Quick Answer

Start by tagging each crypto row, then build Form 8949 before touching Schedule D or Form 1040. Match statement proceeds from Form 1099-B or Form 1099-DA, document basis support, and block any line you cannot trace to source records. Keep offshore checks separate: FBAR (FinCEN Form 114) and Form 8938 are independent decisions, not leftovers after return prep.

Report Crypto on Taxes Without Guesswork#

To report crypto on taxes without creating contradictions in your return, follow the same order every time: confirm your filing context, define what is reportable, then decide whether any unknowns still let you proceed or require escalation. A few terms need to stay precise:

- Digital asset: a cryptographically secured digital representation of value (not cash).

- Disposition: selling, exchanging, or otherwise disposing of a digital asset (or a financial interest in one).

- Reportable event: receiving digital assets as a reward, award, or payment, or disposing of them.

- Unresolved item: our workflow label for a fact you cannot yet support with records (not an IRS defined term).

Decision framework (safe default)#

| Status | What it means | Action |

|---|---|---|

| Known facts | You can substantiate units, dates, values, ownership, and filing context. | Proceed. |

| Unknown facts | Basis, unit identity, ownership, or cross-border facts are still open. | Pause and escalate before filing. |

Startup controls and evidence#

This only works once the facts are pinned down.

| Startup control | What to confirm | Evidence to have ready |

|---|---|---|

| Return context | You have the correct return path and a supportable digital-asset yes/no answer. | Return draft notes and transaction summary tied to your answer. |

| Activity inventory | All reportable digital-asset activity is captured before any gain/loss math. | Exchange exports, wallet histories, payment/reward records, transfer logs. |

| Treatment memo | Each unresolved item has a temporary treatment and owner. | Short assumptions memo with gap, treatment, reason, and review date. |

| Escalation owner | One reviewer is accountable for open issues. | Named owner plus escalation trigger and decision deadline. |

Digital assets are treated as property, so capital gain and loss reporting runs through Form 8949 to Schedule D. If you are unsure how reward-type activity should be treated as income in edge cases, review that separately before you finalize calculations. See Paying Taxes on Crypto Staking and Yield Farming Rewards.

For basis method, do not improvise. If you can specifically identify units and substantiate them, use that support. If you cannot, IRS guidance describes FIFO deemed order. If unit-level substantiation is missing, record that gap before you finalize gain and loss totals.

Run cross-border checks on a separate track from income-tax form flow. Form 8938 and FBAR (FinCEN Form 114) are not the same process, and FBAR is not filed with the IRS. When FBAR applies, the IRS states a $10,000 aggregate foreign-account trigger, a due date of April 15, and an automatic extension to October 15.

Before you rely on any summary, verify the current guidance scope and effective date against official IRS/source records or advisor records. Apply that check especially to Form 1099-DA and broker-reporting changes for transactions on or after January 1, 2025. Final regulations are noted as effective February 28, 2025, with basis reporting updates for covered securities noted for 2026 and beyond.

Gather Your Filing Inputs Before You Open Any Tax Form#

Start the filing work with complete records, not open forms. Do not open Form 8949, Schedule D, or your tax software until your records are complete, reconciled, and decision-ready. The IRS flow is records first, then gain and loss calculation, then basis, then form mapping. If return type, ownership, basis support, or proceeds mapping is unclear, pause and route it to review instead of estimating.

Confirm filing context before intake#

Start with the return you are actually filing. You must answer the digital-asset Yes/No question, and it appears across multiple return types, including Forms 1040, 1040-SR, and 1040-NR.

You are intake-ready only if you can state the return type, who owns the activity, and how that ownership is reported. If activity is mixed across owners or reporting contexts, stop and resolve that first.

Assemble the four core inputs#

Use these terms consistently so intake stays clear and the file stays reviewable:

- Transaction log: your working file for each digital-asset receipt, sale, exchange, disposition, or transfer, including fair market value support.

- Information return: an IRS reporting form or statement, for example Form 1099-B or Form 1099-DA, reporting transactions to the IRS and to you.

