Quick Answer

Set freelance financial goals by building a repeatable get-paid system, not just setting bigger revenue targets. Start with protective policies (tax reserve, low-month buffer, account separation), then run a weekly cashflow scorecard and a pre-client risk check on every project. Use deposits, milestone terms, and a consistent invoice follow-up ladder so payment timing and risk are controlled before problems escalate.

You don't need "bigger goals" - you need a get-paid system you can run on every client#

Build your goals as repeatable policies and habits you can actually follow, not motivational slogans. You run a business-of-one. Your job is to install a system that still works when you're busy, tired, or too close to the work to think clearly.

A solid system tells you what to say yes to, what "done" means, and how you handle the admin that keeps money moving.

Step 1: Turn "goals" into purpose, then into policies#

Start with intent, because it survives messy weeks. One freelancer-focused piece defines purposefulness as: "Purposefulness is the quality of knowing what you intend to do." Use that as your anchor, then translate it into outcomes you can operate. That same piece also raises the idea that focusing too much on goals can be harmful, and points you back toward purpose rather than results alone.

Do this in order, so you end up with rules you can execute:

- Write your purpose in one sentence. Example: "I deliver high-quality client work without wrecking my capacity."

- Choose targets you can measure weekly. Keep it tight: revenue you bill, what you keep after costs, and a couple of operational targets, like how much time you spend on delivery vs admin.

- Convert each target into a policy you can follow without negotiating with yourself. Policies beat willpower, and they keep you from building a plan that only works on your best days. A creator described a burnout turning point as doctors saying her way of working was "unsustainable." Treat that as a warning label for any plan that relies on heroic effort and memory.

Here's the translation layer you'll use as you set targets:

| Goal category | Track weekly | Policy that makes it real |

|---|---|---|

| Revenue targets | Work billed/sent | Decide your quoting and scope boundaries before you commit |

| Profit goals | Key business costs | Set a simple spending rule you can stick to |

| Capacity | Delivery hours vs admin | Block non-negotiable time for admin and recovery |

| Predictability | What slipped and why | Add one "prevent this next time" rule after each miss |

Step 2: Install a simple client loop (with a quick sanity check)#

Run this loop on every client. Make it your default.

| Loop step | Focus | Article detail |

|---|---|---|

| Gate the start | Get clarity in writing | What you're doing, what "done" means, who signs off, and what happens when the work changes |

| Sanity-check the risk | Ask the same fast questions | Is the work clear enough to start? Is the timeline realistic? Do you trust the communication? Are your start conditions accepted? |

| Execute the workflow | Use the same trigger each time | Handle billing, reminders, and tracking what was agreed; keep the essentials in one place |

Step 1: Gate the start. Before you begin, get basic clarity in writing: what you're doing, what "done" means, who signs off, and what happens when the work changes.

Step 2: Sanity-check the risk. Ask a few fast questions you can answer consistently: Is the work clear enough to start? Is the timeline realistic? Do you trust the communication? Are your start conditions accepted?

Step 3: Execute the workflow. Use the same trigger each time to handle the admin you tend to avoid: billing, reminders, and tracking what was agreed. Keep the essentials in one place so you're not reconstructing history from memory.

Hypothetical scenario: a new client wants to "start Monday" but won't confirm deliverables in writing. Your system makes the call for you: no clarity, no kickoff. You do not second-guess it.

Before you start: prep your inputs (so your goals aren't fiction)#

Collect a clean baseline of real cash movement, then organize it so you can measure, repeat, and defend your decisions.

If your inputs are messy, your goals turn into wishful thinking. Your targets drift away from what your bank balance can actually support.

Step 1: Gather your "money truth" (a recent, representative window)#

Pull a recent slice of your finances that reflects how you actually operate, not your best month ever. You are building a usable starting line, not a perfect audit.

Use this data map to pull what you need and capture it consistently:

| What you need | Where to pull it | What to capture |

|---|---|---|

| Invoices sent | Invoicing tool | invoice ID, issue date, due date, amount, client |

| Payments received | Business bank statements | deposit date, amount, payer name, reference/memo |

| Platform income | Platform exports (often labeled Payouts) | payout ID, settlement date, net amount, fees |

| Fee leakage | Processor/platform reports | processing fees, FX charges, refunds |

| Refunds/chargebacks | Processor/platform logs | date, reason code (if shown), amount |

Verification point: you can match each paid invoice to a bank deposit or payout line item without guessing.

