Quick Answer

To set up an IRS payment plan for back taxes as a freelancer, apply as an individual through Online Payment Agreement after confirming filings and account access. Choose one path based on your situation, submit once, and save proof immediately. Then run a repeatable checklist that tracks payment-plan actions and cross-border reporting tasks like FBAR and Form 8938 so tax debt does not recur.

Your 10 Minute IRS Payment Plan Playbook for Freelancers#

Use this IRS payment plan playbook to pick one path, submit through OPA, and run a repeatable checklist that keeps a tax balance from turning into ongoing tax debt. You run a business of one, so the goal is clean execution. This workflow is for sole proprietors and independent contractors who want a low-drama default. Decide once, document once, then pay it down on schedule.

Pick your path and commit once#

- Classify your situation. Choose one branch only: full pay, short-term payment plan, or long-term payment plan (installment agreement).

- Apply the IRS thresholds. A short-term payment plan fits balances less than $100,000 and targets payoff in 180 days or less. A simple payment plan is a long-term installment agreement option when combined tax, penalties, and interest are $50,000 or less.

- Define your fallback before submission. If your first choice fails in OPA, switch to one preselected backup path instead of improvising.

| Path | Best use case | Key rule you should note |

|---|---|---|

| Full pay | You can clear the balance now | Pays the balance now |

| Short-term payment plan | You need brief runway | Balance less than $100,000, pay in 180 days or less |

| Long-term payment plan | You need monthly structure | Runs as an installment agreement |

| Simple payment plan | You qualify for this long-term option | Combined balance at $50,000 or less |

Operator rule: make the choice once, write down why, and execute the same day. That single decision prevents second-guessing and rework.

Execute in OPA and lock your operating checklist#

- Start in Online Payment Agreement. IRS describes OPA as the quickest and easiest setup channel for an IRS payment plan.

- Capture the result immediately. OPA can return an immediate decision on approval status after you submit.

- Protect follow-through. Interest and penalties continue until you pay the full balance, so assign ownership of the first payment date before you close your session.

- Known now: OPA is the default self-service lane, and plan options include full pay, short-term, and long-term installment agreement.

- Unknown until you apply: Your exact approval outcome and final path acceptance.

Use this as your recurring operator loop: choose one path, submit once, save proof, and track payments until the balance is zero. If you want related reading, see The Best Digital Nomad Cities for Entrepreneurs and Startups.

What Should You Prepare Before You Start?#

Prepare five items before you open OPA: current filings, IRS Online Account access, the right applicant profile, clear authority, and a one-page control sheet. This keeps execution fast and helps prevent back-tax cleanup from turning into extra admin work.

| Prep item | What to confirm | Verification |

|---|---|---|

| Required filings | All required returns are filed; note whether Schedule SE applies when net self-employment earnings from all businesses reach $400 or more | Mark filings done and note Schedule SE status |

| IRS Online Account | Account is set up; keep photo ID ready for account creation; confirm you can reach OPA | Sign in successfully and confirm you can reach OPA |

| Applicant profile | If you are a sole proprietor or independent contractor, apply as an individual | Record individual applicant |

| Authority | Name the communication owner; if someone else handles submissions, confirm authorized representative status and power of attorney; use Form 2848 | Record application owner assigned and POA confirmed |

| Operator sheet | Track balance snapshot, filing status, selected path, and next action; flag possible simple installment agreement eligibility if combined tax, penalties, and interest are $50,000 or less | Sheet shows filings done, account access verified, and application owner assigned |

Build your readiness pack#

- Step 1. Confirm required filings. Verify that you filed all required returns before you apply for an IRS payment plan. For self-employment, check whether Schedule SE applies to you. Use Schedule SE when net self-employment earnings from all businesses reach $400 or more.

Verification point: Mark filings done on your prep sheet and note Schedule SE status.

- Step 2. Create IRS Online Account access first. Set up your IRS Online Account before you make plan decisions, and keep photo ID ready for account creation. After setup, you can submit through Online Payment Agreement without calling, mailing, or visiting the IRS.

Verification point: Sign in successfully and confirm you can reach OPA.

- Step 3. Classify yourself correctly. If you operate as a sole proprietor or independent contractor, apply as an individual. This keeps your application aligned with the expected IRS process.

Verification point: Record individual applicant in your notes.

Assign authority and control ownership#

- Step 4. Name the communication owner. Decide who sends updates and responds to IRS notices. If someone else handles submissions, confirm authorized representative status and power of attorney before filing. Use Form 2848 to authorize eligible representation.

Verification point: Record application owner assigned and POA confirmed.