- Carryover: a prior-year capital loss amount carried into the current-year Schedule D process.

- Missing-data queue: your internal label, not an IRS term, for unresolved items that block form entry.

Use this readiness check before any Form 8949 work:

| Input source | Why it matters | Common mismatch | Ready/Blocked decision |

|---|---|---|---|

| Transaction log | Base record for gain/loss, basis support, and event classification. | Missing acquisition dates, units, or fair market value support. | Ready only if all material activity is captured and duplicates are cleared. Blocked if dates, units, or values are missing. |

| Form 1099-B or Form 1099-DA | Form 8949 is where you reconcile amounts reported to you and the IRS. | Statement proceeds do not tie to your log; statement covers only part of activity. | Ready only if each line maps to the log or has an explained difference. Blocked if proceeds cannot be matched. |

| Prior-year Schedule D records | Carryovers affect current-year capital loss treatment. | Current-year file started without prior-year loss continuity. | Ready only if carryover amounts match filed records. Blocked if continuity is unknown. |

| Missing-data queue | Prevents silent guesses from entering Form 8949. | Basis gaps noted but not assigned for resolution. | Ready only if each open item has an owner and deadline. Blocked if material gaps remain unresolved. |

Reconcile proceeds and basis before form entry#

Keep proceeds and basis as two separate checks. Form 8949 is the reconciliation step for amounts reported on Form 1099-B, Form 1099-DA, or similar statements. Proceeds should follow the amount shown on the form or statement in column (d). Do not replace statement proceeds with estimates.

Then run a separate basis check. For 2025 broker sales, brokers are not required to report basis, so your basis support remains essential.

Verify guidance window and scope boundaries#

Before filing work continues, verify the current guidance window and filing-year applicability against official IRS/source records or advisor records. Older virtual-currency FAQs generally apply to transactions completed before Jan. 1, 2025. IRS materials point filers to 2024 regulations for transactions on or after January 1, 2025.

| Reference | Date or scope | Check |

|---|---|---|

| Older virtual-currency FAQs | Transactions completed before Jan. 1, 2025 | Generally apply to that period |

| 2024 regulations | Transactions on or after January 1, 2025 | IRS materials point filers here |

| Gross proceeds reporting | Starts on or after January 1, 2025 | Keep broker-reporting timing explicit |

| Certain basis reporting | Starts on or after January 1, 2026 | Keep broker-reporting timing explicit |

| Final regulations | Limited to brokers that take possession of customer digital assets | Keep scope explicit |

| IRS source freshness | Digital-asset question page last reviewed 13-Feb-2026; Form 8949 overview page updated 24-Jan-2026 | Verify the pages you rely on |

Keep broker-reporting timing and scope explicit. Gross proceeds reporting starts on or after January 1, 2025. Certain basis reporting starts on or after January 1, 2026. Broker reporting under the final regulations is limited to brokers that take possession of customer digital assets. As a freshness check, verify the IRS pages you rely on, including the digital-asset question page last reviewed 13-Feb-2026 and the Form 8949 overview page updated 24-Jan-2026.

Use one escalation trigger. If any material activity sits outside your verified guidance window, or you cannot map it to ownership, basis, and statement proceeds with support, stop intake and send it to review.

