Quick Answer

Australians can generally set up a US LLC, but the real work is running it compliantly after formation. Follow a compliance-first sequence: verify jurisdiction triggers including possible ASIC foreign company registration, prepare consistent entity data, form the LLC, obtain the EIN, open a US business bank account, and maintain a recurring reporting and reconciliation rhythm across Australia and the United States.

Build a US LLC from Australia without compliance surprises#

Treat a US LLC from Australia as a system, not a one-time filing. Forming the LLC is only the first milestone. What matters after that is how you handle the ongoing obligations in Australia and the United States.

If you're doing this yourself, you're not just setting up an entity. You're building a cross-border setup you can keep compliant without constant firefighting.

If you are planning US market entry through a US LLC from Australia, start with compliance logic, not speed. Formation steps help you launch, but they do not remove your ongoing review duties. US rules can keep applying after setup for some foreign-owned structures. State annual reporting rules vary by state and can change.

This guide gives you a compliance-first playbook with safe defaults, decision gates, and operating controls you can actually run each month. It also flags where your facts change the answer, including Australian foreign company registration triggers.

Before you start, use this operator checklist#

- Classify your operating footprint. Confirm where your entity actually carries on business, not just where you filed. In Australia, foreign company registration depends on how business is conducted, so do not assume the answer is yes or no by default. If your facts sit in a gray area, escalate to tailored advice early.

- Lock one source of truth for entity data. Keep legal name, ownership details, and signer authority consistent across your formation, tax, and banking records.

- Run recurring compliance reviews. Add a monthly checkpoint for state filings, federal review points, and Australian obligations. If your ownership and tax classification put you into a reporting context, treat foreign-ownership triggers as a standing review gate, not an afterthought.

A common failure mode is stopping at the filing confirmation. The better move is to pair formation with a standing compliance calendar and documented controls you can defend under pressure.

If you still need to validate structure fit, review Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

Can an Australian resident legally open a US LLC?#

Yes. An Australian resident can generally form a Limited Liability Company (LLC) in the United States, but formation rights do not remove operating compliance duties. Keep the decision simple: confirm you can file, then test where you must register and report. That split avoids the common mistake of treating incorporation as finished compliance.

A US LLC from Australia usually starts with state formation mechanics, not federal permission. In states such as Delaware, an authorized person files the certificate of formation. That creates your entity. It does not automatically clear every rule tied to where you actually do business in the United States, or how your structure operates in Australia.

Separate ownership from operations#

Use this rule: owning an LLC is one question, operating it across jurisdictions is another.

| Area | Question | Action |

|---|---|---|

| Ownership question | Can you, as a nonresident, form the entity? | In general, yes. |

| US operations question | Are you doing business in other US states beyond your formation state? | You may need additional state registrations. |

| Australia question | Is the foreign entity carrying on business in Australia? | Review Australian Securities and Investments Commission (ASIC) foreign company registration requirements. |

| Borderline facts question | If your setup sits in a gray area | Pause and get tailored advice before you lock in providers. |

That distinction matters in practice. You can own the LLC and still need extra state registrations in the US or a separate ASIC review in Australia.

Example: you form a US LLC for market entry, then sign clients while running delivery from Australia. You can own the entity, but you still need to test both US state activity and ASIC triggers before you assume you are fully compliant.

Run this yes/no gate before filing#

| Check | Yes | No |

|---|---|---|

| Do you need a US LLC for your international business model right now | Move to filing prep | Consider a simpler structure first |

| Will you operate in states beyond formation | Map extra state registrations | Keep scope to one state initially |

| Could the entity be carrying on business in Australia | Run ASIC review before filing spend | Document why not and recheck as facts change |

| Are facts unclear | Get tailored advice, then file | Proceed with your formation plan |

If tax residency facts still feel unclear, read A Guide to Tax Residency in Australia for Digital Nomads. Do this before you finalize entity decisions.

What should you prepare before filing anything?#

Prepare a pre-filing packet that lets you move from LLC formation to Tax ID and bank onboarding without rework. If you're an Australian founder planning a US LLC, this is where you move from eligibility checks to execution.