- Step 5. Build a one-page operator sheet. Track balance snapshot, filing status, selected path, and next action. If your combined tax, penalties, and interest are $50,000 or less, flag possible simple installment agreement eligibility for later confirmation.

Verification point: Your sheet shows filings done, account access verified, and application owner assigned.

If you split roles between delivery and admin, keep decision ownership and communication ownership explicit. Payment-plan work stalls when those roles are fuzzy.

Which IRS Path Fits Your Situation Right Now?#

Pick one payment path based on your balance, timeline, and what OPA says you qualify for. Your tax situation determines which options are actually open to you.

Run the decision tree once#

- Step 1. Test full pay first. If you can clear the balance now, choose full pay and close the loop.

Verification point: You can fund payment now without disrupting core business operations.

- Step 2. Check short-term fit. Choose a short-term payment plan when you owe less than $100,000 in combined tax, penalties, and interest, and can finish within 180 days or less.

Verification point: Your notes confirm both the balance threshold and payoff window.

- Step 3. Check long-term fit. Choose a long-term payment plan when you need monthly structure through an installment agreement.

Verification point: Your monthly payment target fits your expected cash flow.

- Step 4. Screen for simple payment plan eligibility. A simple payment plan is a long-term plan for qualified taxpayers. Online criteria include a combined balance of $50,000 or less and all required returns filed.

Verification point: Mark eligibility as likely or unclear before you submit in Online Payment Agreement.

| Label in your notes | What it means | How to use it |

|---|---|---|

| IRS payment plan options | Available payment paths based on your tax situation | Use as your umbrella term |

| Short-term payment plan | Pay in 180 days or less | Use for faster resolution when you qualify |

| Long-term payment plan | Monthly repayment structure | Use when you need more runway |

| Installment agreement | IRS label for long-term monthly plan | Treat as the same lane, not a separate fourth option |

Lock your choice and fallback#

- Step 5. Write one decision line. State your primary path and your fallback if OPA does not offer it.

- Step 6. Record your reason in one sentence. Tie the choice to balance, timeline, and operating stability in your freelance finance system. When income is uneven, discipline matters more than creativity. Choose a path, define one fallback, and execute.

How Do You Execute OPA Without Rework?#

Log into your IRS Online Account, submit once through Online Payment Agreement, and leave with a complete decision record before you close the session. This is about doing it one time, cleanly, with proof.

