Quick Answer

To set up a power of attorney for financial matters, treat it as a cashflow continuity system, not just paperwork. Define roles, map critical accounts and obligations, choose the right document type for your jurisdiction, and grant only the powers needed to keep essential payments moving. Then complete signing formalities, verify acceptance with each institution, and maintain a revocation and review process so the setup stays usable.

Your one-session playbook to protect cashflow with a financial power of attorney#

Use this one-session playbook to set up a simple, practical plan for financial continuity when you are unavailable, while keeping authority controlled. You are not trying to master legal theory. You are setting up a continuity system so the right person can step in and keep invoices, bills, and critical transfers moving where permitted, under defined authority, if work is interrupted. If you run a business-of-one, you are the CEO, and continuity is part of the job.

| Step | Action | Verification point |

|---|---|---|

| Write the outcome in business language | State one sentence your team can test: if you cannot act, essential money operations can continue through delegated authority with clear limits where allowed | A teammate can read that sentence and name the exact tasks that must continue |

| Set the boundary up front | Use this guide as an operational framework, not legal advice, and confirm local requirements before you rely on any setup | You have a short validation list for local law and each institution you depend on |

| Lock role labels before you draft anything else | Keep principal, agent, and attorney-in-fact consistent across every checklist, file name, and approval note | Every document in your working folder uses the same role labels without conflicts |

| Run one disruption scenario | Imagine you lose access during a client payment window while a vendor bill comes due, then walk through who acts, what they can do, and what stays out of scope | You can complete the scenario without guessing responsibilities |

Before you start#

Treat this as practical continuity planning, not a paperwork project. Open your core legal documents folder, your payment tools, and your obligations list in one workspace. If your workflow crosses borders, keep your expat finance notes nearby so you can flag where local rules may change how a power of attorney works in practice.

- Write the outcome in business language.

Write one sentence your team can test: if you cannot act, essential money operations can continue through delegated authority with clear limits (where allowed). Verification point: A teammate can read that sentence and name the exact tasks that must continue.

- Set the boundary up front.

Use this guide as an operational framework, not legal advice. Rules vary by jurisdiction, and institutions may apply their own processes, so confirm local requirements before you rely on any setup. Verification point: You have a short validation list for local law and each institution you depend on.

- Lock role labels before you draft anything else.

Keep principal, agent, and attorney-in-fact consistent across every checklist, file name, and approval note. Your local form defines the formal legal meaning. Your job in this session is to remove ambiguity so no one improvises during a disruption. Verification point: Every document in your working folder uses the same role labels without conflicts.

- Run one disruption scenario.

Imagine you lose access during a client payment window while a vendor bill comes due. Walk through who acts, what they can do, and what stays out of scope. Verification point: You can complete the scenario without guessing responsibilities.

This foundation supports day-to-day control and strengthens your broader estate planning discipline. If you manage cross-border operations, A Guide to Estate Planning for Digital Nomads pairs well with this setup.

What should you prepare before you start?#

Prepare a complete cashflow map, a form decision, and a control packet before you sign any power of attorney for finances. You already set role clarity and risk boundaries. Now turn that into a setup your appointed person can execute without friction. In most of Canada, that person is often called an "attorney," and they do not need to be a lawyer.

Before you start#

Treat this as operating prep for a bad week, not admin cleanup. Your goal is to make the right actions easy and the wrong actions hard. Keep everything in one working folder so you are not assembling evidence under pressure later. Also, do not sign under pressure.

- Map every cashflow endpoint.

List all bank accounts, invoicing tools, recurring obligations, and critical transfer paths. Add owner, backup owner, and the exact action that keeps money moving for each item. Two tools often used for managing financial affairs are powers of attorney and joint bank accounts, so note where those workflows touch your current setup. Verification point: You can point to one source of truth that shows what must continue if you are unavailable.

- Choose your legal lane before you draft details.

