Quick Answer

Start by treating renounce us citizenship as three distinct tracks: the oath before a U.S. consular officer abroad, CLN approval by the Department of State, and tax follow-through. Confirm the legal path first, then check filing readiness before requesting an interview. Keep Form 8854 and five-year compliance certification in scope, and remember Form 8938 does not replace FBAR. If nationality, travel, or prior-year records are unresolved, pause and escalate before taking the oath.

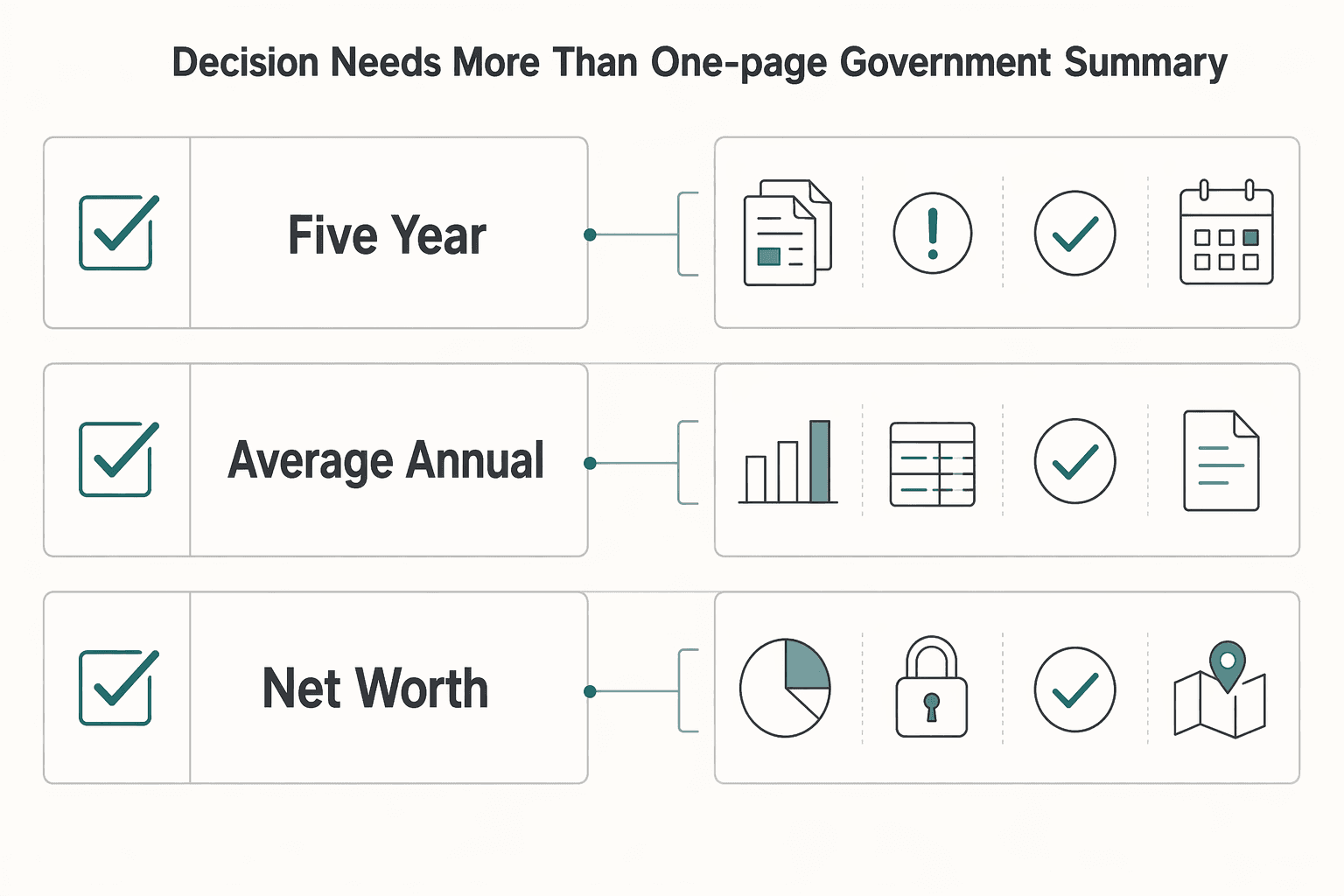

Why this decision needs more than a one-page government summary#

If you plan to renounce US citizenship, treat it as a sequence, not a single embassy appointment. In practice, you are managing three checkpoints: the consular renunciation act abroad, State Department approval reflected in a Certificate of Loss of Nationality (CLN), and tax-compliance follow-through with the IRS.

| Test | Rule | Threshold or period |

|---|---|---|

| Five-year tax compliance certification | Failing to certify 5 years of U.S. federal tax compliance on Form 8854 is one path to covered expatriate treatment | 5 years |

| Average annual net income tax liability | The IRS lists this as a covered-expatriate test | $206,000 for 2025 |

| Net worth | The IRS lists this as a covered-expatriate test | $2 million or more |

Those legal and tax tracks connect, but they involve separate checkpoints. The IRS states that expatriation tax rules under IRC sections 877 and 877A apply to U.S. citizens who renounce. It also ties consular renunciation to later CLN issuance. There is also a State Department administrative processing layer for CLN requests, which is why this is not a one-step event.