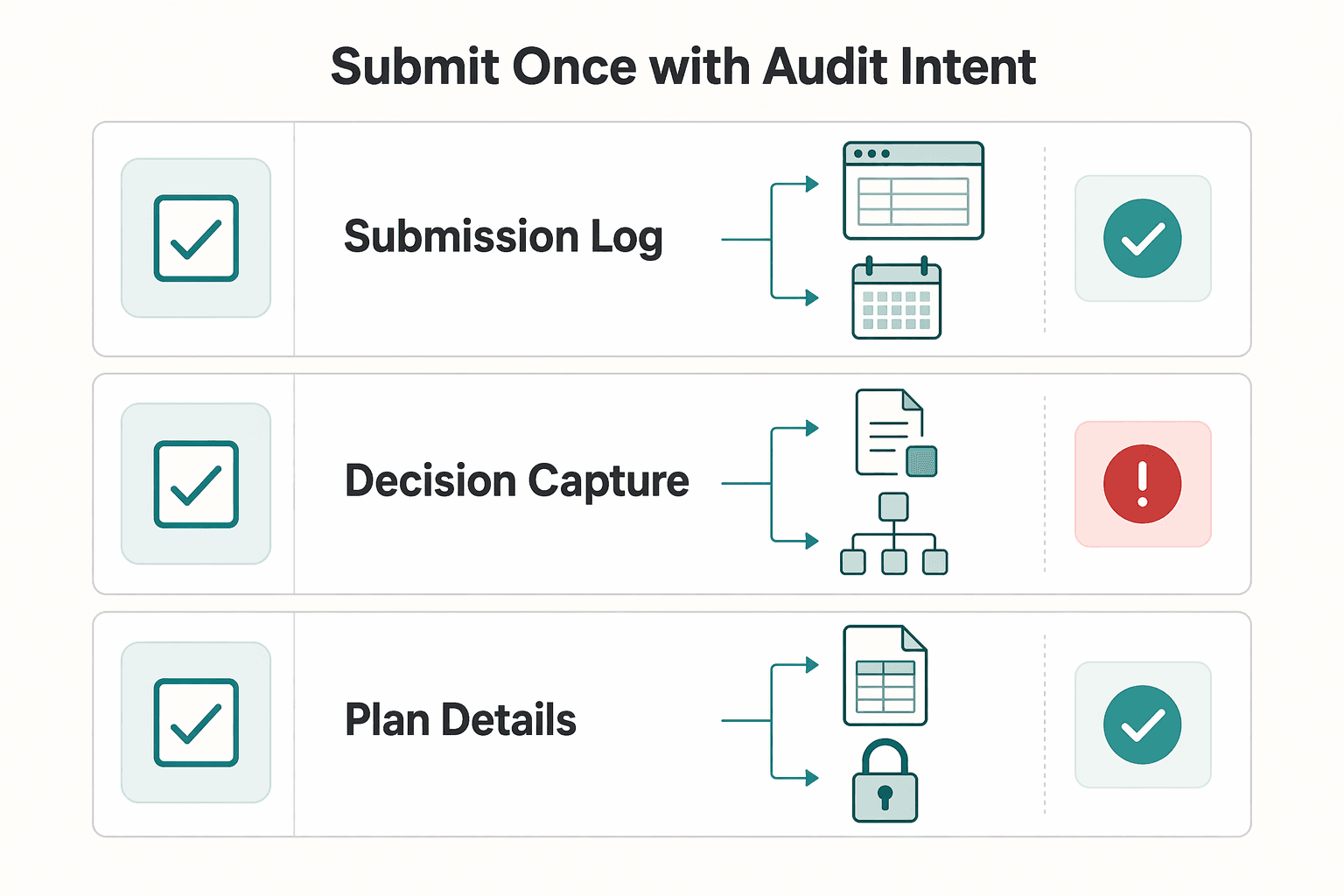

Submit once with audit intent#

- Step 1. Sign in and open OPA first. Use your IRS Online Account, then start in Online Payment Agreement instead of jumping straight to phone or mail. Most taxpayers who qualify can use this self-service lane for an IRS payment plan.

Verification point: You see the payment-plan application flow inside your signed-in account.

- Step 2. Confirm your selected lane labels. Match your notes to the exact IRS terms before you type anything: short-term payment plan, or long-term payment plan (installment agreement).

Verification point: Your selected label in OPA matches your decision sheet exactly.

- Step 3. Enter data once and capture proof immediately. Record a timestamp, what you submitted, and which path you requested. Store that record with your tax files.

Verification point: You saved one submission log with time, plan type, and account snapshot.

- Step 4. Save the decision result the moment OPA returns it. OPA provides immediate approval-status notification after submission. Capture the status screen and copy key details into your tracker.

Verification point: You have an approval status saved in your records.

| Record you save | Why it prevents rework | Minimum detail |

|---|---|---|

| Submission log | Stops duplicate or conflicting applications | Date/time, plan requested, owner |

| Decision capture | Preserves approval outcome for follow-up | Approved or not approved |

| Plan details note | Keeps payment execution on schedule | Agreement type, due dates, payment amount |

Switch lanes intentionally if online blocks you#

| Channel | When to use | Key detail |

|---|---|---|

| Online Payment Agreement (OPA) | Start here when you can apply online | Self-service online flow with immediate approval-status notification after submission |

| Form 9465 | Use if OPA says you cannot apply online | Move to the non-online lane on purpose and log why you escalated |

| IRS phone | Use if OPA says you cannot apply online | 800-829-1040 (individual) or 800-829-4933 (business) |

- Step 5. Escalate with a documented reason. If OPA says you cannot apply online, move to the non-online lane on purpose. Use Form 9465 or call the IRS at 800-829-1040 (individual) or 800-829-4933 (business).

Verification point: Your tracker shows why you escalated and which channel you chose.

- Step 6. Assign first-payment ownership before you stop. If the system shows a first payment date, record it now. If it does not, set a follow-up task to confirm due dates in your account.

Verification point: One owner and one calendar task control the next payment action.

Finish the session the same way you finish a client deliverable: submit, save proof, schedule the next action, then log out.

What Will This Cost and Which Channel Is the Safe Default?#

Start with Online Payment Agreement, then confirm the exact fee line for your plan type before you submit. The goal is not to optimize pennies. It is to choose a channel you can complete, with a fee you expect, and records you can defend later.

Run a fast channel cost check#

- Step 1. Confirm your plan type. Decide whether you are setting up a short-term payment plan (180 days or less) or a long-term payment plan (installment agreement).

Verification point: Your tracker shows one selected path, not multiple drafts.

- Step 2. Price the channel for long-term setup. For long-term direct debit installment agreement setups, IRS lists lower setup fees online than by phone, mail, or in person. IRS also lists lower online setup fees for long-term non-direct-debit plans.