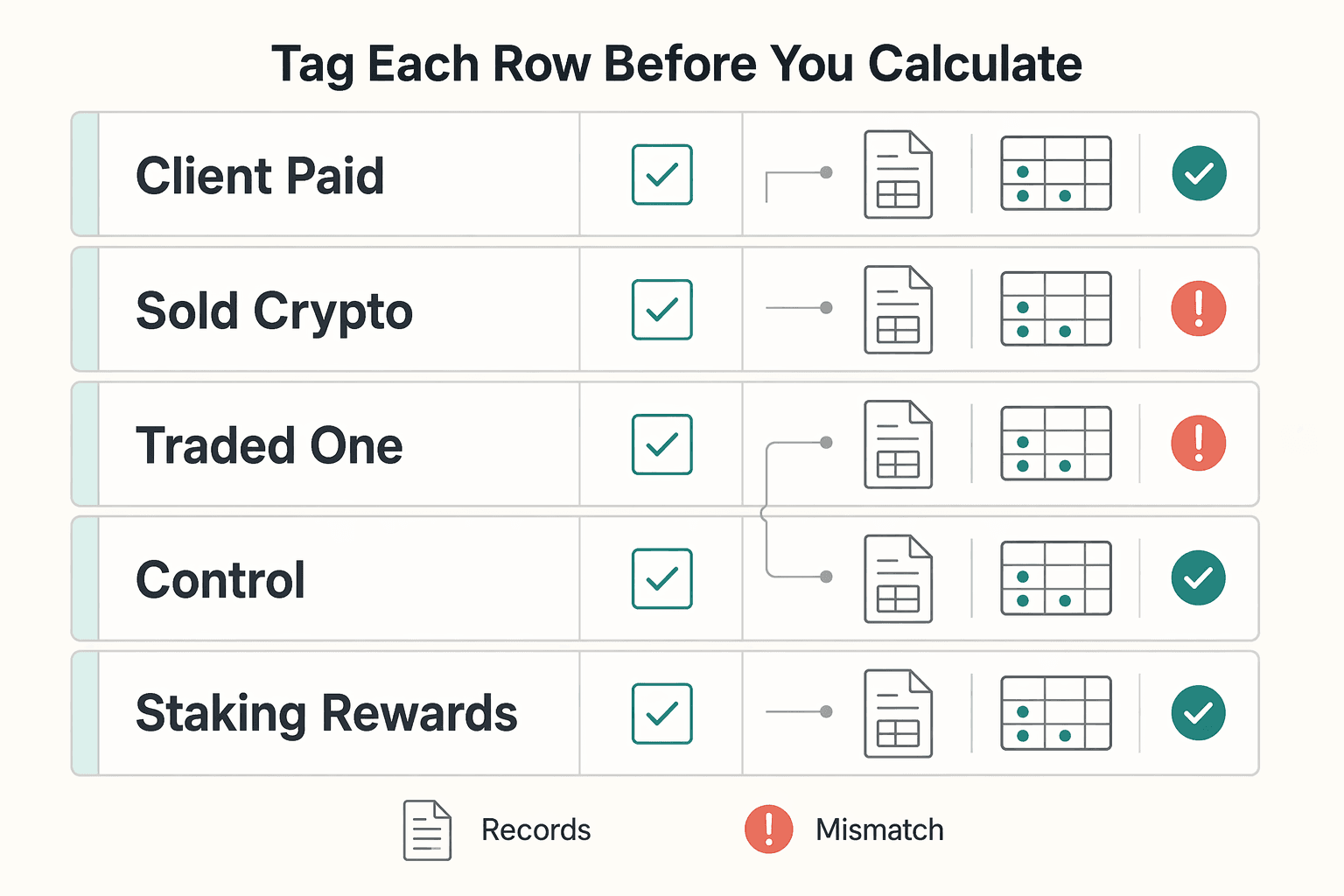

Classify Every Crypto Event Before You Calculate Anything#

Classification errors create downstream filing errors, so tag first and calculate second. Before any gain or loss math, tag each ledger row as a receipt, disposal, self-transfer, fee-related disposal, or needs review. That keeps your form flow and digital-asset Yes/No posture consistent.

Tag each row before you calculate#

Use one plain test for each row: did you receive digital assets, dispose of them, transfer between accounts you control, or pay a fee in digital assets? In many freelancer files, this covers client payments, sales, crypto-to-crypto trades, transfers, staking receipts, and fees.

| Event type | Likely tax character | Required evidence | Provisional status |

|---|---|---|---|

| Client paid you in crypto | Receipt; Yes-box event | Invoice, wallet receipt, timestamp, fair market value support | Ready when ownership and value are supported |

| Sold crypto for cash | Disposal; Yes-box event | Exchange record or Form 1099-DA, units, date, proceeds | Ready when proceeds reconcile to records |

| Traded one token for another | Disposal of the asset given up; Yes-box event | Trade record, both assets, quantities, timestamp | Ready when both legs are captured |

| Transfer between wallets/accounts you control | Self-transfer; can be a No-box scenario if control did not change | Ownership/control support, transfer IDs, fee detail | Review if control is unclear |

| Staking rewards received | Receipt; Yes-box event | Reward logs, credit date, fair market value support at receipt | Ready when receipt timing is documented |

| Fee paid in digital assets | Fee-related disposal; can require Yes | Transaction record showing fee asset and amount | Review if fee data is blended or incomplete |

Each row gets exactly one tag, and uncategorized rows stay blocked.

