Quick Answer

Start your stripe tax setup by locking four controls: origin address, product tax code mapping, registration status, and a clear escalation rule for nexus alerts. Next, run one repeatable close rhythm: review summarized and itemized tax exports, move collected amounts into a dedicated tax-hold account, and deliver a complete filing pack. The core boundary is simple: Stripe Tax supports calculation and reporting, while filing and payment to authorities remain an owned operational step.

The CFO's Playbook for Stripe Tax: A Framework for Bulletproof Global Compliance#

Treat your Stripe Tax setup as a cash-control system, not a settings task. The goal is to assign clear ownership, separate review from execution, and avoid assumptions that turn into cash surprises later.

The material in scope here is promotional lead-form content, not Stripe Tax product or tax-agency guidance. Use it as a reminder to verify, not as setup authority.

Before you configure anything, define your internal workflow labels and verify each one against current primary documentation for every jurisdiction.

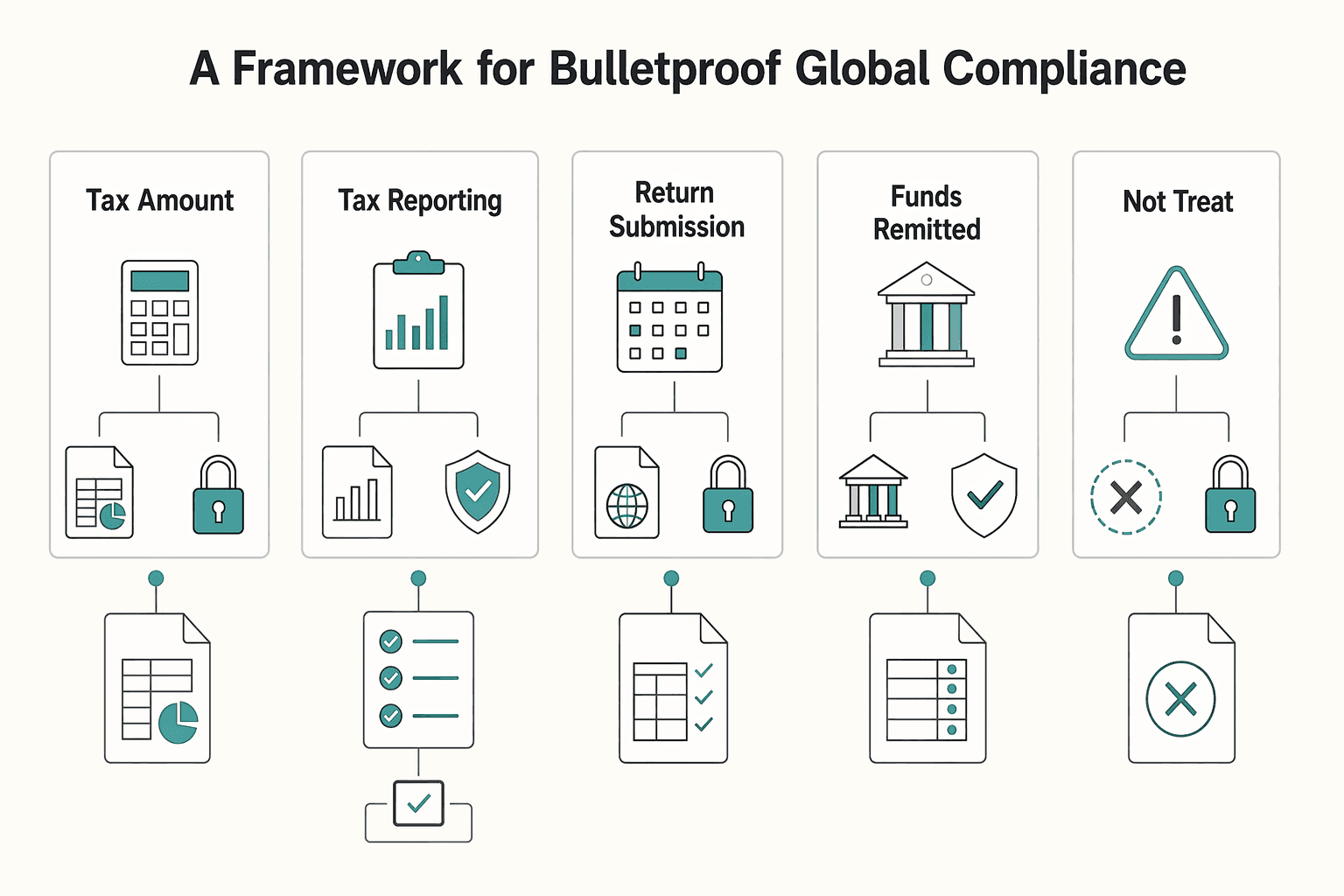

- Tax amount determination

- Tax amount charged and held

- Tax reporting outputs

- Return submission

- Funds remitted to authorities

These are separate jobs, and each can fail in a different way. Until you verify current primary documentation for your jurisdictions, assume each job is owned by you, your team, or your advisor.

Use this decision lens throughout:

- Do not treat marketing pages as compliance guidance.

- If a page asks you to leave contact details or agree to marketing messages, treat it as promotional context, not tax authority guidance.

- Keep jurisdiction-specific rules, thresholds, and filing duties in a "verify before action" bucket.

This playbook is organized around that process:

- Configuration: set ownership and review checkpoints before operational use.

- Workflow: define handoffs so calculated and collected amounts are tracked and reviewed.

- Edge scenarios: flag cases that need extra verification instead of default assumptions.

- FAQs: resolve recurring scope and responsibility questions quickly.

The outcome is a process you can review and update as rules change, not a claim of automatic compliance.

Related: How to Reduce Stripe Processing Fees.

Part 1: Strategic Configuration - Building Your Foundation#

Set this up as a decision system, not a toggle. Before Stripe Tax goes live, lock down four inputs you should be able to defend later: your head office address, your product tax code mapping, your registration status, and whether automation costs less than manual error.

Step 1#

Start by defining the inputs that actually drive calculation:

| Setup input | What it covers | Key note |

|---|---|---|

| Head office address | Business-location input in Stripe Tax setup; for physical goods, the address you ship from | Use the address you can document |

| Product tax code (PTC) | Product or service classification Stripe Tax uses to map what you sell to tax rates | Be as specific as you can justify |