Build your packet before you spend#

Before you start: treat this as a sequence, not a set of separate tasks.

| Step | What to prepare | Verification |

|---|---|---|

| Define | Your business purpose and operating footprint | You can explain what your business sells, who signs contracts, and where work is performed. |

| Compile | State-form details such as principal office, mailing address, and registered agent details. If you plan a Wyoming LLC, confirm your registered agent has a physical Wyoming address. | One source-of-truth document holds every field you will reuse across state filing, EIN paperwork, and onboarding forms. |

| Draft | Articles of Organization inputs and an operating agreement for internal governance | Your signer and ownership data match across all documents. |

| Map | Your Employer Identification Number (EIN) application as its own step using Form SS-4. The EIN is a 9-digit tax ID. | Your responsible party details and legal name match your filing records exactly. |

A practical example: you run consulting from Australia and want a US LLC for client trust. This packet helps you file once, apply once, and onboard once, without rewriting the same details across forms.

Check provider fit before you commit#

| Path | What it can cover | What you must confirm |

|---|---|---|

| DIY | Full control of filing, EIN, and bank outreach | You can manage timelines and document consistency end to end |

| Stripe Atlas | Markets Delaware incorporation, EIN retrieval, then a bank-account opening flow after incorporation | Delaware fit for your model and downstream compliance needs |

| Wise Business | Supports business accounts based on onboarding eligibility | Your country, entity type, and activity qualify |

| Commenda | Markets US entity formation for foreign owners with integrated tax compliance support | Scope, exclusions, and handoff points |

Use a simple go/no-go rule: proceed only when your formation docs, EIN plan, and US business bank account path all show green.

Which state is the right fit for your operating model?#

Pick your formation state based on total operating friction, not the fastest filing path. You already built the pre-filing packet. Now make the decision that will shape your next year of compliance work. The right state is the one you can operate cleanly after launch, not just form quickly on day one.

Run the three filters in order#

- Quantify compliance overhead first. If you form in Delaware, plan for the annual LLC tax of $300.00. It is due by June 1st each year. If you form a Wyoming LLC, plan for an annual report plus a license tax based on Wyoming assets, with a minimum of $60 or $.0002, whichever is greater.

Verification point: you can put every recurring filing and payment on a calendar with a named owner.

- Map multistate activity before you file. If your US LLC will operate beyond its formation state, you may need foreign qualification in additional states, usually through a Certificate of Authority. That can mean extra taxes and annual report fees in both the new state and your home state. If you expect intrastate activity in California, register before you transact there.

Verification point: you have a state-by-state operating map for your first year of US market entry.

- Score banking compatibility and customer trust with evidence. Do not assume state choice guarantees better onboarding. Run provider pre-checks and test your buyer requirements for contracts, invoicing, and entity documents. Then connect the state choice to your downstream compliance review, including potential cross-border registration complexity if your activity footprint expands.

Verification point: you have at least one viable banking path and a documented cross-border compliance plan.

Scenario: you choose a Wyoming LLC because setup feels simple, then your sales activity clusters in California. Formation was easy. Operations may still require California qualification and added recurring filings.

Fill this scorecard before filing#

| Filter | Wyoming LLC | Delaware LLC | Your score |

|---|---|---|---|

| Compliance overhead | Annual report plus license tax (minimum applies) | Annual tax of $300.00 due June 1st | 1 to 5 |

| Expansion exposure | Foreign qualification if you operate in other states | Foreign qualification if you operate in other states | 1 to 5 |

| Banking and trust fit | Confirm with your providers and customer profile | Confirm with your providers and customer profile | 1 to 5 |

| Cross-border complexity | Test impact on your home-country compliance workflow | Test impact on your home-country compliance workflow | 1 to 5 |

Choose only when each filter is acceptable and your legal and tax assumptions are documented.

How do you form the LLC step by step with quality checks?#

Form your US LLC in a clear order: registered agent, state filing, operating agreement, EIN, then banking, and clear each quality gate before moving on. You already chose your state. Now execute without improvising.

Follow the six steps in order#

- Appoint your registered agent first. Confirm the agent can receive official legal documents in your formation state before you file anything.