This guide focuses on voluntary renunciation before a U.S. consular officer abroad. It is not a guide to other loss-of-nationality routes.

The goal is simple: help you decide whether to proceed, execute cleanly, and avoid avoidable IRS cleanup later. The IRS describes this as a serious, irrevocable decision, and tax status is part of that decision from the start.

Before you book anything, confirm these three points with documents, not assumptions:

- Your legal lane is voluntary consular renunciation abroad.

- You have a clear record plan for each checkpoint, including CLN issuance.

- Your tax posture is ready for expatriation filing requirements, including Form 8854 and the five-year compliance certification.

One early risk matters more than most. Failing to certify five years of U.S. federal tax compliance on Form 8854 is one path to covered expatriate treatment. The IRS also lists other covered-expatriate tests, including the average annual net income tax liability threshold ($206,000 for 2025) and a net-worth threshold ($2 million or more).

The legal baseline you cannot skip#

Before you act, pin down the legal path from primary authority and save the exact text you relied on. In practice, do not rely on summary pages alone for controlling legal wording.

Confirm the legal lane first#

Confirm you are in the right legal lane, not an assumed one. A secondary case-law summary says expatriation depends on both a statutory act and intent to relinquish nationality. Use that as a guardrail against "automatic loss" claims, then verify your exact pathway in primary legal text.

Verify legal wording from official text#

Verify legal wording from official editions before you act. For legal research, treat FederalRegister.gov as informational and verify wording against the official edition or the linked official PDF checkpoint. The XML rendering is not legal notice, so save the official text you relied on in your records.

Verify the endpoint before you rely on it#

Do not assume process endpoints. Confirm the exact renunciation procedure and which document is the final agency determination directly with current primary authority before you take procedural steps. Keep the document trail you will use to prove completion.

Decision gates before you start the process#

This is your first real go/no-go point. Proceed only when your documentation is clear enough to defend year by year. Treat unresolved tax filing questions as a hard pause. Treat nationality or travel outcomes as separate issues you must verify directly in primary authority, because this material does not establish those rules.

| Decision gate | Proceed only if | Pause if | What to verify now |

|---|---|---|---|

| Second nationality status (outside this pack) | If this applies to your case, you have written, primary-authority confirmation of your status or pathway | Your status is assumed or informal | Your current nationality documents and official records tied to non-U.S. status |

| Statelessness risk (outside this pack) | If this applies to your case, you can document your post-change nationality outcome from primary authority | You cannot document a clear outcome | The exact legal outcome under the nationality law that applies to you |

| U.S. travel dependence (outside this pack) | If this applies to your case, you have confirmed your likely post-change travel path and can operate with it | Entry assumptions are still unverified | Your travel document and any entry permissions tied to that nationality |

| IRS complexity | Your filing record is organized and you can explain what was filed, by year | You are missing filings, records, or clear form-by-form status | Your current posture for Form 8938 and FBAR, plus open questions you still need to resolve for other forms |

Pause if nationality status is still unclear#

Pause if your nationality outcome is not documented. Do not move forward on assumptions. This material does not establish nationality-law outcomes, so verify those from primary authority before booking anything.

Confirm travel reality before you set timing#

Confirm travel reality before you lock timing. This material does not establish visa or re-entry rules. Treat travel access as a practical dependency you verify directly, not something to improvise later.

Audit your filing posture before you book#

Audit your filing posture before you book anything. One grounded checkpoint here is Form 8938. It is threshold-based, and a U.S. citizen is a specified individual for that test. IRS guidance includes a general $50,000 reference for certain taxpayers. It also states that higher thresholds apply for some taxpayers, including joint filers and taxpayers residing abroad.

If Form 8938 applies, attach it to your annual return and file by that return due date, including extensions. Also make sure it shows the applicable calendar year or tax year. Keep FBAR separate. Filing Form 8938 does not remove FBAR obligations when FBAR is otherwise required.

If no income tax return is required for the year, IRS guidance says Form 8938 is not required even if asset values exceed the threshold.

Build a timing sheet before you move#

Build a timing sheet that separates what is confirmed from what is still open. List each tax year, what you filed, what you should have filed, and what remains unresolved. Form 8938 mechanics and the Form 8938 and FBAR separation are grounded. Renunciation-specific Form 8854 and Schedule SE outcomes are not established here and must be verified separately before you act.