Keep edge cases in a hard review bucket#

This is where you need the most discipline. Use needs review for ambiguous rows, including wrapped-token or bridge flows, liquidity or yield activity, mixed personal and business wallets, or any movement where you cannot prove destination and control. Do not force uncertain rows into "transfer" just to keep momentum.

Reconcile tags to your return posture before forms#

Before you move into forms, compare the classified ledger to your return posture. The digital-asset question is a required Yes/No check for activity from Jan. 1 to Dec. 31. If your tags show receipt or disposal activity, for example client payments, staking receipts, sales, trades, or digital-asset fees, but your draft posture is "No," pause and resolve the conflict before gain/loss form work (including Form 8949 for capital-asset disposals).

If an event is timeline-sensitive or still ambiguous after classification, verify the current guidance scope against official IRS/source records or advisor records before final tagging, then route unresolved calls to professional review.

Map Transactions to the Exact Form Flow#

Once classification is settled, the handoff should be mechanical. Use a fixed sequence: finish Form 8949 at the transaction level, roll subtotals to Schedule D, then carry finalized results into the return.

| Step | What to do | Key rule |

|---|---|---|

| Form 8949 | Enter each reportable sale or exchange at the transaction level | Complete it before Schedule D lines 1b, 2, 3, 8b, 9, and 10 |

| Schedule D | Roll in Form 8949 subtotals | Move forward only when each subtotal ties out to the validated Form 8949 bucket |

| Form 1040 | Carry finalized results into the return | For 2025 instructions, if Schedule D line 16 is a gain, carry it to Form 1040 line 7a |

Build Form 8949 from your ledger#

Form 8949 is the line-level build, so complete it before you summarize anything on Schedule D. Enter each reportable sale or exchange on Form 8949. Complete Form 8949 before Schedule D lines 1b, 2, 3, 8b, 9, and 10. If basis is missing, calculate it before filing. If no Form 1099-DA was issued, including for foreign-broker activity, still report the transaction.

Use a reconciliation sheet alongside the form:

| Ledger record | Information return | Form entry | Variance note | Status |

|---|---|---|---|---|

| Transaction in ledger | 1099-DA received (or none) | 8949 row drafted | Match, mismatch, or missing field noted | Ready / Blocked |

For this workflow, traceability means each Form 8949 row can be traced back to a ledger entry, timestamp, and source record. A variance is any mismatch between ledger data, an information return, and the form entry. Stop if any variance is unresolved.

Roll only tied-out subtotals into Schedule D#

Schedule D is the summary layer, not the place to solve unresolved detail. Carry Form 8949 subtotals into Schedule D and confirm each subtotal matches the validated Form 8949 bucket.

For this workflow, a tie-out means the Schedule D subtotal exactly matches the corresponding validated Form 8949 subtotal. Move forward only when all subtotals tie out. Keep any mismatched bucket blocked and documented.

Carry final results into the correct return track#

Once Schedule D is clean, the rest should be a controlled carry-forward, not another round of interpretation. For 2025 instructions, if Schedule D line 16 is a gain, carry it to Form 1040 line 7a.

Keep individual and entity activity on separate filing tracks. The digital-asset Yes/No question applies across individual and entity return types, so use the return logic for each filer type.

Clear the Cross-Border Compliance Flags Freelancers Miss#

A clean domestic tie-out does not answer offshore reporting for you. Before you file, run two separate tracks and document both: your income-tax crypto reporting on the return, and your offshore information-reporting checks. A clean income-tax tie-out does not decide FBAR or Form 8938.