Verification: you have the agent name and in-state physical address needed for filing.

- Submit your Articles of Organization. File the state formation document with your final legal name and core company details.

Verification: every state-required field matches your master entity profile.

- Archive state acceptance evidence immediately. Save the filing receipt and accepted formation record as your source-of-truth proof.

Verification: your archive includes the filing date, company name, and the key extract from your accepted filing.

- Prepare and maintain your Operating agreement. Keep ownership, signer authority, and internal decision rules current as you move into tax and banking steps.

Verification: owner names and signer permissions align with your formation records.

- Apply for your Employer Identification Number (EIN). Treat the EIN as a separate federal tax ID step after state formation. Applying before formation can create delays. International applicants may use the phone path, and fax can work when you provide a fax number.

Verification: legal name and responsible party details match your state records exactly. Track that the online flow allows one EIN per responsible party per day.

- Open your US business bank account. Start bank onboarding after you obtain the EIN, then confirm ownership and signer permissions for your international business model.

Verification: bank records and operating documents align, and you have the exact items your bank requests.

This order prevents circular delays. Many bank stalls come from document mismatches that show up during onboarding.

Recover fast when a step fails#

- Rejected filing: Compare the rejection reason against your master profile, correct mismatches, refile, then update every downstream document.

- Delayed EIN: Confirm the state accepted formation first, validate EIN application fields, then switch to phone or fax if needed.

- Banking denial: Request the exact missing items, align ownership and signer records, and retry with a backup provider using the same verified entity data.

Hard rule: do not start the next step until the current step shows green evidence.

How do you handle tax and reporting obligations across Australia and the US?#

Handle cross-border tax and reporting with a jurisdiction map, a trigger watchlist, and a fixed review cadence. After setup, this becomes an ongoing controls job.

Map obligations by jurisdiction first#

| Item | Trigger or scope | Note |

|---|---|---|

| Worldwide income in Australia | If you are an Australian tax resident | Declare worldwide income in Australia. |

| FBAR (FinCEN Form 114) | Aggregate foreign account value exceeds $10,000 at any time in the year | FinCEN filing, not an IRS filing. |

| Form 8938 | Thresholds can start at $50,000 for specified foreign financial assets for certain US taxpayers | Filing one does not replace the other. |

| Schedule SE | Net earnings hit $400 or more and your filing facts put you in scope | Mark as not relevant, possible, or in scope. |

- Classify your filing position in both countries.

If you are an Australian tax resident, declare worldwide income in Australia. Then run a separate United States status check to confirm whether US person rules apply to you personally.

Verification: you keep a one-page map that lists owner status, entity status, and account locations.

- Build a US reporting watchlist using clear triggers.

FBAR (FinCEN Form 114) is a FinCEN filing, not an IRS filing. It can trigger when aggregate foreign account value exceeds $10,000 at any time in the year. Form 8938 is an IRS filing for specified foreign financial assets for certain US taxpayers, with thresholds that can start at $50,000.

Verification: each account sits in either "monitor" or "report" with a written reason.

- Separate Form 8938 and FBAR filing mechanics.

Form 8938 and FBAR are separate obligations, and filing one does not replace the other. Confirm which, if any, applies to your facts.

Verification: you track Form 8938 and FBAR as related but distinct review points.

- Review self-employment exposure early.

Schedule SE can become relevant when net earnings hit $400 or more and your filing facts put you in scope.

Verification: you mark Schedule SE as "not relevant," "possible," or "in scope," and document why.

If you run revenue into a US account while operating cash stays in Australia, this map helps you avoid missing a trigger. It also helps you avoid discovering issues at year-end.

Run a monthly and annual compliance rhythm#

| Cadence | Action | Review with advisor gate |

|---|---|---|

| Monthly | Reconcile all Australia and United States accounts, refresh threshold tracking, and update owner status notes | Trigger status changed or new account opened |

| Quarterly | Recheck tax treaty assumptions and cross-border income characterization | Any uncertainty on treaty eligibility or income type |

| Annual | File required returns and reports when applicable | Any new filing obligation, classification change, or missing data |

If residency is the part you keep revisiting, use A Guide to Tax Residency in Australia for Digital Nomads. Treat it as a refresher before you lock decisions.