Step 2: Separate accounts and paperwork so you can operate weekly (not scramble yearly)#

If it fits your situation, separate your money flows, for example one account for operating cash and another you treat as a tax reserve. This keeps planning simpler, reduces missed transfers, and gives you cleaner records when someone asks, "What happened here?"

Next, create a client folder template, one folder per client, and drop in the docs you actually rely on to prevent scope and payment disputes.

Finally, choose your year-end tax paperwork stance early. If you are an employee, employers use Form W-2 (Wage and Tax Statement) to report wages paid and furnish it to you and the Social Security Administration, which shares the information with the IRS. If you are an independent contractor, payers may use Form 1099-NEC (Nonemployee Compensation) to report certain payments, including when payments total $600 (and $2,000 for payments made after December 31, 2025). Track which forms you expect from payers, and keep your records organized so year-end paperwork does not turn into a reconstruction project.

5-minute practical check: Can you answer, from records, "Which three clients paid slowest, and what terms did I agree to?" If not, set your first goals to visibility before growth.

Hypothetical scenario: you feel tempted to set aggressive revenue targets, but you cannot tell whether late payers cluster around net-30 terms. You pause goal-setting, standardize your invoice naming, and rebuild your baseline. That move prevents you from scaling chaos.

Step 1: Lock in the non-negotiables (tax reserve, buffer, and clean separation)#

Treat your goals as protective policies first: taxes, a buffer for volatility, and hard separation between business cash and personal spending.

These guardrails keep your plan intact the first time a client pays late or a tax bill lands.

1) Set a tax reserve policy you can execute#

Pick a repeatable reserve rule, then refine it to your jurisdiction and your real tax situation. You will see people throw around simple rules of thumb online. Use those only as a temporary placeholder if you lack a better number.

Replace it with a figure based on your own situation, and professional advice where needed.

Verification point: before you take owner pay, you can show that you already moved money into a dedicated tax reserve bucket.

2) Write a low-income-month buffer policy (with triggers)#

Freelance finance breaks when you treat buffers like optional savings. One cited freelance finance source reports that 60% of freelancers face monthly fluctuations of over 30%, so plan for a down month as normal operations.

Define:

- Buffer minimum: your baseline bills and commitments, using the period that fits your risk tolerance.

- Trigger rule: if the buffer drops below your minimum, you pause optional spend and tighten terms, for example by requiring deposits on new work until you rebuild.

Hypothetical: a reliable client slips payment timing by a few weeks. Your buffer trigger activates, you stop discretionary tooling upgrades, and you require a deposit for any new scope. You stay calm because the policy already made the decision.

3) Separate accounts to contain risk and stop "phantom profitability"#

Separation makes decisions obvious. The goal: business income stays in the business lane until you allocate taxes and owner pay. One source puts it simply: "Keep business and personal accounts separate for clarity."

If you're in France, the same source notes that a dedicated compte pro becomes legally required once annual revenue exceeds €10k.

Either way, separation stops you from confusing "cash that arrived" with "cash you can spend."

| Bucket | Purpose | Default rule |

|---|---|---|

| Business account | Collect client payments, pay business expenses | No personal spending here |

| Tax reserve | Hold money you do not touch | Fund it before owner pay |

| Owner pay (personal) | Your living costs | Pay yourself on a set cadence |

Verification point: you can explain every transfer in one sentence: what it was, why you moved it.

4) Make retirement and benefits a cashflow goal#

Stop funding retirement "in good months." The IRS notes that if you're self-employed, "you have many of the same options to save for retirement on a tax-deferred basis."

Two examples the IRS highlights:

- SEP: contributions can be up to 25% of net earnings from self-employment, up to $69,000 for 2024.

- 401(k): annual salary deferrals up to $23,000 in 2024, plus an additional $7,500 (2023 and 2024) if you're 50 or older.

And if you choose a SEP, the IRS also notes you can set it up for a year as late as the due date, including extensions, of the income tax return for that year.

Operational move: tie retirement, and other must-fund benefits you're responsible for, to a percentage of paid invoices, so it happens by design, not luck.

Step 2: Turn "financial goals" into a cashflow scorecard you can actually run weekly#

Turn your goals into a weekly scorecard that makes the next decision obvious. At its core, this is cash flow: understanding how much money comes in and where it goes so you can plan realistically and avoid the paycheck-to-paycheck scramble.