A few definitions keep the decision clean. In FBAR context, a U.S. person includes U.S. citizens, U.S. residents, and domestic legal entities. A foreign financial account is generally an account at a financial institution outside the United States. For Form 8938, specified foreign financial assets include foreign financial accounts and certain non-U.S. investment assets, and filer status includes specified individuals such as U.S. citizens, resident aliens, and certain nonresident aliens.

On the return track, Form 1040 filers must answer the digital-asset Yes/No question for Jan. 1 to Dec. 31, and digital-asset income must be reported on the federal return. On the offshore track, FBAR is FinCEN Form 114, not filed with the IRS, while Form 8938 is attached to your annual return and filed by that return's due date, including extensions. Form 8938 does not replace FBAR, and depending on your facts you may need one or both.

| Obligation | Who it applies to | What triggers review | What to document | Escalate when |

|---|---|---|---|---|

| Form 1040 | Form 1040 filers with digital-asset activity/income | Digital-asset activity during Jan. 1-Dec. 31, or digital-asset income to report | Yes/No answer basis and digital-asset income reporting support | Residency facts conflict with return position, or wallet/account ownership is unclear |

| FBAR (FinCEN Form 114) | U.S. persons with financial interest, signature authority, or other authority over foreign financial accounts | Aggregate foreign financial accounts exceeded $10,000 at any time in the calendar year | Account jurisdiction, authority type, ownership basis, max-value method, and required records (generally five years from FBAR due date); due April 15 with automatic extension to October 15 | You cannot verify account location, authority, ownership basis, or max value |

| Form 8938 | Specified individuals | Specified foreign financial assets meet the applicable threshold; confirm the current threshold with the relevant tax authority for the taxpayer's filing status and residency context. | Asset type, foreign institution/issuer, valuation method, and filing-status/residency basis for threshold test | You are unsure an item is a specified foreign financial asset, or filing-status/residency facts change the threshold result |

Use explicit stop and go rules for edge cases before submission:

- Mixed personal/business account use: do not assume labeling changes the FBAR test. Go only if ownership, authority, jurisdiction, and max value are documented. Stop if facts are blended across people or entities.

- Exchange custody ambiguity: do not assume reportable or non-reportable by default. Go only when jurisdiction is verifiable from records. Stop if you only have app-level branding with no reliable location evidence.

- Conflicting residency facts: if citizenship, residency, visa, or return type do not align cleanly, stop and get professional review before filing.

- Partial or joint ownership: where each person has a financial interest, each person reports the entire account value on FBAR. Do not report only your share.

Keep one cross-border memo before filing. It should record your residency position, each account's jurisdiction, ownership basis, unresolved questions, owner-by-owner follow-up tasks, and final outcome for Form 1040, FBAR, and Form 8938. If any track is still pending review, do not submit yet.

If your offshore account picture is still fuzzy, run a quick threshold check before filing so you know whether deeper review is needed: Use the FBAR calculator.

Build an Evidence Pack That Survives an IRS Question#

A defensible return depends on traceability, not just totals. To keep filing from turning into rework, make your file trace each reported amount from source records through the forms you use: Form 8949 (when required), Schedule D, and then Form 1040. If a reviewer cannot follow that path quickly, your file is not ready.

Start with storage discipline#

Create one filing-year folder and a visible checklist before you finalize forms, so missing records show up early instead of after totals are built. Use any format that keeps gaps visible; one option is:

| Artifact | Why it matters | Where stored | Status |

|---|---|---|---|

| Source records for each digital asset event | Primary support for income, basis, proceeds, deductions, or credits | /2025/source-records/ | Ready / Missing / Needs review |

| Immutable snapshots of statements and exports | Preserves what existed at filing time and helps detect unauthorized changes | /2025/snapshots/ | Ready / Missing / Superseded |

| Form 8949 workpapers | Bridges raw records into return-ready line items | /2025/form-8949-workpapers/ | Ready / Blocked |

| Schedule D tie-out | Confirms Form 8949 subtotals flow correctly to Schedule D | /2025/schedule-d-tieout/ | Ready / Blocked |

| Form 1040 support | Shows where Schedule D results land on the return | /2025/final-return-support/ | Ready / Blocked |

| Decision log for ambiguous items | Documents judgment calls and unresolved follow-up | /2025/decision-log/ | Ready / Open |

Define the file so it stays reviewable#

Use consistent definitions so the file stays reviewable:

- A source record is the primary document that supports a return item.