Decide what type of power of attorney document you actually need based on your continuity goal, using the options available where you live. Confirm local rules because legal definitions vary across provinces and territories, including how they define mental capacity. Also note that a power of attorney is only valid if you are mentally capable at the time you sign.

| Decision checkpoint | What you confirm now | Output |

|---|---|---|

| Document type | Which POA format matches your continuity goal | Chosen baseline form |

| Capacity standard | How your jurisdiction defines mental capacity at signing | Signing readiness note |

| Scope boundary | Which actions support cashflow and which stay restricted | Draft authority matrix |

- Assemble your execution packet.

Prepare a draft form, identity documents, and appointment details for any signing steps your jurisdiction requires. Add a simple intake sheet you can use to track what institutions request during their review. Verification point: Your packet is complete enough to start validation without last-minute scrambling.

- Prebuild your control documents and rollback plan.

Create an authority matrix and a document inventory. Then run one hypothetical scenario: you lose access while client payments and supplier bills hit at the same time. Your attorney should follow the matrix, keep approved payments moving, and trigger your rollback plan fast if risk appears. Verification point: You and your backup can execute the scenario without guesswork.

Which powers should your agent have to keep money moving without overexposure?#

Give your agent only the powers required for critical cashflow, then expand authority only when a written trigger justifies it. You have the account map and the control packet. Now you convert that into a scope that works in the real world without handing over a blank check.

Use this as an operational framework, not legal advice. Jurisdictions and institutions differ, so validate your final language and process before execution.

Consider building a narrow permission ladder first#

- Define essential powers for daily continuity.

Draft a minimum set of actions tied to real operations: for example, routine bill pay, access to selected bank accounts for operations, and urgent vendor or client payment actions. Mark each item as proposed scope in the document. Verification point: Every essential power maps to a specific payment workflow in your account map.

- Separate expanded powers from exceptional powers.

Create a second tier for actions you may allow later and a third tier for high-impact actions that need written triggers. Consider treating real estate transactions and broad asset moves as exceptional until you complete stricter review.

| Tier | Purpose | Control rule |

|---|---|---|

| Essential now | Keep invoices and bills moving | Agent can act within documented limits |

| Expanded later | Handle less frequent operational tasks | Consider requiring prior written approval by the principal |

| Exceptional only | Cover high impact decisions | Consider requiring a written trigger, extra review, and explicit recordkeeping |

- State role boundaries in plain language.

Write three short lists: what the agent may do, what needs prior approval, and what remains reserved to the principal. Keep the language concrete so your team can execute quickly during a disruption.

- Stress test before final signoff.

Run one hypothetical scenario where you are unreachable during a client payout cycle. The agent follows the essential tier, escalates anything outside scope, and records each action for audit and continuity. Verification point: Your process keeps payments moving without ad hoc decisions.

If you handle cross-border operations, review A Guide to Estate Planning for Digital Nomads to align this control model with expat finance realities.

How do you choose an agent with real risk controls?#

Choose an agent who follows written controls, stays inside scope, and can execute your cashflow system under pressure. The permission ladder is only as safe as the person running it.

A power of attorney is a legal document that gives someone authority over money and property, so treat the role like access to production systems. Your attorney does not need to be a lawyer, but you are still delegating significant power. Keep pressure out of the decision, make sure you are mentally capable at the time you sign, and confirm local rules because requirements vary by jurisdiction.

Score candidates by operational fit#

- Step 1. Rank critical workflows first.

List the money tasks that cannot stop, then map each task to the level of trust and response speed it needs. Pick by workflow criticality, not by family role or personal closeness alone. Verification point: Every task has a named primary owner and a backup decision owner.

- Step 2. Score each candidate with objective criteria.