The point is not to track more. The point is to make the next decision obvious.

1) Define the goal categories (so "growth" doesn't hide risk)#

It is easy to over-focus on revenue and profit. Those matter, but they do not always show whether your timing is tight or whether you are about to run into a cash pinch. One simple way to keep yourself honest is to separate "how much" from "when."

| Goal category | Definition | Weekly question it answers |

|---|---|---|

| Revenue goal | What you bill | "Did I ship billable work?" |

| Cost/profit goal | What you keep after business costs | "Did costs creep up?" |

| Cash flow goal | What comes in and what goes out | "What changed in the way money moved this week?" |

| Timing goal | Whether cash arrives before expenses hit | "Do I have enough cash on hand before the next bills are due?" |

Operator move: note any friction that can slow cash, like approval steps, new client setup, or extra admin. The goal is not perfect labeling. It is to stop treating preventable blockers like "random delays."

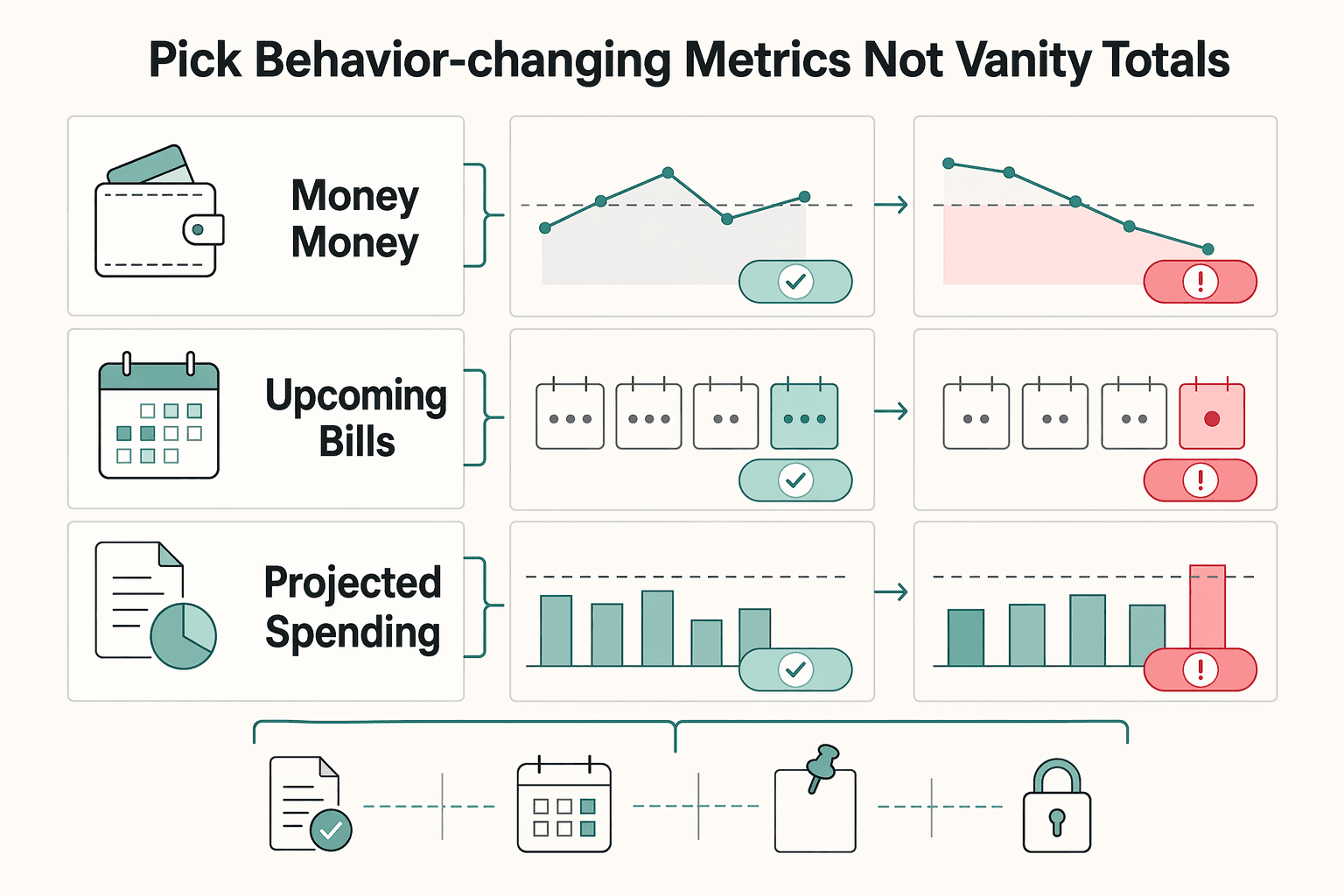

2) Pick behavior-changing metrics (not vanity totals)#

Totals hide the truth. Weekly metrics force action. Keep the list short, then standardize definitions so you can compare week to week.