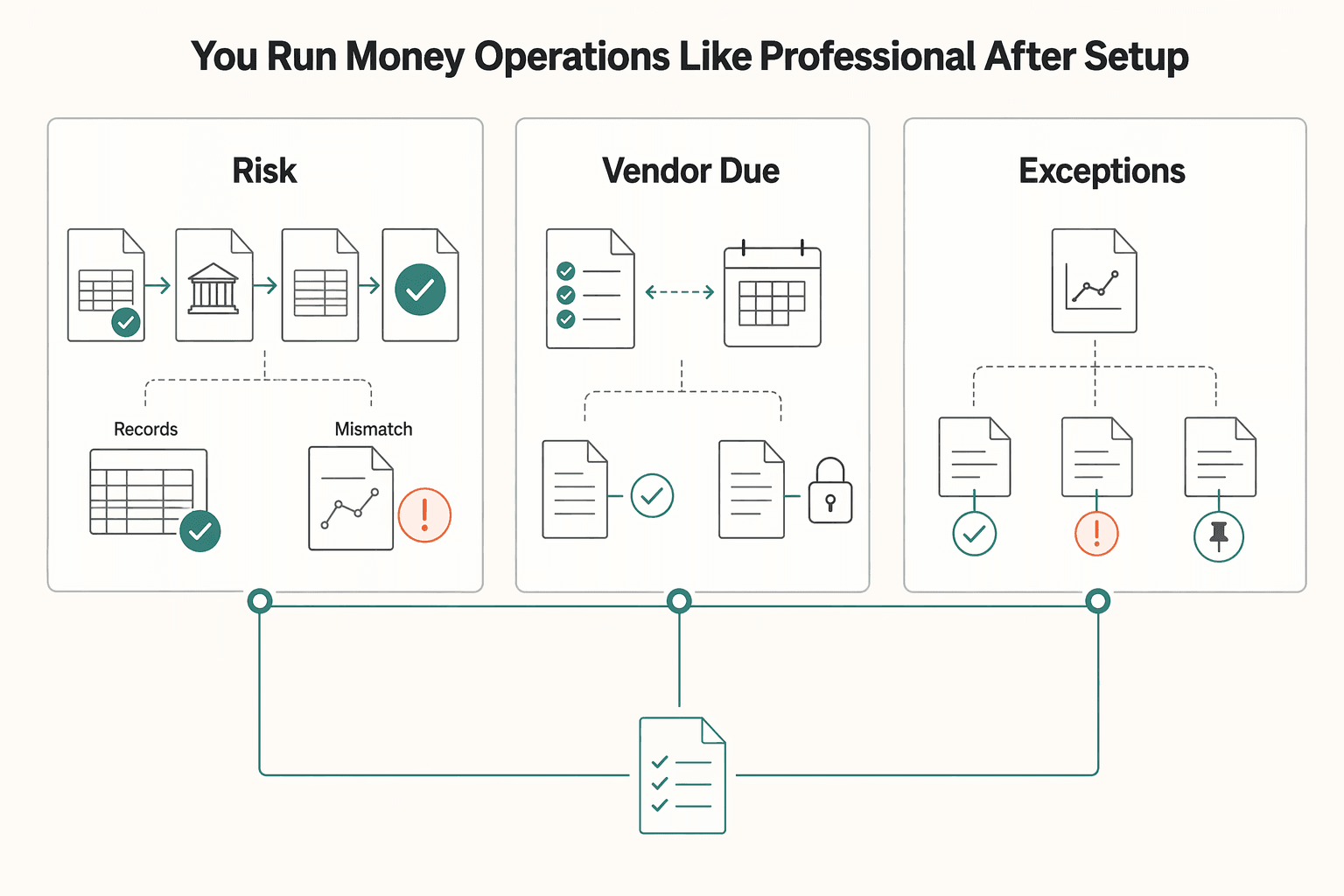

How do you run money operations like a professional after setup?#

Run money operations with strict invoice-to-settlement controls, reconciliation discipline, and auditable approvals across every payment flow. You already mapped tax and reporting triggers. Now turn them into day-to-day operating rules.