Use a simple screen before you name an agent.

| Criteria | What to check | Fail signal |

|---|---|---|

| Trust history | Follows boundaries and documents decisions | Ignores agreed controls |

| Financial reliability | Handles routine money tasks accurately | Repeated avoidable errors |

| Responsiveness | Acts quickly during payment issues | Delays urgent actions |

| Control discipline | Uses logs and approvals consistently | Makes side decisions offline |

Install abuse prevention and continuity gates#

- Step 3. Set abuse prevention gates in writing.

For exceptional actions, set a dual-review expectation, keep action logs, and define immediate escalation for suspicious account activity. Treat these as practical operating controls you put in writing (and, where supported, into your legal paperwork), not as universal legal requirements.

- Step 4. Name a backup path before you sign.

Designate a successor agent and state when control shifts. This can reduce the risk of urgent last-minute intervention if your first choice cannot serve. Imagine you become unreachable during a client payment cycle. Your backup steps in, follows the same controls, and keeps cashflow moving without improvisation. Verification point: Your backup can run the workflow from your written playbook on the first pass.

If you manage cross-border operations, review A Guide to Estate Planning for Digital Nomads so your expat finance setup stays consistent. Want a quick next step for "power of attorney for finances"? Try the free invoice generator.

How do you execute and activate the document so institutions actually accept it?#

Use a jurisdiction-checked form, a controlled signing packet, and an account-by-account activation log to improve real-world acceptance by the institutions you depend on. Design is cheap. Acceptance is the real test.

Run an acceptance first execution sequence#

- Step 1. Validate the form against your legal lane.

If your jurisdiction offers a statutory template, compare your draft line by line before signing. These forms often warn that granted powers can be broad and may allow you to grant less than everything listed. Verification point: The principal can explain exactly which powers are included and excluded.

- Step 2. Confirm signing readiness and complete execution.

Confirm the principal is mentally capable at signing, then complete execution using the signing requirements that apply in your jurisdiction (for example, notarization where required). Preserve signed originals and prepare a controlled copy set for institutions. Label each file clearly so the agent uses the current version only. Verification point: You can locate originals, controlled copies, and version history in under a minute.

- Step 3. Drive institution acceptance account by account.

Do not assume one valid Personal Financial Power of Attorney will pass everywhere. Institutions can refuse acceptance or request supplemental forms, so run a submission workflow for each bank and platform.

| Activation element | What you decide now | Output |

|---|---|---|

| Submission owner | Who sends and follows up | Named owner and backup |

| Required documents | Which forms each institution asks for | Institution checklist |

| Acceptance evidence | What confirms acceptance | Date, contact, reference note |

- Step 4. Document activation and shutdown logic in writing.

State when authority starts and when it ends. Spell out how revocation works and what happens if an agent cannot or will not act, so the principal and agent do not improvise under stress. Imagine you lose access during a payout week. Your agent follows the written trigger, executes approved actions, and stops when the end condition appears.

If your workflow spans borders, review A Guide to Estate Planning for Digital Nomads so your expat finance process stays aligned.

If you want a deeper dive, read Japan Digital Nomad Visa: A Guide to the New 2025 Program.

How do you run an audit-ready POA workflow after signing?#

Run your financial POA as a recurring control cycle after signing. Execution and acceptance get you to baseline. The workflow keeps it usable.

Manual, paper-heavy POA handling creates bottlenecks and avoidable errors. When reviews drift or documents go stale, you increase the chance of delays, rejected actions, and unauthorized transaction exposure.

Build a living register and evidence trail#

- Step 1. Create one control register for all financial accounts and endpoints.

Track each account, submission date, acceptance status, scope notes, and reference IDs in one place.

| Field | What you track | Why it matters |

|---|---|---|

| Endpoint | Bank or platform name and account purpose | Links authority to real cashflow |

| Acceptance status | Pending, accepted, rejected, rework needed | Prevents false confidence |

| Authority scope | Allowed actions under your legal documents | Stops out of scope requests |

| Reference record | Case ID, contact, decision date | Supports fast follow up |

- Step 2. Maintain a clean evidence file.

