Quick Answer

Route your complaint by harm: for unpaid minimum wage or overtime, start with the U.S. Department of Labor Wage and Hour Division; for federal worker-status tax treatment, use Form SS-8. Then build one evidence packet with contracts, pay records, hour logs, and direction-related communications, and split labor facts from tax facts before filing. Keep the same dates, role description, and document labels across every submission so follow-up requests do not create contradictions.

Start here if you need to report misclassification now#

Start with one sequence: pick the right agency lane, prepare one consistent evidence pack, and reuse the same facts in each submission. That order can cut avoidable delays and help you avoid conflicting statements across filings. This article is U.S.-focused and centered on the U.S. Department of Labor Wage and Hour Division, the Internal Revenue Service, and state agencies.

Under the Fair Labor Standards Act, misclassification means an employer treats a worker who is an employee as an independent contractor. That can affect minimum wage and overtime protections. Employers are responsible for classification under the FLSA, and current federal guidance is in 29 CFR Part 795 (effective March 11, 2024).

Use this article as a sequence, not a menu. If you skip ahead and file before your facts are organized, you may create rework later. If you move in order, you can reuse the same timeline, core statements, and document labels across every lane.

Before you file#

-

Route by harm first. If your immediate issue is unpaid minimum wage or overtime, start with the Wage and Hour Division. Add an IRS lane when the issue includes federal tax handling, and add a state lane based on your state process (for example, California directs group misclassification reports to the Bureau of Field Enforcement). This keeps each filing tied to one clear question instead of mixing issues in one submission.

-

Build one record, then organize it by question. Keep one core packet and separate labor-related facts from tax-related facts so each filing stays clear. A single master record also makes it easier to answer follow-up requests without changing your core narrative.

-

Use official intake channels and keep a contact log. Save submission dates, confirmation details, contact names, and follow-up requests in one place. When offices ask for clarification later, your log can help you answer quickly with consistent wording.

-

Set expectations early. Misclassification often overlaps with labor and tax issues, but outcomes still depend on agency review of your facts. Use this as filing guidance, not legal advice for your full dispute.

Confirm you have a misclassification issue before you file#

Start here: if your day-to-day relationship looks like employment under the Fair Labor Standards Act but you are treated as an independent contractor, you likely have a misclassification issue. Getting that call right up front makes every later filing cleaner.

-

Anchor your check to current FLSA guidance. Use WHD classification materials, including Fact Sheet 13 (Employee or Independent Contractor Classification Under the Fair Labor Standards Act), and

29 CFR Part 795. The rule was finalized on January 10, 2024, and took effect March 11, 2024. Focus on how the relationship actually works, not just what the paperwork says. -

Treat common signals as clues, not conclusions. A Form 1099, a contractor agreement, cash pay, or offsite work does not, by itself, prove correct classification. Those facts can appear in compliant and noncompliant relationships. Keep these items in your evidence file, but do not let them replace relationship-level analysis.

-

Separate wage harm from tax handling before you file. Under the FLSA, minimum wage and overtime protections depend on an employment relationship and coverage. IRS treatment also depends on the relationship. If your main harm is unpaid minimum wage or overtime, document those FLSA wage issues first and assess tax-handling issues separately.

-

Check state tests that can increase risk. Federal analysis is the baseline, but some states apply stricter tests. In California, the ABC test starts with a presumption that workers are employees, and the hiring entity must satisfy all three conditions to classify a worker otherwise. If you worked in more than one state, keep notes by state so you do not blend standards.

Use this go-or-no-go rule: if your facts show employee-type work plus denied wage protections, you likely have a misclassification issue. Build one record and use it to evaluate labor and tax paths based on the same facts. For a deeper self-screen, use Are You an Employee or a Contractor? A Self-Assessment Checklist.

If you want a deeper dive, read What to Do If You've Been Misclassified as an Independent Contractor.

