provides workers' compensation coverage. For contractors, the contractor is responsible for securing their own protection. Employees receive state-regulated benefits through the employer's policy, while contractors usually need a private policy that offers similar protection.

How can a remote contractor mitigate injury liability in their client contracts?

Use your Master Service Agreement to create clear legal boundaries. An indemnification clause helps assign responsibility between you and the client, and a limitation of liability clause caps your financial exposure. A clear scope of work also helps distinguish work-related activity from personal activity at home.

What is Occupational Accident Insurance and how does it differ from workers' comp?

Occupational Accident Insurance is a private policy designed for independent contractors who are not covered by state-mandated workers' comp. It can cover work-related medical expenses, disability benefits, and death benefits, often with more flexibility and lower cost. Traditional workers' compensation is generally more complete and may be required by some clients or state rules.

If I form an LLC or S-Corp, do I still need workers' comp for myself?

It depends on state law and how your entity is structured. In some cases, a sole owner may be able to exclude themselves from workers' comp requirements, but that also means giving up coverage for their own injury. Many business owners still choose coverage to protect against medical bills and lost wages.

What kind of home-office injuries are typically covered by these policies?

Coverage usually depends on whether the injury arose out of and in the course of work. Common examples include repetitive strain injuries like carpal tunnel syndrome, falls in a designated home office while performing a work task, and some injuries during normal work breaks. The remote worker generally must show the injury was directly related to job duties.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- beta.dol.gov/policy-regulations/pay-benefits/workplace-in...trusted

- dir.ca.gov/dwc/employer.htmtrusted

- dir.ca.gov/dlse/california_equal_pay_act.htmtrusted

- dol.gov/agencies/owcp/procedure-manual/owcpBulletinstrusted

- dol.gov/agencies/whd/fact-sheets/13-flsa-employment-...trusted

- federalregister.gov/documents/2024/01/10/2024-00067/employee-or-...trusted

- federalregister.gov/documents/2024/01/10/2024-00067/employee-or-...trusted

- fordlibrarymuseum.gov/sites/default/files/pdf_documents/library/do...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

How to Handle Payroll Taxes for a Remote US Team

Use a risk-first setup before your first run. Put decisions and verification in a fixed order so payroll tax mistakes are less likely to turn into cashflow problems.