| Registration status | Jurisdictions you add in Stripe where you are registered to collect tax | Stripe Tax only calculates where you've added registration |

| Nexus monitoring | Alerts for potential registration obligations, including US economic nexus signals | Monitoring is advisory; confirm whether registration is required |

Keep each one explicit:

- Head office address (origin input): the business-location input in Stripe Tax setup and, for physical goods, the address you ship from.

- Product tax code (PTC): the product or service classification Stripe Tax uses to map what you sell to tax rates.

- Registration status: the jurisdictions you add in Stripe where you are registered to collect tax.

- Nexus monitoring: Stripe's alerts for potential registration obligations, including US economic nexus signals.

Keep the responsibility boundary explicit. Stripe Tax calculates using your business address, registrations, PTCs, customer location, and customer status. It only calculates where you've added registration, and monitoring is advisory. You still need to confirm whether registration is required in each jurisdiction. You also still need to file and remit what you collect, even if you use a filing partner to automate part of the process.

Step 2#

Use the head office address you can document, not the one that feels most convenient today. A common approach is to use the stable business location in your formal records. If you ship physical goods, use the shipping-from address Stripe setup expects.

Before you move on, reconcile the address in Tax settings with your business documents and tax records. If those drift, calculations can still rely on stale origin data.

Step 3#

Classification is where otherwise clean setups often go wrong, so be as specific as you can justify. If one commercial offer could fall under more than one treatment, split it into separate Stripe products and assign each its own code.

| Offer type | Potential treatment | Edge case to watch | Verify before publishing |

|---|---|---|---|

| Live consulting, coaching, custom services | Can vary by service scope and jurisdiction | Bundle also includes downloadable assets | Confirm the primary deliverable and match it to Stripe's tax-code list |

| Downloadables, self-paced digital content | Can vary based on whether the offer is purely digital or mixed | Offer also includes live support or implementation | Confirm whether the value is mostly digital or mixed |

| Recurring software access | SaaS treatment can vary by use case and jurisdiction | Contract includes services or other bundled components | Review Stripe tax-code options and document your rationale |

| Memberships combining content + access/perks | Often mixed, not one clean treatment | One price hides multiple taxable components | Split into separate products when classification is unclear |

If classification is still unclear, use a General code family as a fallback, then revisit it before volume builds.