Build your evidence pack before contacting any agency#

Build one complaint-ready packet before you contact any agency. A clean evidence record helps you explain the relationship once and reuse the same core facts without rewriting the story each time.

| Packet item | What to include | Use |

|---|---|---|

| Issue statement | You were treated as an independent contractor, but the relationship may be employment under the FLSA | Set the legal frame first |

| Intake details | Your contact details, employer identity and location, and how and when you were paid | Keep the first intake conversation focused |

| Contracts and statements of work | Copies of contracts and statements of work | Add proof, not labels |

| Pay and hour records | Pay stubs, pay records, and personal hour logs | Pair each claim sentence with at least one document you can point to quickly |

| Work-direction records | Communications or written instructions that show direction over schedule, assignments, or work method | Show direction over schedule, assignments, or work method |

| Timeline | Engagement start, role changes, pay method changes, and complaint-related events | Separate wage and overtime facts from other records |

| Index | File name, date, and why each item matters | Makes repeat requests easier |

-

Set the legal frame first. Open with a short issue statement: you were treated as an independent contractor, but the relationship may be employment under the FLSA. Tie your fact review to Employee or Independent Contractor Classification Under the Fair Labor Standards Act and

29 CFR Part 795. -

Capture intake details up front. Include your contact details, employer identity and location, and how and when you were paid. Use concrete wording so your first intake conversation stays focused. Keep phrasing simple enough to paste into phone intake notes, portal text boxes, and follow-up emails.

-

Add proof, not labels. Group contracts and statements of work first, then include copies of pay stubs, pay records, and personal hour logs. Add communications or written instructions that show direction over schedule, assignments, or work method. When possible, pair each claim sentence with at least one document you can point to quickly.

-

Build a timeline and split it by issue. List engagement start, role changes, pay method changes, and complaint-related events. Then separate wage and overtime facts from other records so intake discussions stay focused.

-

Clean and index for reuse. Add a simple index with file name, date, and why each item matters. This is an organization step, not a legal filing requirement, but it makes repeat requests easier. Consistent file names and date formats also reduce mistakes when you update the packet later.

Close with a short cover note summarizing the work performed, how pay was handled, and which protections were denied. Lead with wage and overtime facts if wage harm is central, keep a post-filing contact log, and remember that WHD states complaint services are confidential and employers cannot lawfully retaliate for filing.