Step 1. Standardize invoice to settlement controls. Set one path for issuing invoices, collecting funds, posting entries, and confirming settlement into your business bank account. Match every incoming payment to an invoice ID and customer record before you close the period. Bank reconciliation compares bank activity against accounting records and requires follow-up on differences.

Verification: each settled payment ties to one invoice, one ledger entry, and one owner-approved exception note when mismatches appear.

Step 2. Build a compliance-first recordkeeping stack. Choose a recordkeeping system that clearly shows income and expenses, then store the documents that support book entries and tax return positions. Use a digital-first approach where possible so your Australia and United States files stay searchable during reviews. Add policy gates for high-risk events like payout destination changes, unusual refunds, or new cross-border vendors. Require traceable approvals before release.

Verification: an operator can trace any transaction from source document to ledger to bank line without guesswork.

Step 3. Place Gruv modules where control risk is highest. If you use Gruv, put it where control risk is highest: payment collection flows for receivables and payout flows for outbound money, with status visibility when enabled. Confirm module coverage for your current market and program before you depend on a workflow.

Verification: exceptions route to a defined review queue and do not silently drift.

| Control area | Safe default | Verification signal |

|---|---|---|

| Payment risk | Hold and review transactions that break normal customer or payout patterns | Release decision includes owner and reason |

| Vendor due diligence | Screen third parties before first payout and on material changes | Vendor file shows identity, business purpose, and approval trail |

| Exception handling | Route failed settlements, reversals, and unmatched entries to a single queue | Queue age stays visible and each item has a named owner |

Decision rule: if facts conflict across your LLC records, bank data, or tax positions, pause changes and fix the record first.

What mistakes cause delays and what is the fastest recovery path?#

Recover fastest by triaging four failure points in order: jurisdiction scope, entity data consistency, governance authority, and reporting watchlists. If your controls are working, you should catch most delays early.

Step 1. Run a jurisdiction check before your first invoice. Do not treat US LLC formation as complete compliance. If your activity means you conduct business in Australia, foreign company registration with ASIC can become a live requirement. Recovery: pause expansion moves, write a short jurisdiction memo, and log who owns the decision.

Verification: your file states whether ASIC review triggered, what facts you used, and what you will monitor next.

Step 2. Align entity identity across every system. Compare your Articles of Organization, Employer Identification Number (EIN) records, Tax ID references, and bank onboarding profile line by line. Small mismatches can trigger preventable rejects. Recovery: create one source-of-truth entity profile and force every form to pull from it.

Verification: legal name, EIN, and address fields match exactly across tax, banking, and accounting records.

Step 3. Tighten governance before you scale payouts. Treat the Operating agreement as your core rulebook, because it defines member, manager, and company relationships under LLC law. Then add a signer authority matrix for payments, vendor approvals, and account changes.

Verification: each high-risk action has a named approver, backup approver, and documented approval trail.

Step 4. Split FBAR and Form 8938 into separate monitoring lanes. Do not combine these obligations into one checkbox. FBAR (FinCEN Form 114) is separate from Form 8938, and FBAR files with FinCEN rather than the IRS. If US person status applies, monitor the $10,000 FBAR trigger. For certain taxpayers, Form 8938 reporting can start at $50,000, with higher thresholds in qualifying cases. If residency affects this review, see A Guide to Tax Residency in Australia for Digital Nomads.

| Delay risk | Fastest recovery action | Done when |

|---|---|---|

| Missed ASIC trigger | Run jurisdiction gate before first invoice | Written decision and monitor rule exist |

| EIN and name mismatch | Enforce source-of-truth entity profile | All records match exactly |

| Weak governance docs | Update Operating agreement and signer matrix | Authority is unambiguous |

| FBAR or Form 8938 surprise | Track each obligation separately with calendar reviews | Trigger log stays current |

Use this copy-paste checklist to launch with confidence#

Use this checklist to turn your US LLC plan into a controlled, audit-ready operation before money moves. Lock decisions into execution gates, then run the gates on schedule.

- Step 1. Confirm eligibility facts and local triggers.