Step 4#

Enable monitoring, but decide in advance what turns an alert into a registration review. Manage registrations in the Tax page's Registrations tab, then use this checklist:

- Add jurisdictions where you are already registered.

- Turn on threshold monitoring for target jurisdictions.

- Track non-Stripe sales separately, since monitoring primarily reflects Stripe-processed payments.

- Log each jurisdiction with a current-threshold field marked

Current threshold pending source-record verificationuntil the source has been checked, then record the source, check date, and owner. - Escalate to registration only after you confirm the rule applies to your facts.

- If you are a US remote seller, check Stripe's registration-on-your-behalf option, typically 30 days or less, and 60 days or less in Dec-Feb.

Operational note: newly processed transactions are usually reflected in monitoring within 7 days, so treat the dashboard as delayed, not instant.

Step 5#

Make the cost decision with a break-even view, not instinct. Stripe lists Tax Basic at 0.5% per transaction (no-code) or 50 cents per transaction (API), where you're registered to collect taxes, plus 5 cents per calculation API call above 10. Stripe also advertises Tax Complete starting at $90 per month.

| Pricing item | Price | Note |

|---|---|---|

| Tax Basic (no-code) | 0.5% per transaction | Where you're registered to collect taxes |

| Tax Basic (API) | 50 cents per transaction | Where you're registered to collect taxes |

| Calculation API calls above 10 | 5 cents per calculation API call | Additional charge above 10 |

| Tax Complete | Starting at $90 per month | Advertised starting price |

Use a simple test. Compare tool cost against manual classification work, registration tracking effort, correction time, and under-collection exposure. Low-volume, single-jurisdiction setups can justify more manual handling. Mixed offers and multi-jurisdiction sales can increase complexity, which may justify automation earlier.

We covered this in detail in Using Wise 'Jars' to Automatically Set Aside Tax Money for Multiple Jurisdictions.

Part 2: The Workflow - From Calculation to Compliance#

A setup is only useful if you can carry it through to a filed return without guesswork. Stripe Tax handles calculation and reporting. Filing and remittance still sit with you in every jurisdiction where you are registered, unless you delegate filing through a partner flow.

Use the same order every period: read reports, segregate funds, then hand off a filing pack. Keep that sequence tight, because collected tax is added to your Stripe balance and paid out based on your payout settings, not automatically ring-fenced.

Step 1. Read the reports#

This is where you decide whether a period is ready to close. You, or a close-process owner, should export reports after report lag clears, then use them to estimate filing totals and keep a defensible transaction trail.

| Report | Output | Primary use |

|---|---|---|

| Summarized export | CSV | Filing totals by jurisdiction |

| Itemized export | CSV | Transaction-level audit trail, refund review, and US sub-state detail where required |

| Location reports | Aggregated view | Your US and Canada registrations |

Those outputs do different jobs, so do not substitute one for another.

Before you lock a period, run these checks:

- Jurisdiction totals in the summarized export match your expected filing view.

- Refunds for the period are included.

- Presentment and filing-currency views reconcile for cross-border sales.

If a mismatch appears, stop and resolve it before submission. Common causes include report timing delay, typically within one day; refunds posted after close; reduced detail on imported external transactions; or jurisdiction-name structure changes since May 2024.

Step 2. Segregate the funds#

If you do not separate collected tax from operating cash, the rest of the process gets fragile. You or your finance lead can move collected tax into a dedicated tax-hold account so remittance cash stays available and out of operating spend.

Treat the tax-hold account as a control, not a Stripe-managed feature. Trigger transfers from a repeatable event, commonly after payout receipt and once the related report window is clear. Then document the timing rule only after it has been verified against finance or source records.

Handle exceptions with rules:

- If refunds post after transfer, adjust the next transfer.

- If reconciliation is unresolved, pause the transfer for that period and move only the reconciled amount.

- Do not assume transfer cadence equals filing cadence. Filing can be monthly, quarterly, annually, or another authority-defined frequency; if unclear, confirm with your local tax authority.

