Quick Answer

To set up a US LLC as an Australian SaaS founder, first confirm your Australian baseline: you are carrying on an enterprise in your own right, the activity is not employee activity, and your ABN position is clear. Do not treat the LLC decision as final until that baseline is settled. Then choose a state by intent, verify provider scope in writing, and set up monthly records and an annual filing pack.

Stage 1: Assess - Is a US LLC Your Winning Move?#

Start here: do not treat this as a final US entity decision until your Australian baseline is clear. This material helps you confirm sole trader status and ABN entitlement. It does not support a hard recommendation on whether an LLC or Delaware C-Corp is the better choice.

Step 1. Confirm your current legal baseline#

Before you compare US structures, settle your current position first. Check these points:

- You are operating as a sole trader only if you are the only owner.

- As a sole trader, you are legally responsible for all business aspects, including debts.

- You are entitled to an ABN if you are carrying on an enterprise.

- You are not entitled to an ABN for activity performed as an employee.

- You can employ other workers, but you cannot employ yourself.

If any part of that is unclear, fix it before you layer a US entity decision on top.

Step 2. Keep LLC vs Delaware C-Corp as an open question for now#

At this stage, separate what you can verify now from what you cannot:

| Decision criterion | What you can verify now | What this section cannot prove |

|---|---|---|

| Funding path | Whether you are carrying on an enterprise in your own right | Whether LLC or Delaware C-Corp is better for future funding |

| Ownership flexibility | Whether you are currently a single owner (sole trader baseline) | How each US structure handles future owners or investor rights |

| Admin burden | Whether the activity is your own enterprise activity or employee activity | Which US structure is lighter to run |

| Future conversion complexity | Whether your ABN position for the current activity is clear | How hard or costly later conversion would be |

Step 3. Use a readiness checklist#

Do not move into formation just because the idea sounds sensible. Keep assessing only when the baseline facts line up.

| Status | Condition |

|---|---|

| Ready to continue | You are carrying on an enterprise in your own right. |

| Ready to continue | The activity is not employee activity. |

| Ready to continue | You can name the specific problem your current structure is not solving. |

| Likely too early | You cannot show clear enterprise activity. |

| Likely too early | Your setup still looks like employee work for that activity. |

| Likely too early | Your sole trader or ABN position for that activity is still unclear. |

In practice, continue only if all three "Ready to continue" conditions apply. If any "Likely too early" condition applies, pause here.

Step 4. Treat "benefits" as testable hypotheses#

Claims about procurement, contracting, or payments are not established in this material. Treat them as hypotheses to test, not conclusions.

| Potential benefit label | Plain-language meaning | Operational upside if true | Caveat |

|---|---|---|---|

| Procurement confidence | A claim that buyers may feel more comfortable with your contracting setup | Unknown from this material | Not established by this material |

| Contracting comfort | A claim that counterparties may be more willing to sign | Unknown from this material | Not established by this material |

| Payment operations | A claim that billing and collection may be easier for counterparties | Unknown from this material | Not established by this material |

If your Australian baseline is clean, move to the next stage. If it is not, pause and resolve classification and ABN position first.

If you want a deeper dive, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

Stage 2: Execute - The Step-by-Step Formation Playbook#

Do not execute until Stage 1 is internally consistent. This material supports your Australian baseline checks only; it does not verify specific US formation rules.

Step 1. Confirm your baseline before you buy support#

Before you pay a provider, lock down what is already verified:

- You are carrying on an enterprise in your own right.

- The activity is not employee activity.

- If you are a sole trader, you are the only owner.

- If you are a sole trader, you are legally responsible for business debts.

- You can employ other workers, but you cannot employ yourself.

- If you are carrying on an enterprise, you are entitled to an ABN.

Use this quick pre-file checklist:

- ABN status, or the ABN application basis

- One-line description of your enterprise activity

- Note confirming this is not employee activity

- Note confirming whether you are still the only owner

If those four points do not align, stop and resolve that first.