- Record founder residency, service footprint, and where you conduct business. - Review local registration and compliance obligations before first invoice, then log the decision and owner. - Verification: you can show a dated yes or no decision on jurisdiction-specific registration and compliance checkpoints.

- Step 2. Finalize formation artifacts in the right order.

- Appoint a Registered Agent (if you form in Delaware, keep an in-state registered agent address). - File Articles of Organization, keep an updated Operating agreement, then apply for the Employer Identification Number (EIN) after state formation. - Verification: legal name and core entity fields match across state records, EIN records, and your internal profile.

- Step 3. Complete banking and operations readiness.

- Open your US business bank account and prepare identity fields banks verify: name, date of birth, address, and ID number. - For non-US onboarding, prepare passport number and country of issuance, plus other accepted identifiers your provider requests. - Start a monthly reconciliation workflow that matches invoices, bank lines, and ledger entries. - Verification: each payment traces from invoice to settlement to books without manual guesswork.

- Step 4. Stand up your reporting watchlist.

- Track FBAR (FinCEN Form 114) and Form 8938 as separate controls. - File FBAR with FinCEN, not the IRS, when aggregate foreign account value exceeds $10,000 at any time in the year. - Keep the FBAR due date on your calendar for April 15. - Review Form 8938 separately when thresholds apply (for certain US taxpayers, reporting can begin above $50,000 aggregate value). - Verification: your watchlist shows trigger, filing channel, owner, and due date for each item.

- Step 5. Publish your first 90-day operating plan.

- Document your state choice, compliance gates, and advisor review cadence. - Add one exception script: if a new payout request conflicts with your records or tax reporting assumptions, hold the change and resolve facts first. - Verification: your team can execute the same decision path every time.

For a structure comparison before you lock this plan, review Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

Frequently Asked Questions

Can an Australian resident legally open a US LLC?

Yes. A nonresident can legally form a Limited Liability Company (LLC) in the United States. The bigger risk is missing post-formation compliance in both Australia and the US.

Do Australians need US citizenship or a US address to form an LLC?

No US citizenship is required. You do not need to personally live at a US residential address to form the company. For Delaware filings, you do need a registered agent with a physical in-state street address.

What are the exact steps to open a US LLC from Australia?

Choose your state and registered agent, form the entity through the state, then apply for an Employer Identification Number (EIN). After the EIN, complete bank onboarding and identity verification. Before trading in Australia, check whether ASIC foreign company registration is required for your facts.

What is needed to get an EIN as a non-resident?

Form your entity through the state first, then apply for the EIN. If your principal place of business is outside the US, use the international IRS routes (phone, fax, or mail) instead of assuming online processing. Keep your legal name and entity details exact, and plan for the IRS limit of one EIN application per responsible party per day.

Can a non-resident open a US business bank account for an LLC?

Yes, but approval depends on each bank or fintech policy. Banks verify core identity fields, including your name, date of birth, address, and ID number, and they may request additional LLC documents. A Social Security number is not strictly required in every case, but onboarding requirements vary by provider.

Do I need to register a US LLC with ASIC in Australia?

You may need to, depending on whether your company conducts business in Australia. ASIC treats this as a separate compliance track from US formation. Do not assume US approval closes Australia-side duties.

What ongoing compliance tasks should I expect after formation?

Expect recurring compliance work after formation. Requirements vary by jurisdiction and by what your company actually does. If you register as a foreign company in Australia, maintain ASIC obligations such as a registered office, a local agent, and ongoing reporting.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints

The goal is a defensible, low-drama position the Australian Taxation Office (ATO) can follow from your records, not a clever workaround. For a digital nomad, that usually means keeping two tracks straight: residency and GST/ABN admin. Consistency is what holds up over time: use real facts, take steps in a clear order, and keep documents that still match months later.

The Best Podcast Hosting Platforms for Beginners

**Pick podcast hosting like an operator: optimize for control, continuity, and clean workflows, not whatever looks appealing on a pricing page.** Podcast hosting is infrastructure. What you choose at signup sits upstream of your RSS feed, Apple Podcasts listing, analytics, monetization options, and how painful it is to change systems later.