Verification point: You record the fee row that matches your exact setup.

- Step 3. Choose channel by reliability first, then cost. Use OPA as your default when you can complete it because it is a self-service online flow and can return immediate approval-status notification after submission.

Verification point: You can complete the online application flow for your selected plan.

| Long-term setup type | Apply online | Apply by phone, mail, or in person | Operator takeaway |

|---|---|---|---|

| Direct debit installment agreement | $22 setup fee | $107 setup fee | Online is usually the cleaner default when eligible |

| Non-direct-debit plan | $69 setup fee | $178 setup fee | Online often reduces setup cost for long-term plans |

Keep a known vs unknown log#

- Known now: Setup fees may differ by channel, and card payments can add processing fees.

- Unknown until final click: The exact fee matrix that applies to your case at submission time.

- Action: Recheck current IRS fee details immediately before you submit, then lock your decision. Do not chase small fee differences until you confirm eligibility and execution reliability for your selected plan.

How Do Globally Mobile Freelancers Avoid Compliance Drift?#

Run two parallel compliance lanes every month, one for your IRS payment plan and one for cross-border reporting, so progress on tax debt never hides new filing risk. If you are moving across borders, you need separation inside your system. Debt resolution is one lane. Foreign reporting is another lane.

Treat foreign-account disclosure as a high-stakes process and execute it with a checklist, not memory.

Build a two lane tracker#

- Step 1. Open lane one for IRS payment plan status. Track your installment agreement status, next payment date, and proof of each completed payment.

Verification point: Your tracker shows current plan status and next action owner.

- Step 2. Open lane two for cross-border reporting status. Track FBAR, FATCA, and Form 8938 separately from payment-plan tasks.

Verification point: You can answer, in one glance, what is filed and what is pending.

- Step 3. Apply the right filing destinations. File FBAR on FinCEN Form 114 with FinCEN, not with the IRS. Attach Form 8938 to your annual tax return when required.

Verification point: Your checklist distinguishes FinCEN filing from IRS return attachments.

| Lane | Core items | Decision rule |

|---|---|---|

| IRS payment plan status | Plan type, payment date, confirmation records | Keep payments current and documented |

| Cross-border reporting status | FBAR trigger check, Form 8938 check, filing destination | Never assume one filing replaces another |

Tie both lanes to your annual cycle#

| Item | Threshold or trigger | Handling note |

|---|---|---|

| FBAR | Aggregate foreign account value exceeds $10,000 at any time during the year | File FBAR on FinCEN Form 114 with FinCEN, not with the IRS |

| Form 8938 | FATCA reporting generally starts at $50,000; thresholds vary by filing context | Attach Form 8938 to your annual tax return when required |

| Schedule SE | Net self-employment earnings from all businesses reach $400 or more | Keep Schedule SE readiness in your self-employed annual workflow |

- Step 4. Run threshold checks on schedule. FBAR filing can trigger when aggregate foreign account value exceeds $10,000 at any time during the year. FATCA reporting uses Form 8938 and generally starts at $50,000, with thresholds that vary by filing context.

Verification point: You log threshold checks before filing deadlines.

- Step 5. Anchor to self-employed routines. Use your self-employed annual workflow, including Schedule SE readiness, so your IRS payment plan process supports broader freelance finance control.

Verification point: One calendar links payment-plan actions, Schedule SE prep, and cross-border checks.

If you move countries mid-year, do not merge these lanes in your head. Keep them separate on paper, then run them side by side.

What Are the Common Failure Points and How Do You Recover Fast?#

Recover fastest by fixing identity, authority, records, and cross-border checkpoints in that order before you touch price or timing decisions. This is the stress test. When the process breaks, you want a clean recovery sequence, not a scramble.

| Failure point | What it looks like | Fast recovery | Verification point |

|---|---|---|---|

| Wrong applicant framing | You submit as a business flow even though you operate solo | Reapply as an individual when you are a sole proprietor or independent contractor | Your submission profile matches individual taxpayer status |

| Incomplete authority setup | A helper contacts IRS without formal authority | Set up authorized representative status and submit Form 2848 power of attorney before the next payment-plan application attempt | IRS interactions now run through the named representative path |

| Process opacity | You cannot prove what you submitted in OPA | Keep a dated log of OPA actions and confirmation messages, and retain your recent statement or confirmation letter | You can retrieve approval evidence and confirm payment date and amount |

| Compliance tunnel vision | You track installment payments but ignore foreign reporting | Add FBAR and Form 8938 checkpoints to the same calendar | You file FBAR with FinCEN and handle Form 8938 separately when required |

Run the recovery loop in order#

- Confirm applicant type. If your first attempt fails, reset to the individual path for your IRS payment plan or installment agreement.