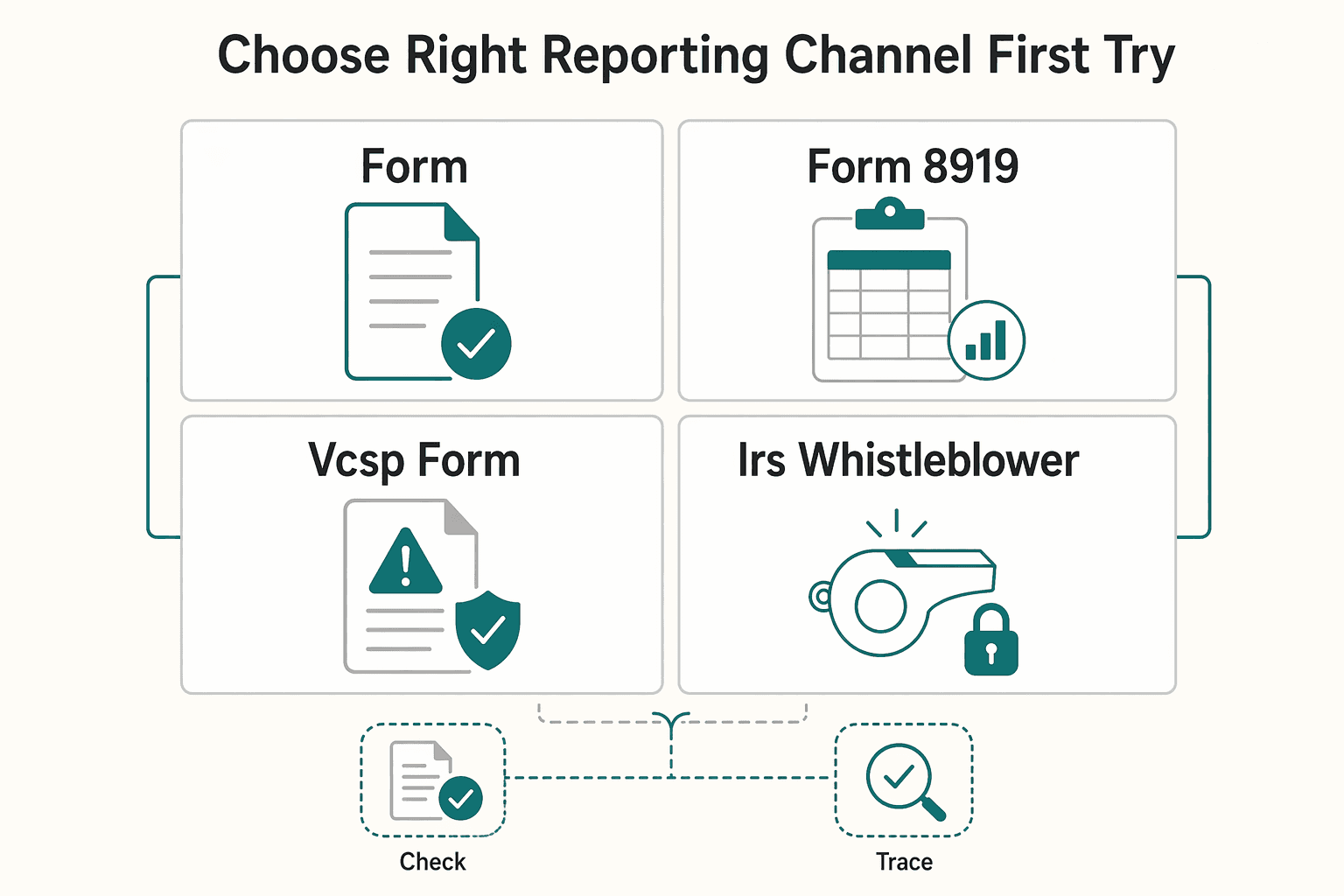

Choose the right reporting channel on the first try#

Choose the channel by the exact question you need answered. Keep worker-status determinations separate from tax noncompliance reporting so each submission has one clear purpose.

| Channel | Primary use | Key note |

|---|---|---|

| Form SS-8 | Worker-status determination for federal employment taxes and income tax withholding | Workers who believe they were improperly classified generally need an IRS worker-status determination |

| Form 8919 | Report a worker's share of uncollected Social Security and Medicare taxes | Use after status is determined |

| VCSP / Form 8952 | Prospective reclassification by taxpayers | Employer-side compliance route, not a worker remedy channel |

| IRS Whistleblower Office | Award claim with specific, timely, and credible information about tax-law noncompliance | Keep separate from SS-8 so each filing has one objective |

-

Start by naming the tax question. Keep two lanes: worker-status determination and tax noncompliance reporting. Reuse the same core facts, dates, and role description in every submission. If you cannot state the question in one sentence, tighten it before filing.

-

Use Form SS-8 for worker-status determination. If your question is whether you should have been treated as an employee for federal employment taxes and income tax withholding, route it to Form SS-8. IRS guidance says workers who believe they were improperly classified generally need an IRS worker-status determination.

-

Use Form 8919 after status is determined. Once status is determined, workers can use Form 8919 to report their share of uncollected Social Security and Medicare taxes. Treat this as a separate step from SS-8.

-

Do not use VCSP/Form 8952 as a worker complaint path. The Voluntary Classification Settlement Program (VCSP) is for taxpayers who want to prospectively reclassify workers. It uses Form 8952 and a closing agreement with the IRS, so it is an employer-side compliance route, not a worker remedy channel.

-

Treat whistleblower reporting as its own path. The IRS Whistleblower Office handles award claims tied to specific, timely, and credible information about tax-law noncompliance. Keep this separate from SS-8 so each filing has one objective.

Decision rule: pick the channel that answers your immediate question first. If the question is worker status, start with SS-8. If your facts are still mixed before you choose a filing path, run a quick status sanity check first with the W-2 vs 1099 calculator.

File with the U.S. Department of Labor without losing leverage#

For a Wage and Hour Division complaint, stay focused: lead with work-control facts, tie them to denied protections, and preserve retaliation records from day one.

Step 1 Document process details when you contact WHD#

When you contact WHD, use the conversation to confirm process details and keep your records straight, not to deliver your full argument. Log the office details, date, and any intake information you receive.

If privacy is a concern, ask process questions during intake and write down the answers. Do not assume every complaint is fully confidential or anonymous in every situation. Save the exact phrasing from intake answers so later discussions stay aligned with what you were told.

Step 2 Write a tight narrative on control, pay, and denied rights#

Write a short timeline showing who directed your work, how pay was set, and what happened when pay or hour issues surfaced. Then connect those facts to denied employee protections, such as minimum wage or overtime where applicable.

Do not rely on labels alone. A 1099 or an independent contractor agreement, by itself, does not settle worker status. A clear narrative usually reads this way: relationship facts first, pay facts second, denied protections third.

Step 3 Submit evidence that maps to each claim#

Send a focused packet that matches your timeline: records on pay practices, time and hours, and work direction. Tie each file to a specific fact so a reviewer can follow it quickly.

Avoid both extremes: too little evidence can make review harder, while an unstructured document dump can bury your core wage issues. A useful checkpoint is whether a reviewer could reconstruct your timeline from the first page and index alone.