- A workpaper is compiled support that turns raw records into return figures.

- A tie-out is the reconciliation layer between statements and what you report.

- An immutable snapshot (operationally) is a stored version protected against unauthorized changes.

Keep dated versions of statements and exports, and do not overwrite prior files.

Build line-level support before totals#

Line-level support is what turns a pile of exports into a defensible return. Build that support before you finalize totals. The IRS sequence is records first, then gain and loss and basis, then reporting on the correct form.

Use Form 8949 as the reconciliation layer when required, and keep statement-to-return support with each reported line. Complete Form 8949 before the relevant Schedule D lines, then confirm the carryover. If Schedule D line 16 is a gain, confirm it flows to Form 1040 line 7a. Remember that digital asset transactions must be reported even when they do not produce taxable gain or loss.

Keep a decision log for judgment calls#

Judgment calls need their own paper trail. If you keep a decision log, capture enough detail to explain the treatment and any open follow-up (for example: issue, tax treatment, supporting records, reviewer, approval status, and follow-up owner). Verify retention and documentation timing against official IRS/source records or advisor records before relying on the log as filing support.

If you have ledger-backed payout history, use it as optional corroboration by mapping transaction IDs to workpapers. Consider pausing filing prep when a material amount lacks clear provenance or a judgment call still lacks an approval trail.

Fix Common Filing Errors Before They Become Notices#

This is your last consistency check before submission. Confirm the return tells one coherent story across the digital-asset question, Form 8949, Schedule D, and Form 1040. Notice risk rises when information does not match across forms or with third-party reporting.

| Error pattern | How you detect it | Immediate fix | Escalate if unresolved |

|---|---|---|---|

| Digital asset question answer does not match your tax-year activity | Compare your Yes/No answer against your transaction log for Jan. 1-Dec. 31, including receipts, sales, exchanges, or other dispositions; also confirm the answer is completed even if you did not receive Form 1099-DA | Reclassify the year's activity and correct the Yes/No answer before filing | If you still cannot determine whether the answer matches the facts |

| Form 8949 line data conflicts with statements | At line level, compare statement proceeds to Form 8949 column (d), statement basis to column (e), and any correction to column (g) | Rebuild each affected line from source records and statement amounts; do not force totals | If any amount cannot be tied to records or fair market value support |

| Schedule D does not tie to Form 8949 | Verify Form 8949 is completed first, then confirm totals flow to Schedule D lines 1b, 2, 3, 8b, 9, and 10 (or use allowed direct aggregation where applicable) | Re-carry totals from validated Form 8949 workpapers | If differences remain after line-by-line review |

| Form 1040 does not reflect the capital result | Confirm the Schedule D result carries through correctly, including the digital-asset gain/loss reporting reference to Form 1040 line 7(a) | Fix the form flow end-to-end, not just the final number | If fixing one form creates a new mismatch in another |

Third-party information mismatches are a stated CP2000-series trigger, so consistency beats speed.

Define basis issues before recalculating anything. Incomplete basis means basis was not reported to the IRS for that transaction category. Conflicting basis means basis was reported, but the reported basis is wrong and must be corrected through Form 8949 adjustment mechanics. Line-level reconciliation means each disposition is traceable from source export or statement to one Form 8949 line. If a line is not traceable, treat that as an internal quality-control stop and rebuild from dated exports and saved statements.

Run an entity-boundary check before final submission. Label each wallet, account, and statement by legal owner, separate personal and entity return paths, and confirm each transaction is reported once on one path only. If an item is still unsupported, pause filing and hand off supporting records plus the unresolved questions.