Verification point: Your resubmission reflects individual filing identity.

- Formalize representation. If someone acts for you, complete power of attorney setup first, then reopen the process.

Verification point: The right person can act through the authorized representative path.

- Audit every handoff. Record each OPA action, save confirmation text, and store your recent statement or confirmation letter with your freelance finance records.

Verification point: You can confirm payment date and amount without guessing.

- Protect the compliance perimeter. If online eligibility fails, switch intentionally to another IRS channel and keep the log intact. If a plan defaults, pursue reinstatement quickly. Keep FBAR and Form 8938 checks active in parallel.

Verification point: No channel switch or cross-border filing obligation falls out of view.

If a teammate submits under the wrong role, pause. Fix identity and authority first, then rebuild your record trail, then move forward. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Run This Checklist and You Will Stay in Control#

Use this checklist regularly to keep your workflow stable and your compliance risk visible. Everything above comes down to one system: one owner, one chosen path, one submission record, and one tracker that stays current.

Start with one path and one owner. If you are a sole proprietor or independent contractor, apply as an individual. Keep your IRS Online Account active so you can use the online payment agreement application (OPA) first and avoid unnecessary phone or mail handoffs.

| Path | Use when | Control to log |

|---|---|---|

| Full pay | You can clear the balance now | Payment date and confirmation record |

| Short-term payment plan | You can finish within 180 days or less and owe less than $100,000 combined | End date and remaining balance checkpoints |

| Long-term payment plan (installment agreement) | You need monthly payments; the simple online path generally requires $50,000 or less | Monthly due date, amount due, and plan type |

Copy and paste checklist#

[ ]I confirmed I am applying as an individual sole proprietor or independent contractor.[ ]My IRS Online Account is active and I can access OPA.[ ]I selected one path only: full pay, short-term payment plan, or long-term payment plan/installment agreement.[ ]I recorded my submission date, first payment date, and any status updates available.[ ]I documented unknowns to verify on IRS pages, including current fee details and channel differences.[ ]I added parallel reminders for FBAR (FinCEN Form 114) and Form 8938 where relevant.

If OPA blocks you or marks you ineligible, switch to the offline fallback and file Form 9465 so momentum does not break. If a teammate handles filing while you are abroad, assign one checklist owner and one review date, then close every open item before the week ends.

Use this list as your control loop for back taxes and tax debt. Bring in a qualified tax professional when authority, eligibility, or cross-border reporting turns unclear, especially when you may need Form 8938, FBAR, or both.

Frequently Asked Questions

Can a freelancer apply for an IRS payment plan as self-employed?

Yes. If you work as a sole proprietor or independent contractor, apply as an individual through Online Payment Agreement.

What is the difference between a short-term payment plan and an installment agreement?

Use a short-term payment plan when you can pay within 180 days or less. Use a long-term payment plan (installment agreement) when you need monthly payments. The difference is the payoff timeline and structure.

What qualifies someone to use Online Payment Agreement?

Eligibility depends on plan type and what you owe. For a simple long-term individual plan, IRS says you must owe $50,000 or less in combined tax, penalties, and interest, and you must file all required returns. For a short-term online plan, IRS says you must owe less than $100,000 combined.

Do I need all required returns filed before applying?

For the simple online installment agreement path, yes. IRS ties eligibility to filing all required returns first. If you still need to file, close that gap before you apply.

Is applying through OPA cheaper than phone or mail?

Channel choice affects setup fees, and IRS says phone, mail, or in-person setup fees may run higher. Current long-term examples show lower online fees in common cases, including $22 versus $107 for direct debit and $69 versus $178 for non-direct debit. Confirm current fee tables before you choose a channel.

What happens right after I submit an OPA application?

After you submit OPA, the system gives you immediate notice about approval status. Save that result for your records. If your request stays pending, IRS may pause levy action, though exceptions apply.

What should I do if I cannot complete the process online?

Switch to the offline lane instead of waiting. IRS still lets individuals request installment payments with Form 9465, and phone support remains available. Use your fallback promptly and log each step so you can document what happened.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

The Best Digital Nomad Cities for Entrepreneurs and Startups

Choosing a nomad base for your company is an execution decision first. Lifestyle matters, but it belongs in the second round. The costly mistakes usually show up after the city-ranking stage, when a place that looks great online turns into a slow or expensive setup once you start invoicing, signing contracts, and working against real deadlines.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.