Step 4 Preserve retaliation evidence from the day you report#

Start a dated retaliation log as soon as you file and keep it current through each employer response. Track concrete changes in assignments, pay handling, access, communications, or threats linked to your complaint, and keep originals where possible.

If treatment shifts after filing, this log helps you report specific events instead of broad impressions. Update it the same day when possible so details stay accurate if they are challenged later. For current rule context, see The Department of Labor's New Independent Contractor Rule (2024).

Use IRS paths correctly and avoid channel confusion#

Use the IRS lane by objective, not by form name. Define the tax outcome you need, verify the exact path, and keep separate tracks for anything that is not yet confirmed.

Step 1 Define the IRS objective before choosing any form#

Write one sentence stating your IRS objective and whether you are pursuing a whistleblower award claim. Keep your records organized by objective so the narrative stays consistent.

If you are choosing between Form SS-8 and Form 3949-A, treat their exact roles and privacy implications as unconfirmed until you verify current IRS instructions. That caution helps you avoid a misrouted filing and later rework.

Step 2 Use the IRS Whistleblower Office only for award-claim conditions#

Use this path when you have specific, timely, and credible information about tax-law noncompliance and you are submitting an award claim. This is an award-focused channel, not a general intake lane.

Awards can be paid to eligible individuals if the IRS uses their information, and the published range is generally 15 to 30% of collected proceeds. The gate here is claim quality.

Pre-submit check:

- Identify the noncompliance facts clearly.

- Show why the information is specific, timely, and credible.

- State how the IRS can verify the issue from your records.

Step 3 Keep unconfirmed IRS frameworks in context, not as your worker filing#

Do not treat VCSP, CSP, Announcement 2011-64, or Announcement 2012-45 as confirmed worker remedy channels.

Failure mode to avoid: filing material that is not tied to your chosen objective and delaying the channel you actually need. If a document is not tied to your objective, keep it in a separate reference folder and out of the filing packet.

Step 4 Log unknowns before submission#

Add a short preflight note with three lines: confirmed facts, unresolved assumptions, and where you will verify each assumption. Include unknowns such as form purpose, privacy expectations, and response mechanics when they are not confirmed in your evidence pack.

A brief verification pass now is usually faster than fixing a misrouted filing later. It also keeps your future updates cleaner because you can trace why each filing decision was made.

Use state agencies when wages are not the only harm#

Use state paths by harm type instead of assuming one combined complaint covers everything. Keep the same dates and core facts across filings so your record stays consistent.

Step 1 Map each harm to the right state path#

Build a simple routing map before you file. In California, guidance separates wage claims, workers' compensation claims, and benefit applications, with EDD deciding eligibility. It also says a worker can file one or more paths. Missouri also provides a direct suspected-misclassification reporting channel, including an online form and phone intake at 573-751-1099. Treat these as state-specific examples, not a national template.

A practical format is one row per harm with four columns: agency lane, filing channel, confirmation field, and next follow-up date. That keeps action steps visible without repeating the same notes across multiple documents.

Step 2 Match your filing to the state's classification framework#

Do not assume every state uses the same test. California applies the ABC test and requires all three listed conditions for independent-contractor treatment, while Missouri says it uses the IRS 20-factor test as a guide. Keep one core fact record, then tailor each submission to the state test that applies.

Filings can drift when the facts stay constant but wording changes too much between agencies. Keep your factual baseline identical and only adjust test-specific framing.

Step 3 Coordinate multiple filings without changing facts#

If facts overlap across filings, use one consistent record and avoid changing core details between submissions. The priority is consistency: use the same timeline, role description, and pay facts in every submission.

If one agency asks for an expanded explanation, update your master notes first, then reuse that language across all active lanes. That helps prevent contradictions caused by ad hoc edits.

Step 4 Treat cross-border jurisdiction as a verification step#

If you worked across jurisdictions, confirm intake jurisdiction with the relevant agency before you file rather than guessing which state has the strongest employment connection. Then keep one log for each case with:

- Confirmation number or receipt ID

- Intake email or portal acknowledgment

- Case contact details and date of contact

Review those logs weekly while cases are active. Missing a follow-up date can slow progress in multistate matters.