Store signed versions, institution acknowledgments, and change logs tied to principal approval records. Keep version labels strict so your team never uses stale files. Verification point: Use documented review layers to confirm signatures, notarization, completeness, and jurisdiction-specific legal requirements. You should also be able to prove who approved each change and which version is active.

Run monthly controls and incident response#

| Control | Trigger | Action |

|---|---|---|

| Review scope against current risk | Every month | Check whether your POA still matches current operations, vendor exposure, and team structure |

| Prewrite incident actions for misuse risk | Before an incident | Define triggers for revocation steps, institution notifications, and immediate access lockdown |

| Document jurisdictional variance explicitly | If you operate across jurisdictions | Track where validity and acceptance can differ by jurisdiction, provider, and compliance program, then verify locally before relying on authority |

- Step 3. Review scope against current risk every month.

Check whether your POA still matches current operations, vendor exposure, and team structure. This is an operating cadence for financial planning and estate planning discipline, not a universal legal requirement.

- Step 4. Prewrite incident actions for misuse risk.

Define triggers for revocation steps, institution notifications, and immediate access lockdown (for example, credential rotation where relevant). Run one hypothetical drill: a suspicious transfer appears while you are unreachable, and your backup follows the script without debate. Verification point: The team can execute the revocation and access-lockdown plan using the same documented playbook.

- Step 5. Document jurisdictional variance explicitly.

If you operate across jurisdictions, track where validity and acceptance can differ by jurisdiction, provider, and compliance program, then verify locally before relying on authority.

If you operate across jurisdictions, A Guide to Estate Planning for Digital Nomads helps align this control system with broader estate planning decisions.

What mistakes cause payment disruptions and how do you recover fast?#

Payment disruptions often come from four avoidable breakdowns in a financial power of attorney: authority that is too broad, false acceptance assumptions, poor revocation readiness, and no backup authority path. A regular review should catch these early, before they block invoices, vendor payments, or approvals.

Practical usability means banks and platforms honor your Financial Power of Attorney (FPOA) when pressure hits, not just that the document looks valid in a file.

| Mistake | What breaks first | First recovery move |

|---|---|---|

| Broad powers with no boundaries | High-risk misuse exposure | Reissue with a tighter permission ladder |

| One-form-fits-all assumption | Institution rejection and delays | Run an acceptance sweep across all bank accounts |

| No revocation readiness | Slow incident response | Pre-draft and stage a revocation package for your financial POA |

| No backup continuity | Decision bottleneck if agent is unavailable | Define alternate authority and handoff triggers |

Run this four-step recovery sweep#

- Step 1. Tighten authority scope immediately.

Rewrite your financial power of attorney with clear boundaries and explicit exclusions for actions you do not want delegated. Keep routine cashflow powers clear, narrow, and testable. Verification point: Your agent can execute routine payment actions, and your document limits excluded actions without interpretation fights.

- Step 2. Validate acceptance endpoint by endpoint.

Do not assume one signed form works everywhere. A legally valid older or grandfathered POA can still fail in practice, and cross-jurisdiction use can trigger refusal questions. If there is more than one POA in circulation, third parties may also question which one is valid. Institutions may update their internal requirements over time. Verification point: Every institution record shows accepted, rework needed, or rejected, plus the exact supplemental forms required.

- Step 3. Operationalize revocation before you need it.

Store a draft-ready revocation template, notification list, and escalation script with your legal documents. Run one drill: you are unreachable, suspicious activity appears, and your backup executes notifications without improvising. Verification point: Your team can trigger revocation communications in one controlled workflow.

- Step 4. Build continuity beyond one person.

Name an alternate authority path and document when control transfers from the primary agent. This reduces emergency dependence on last-minute workarounds when continuity matters most, especially when finances span jurisdictions.

If your estate planning spans borders, pair this recovery workflow with A Guide to Estate Planning for Digital Nomads.