Set a Monthly Operating Rhythm So Next Filing Is Easier#

If year-end still feels like a rebuild, your monthly close may not be doing enough. Make your monthly close the default so filing season becomes a validation pass, not a reconstruction project. Your goal is simple: by filing time, each disposal is already supported for Form 8949 and ready to flow to Schedule D.

Each month, keep one live operating table and update it from dated records:

| Task | Owner | Evidence captured | Status | Escalation trigger |

|---|---|---|---|---|

| Import all wallet, exchange, and payment-platform activity for the month | You | Dated CSV/API export, monthly statement or account history, wallet/account ID, legal-owner label | Complete / Blocked / Escalated | Activity appears in a source record but is missing from your master log |

| Classify each event before calculations | You | Event tag, date/time, asset, quantity, account, disposition flag, decision-log link when judgment is needed | Complete / Blocked / Escalated | You cannot determine whether an item is a transfer, income event, or disposition |

| Resolve basis and proceeds gaps | You or advisor | Acquisition support, cost/fee support, proceeds support, valuation note when needed | Complete / Blocked / Escalated | Basis or proceeds cannot be tied to records at line level |

| Confirm disposal readiness for Form 8949 | You | Form-8949-ready line inputs (proceeds, basis, adjustments if any), tie-out to running gain/loss workpaper | Complete / Blocked / Escalated | Any disposal cannot be traced to one supportable Form 8949 line |

Use the statuses as internal control terms, not legal terms. Complete means filing support is present and no follow-up is needed. Blocked means something is missing but likely recoverable from records. Escalated means the issue needs outside judgment, for example ownership or tax treatment. A material unresolved item is anything that could change your digital asset Yes/No answer, gain or loss, legal owner, or whether a separate filing is required.

Run offshore checks quarterly as an internal control on separate tracks so they do not get mixed into income-tax form prep:

- Form 8938 track: Record whether you hold specified foreign financial assets and confirm the applicable threshold by filing status and whether you live in or outside the U.S. Do not treat directly held foreign currency as reportable on Form 8938.

- FBAR (FinCEN Form 114) track: Check whether aggregate foreign financial accounts exceeded $10,000 at any point in the year. If yes, treat FBAR as a separate filing with FinCEN, not with your IRS return. Track due dates as April 15 with automatic extension to October 15.

Freeze each monthly evidence pack as immutable, dated, and linked to your decision log, for example 2026-05-close. Keep exports, statements, the monthly table, and classification notes together. If anything is corrected later, add a new dated version and preserve the prior snapshot so every change is traceable at filing time.

Final Checklist Before You Submit#

Use this as a hard pre-filing gate. If any item fails, do not file until it is resolved.

| Check | Pass | Fail |

|---|---|---|

| Digital-asset answer | Your digital-asset answer matches your records, and nothing else in the return contradicts it | Your answer conflicts with your records or other reported items |

| Form 8949 to Schedule D to Form 1040 | All subtotals carry forward cleanly, and every adjustment is supported by records | Any amount is unsupported or unexplained |

| Form 8938 track | You verified current Form 8938 rules and thresholds, and either prepared the form or documented a supported no-file conclusion | You are assuming thresholds, guessing classification, or skipping the analysis |

| FBAR track | You tested FBAR independently, documented the result, and prepared FinCEN Form 114 if required | You treated FBAR as covered by tax-return filing or still cannot support account classification |

| Evidence packet | The folder is complete and every material position is supported | Material basis, ownership, or cross-border classification is still unsupported |

Check the digital-asset answer on your return#

Answer the digital-asset Yes/No question on your Form 1040 family return so it matches your transaction log and classifications. If you had digital-asset transactions, you still need to report them even if they did not produce taxable gain or loss.

Pass: your digital-asset answer matches your records, and nothing else in the return contradicts it. Fail: your answer conflicts with your records or other reported items, so stop and fix classification first.

Tie out Form 8949 to Schedule D and Form 1040#

Reconcile at the line level in Form 8949 first, including amounts reported on forms like Form 1099-B or Form 1099-DA, then carry clean subtotals to Schedule D (Form 1040). If any number changes without support, trace back to the last verified figure before moving forward.