Check your contract before filing and after filing#

Review the contract to spot pressure points, but do not assume contract language must be resolved before agency filing. Worker status is assessed on the overall worker-business relationship under FLSA analysis and 29 CFR Part 795, not just contract labels.

| Clause | What to pull | What to note |

|---|---|---|

| Termination | Exact language; mark notice periods | Aggressive termination language that appears after you raise a classification concern |

| Limitation of Liability | Exact language | Keep short notes on potential filing friction |

| Indemnification | Exact language | Broad indemnification demands that appear to shift most company claims to you |

| Governing Law | Exact language | Keep short notes on potential filing friction |

| Jurisdiction | Exact language; mark venue terms | Keep short notes on potential filing friction |

| Dispute Resolution | Exact language; mark arbitration triggers and fee-shifting clauses | Forum or dispute terms framed in ways that may discourage agency intake |

- Build a one-page clause sheet. Pull exact language for Termination, Limitation of Liability, Indemnification, Governing Law, Jurisdiction, and Dispute Resolution. Mark notice periods, venue terms, arbitration triggers, and fee-shifting clauses. Keep a short note beside each clause describing potential filing friction.

- Keep filing timing on track. If arbitration or venue terms look hostile, treat that as a parallel private-dispute issue and do not delay agency intake while you sort out contract concerns.

- Use contract text as one evidence input. Pair each clause with what happened in practice, since written terms are only one part of status analysis. This side-by-side check keeps your position grounded in conduct, not labels.

- Document pressure after filing. Save clause-heavy warnings, log dates, and keep the same core facts across submissions. If pressure language changes over time, keep those versions in chronological order.

Flag these early:

- Broad indemnification demands that appear to shift most company claims to you.

- Aggressive termination language that appears after you raise a classification concern.

- Forum or dispute terms framed in ways that may discourage agency intake.

- Contract terms can be relevant evidence, but they do not by themselves decide worker status.

Protect your income and records while the case moves#

Protect cash flow and records in parallel while the case is active. Long gaps in either track can create avoidable pressure.

Create two live documents and update them daily: a receivables tracker and an evidence log. These answer two practical questions under stress: what money is still collectible, and what changed after you filed.

- Step 1: Map immediate income risk. List every open invoice with amount, due date, contact owner, and last follow-up date. Split entries into

due now,due in 7 days, andoverdue. Add a short backup client list you can activate if one account freezes work. - Step 2: Keep filings and collections on separate tracks. If you decide to file a misclassification complaint, do not pause filing actions while chasing late payments. Handle payment follow-up and classification actions in parallel, including Form SS-8 when relevant.

- Step 3: Preserve a complete post-filing trail. Log assignment changes, access revocations, payment-method shifts, and communication changes with date, time, sender, and attachment. Save originals such as email headers, portal notices, and invoice exports.

- Step 4: Document potential retaliation signals promptly. If work access, assignments, hours, or communications change after filing, record each event in sequence and update your case record promptly. Keep wording factual and consistent with earlier submissions.

An avoidable failure mode is having to rebuild events from memory later. Note key filing milestones in the same log so your timeline stays complete. Another useful checkpoint is a weekly review: make sure your receivables tracker and case log tell the same story about dates and account activity.

Know what happens next and where uncertainty remains#

After you file, expect some uncertainty. There is no single timeline or guaranteed outcome across U.S. Department of Labor, IRS, and state processes.

Keep one master case log, one evidence index, and one fact baseline, then reuse the same core facts in every update. Include role description, pay method, control-related facts, and key dates, and keep wording consistent across submissions.

- Set expectations with ranges, not promises. Track agency name, submission date, confirmation ID, latest contact, requested documents, and next follow-up date. Use neutral statuses like

submitted,acknowledged,request received, andunder reviewonly when you have direct proof. - Treat process steps as possible, not universal. Post-filing intake and review can vary by agency and office. When asked for clarification, respond with the same fact baseline you already used elsewhere.

- Plan escalation with caution. If instructions conflict or the dispute materially expands, consider legal advice, and supplement the record only with dated, material evidence.

- Keep policy variation in view. State classification standards are not uniform, and many states use an ABC test. California adopted the ABC test in 2019, and app-based rideshare and delivery drivers were later exempted from AB5, which is a practical reminder that coverage rules can change.

Do not infer outcomes from silence. Keep your facts fixed, log every contact, and follow your check-in schedule across any filings you have made. If new information appears, update the master baseline first, then propagate that update to active filings.

Copy-paste checklist and your next move#

Use one disciplined sequence from here: confirm FLSA status, organize support, file with a consistent fact record, and track updates until closure.

- Confirm issue type under the FLSA and 29 CFR Part 795.