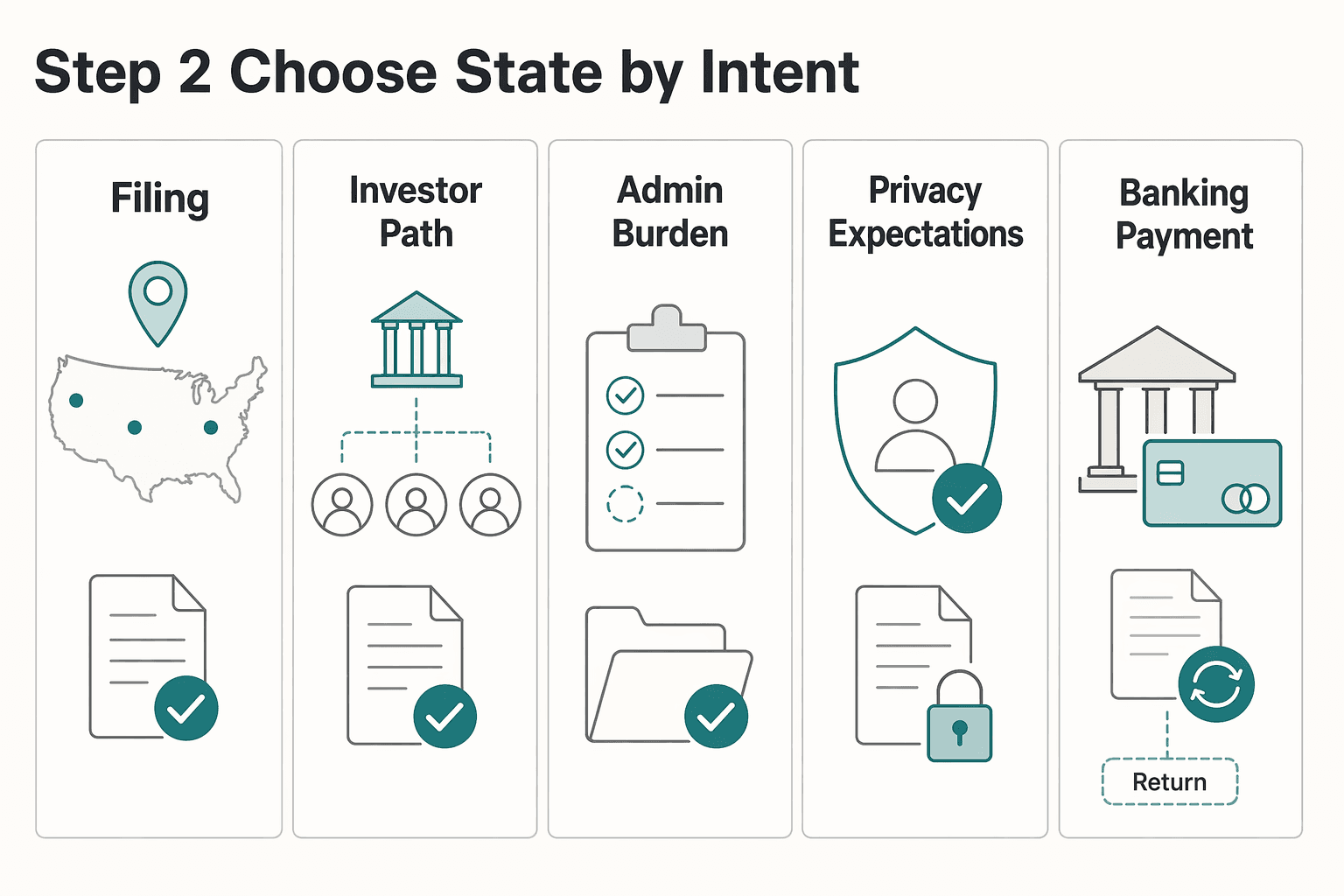

Step 2. Choose state by intent, then verify details#

State choice should follow your actual plan, not habit or marketing. Use this matrix to structure the decision, then fill it with current verified data from your own providers or counsel.

| Founder intent | What to verify before choosing | Delaware (verify separately) | Wyoming (verify separately) |

|---|---|---|---|

| Bootstrapped operations | Current fees, ongoing filings, practical admin load | Pending written verification from provider or counsel. | Pending written verification from provider or counsel. |

| Investor path | Whether your likely counsel or investors require a specific state | Pending written verification from provider or counsel. | Pending written verification from provider or counsel. |

| Admin burden | Who handles recurring compliance work | Pending written verification from provider or counsel. | Pending written verification from provider or counsel. |

| Privacy expectations | What ownership details are public vs private | Pending written verification from provider or counsel. | Pending written verification from provider or counsel. |

| Banking/payment compatibility | Requirements from your chosen bank or processor | Pending written verification from provider or counsel. | Pending written verification from provider or counsel. |

Decision rule: pick the state only after you can state your primary reason in one sentence and support it with verified current details.

Step 3. Compare formation support by scope, not branding#

Branding is not the right filter here. Focus on scope, responsibility, and what still sits with you after filing.

| Term | Get in writing |

|---|---|

| Registered Agent | What it is; who prepares it; who signs it; what ongoing responsibility it creates for you |

| Articles of Organization | What it is; who prepares it; who signs it; what ongoing responsibility it creates for you |

| Operating Agreement | What it is; who prepares it; who signs it; what ongoing responsibility it creates for you |

| EIN | What it is; who prepares it; who signs it; what ongoing responsibility it creates for you |

Ask each provider for written scope covering:

- What they do

- What you must do

- What they prepare

- What you sign

- What support continues after filing

For terms like Registered Agent, Articles of Organization, Operating Agreement, and EIN, get four plain-language answers in writing:

- What it is

- Who prepares it

- Who signs it

- What ongoing responsibility it creates for you

Escalate to legal or tax counsel if your baseline is unclear. For example, do it if ownership is uncertain, part of the activity looks like employee work, or your ABN basis is not clear.