Step 3. Handoff the filing pack#

A filing handoff should be boring. Prepare one complete, period-labeled package so your accountant, tax partner, or delegated provider can file without avoidable back-and-forth.

| Required file/document | Format | Naming period example | Purpose | Sign-off criteria |

|---|---|---|---|---|

| Summarized export | CSV | 2026-03 Tax Summary | Filing totals by jurisdiction | Totals match period close |

| Itemized export | CSV | 2026-03 Tax Itemized | Audit trail, refunds, sub-state support where needed | Spot-check rows against source transactions |

| Tax cash reconciliation | CSV or sheet | 2026-03 Tax Cash Reconciliation | Shows payouts vs tax-hold transfers | Difference is zero or documented |

| Registration and tax identity docs | Jurisdiction Registration Pack 2026-03 | Required in some partner-assisted filing flows | Tax IDs and entity details match current registrations |

If you use a partner-assisted route, include registration documents, tax IDs, and any location-specific forms with the exports. For API-heavy workflows, keep related Tax Transaction records available for traceability. Submit only when totals, refunds, and cash movement reconcile, or when any open difference has a named owner and a resolution date.

You might also find this useful: The Best Software for Calculating and Remitting Sales Tax.

Before you finalize your filing workflow, sanity-check customer VAT IDs so reverse-charge handling is less error-prone: Use the VAT Number Validator.

Part 3: The Edge - Mastering High-Stakes Global Scenarios#

You can close a period cleanly and still mishandle the cases that matter most. For this section, the only verified external checkpoint is the EU VAT e-Commerce OSS Guides page on europa.eu and its Explanatory Notes entry; legal determinations and tool-specific setup details are not established here.

| Scenario | What determines treatment | Stripe configuration action | What you must validate and retain manually |

|---|---|---|---|

| EU B2B reverse charge | Confirm jurisdiction-specific legal conditions with the relevant authority | Confirm reverse-charge Stripe setup with the relevant authority | Verified legal basis, customer evidence, invoice wording, and the exact EU guidance page/file version used |

| US nexus exposure | Confirm US state requirements with the relevant authority | Confirm US nexus Stripe configuration with the relevant authority | Your current internal analysis, dated decisions, and advisor confirmation |

| Cross-border service delivery | Confirm indirect-tax and related tax-treatment rules with the relevant authority | Confirm cross-border Stripe setup with the relevant authority | Contract/invoice/customer-location records and dated review notes |

EU B2B reverse charge#

Treat this as a stop-and-verify case, not a default invoice shortcut.

- Trigger condition: a customer request can indicate a review need, but it does not confirm treatment on its own.

- Required data: collect complete customer and entity records before deciding treatment.

- Configuration action: make tooling changes only after separate legal/tax verification.

- Documentation to retain: if you rely on EU guidance, keep the official

europa.eupage and file details. A practical checkpoint is the VAT e-Commerce Guides page Explanatory Notes entry, including page date 30 JULY 2021, English filename token 28102020, file size 1.83 MB, and Other languages (22) where relevant; verify the version/date before operational reliance. - Escalation point: escalate whenever legal basis, wording, or entity alignment remains unverified.

US nexus exposure#

Treat this as an ongoing monitoring decision, not a one-time setup.

- Trigger condition: internal monitoring may surface risk.

- Required data: use your own current activity records and measurement windows.

- Configuration action: do not treat this section as Stripe or registration workflow guidance.

- Documentation to retain: keep measurement reports, dated decisions, and advisor notes.

- Escalation point: escalate when obligations or start timing remain unclear after review.

Cross-border service delivery#

Keep cross-border cases in a dedicated review lane from the start.

- Trigger condition: multi-country facts indicate review need.

- Required data: contract entity, invoice entity, customer/location evidence, and service description.

- Configuration action: do not treat this section as cross-border tooling setup guidance.

- Documentation to retain: contract, invoice, customer evidence, and a dated note of your reviewed rationale.

- Escalation point: escalate when tax treatment remains uncertain.

The control that ties all three scenarios together is straightforward: treat unverified legal/tax points as unresolved, avoid tool-first assumptions, and keep audit-ready records of what was verified at invoice time.

If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

Conclusion: From Compliant to Confident#

A reliable setup is one you can defend from settings through filing. The standard is not whether calculation worked on screen. It is whether you can show how settings, ownership, and verification connect calculation to filing and remittance.

- Run Stripe Tax as your primary setup when your taxable sales are mostly processed in Stripe.

Use Stripe as the core when you can keep three controls accurate: your head office address, the product tax code for each product or service, and tax behavior (tax added on top vs included in price). Stripe can automatically calculate and collect after setup, but the output is only as good as those inputs.

- Add a filing/remittance partner when calculation is stable but filing execution is the bottleneck.