| Metric | What it tracks | Why it matters |

|---|---|---|

| Money in vs. money out (cash flow) | What came in and where it went | Plan realistically instead of guessing |

| Upcoming bills and expected income | What is due soon and what you expect to receive | So nothing surprises you |

| Projected spending-account balance | How your spending-account total changes over time | A forward-looking estimate based on entered bills and expected income |

Hypothetical: your revenue looks fine, but your projected balance dips below comfort before the next round of bills. You do not chase more leads. You adjust the plan: tighten spending, move a billable milestone earlier, or follow up on outstanding work so expected income becomes real cash sooner.

Verification point: you can explain each metric in one sentence and tie it to a decision. Momentum Financial Coaching frames this well: "Money Management is the art of organizing, planning, and adjusting your finances so you can achieve your financial goals."

Practical check: if you cannot update the scorecard quickly on Monday, simplify. The scorecard should help you fix cash flow, not create more work hunting for numbers.

What financial goals should you prioritize first (so you don't build on sand)?#

Prioritize clean payout records and information-return tracking (Form 1099 and, if you have employees, Form W-2) before you scale subcontracting or set aggressive growth goals. It is hard to run a stable freelance business when your reporting and records are fuzzy.

If you want a simple operator rule: clean up the paperwork first, then turn up the volume.

Track the forms that map to how you pay people#

- If you pay employees, employers use Form W-2 (Wage and Tax Statement) to report wages paid to an employee. Employers furnish Form W-2 to the employee and the Social Security Administration (SSA), and the SSA shares that information with the IRS.

- If you pay nonemployees in your business, the IRS notes that payers use Form 1099-MISC and/or Form 1099-NEC to report certain payments and to report any amount of federal income tax withheld under the backup withholding rules.

If you subcontract, make recordkeeping part of the goal#

Add targets for: (1) clear payment timing, (2) signed agreements, and (3) audit-ready payout records. Keep clean Payouts logs and track whether you may need Form 1099 reporting.

Concrete thresholds the IRS highlights, in its Form 1099-MISC discussion, include:

| Threshold | Payment type | Article note |

|---|---|---|

| $10 or more | Royalties; broker payments in lieu of dividends or tax-exempt interest | During the calendar year |

| $600 | Certain payments | During the calendar year |

| $2,000 | Certain payments | For payments made after December 31, 2025 |

For a step-by-step operator playbook, use Hiring Your First Subcontractor: Legal and Financial Steps.

Practical check: if one large client pays late, can you still cover taxes plus baseline bills from your buffer? If not, your next move is stability, buffer and tighter terms, not lead gen.

How do you decide if a client is financially safe to work with? (10-minute go/no-go scorecard)#

Run the same short risk scorecard before every kickoff, and let the scorecard decide your terms or your "no," not your excitement.

This is how you protect cash timing and payment certainty before you get emotionally committed.

Step 1: Run the pre-engagement risk check (before you feel committed)#

Open a doc, set a 10-minute timer, and check these four boxes. If you can't check them, don't "hope it works out." Tighten the terms or walk.

| Scorecard item | What you want to see | If it's missing, do this |

|---|---|---|

| Contract readiness | A signed SOW (or equivalent) that states scope, milestones, and acceptance criteria | Convert "verbal yes" into written milestones. Don't schedule kickoff until they sign. |

| Legal clarity | Clear agreement on the basics of how disputes would be handled (whatever you and the client decide to document) | Ask directly: "If there's a dispute, where does it get handled?" Write down the answer in the contract or SOW if that's how you're operating. |

| Payment protection | Terms that cap your "max exposure" (upfront payment and/or smaller paid milestones) | Break work into smaller, paid checkpoints. Tie each checkpoint to a deliverable and acceptance. |

| Payment method | A method with low dispute exposure for your situation (often bank transfer where feasible, including Virtual Accounts where enabled) | Offer two options and state the fee and confirmation details upfront. |

Hypothetical: a new brand wants a fast turnaround, but they also want to "sort paperwork later." Your scorecard fails on SOW and payment protection. You respond with a smaller first milestone plus upfront payment to book the slot. If they resist, you just learned what month two will feel like.