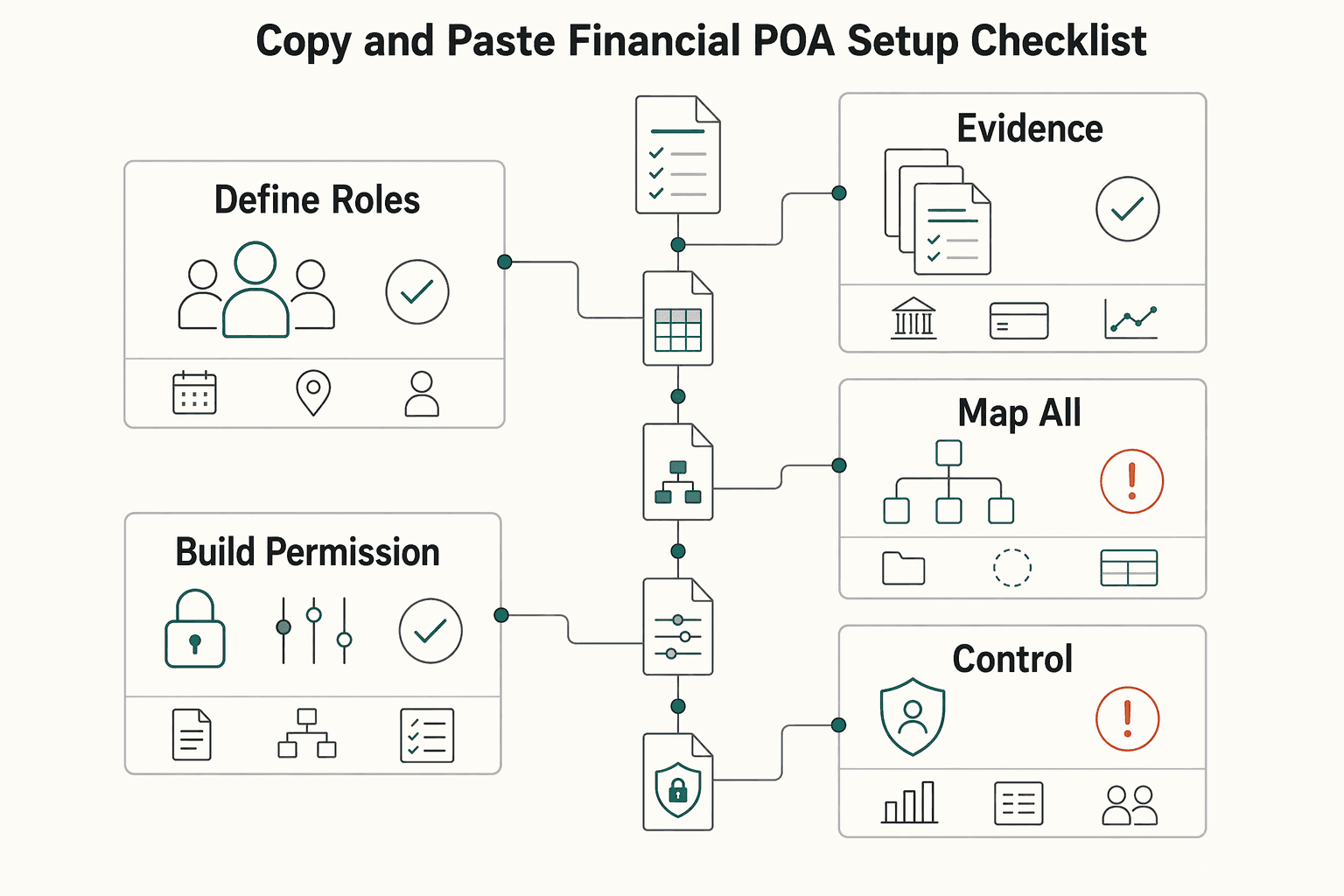

Copy and paste financial POA setup checklist#

Use this checklist to run the setup as a controlled system that keeps cashflow moving and limits downside risk. This is the same system you built above, compressed into one runbook.