You still own registration, filing, and remittance in each location where you are registered. Stripe's filing partners can automate much of filing, with pricing that varies by partner and location. If reporting is on time but filing tasks or payments are not, this can be the handoff to fix.

- Escalate to tax counsel when threshold signals or jurisdiction rules are unclear.

Threshold monitoring flags potential obligations, including economic nexus, but Stripe describes this as advisory and primarily based on Stripe-processed payments. If your sales footprint includes off-Stripe channels or unclear local rules, confirm obligations with your advisor or the relevant tax authority before changing collection settings.

In practice, the backbone is simple: keep settings current, review product classification, make reporting-to-remittance ownership explicit, and monitor thresholds on a recurring schedule.

- Review your head office address, tax behavior, and every product tax code.

- Verify registrations where collection is enabled; document current threshold status and the effective date after verification.

- Confirm named owners for reporting, filing, and remittance in each jurisdiction.

- Schedule a monthly compliance check for threshold monitoring, off-Stripe channel coverage, and refund-impact follow-up.

For a step-by-step walkthrough, see How to use Paddle to handle sales tax and VAT for a SaaS product sold globally.

If you want to turn this setup into a repeatable operating process with clear controls and traceable records, use this as your implementation checklist: Read the docs.

Frequently Asked Questions

Does calculation and reporting mean filing and remittance are handled too?

Not confirmed from this excerpt. Treat calculation and reporting, and filing and remittance, as separate owned steps until your team verifies end-to-end behavior in your actual setup. Keep a dated owner list for each step before every close cycle.

Is Stripe alone enough for your Stripe Tax setup?

This excerpt alone cannot confirm that. Use this fit check before you lock your workflow: | Option | Choose this if... | Watch for | | --- | --- | --- | | Native Stripe-centered setup | Most sales records and tax-review inputs are managed in one Stripe workflow | Missing non-Stripe activity, unclear filing owner | | Stripe plus filing/remittance partner | You want Stripe in billing but want a separate filing/remittance operating lane | Weak handoff from transaction review to filed return | | Broader multi-channel compliance stack | You need one reconciled view across channels or entities before filing | Duplicate records, inconsistent customer tax data, late registration decisions |

Can you treat VAT reverse charge as automatic for B2B invoices?

Not confirmed in the provided excerpt. Keep this as a stop-and-verify decision. Verify any jurisdiction-specific text or rule logic from official source records before you use it in process documentation or configuration.

Should you rely on built-in nexus monitoring by itself?

Not from this excerpt alone. It does not confirm threshold logic, alerts, or registration-trigger behavior. Build one dated report across your full sales footprint and record thresholds, measurement windows, and start-date decisions only after official source-record verification.

What limitations should you actively check each month?

The excerpt does not list detailed product limitations. As an operational control, run a four-part checklist every month: confirm data quality, confirm channel coverage, document registration-trigger decisions, and confirm filing and remittance ownership before period close. If any of those four are unclear, treat it as an open control gap.

If you use Connect, where should you look for tax-reporting guidance first?

Start with the Connect docs items visible in the excerpt: “Support recommendations and FAQ templates,” “Tax forms for your Connect platform,” “Implementation and timeline,” and “Communication timeline.” If year-end reporting is in scope, also review the referenced “1099 tax support and communication guide.”

What is a practical failure mode when you verify docs or settings?

Plan for access friction. The captured docs session shows a challenge failure state: “Please try again. ⚠️” Keep a saved page title and dated decision notes so your team can keep moving even if you cannot immediately reopen the page.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- docs.stripe.com/tax/filingtrusted

- docs.stripe.com/tax/set-uptrusted

- ncpc.gov/files/projects/2016/MP20_Transportaton_Manag...trusted

- sme-vat-rules.ec.europa.eu/sme-scheme/cross-border-sme-scheme_entrusted

- stripe.com/tax/pricingtrusted

- support.stripe.com/questions/what-happens-to-the-funds-after-ta...trusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- vat-one-stop-shop.ec.europa.eu/guides_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

How to Reduce Stripe Processing Fees

**You can protect margin by treating fees, payout timing, and dispute exposure as one risk system.** It is easy to fixate on headline Stripe fees. In practice, margin usually leaks from three places at once:

The Best Software for Calculating and Remitting Sales Tax

If you are looking for the best software for sales tax, decide on the operating model before you compare calculators. The real risk is not just getting the rate wrong. It is knowing where tax is due, who has to account for it, and whether the liability stays with you.