Pass: all subtotals carry forward cleanly, and every adjustment is supported by records. Fail: any amount is unsupported or unexplained, so pause and reconcile before submission.

Run the Form 8938 check as its own track#

Evaluate Form 8938 separately from your capital-gains workflow. Confirm whether you meet the filing test using current rules and the current threshold for your filing context, then verify the threshold against official IRS/source records or advisor records before use.

Pass: you verified current Form 8938 rules and thresholds, and either prepared the form or documented a supported no-file conclusion. Fail: you are assuming thresholds, guessing classification, or skipping the analysis, so stop and resolve it.

Run the FBAR check as its own track#

Evaluate FBAR separately from Form 8938. FBAR is filed as FinCEN Form 114 through the BSA E-Filing System, not with the IRS. It must be tested under its own threshold of aggregate foreign financial accounts exceeding $10,000 at any point in the year.

Pass: you tested FBAR independently, documented the result, and prepared FinCEN Form 114 if required. Fail: you treated FBAR as covered by tax-return filing or still cannot support account classification, so stop and resolve it.

Make the final evidence packet and go/no-go decision#

Before filing, store one dated folder that includes internal control artifacts such as:

- source exports

- reconciliations

- filed forms

- decision log

- cross-border analysis notes

Add return PDFs and FBAR confirmation, if applicable. These are internal control artifacts that let you defend your filing position.

Pass: the folder is complete and every material position is supported. Fail: any material basis, ownership, or cross-border classification is still unsupported, so pause filing and escalate with the full packet.

Frequently Asked Questions

Do I need to report crypto on taxes if I only had a few transactions?

In many cases, yes. You must answer the digital-asset Yes/No question on your federal return, and income from digital assets is taxable. Start by reviewing each transaction and your records before you begin reporting.

Is cryptocurrency treated as property or currency by the IRS?

Property. For U.S. tax purposes, digital assets are considered property, so basis-and-proceeds reporting rules apply when you calculate gains, losses, or income. Verify current-year IRS guidance before relying on older FAQ wording, since that FAQ page generally applies to transactions completed before Jan. 1, 2025.

Which forms do freelancers usually need for crypto reporting: Form 8949, Schedule D, and Form 1040?

Often, yes. Complete Form 8949 first, reconcile reportable amounts there, carry subtotals to Schedule D, then complete your return. IRS instructions say to complete Form 8949 before Schedule D lines 1b, 2, 3, 8b, 9, and 10. If all received Form 1099-B or Form 1099-DA entries show basis was reported and no correction is needed, you may not need to file Form 8949.

What should I prepare first before I start filling crypto tax forms?

Start with records, not forms. Gather statements and any Form 1099-B or Form 1099-DA, then organize each reportable sale or exchange so it can be entered on Form 8949.

When do Form 1099-B or Form 1099-DA change how I report?

It depends. When a statement is present, report statement proceeds in Form 8949 column (d), and report statement basis in column (e) when basis is shown. If amounts need changes, make the correction in column (g). If you cannot support the change, pause instead of forcing an entry.

When should I talk to a tax professional instead of filing on my own?

When key items remain unresolved. Common triggers are unclear ownership, unresolved basis, or records you cannot reconcile to statements and Form 8949 entries. Pause and get professional review before filing if you cannot support a reporting position.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Freelance Crypto Payments That Protect Cashflow and Reduce Disputes

Crypto payments make sense only when they improve how reliably you get paid after you plan conversion, compliance, and recordkeeping up front. They can reduce friction in some international setups where traditional platforms add fees, restrictions, or extra steps. They also move risk onto conversion timing, exchange-fee exposure, and documentation quality, so use a simple acceptance test before you agree:

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Paying Taxes on Crypto Staking and Yield Farming Rewards

Use a U.S.-first baseline, then confirm everything else locally. For staking and yield farming, this article follows what the Internal Revenue Service (IRS) states and treats non-U.S. treatment as something to confirm in the local jurisdiction.