Step 4. Runbook for your next actions#

Once you have chosen support, document the sequence your provider requires and keep every confirmation. This material does not confirm a universal US order, so treat the sequence below as checkpoints to verify with your provider:

- Formation filing requirements

- Whether an EIN step applies

- Banking setup requirements

- Payment rails setup requirements

Keep a document-prep checklist:

- Your ABN details

- Evidence of your current enterprise activity

- Your identification documents

- Every document and approval your provider issues

Risk note: requirements can differ by provider and can change over time. Confirm current requirements directly with each provider in writing and store those confirmations with your formation file.

Related: A Guide to Tax Residency in Australia for Digital Nomads.

Before you activate billing, confirm which onboarding tax paperwork your providers require so setup does not stall later: W-8 Form Generator.

Stage 3: Operate - Managing Your Global Business#

Formation is only the start. Once the entity is live, it stays useful only if your operations are consistent, clearly labeled, and easy to review. The practical routine is simple: document cash movement clearly, close records on a fixed cadence, and keep a verification file ready before filing season.

Step 1. Label founder-company money movement before it happens#

To reduce ambiguity, treat every transfer between you and the business as its own tracked item, not part of day-to-day sales or expenses.

Keep a separate owner transaction register with the date, amount, account reference, and purpose for each movement. For terms that are often interpreted differently, get written definitions from your adviser before year-end.

Ask them to define exactly how they want you to label:

- money you put into the business

- money you take out

- any payment they treat differently from those two categories

Do the same for terms like "disregarded entity treatment," "pro-forma filing," and "reportable transaction." If a provider cannot map those labels to the forms they prepare, pause. Get written clarification before you keep going.

Step 2. Run a two-view bookkeeping routine with monthly checkpoints#

Use monthly closes to keep records consistent. Keep one operating record for day-to-day activity and one reporting view your adviser can use for reporting work. Then close each month to a fixed period and lock it after reconciliation.

| Record layer | What to keep | Monthly checkpoint |

|---|---|---|

| Operating ledger | Invoices, payouts, refunds, vendor costs, bank fees, contractor payments, founder-company transfers | Tie ledger totals to bank and processor statements |

| Reporting view | The period-based reporting format your adviser requests | Confirm method and period are documented and consistent |

| Owner transaction register | All owner-business transfers and direct payments | Match each line to a bank entry and supporting note |

Use explicit period markers in your close pack. For example, use a clearly labeled range such as 2024-01-01 to 2024-12-31 so reconciliation is easier to follow later. The provided SEC extract also uses date-stamped tagged items, including foreign currency translation, transactions with non-controlling interests, and potential ordinary share transactions, with markers such as 2025-01-15, which supports using consistent labels and period checkpoints.

Step 3. Handle tax concepts as escalation triggers, not assumptions#

When treaty relief, CFC analysis, or ECI comes up, treat each as a trigger for fact-specific review rather than something to assume from a generic summary.

| Situation | What to do |

|---|---|

| No adviser has tied the issue to your actual structure and transactions | Log it as open and request written analysis. |

| Your facts change | Reopen the analysis and request updated written analysis. |

| Advice is given | Store the assumptions used, what was reviewed, and what change would require a new review. |

Use the same rule operationally: if no adviser has tied the issue to your actual structure and transactions, log it as open and request written analysis. If your facts change, reopen the analysis and request updated written analysis. If advice is given, store the assumptions used, what was reviewed, and what change would require a new review.

Step 4. Build a verified annual filing pack early#

Build the pack as you go so filing decisions can be made from complete records.

Keep formation records, EIN documentation, registered-agent details, monthly statements, year-end ledger exports, and the full owner transaction register in one filing folder.

If your preparer raises a Form 5472 package, ask for written dependencies and companion filings they require, including any pro-forma item they require. Also ask who signs, and which transaction categories they want tracked. In your compliance calendar, track these unresolved items until your preparer confirms them:

- Penalty threshold: pending written verification by your preparer.

- Filing deadline: pending written verification by your preparer.

Keep one standing rule in your operating checklist: if your US operating facts change, reassess immediately and update your advice file before continuing expansion.

You might also find this useful: How to Set Up a US LLC from Australia.