Step 2: Lock in compliance and tax basics early (so money doesn't stall later)#

Treat onboarding paperwork as part of getting paid.

- US-based clients: collect whatever vendor onboarding details and tax paperwork they require before they can pay you.

- Cross-border: ask what documentation they require before they can pay, and who handles any relevant indirect taxes, where applicable. If a client asks for proof of U.S. residency certification, know that the IRS ties that request to Form 8802 ("Application for United States Residency Certification"). If the client mentions Form 6166, see: Form 6166 and IRS residency certification paperwork.

Practical check: if the client fails 2+ items, default to "tighten terms" - higher upfront payment, smaller milestones, shorter net terms, clearer acceptance - or decline. This one policy protects every other goal in your business planning.

If you want a deeper dive, read How to Set Up a US LLC from Australia.

If you need a quick next step, try the free invoice generator.

Step 3: Design payment terms that hit your goals (deposits, milestones, and leverage points)#

Use deposits plus a milestone ladder to control cash timing and cap your downside, then write terms that make payment triggers unarguable.

The goal is not to sound "tough." It is to make payment routine.

1) Build a milestone ladder that caps exposure (deposit, checkpoints)#

Start by designing your billing schedule around collection reality, not optimism. One practical approach: "Bill clients at milestones or every two weeks, offer ACH and card payments, and ask for deposits from new clients." That structure keeps cash moving even when a project drags.

Run this ladder like an operator:

- Collect a deposit to book the slot. Treat it as a scheduling gate, not a "nice to have."

- Break the project into milestones you can prove. Tie each milestone to a concrete deliverable inside the SOW so it's easy to see what was delivered and what triggers the invoice.

- Keep money moving with a cadence. Bill at milestones, or on a regular cadence like every two weeks, instead of waiting for "the big finish."

- Make it easy to pay. Offer ACH and card options.

Hypothetical: a client wants "one big delivery at the end." You counter with a deposit plus smaller milestones tied to tangible outputs. If they push back, you just found the leverage point that would have turned into month-two cash stress.

2) Reduce ambiguity (revisions, scope, inputs, due dates, follow-up)#

Disputes usually start with fuzziness. Fix it up front.

- Define revision rounds and scope edges. Write what counts as a revision, what counts as "out of scope," and how you quote add-ons.

- Assign responsibilities for inputs. List what the client must supply, access, copy, approvals, and what happens when they stall.

- Set payment due dates as a policy so you stop renegotiating every project. Choose due dates that match your cash-flow goals and the client's risk profile.

- Only include enforcement you'll actually execute. If you name a consequence or follow-up process for late payment, make sure it's something you'll do consistently.

| Lever in your terms | What it protects | What "clear" looks like |

|---|---|---|

| Deposit + milestones | Cash timing, reduced exposure | Payment tied to named deliverables (and/or a recurring billing cadence) |

| Milestone definitions in SOW | Fewer disputes | What "done" means for each checkpoint |

| Scope + revisions | Profit goals, fewer disputes | Included rounds, change process, add-on pricing method |

| Payment methods (ACH + card) | Faster collections | How the client pays, with friction removed |

Practical check: after reading your invoice plus SOW, a third party must answer, without guessing: What triggers payment, when does it come due, and what happens if it runs late?

How do you run an invoice + collections workflow that reduces late payments (without awkwardness)?#

Run a simple, repeatable invoice-to-cash workflow with clear triggers, a pre-written follow-up ladder, and clean records so you never have to wing it in your inbox.

Terms only work if you execute them the same way every time.

Step 1: Set invoice timing rules that remove decision fatigue#

Late payments often start with sloppy starts. One source cites a survey where 71% of freelancers have experienced late payments and 54% say it takes too long to get paid, so treat speed and consistency as part of operations, not admin you do "when you get to it."

Build two trigger-based rules and run them on every client:

- Milestone rule: when you complete a billable milestone, as defined in the SOW, send the invoice promptly as part of your closeout process.

- Deposit rule: when the client signs, send the deposit invoice immediately as your first operational gate. If you use deposits to protect cash timing, define clearly how work starts and what happens if payment is delayed, in writing.