| Step | Focus | Verification point |

|---|---|---|

| Define roles before you draft authority | Name the principal, the agent, and the attorney-in-fact in plain language | Your team can explain who approves, who executes, and who escalates |

| Choose the right document type for your actual workflow | Select a durable power of attorney or a jurisdiction-appropriate equivalent when that is the right fit; POA types include general, limited, durable, and non-durable | Your document type matches your risk window and operating needs |

Map all operational bank accounts by payment priority | List invoicing inflows, bill pay outflows, and critical transfer paths, and define exactly what the attorney-in-fact may do | Every account has a clear priority and allowed action set |

| Build a permission ladder with explicit exclusions | Start with routine cashflow actions, then add higher-risk powers only with written triggers; put real estate transactions in an exception lane unless you intentionally authorize them | Your Financial Power of Attorney (FPOA) separates routine authority from exceptional authority |

| Complete execution and acceptance controls | Finalize signing, complete any required formalities, submit to each institution, and log acceptance evidence | Each institution status reads accepted, rework needed, or rejected |

| Stage revocation and set your review rhythm | Store signed originals, controlled copies, and a ready revocation plan in one access-controlled system, then set a review rhythm | A backup operator can locate current records and run the handoff workflow immediately |

- Step 1. Define roles before you draft authority.

Name the principal, the agent, and the attorney-in-fact in plain language. Role clarity protects execution speed and control boundaries. Verification point: Your team can explain who approves, who executes, and who escalates.

- Step 2. Choose the right document type for your actual workflow.

Select a durable power of attorney (or a jurisdiction-appropriate equivalent) when that is the right fit for your use case. POA types include general, limited, durable, and non-durable, and a limited model can fit specific tasks for a defined timescale. Verification point: Your document type matches your risk window and operating needs.

- Step 3. Map all operational

bank accountsby payment priority.

List invoicing inflows, bill pay outflows, and critical transfer paths. For each account, define exactly what the attorney-in-fact may do, including practical powers like receiving income owed to the principal when appropriate. Verification point: Every account has a clear priority and allowed action set.

- Step 4. Build a permission ladder with explicit exclusions.

Start with routine cashflow actions, then add higher-risk powers only with written triggers. Put real estate transactions in an exception lane unless you intentionally authorize them. Verification point: Your Financial Power of Attorney (FPOA) separates routine authority from exceptional authority.

- Step 5. Complete execution and acceptance controls.

Finalize signing, complete any required formalities (which may include notarization, depending on your jurisdiction or institution), submit to each institution, and log acceptance evidence. Treat commercial templates carefully because some providers are not affiliated with any government organization. Verification point: Each institution status reads accepted, rework needed, or rejected.

- Step 6. Stage revocation and set your review rhythm.

Store signed originals, controlled copies, and a ready revocation plan (including any revocation document your jurisdiction or institution expects) in one access-controlled system. Set a review rhythm (for example, quarterly) and revisit after major business or location changes as part of ongoing financial planning, estate planning, and expat finance risk control. Verification point: A backup operator can locate current records and run the handoff workflow immediately.

Hypothetical scenario: you lose access during a payout cycle, and your backup executes this checklist cleanly without improvising. If you run cross-border operations, pair this with A Guide to Estate Planning for Digital Nomads.

Put this system in place before the next disruption#

Your Financial Power of Attorney (FPOA) protects revenue best when you run it as an operating control system, not a one-time document. Put your setup materials, scope decisions, and institution acceptance tracking on a cadence so it is ready before you need it.