State the core issue in one line: a worker who should be treated as an employee under the FLSA is being treated as an independent contractor. Check the full relationship under the economic realities approach, not one isolated detail, and avoid relying only on common-law control language. Note that 29 CFR Part 795 is the current regulation, effective March 11, 2024.

- Build and index your evidence pack before filing.

Create a simple index for each item: document ID, date range, source, and what it supports. Keep names and dates consistent across drafts and submissions. If you cite rule text, use the official govinfo PDF linked from the Federal Register entry for 89 FR 1638.

- Keep facts consistent across any submissions.

When you file, start with a narrow factual summary tied to your confirmed issue. If you submit in more than one place, reuse the same timeline, dates, and core statements so your record does not conflict.

- Keep contract-risk review separate from status analysis.

If you review terms like termination, indemnification, governing law, or dispute resolution, treat that as a separate risk note. Do not use those terms as the basis for your FLSA status analysis.

- Maintain one case log until resolution.

Track submission dates, confirmation IDs, contacts, requests, and next follow-up date in one place. Add updates the same day events happen. Include a policy-watch note: the 2024 rule is being litigated, remains in effect for private litigation, and the Department announced an NPRM on February 26, 2026, with comments due April 28, 2026 at 11:59 ET.

Completion signal: you are done with this checklist when each active submission has a confirmation record, a scheduled follow-up date, and a matching fact baseline.

For future engagements, consider documenting scope, control, and payment terms in writing: Create a freelance contract draft.

Frequently Asked Questions

How do I report worker misclassification quickly if I need action this week?

This grounding set does not confirm a one-week agency timeline. If your main issue is unpaid minimum wage or overtime, the U.S. Department of Labor Wage and Hour Division is the channel tied to those FLSA protections. If worker tax status is also disputed, IRS guidance says workers generally must receive an IRS worker-status determination (Form SS-8), then can use Form 8919 to report their share of uncollected Social Security and Medicare tax. Keep the same facts and dates across filings.

Is a Wage and Hour Division complaint confidential?

This grounding set does not confirm a confidentiality rule or guarantee for WHD complaints. Treat confidentiality as a direct intake question before sharing extra personal details. Send only the evidence needed to support your claim.

Can my employer retaliate after I file with the U.S. Department of Labor?

The material here does not confirm specific retaliation remedies or filing steps after a DOL report. If your hours, assignments, access, or pay change after filing, document each event with dates and keep your case record updated. Keep every submission factual and consistent.

If I received a Form 1099 and signed a contractor agreement, am I still possibly an employee?

Yes, that is still possible. IRS says classification depends on the working relationship across three categories, including whether the company controls what you do and how you do it, not just labels. Indiana UI guidance also states that forms like a 1099 or W-9 are not conclusive by themselves.

Is the Voluntary Classification Settlement Program a worker complaint option?

Do not assume VCSP replaces other reporting options when you have active wage or classification harm. Verify current VCSP rules separately before relying on it.

What is the difference between Form SS-8 and Form 3949-A?

From the confirmed material, Form SS-8 is the IRS worker-status determination process for workers who believe they were improperly classified. After that determination step, workers can use Form 8919 to report their share of uncollected Social Security and Medicare tax. This section does not include verified details about Form 3949-A.

How long does a misclassification complaint usually take?

There is no single reliable timeline in the provided material for DOL, IRS, or state outcomes. Process steps and response windows can vary by agency and jurisdiction. Use a follow-up calendar with confirmation IDs, contact dates, and document requests so delays do not weaken your record.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- dol.gov/sites/dolgov/files/ETA/publications/ETAOP201...trusted

- dol.gov/agencies/whd/contact/complaints/informationtrusted

- federalregister.gov/documents/2024/01/10/2024-00067/employee-or-...trusted

- irs.gov/newsroom/worker-classification-101-employee-...trusted

- irs.gov/businesses/small-businesses-self-employed/in...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

Are You an Employee or a Contractor? A Self-Assessment Checklist

Forget the label. Classification turns on the relationship you actually run, not the title you typed into the contract. It is also much easier to fix before you sign.

The Department of Labor's New Independent Contractor Rule (2026)

The right way to operate right now is simple: treat the DOL action as a live proposal, not settled law. The Wage and Hour Division published a Notice of Proposed Rulemaking on 02/27/2026 for worker status under the Fair Labor Standards Act, listed as RIN 1235-AA46. The proposal says WHD would rescind the analysis now codified at 29 CFR part 795 and return to the Department's 2021 approach, with modifications. It also proposes using the same analysis when FMLA or MSPA coverage is in play.