Operator move: write the trigger into your checklist so you never renegotiate with yourself.

Step 2: Use a calm escalation ladder (firm, not emotional)#

You do not need awkwardness. You need a script and a timeline tied to your terms.

| Stage | When you send it | What you say (keep it boring) | Outcome you want |

|---|---|---|---|

| Invoice + next steps | When the invoice goes out | Confirm due date, payment method, and what you will deliver next | No confusion about "what happens now" |

| Friendly reminder | A few business days later (or near due date) | Reshare the link and ask if AP needs anything | Remove friction, prompt action |

| Firm reminder + consequence | Shortly after due date | Point to the SOW and any agreed work-pause policy (if included) | Create urgency without threats |

| Enforce the gate | If your contract allows and your policy says "stop" | Pause work, resume after payment, escalate per contract and jurisdiction if needed | Protect profit goals and time |

Hypothetical: a client says, "We're processing it." You reply with the same template, reshare the link, and restate what your SOW says. Calm tone, hard boundary.

Reduce friction, not just reminders: double-check invoice accuracy, include a clear way to pay, and offer the payment methods you can support.

Automation helps here. One source defines invoice automation as tech that "handle[s] your invoices from arrival until payment," and another claims manual invoices cost $15 each to process and 39% contain errors. Fewer errors can mean fewer avoidable delays.

Recordkeeping discipline: keep clean, complete records so you can reliably see what's unpaid, what's due, and what's been followed up. One source warns: "Disorganized invoicing...can lead to missed payments and strained client relationships."

Practical check: you should be able to answer "Which invoices are at risk this week?" from one list, invoice status, due date, last touch, not from scattered email threads.

When things go wrong: the exception playbook for holds, disputes, FX surprises, and non-payment#

Treat exceptions as a built-in part of your freelance finance system: define triggers, freeze scope, and fall back to paperwork, not panic.

If you plan for exceptions, they stay annoying instead of becoming existential.

Before you start (so exceptions stay small)#

Set two policies in advance and you will move faster when something breaks:

- Time-to-cash buffer: for cross-border work, build extra lead time into your cash timing goal. Do not schedule tax transfers, subcontractor payouts, or large purchases based on "invoice sent." Schedule them based on "cash received."

- Identity consistency: keep your business name, invoice name, and bank receiving details consistent across the SOW, invoice, and payment instructions. Mismatched details can create delays you cannot fix with another email.

Step-by-step: run the exception workflow#

Step 1: Triage the exception and pick the right lane. Tag the issue and choose one next action. Do not mix lanes.

| Exception | What it usually looks like | Your safe next action |

|---|---|---|

| Payout delay or "on hold" status | Funds show as sent, but you do not see cash | Ask for the payment reference, confirm payee name and invoice details match, then wait before you reissue invoices |

| Dispute about scope or acceptance | "This isn't what we wanted" or "we need more rounds" | Freeze new work, pull the signed SOW, and start a written change log from that day forward |

| FX or cross-border shortfall | "Why is it less than the invoice?" | Ask which rail they used and what currency they sent. Keep proof of conversion or settlement in your reconciliation notes |

| Non-payment | Due date passes with vague replies | Enforce your pause-work gate and move to formal escalation per your contract |

Step 2: Contain disputes with documentation, not debate. A clean paper trail helps: signed SOW, acceptance evidence (email approval, delivered files, recorded walkthrough), and a simple change log. If escalation becomes necessary, your contract terms, including things like governing law or arbitration language when present, can shape the path, so read them while you still feel calm.

Step 3: Design an "FX exposure" rule for every cross-border quote. Define three items in writing: quote validity window, who pays conversion and wire costs, and what happens if the client pays using an unexpected currency or payment path.

One source specifically warns that paying a USD invoice from a CAD bank account can create "FX fees, bank markups and wire charges," so do not let clients improvise rails. Example: Canada uses EFT and the U.S. uses ACH.

Step 4: Recover fast from the three operator mistakes.

- Started work without a deposit: pause work, convert remaining scope into paid milestones, require the deposit to resume.

- Vague scope: send a written scope clarification plus a change order, then attach it to the SOW.

- Mixed personal and business funds: separate accounts immediately, rebuild your records for tax time, and document every transfer with a memo you can defend later.

Hypothetical: a client claims the final deliverable "needs just a few tweaks" that actually expands scope. You reply with a change order, price it, and pause the extra work until they approve and pay. That protects profit goals without turning the relationship into a fight.