Use one safe default rule: start narrow, prove acceptance, then expand only when risk clearly justifies broader scope. Keep the principal, agent, and attorney-in-fact aligned on this rule so no one improvises under pressure.

| Control rule | Action this week | Evidence to keep |

|---|---|---|

| Start narrow | Keep authority focused on essential payment continuity actions | Current scope summary signed off by owner |

| Prove acceptance | Validate each institution process and record status | Acceptance log with pending and completed items |

| Expand with intent | Broaden authority only after a documented risk review | Change record with reason and approval |

- Step 1. Run your checklist end to end.

Assign an owner, due date, and status for every item from setup through incident readiness. Treat your chosen POA form as a living operating asset, not static paperwork. Verification point: No checklist item sits without an owner or next action.

- Step 2. Test acceptance and handoff in one pass.

Walk through institution handling, exception escalation, and backup handoff readiness as one connected workflow. Hypothetical scenario: the primary operator loses access during a payment week, and the backup completes the handoff cleanly without debate. Verification point: The team completes the drill with no blocked decision point.

- Step 3. Build for document drift and policy updates.

Formal filings can be amended over time, and some official presentations explicitly state they are not legal advice, so keep version control, review notes, and approval history current. Verification point: You can show the active version, last review date, and decision trail in minutes.

If your cashflow spans borders, add policy gates, status visibility, and audit-ready records as standard operating practice. For cross-border planning context, review A Guide to Estate Planning for Digital Nomads. Related: A Guide to Superannuation for Australian Freelancers.

Frequently Asked Questions

What is a power of attorney for finances in plain terms?

A power of attorney for finances is a legal document that gives someone else legal authority to handle money and property for you. You sign the document to appoint that person (often called an “attorney” under the POA), and in this role, attorney does not mean lawyer.

What can an agent do under a financial POA and what stays off-limits?

Whatever you authorize in writing is in scope, and everything else is out. You can grant broad authority for many financial or legal actions, or limit authority to specific tasks like deposits, withdrawals, and bill payments. Write boundaries and exclusions in plain language, then tie them back to your account map and authority matrix.

When does a continuing/enduring financial POA start and end?

Your document defines the start trigger, so write that trigger clearly. A continuing or enduring POA continues if you become incapable, while a non-continuing/enduring POA stops at that point. You must sign while mentally capable for the document to be valid.

Do I need notarization and bank-specific forms for acceptance?

Do not assume one process works everywhere. Local rules and institutions can set different acceptance standards, so confirm requirements before you rely on your financial POA. Plan for extra institution paperwork and track each acceptance decision in your activation log.

How should freelancers choose an agent safely?

Choose someone who follows controls, communicates quickly, and respects boundaries under stress. Walk them through your permission ladder, logging expectations, and escalation rules before you sign. If anyone pressures you to sign, stop and reassess, because you should never feel pressured to sign a power of attorney.

Can a financial POA keep invoices and bills moving if I am unavailable?

Yes, if you grant those powers explicitly and the institution accepts the document. Depending on what you authorize, a POA can let your attorney handle day-to-day banking tasks such as bill payments, deposits, and withdrawals while you are unavailable. The difference between theory and reality is your acceptance evidence and your ability to audit actions after the fact.

Is one financial POA valid across all states or countries?

No. Jurisdiction rules differ, and institutions can interpret requirements differently, so one document may not work everywhere. If you operate across borders, validate your setup country by country and institution by institution before you depend on it.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

Estate Planning for Digital Nomads: Legal Intent and Cashflow Continuity

Treat estate planning for digital nomads as a two-part continuity system: legal intent plus operational execution, so your business keeps moving when you cannot. The common trap is thinking, "I have a will, so I'm covered." If you run a business-of-one, cashflow, logins, and process often live in your head until you deliberately externalize them.

A Guide to Superannuation for Australian Freelancers

**Treat superannuation for freelancers australia as a repeatable operating decision, not a guess you make under invoice pressure.** As the CEO of a business-of-one, your job is to turn fuzzy compliance questions into a simple system you can run on demand. Freelance income moves, contract terms shift, and one wrong super call can squeeze cashflow or create a compliance problem you only notice later.