Your Path to Confident US Expansion#

Treat Australian GST and ABN compliance as an ongoing discipline, not a one-time setup task.

| Stage | Ongoing decision you own | What to monitor, document, and escalate |

|---|---|---|

| Assess | Do your current activities mean GST registration may be required now? | Track business activities and turnover against the excerpted $75,000 turnover reference, confirm which entity is trading, and record ABN status and review date in writing. |

| Execute | When must you register, and through which non-resident pathway? | Confirm ABN first, then act within 21 days once registration is required. If pathway choice is unclear, including simplified, standard, or standard GST-only, escalate for specialist advice before filing. |

| Operate | Is your compliance position still accurate as facts change? | Recheck on a fixed cadence and on any material change in activities or structure. Keep proof-of-identity, ABN records, registration confirmations, and your written GST rationale in one folder. |

Keep two control reminders active. Penalties may apply if registration is required and missed. GST registration is once per entity, even if that entity runs more than one business.

First quarter after setup#

Use the first quarter to lock down your records and review routine:

- Confirm which entity is trading and whether ABN prerequisites are complete.

- Write and store your GST position note, including the facts reviewed, turnover tracking, and decision date.

- If the non-resident pathway or GST-credit treatment is uncertain, get written specialist guidance.

- Set your recurring review cadence and keep all compliance evidence in one place.

You are operationally ready when your records are clean, your review and registration routine is repeatable, and each decision has written support you can revisit quickly.

For a step-by-step walkthrough, see How to Set Up a US LLC as an Indian Citizen.

Frequently Asked Questions

What are the penalties for failing to file Form 5472?

It is treated as a critical filing. Current IRS instructions state a $25,000 penalty for failing to file Form 5472 when due and as prescribed. If your entity is a foreign-owned U.S. disregarded entity covered by these rules, it is generally filed as Form 5472 attached to a pro forma Form 1120, and extra time can be requested with Form 7004.

Is an LLC or C-Corp better for seeking venture capital?

There is no one-size-fits-all answer. Choose based on your likely funding path, governance needs, and compliance workload over the next 12-24 months. LLCs are often used for bootstrapped or closely held growth, while C-Corps are often used when institutional equity rounds or formal governance structures are likely.

How do you pay yourself from your US LLC back to Australia?

In many single-owner LLC setups, owners pay themselves through an owner's draw. In that accounting context, an owner's draw is a withdrawal from equity, not payroll wages. If you are an Australian tax resident, you generally still need to declare foreign income in Australia, so keep the transfer clearly recorded and confirm treatment with your tax adviser.

What constitutes ECI for a SaaS business?

ECI is income effectively connected to a U.S. trade or business, and it depends on your facts. IRS guidance points to whether your U.S. business activity is considerable, continuous, and regular. Treat U.S. nexus as an ongoing risk assessment and define your U.S. activity triggers before operational changes.

Do I need to pay US tax if my LLC has no US employees?

Not necessarily, but U.S. reporting obligations may still apply. A single-member disregarded LLC may be treated as part of the owner's return for income-tax reporting, but a foreign-owned U.S. disregarded entity can still be treated as a reporting corporation for Form 5472 purposes. Confirm both ECI exposure and whether Form 5472 plus pro forma Form 1120 applies to your facts.

Which US state is best for an Australian founder's LLC?

There is no universal best state. The right choice depends on your operating plan and funding path. Wyoming is often considered for lower baseline state fees, while Delaware is often chosen for its established corporate forum and broad company adoption, so match the state to your likely next 12-24 months and record each annual compliance date immediately.

Does the US-Australia tax treaty prevent all double taxation?

No, not automatically. Treaty outcomes depend on income type and your facts, and Australian residents generally still declare foreign income and then check whether a foreign income tax offset is available. Treat treaty relief as claim-based, not automatic, and keep evidence of any foreign tax paid.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ato.gov.au/businesses-and-organisations/gst-excise-and-...trusted

- ato.gov.au/businesses-and-organisations/international-t...trusted

- corp.delaware.gov/alt-entitytaxinstructionstrusted

- corp.delaware.gov/paytaxestrusted

- irs.gov/individuals/international-taxpayers/effectiv...trusted

- irs.gov/instructions/i5472trusted

- sba.gov/blog/5-things-know-about-your-balance-sheettrusted

- sec.gov/Archives/edgar/data/1940674/0001641172250103...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints

The goal is a defensible, low-drama position the Australian Taxation Office (ATO) can follow from your records, not a clever workaround. For a digital nomad, that usually means keeping two tracks straight: residency and GST/ABN admin. Consistency is what holds up over time: use real facts, take steps in a clear order, and keep documents that still match months later.

How to Set Up a US LLC from Australia

**Treat a US LLC from Australia as a system, not a one-time filing.** Forming the LLC is only the first milestone. What matters after that is how you handle the ongoing obligations in Australia and the United States.