Conclusion: Your freelance financial goals aren't numbers - they're policies you enforce#

Protect yourself with repeatable decisions, especially around client risk. When things get messy, what saves you is having a default way to respond.

Step 1: Write down the decisions you want to make the same way every time#

Turn fuzzy intentions into plain-language "if this, then that" rules you can actually follow under pressure.

A clearly hypothetical example: you feel excited about a new client, but they keep "forgetting" to confirm how payment will work. Your rule kicks in, and you do not move forward until you get a clear commitment.

Step 2: Treat client risk like a real part of the job#

Not every client is right for you, and it is worth protecting yourself early. Timing's freelance red flags guide puts it plainly: "it's smart to identify your problem clients and abandon them quickly." You can often spot trouble earlier than you think by looking for red flags that tell you the arrangement will not be pleasant to work through.

Step 3: Keep growing (without breaking the machine)#

The IRS notes that if you're self-employed, "you have many of the same options to save for retirement on a tax-deferred basis." Confirm what fits your situation with a qualified professional.

If you want a quick starting point, the IRS highlights options like a SEP (including contributions up to 25% of net earnings from self-employment, up to $69,000 for 2024) and a self-employed 401(k) plan (including annual salary deferrals up to $23,000 in 2024, plus an additional $7,500 in 2023 and 2024 if you're 50 or older, with $69,000 for 2024 referenced for total contributions).

If you want one next read, use: Hiring Your First Subcontractor. Other deep dives: Form 6166 and IRS residency certification paperwork and How to Set Up a US LLC from Australia.

Copy/paste checklist (run this on every new client):

- I looked for red flags and decided whether this client is a fit

- If I see clear red flags, I am willing to walk away quickly

- I reviewed my retirement options for self-employment (SEP, 401(k)) and noted my next step

Frequently Asked Questions

How do I set financial goals as a freelancer without overcomplicating it?

Keep it simple: start with your must-pay monthly costs, your cash on hand, and what clients currently owe you. Then decide ahead of time what you will pause or reduce when cash is tight, so you are not making decisions in a panic. Keep it informational: this guidance is for informational and educational purposes only, not legal or financial advice, and it does not establish any kind of client relationship.

What financial goals should a freelancer prioritize first?

Start with goals that help you stay financially afloat when income is uneven: visibility into cash coming in, cash going out, and what is still outstanding. From there, add goals that make the business sturdier over time, like planning for taxes and building a bit of breathing room for gaps between payments, where possible.

How much should freelancers set aside for taxes?

There is no “universal” percentage that is safe to apply to everyone. A more reliable approach is to build a consistent tax-reserve habit and confirm what makes sense with a qualified tax professional, since rules vary by jurisdiction and your income mix.

How do freelancers manage irregular income during low months?

Some freelancers deal with sporadic paychecks, get paid in lump sums, and can have long stretches between paychecks, so it helps to plan for that reality. Practical approach: make commitments based on cash you have (not just invoices you sent), and set a clear personal rule for when you cut back optional spending.

Should freelancers separate business and personal accounts even if they’re just starting?

Yes, because it makes your money clearer fast: what you earned, what it cost to earn it, and what you actually keep. It can also reduce the end-of-year scramble because you are not reconstructing everything from one mixed statement.

How can freelancers reduce late payments and payment risk?

Treat payment clarity as part of the job: use clear written agreements, clear payment terms, and consistent invoicing. If payment slips, follow a consistent process so you are not renegotiating your boundaries every time.

What should I track weekly vs monthly to stay on top of cashflow?

Track cashflow regularly in a cadence you can sustain. At minimum, keep an up-to-date view of money in, money out, what is owed to you, and what is due soon, and simplify until you can understand your cash timing quickly.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

How to Get a Certificate of Residence (Form 6166) from the IRS

Start with purpose, not paperwork. Before anyone opens Form 8802, get clear on why the foreign payer or tax authority wants a U.S. residency certificate. That answer drives almost everything that follows: whether you should file at all, how the request should be framed, what tax period matters, and how much lead time you really need. If the reason stays vague, the rest of the process gets expensive fast.

How to Set Up a US LLC from Australia

**Treat a US LLC from Australia as a system, not a one-time filing.** Forming the LLC is only the first milestone. What matters after that is how you handle the ongoing obligations in Australia and the United States.