What to prepare before contacting an embassy#

Do the prep work before first contact. A solid file set makes the consular step easier and reduces the odds of messy follow-through later.

| Prep item | What to keep | Note |

|---|---|---|

| Document pack | Identity and citizenship records; tax history; prior IRS notices; intended post-change residency documents | For FBAR support, keep the underlying account records, not just filing confirmations |

| Saved instructions | Official federal guidance and local post pages; exact page relied on; date checked; contact path used | Before sharing sensitive information, confirm you are on an official federal site |

| One-page consequence memo | Travel-document or visa questions; Social Security questions; banking/KYC questions | Keep this memo as a decision tool, not a legal conclusion |

| Secure archive | Embassy correspondence; IRS submissions; FinCEN confirmations; CLN, once issued | Use consistent file labels with date and document type |

Build a document pack you can reopen later#

Build a document pack you could reopen six months later and still understand quickly. Start with identity and citizenship records, then add tax history, prior IRS notices, and your intended post-change residency documents.

For tax records, organize by year. Your checkpoint is simple: can your files support a Form 8854 certification that you complied with U.S. federal tax obligations for the 5 years before expatriation? If not, pause.

For FBAR support, keep the underlying account records, not just filing confirmations. FinCEN allows periodic account statements to determine maximum account value. FBAR filing is required when a single-account maximum or aggregate maximum exceeds $10,000 at any time during the calendar year.

Save the exact instructions you relied on#

Pre-verify instructions from official federal guidance and local post pages before you email, upload, or travel. Save the exact page you relied on, the date checked, and the contact path you used.

Before sharing sensitive information, confirm you are on an official federal site. If instructions seem inconsistent, stop and reconcile them before moving forward.

Write a one-page consequence memo#

Draft a one-page consequence memo in plain language so you are not making last-minute assumptions. Cover:

- travel-document or visa questions you still need to verify after CLN issuance

- Social Security questions you still need to verify from primary authority

- banking/KYC questions you still need to verify after a citizenship-status change

Keep this memo as a decision tool, not a legal conclusion. If key items are still assumptions, treat that as a pause signal.

Set up the archive before first contact#

Set up a secure archive before first contact. Keep embassy correspondence, IRS submissions, FinCEN confirmations, and your CLN, once issued, in one indexed system you can retrieve quickly.

Use consistent file labels with date and document type so records stay reproducible under pressure. This matters because expatriation rules depend on your expatriation date, and renunciation-date treatment is tied to later CLN issuance.

Related reading: US Citizenship-Based Taxation Explained for Mobile Freelancers.

Booking and confirming the consular path abroad#

Do not spend money until you know the local post's actual sequence. Book through the U.S. embassy or consulate in the country where you intend to live, then confirm that post's process before you pay or travel.

Choose the post tied to your intended residence#

Start with the U.S. embassy or consulate in the country where you intend to live. USAGov directs you to contact that post to sign the oath, and USEmbassy guidance confirms requests are handled by an embassy, consulate, or office providing consular services.

Checkpoint: find the exact official USEmbassy.gov page for that post covering renunciation or loss-of-nationality services. If you cannot find it, pause before booking travel.

Confirm the local sequence before requesting an appointment#

Treat the sequence as post-specific. USEmbassy describes a four-step CLN request flow tied to taking the renunciation oath abroad, and applicants are instructed to review local post information before proceeding.

Verify the order the post requires, for example, contact path first, then any pre-submission items, then appointment sequencing. Save the page, URL, and check date so your process record is reproducible.

Cross-check official guidance before you spend#

Before paying fees or traveling, confirm the local USEmbassy instructions follow the core legal path in official guidance. That means the oath of renunciation under INA 349(a)(5) before a U.S. diplomatic or consular officer abroad, and CLN approval by the Department of State as the final agency determination.

If those sources do not line up, or a local page appears incomplete, request written clarification through the post's official contact path and pause until it is resolved. This is a serious, irrevocable step.

Completing the oath appointment and CLN request#

At this stage, execution and recordkeeping matter more than speed. Complete the appointment carefully, document exactly what happened, and treat your CLN request as pending until final documentation is issued.

Confirm the case details before you leave#

Use the appointment to make sure the process record is clear, not assumed. Before you leave, confirm what was submitted, what the post retained, and what, if anything, you should expect next in writing.

If any part of the sequence is unclear, ask for written clarification through the post's official channel while details are still fresh. You can confirm contact details through Travel.State.gov's "Find U.S. Embassies & Consulates" directory.

Leave with a defensible paper trail#

Keep a complete file for this appointment:

- Appointment date and post

- Officer name/title, if provided

- Payment proof

- Submission receipts

- Copies of documents you signed or submitted

- A same-day note of what happened and in what order

This is the practical safeguard if you later need to reconcile records across institutions.

Log the formal CLN request reference#

For your records, the Department of State rule published on 03/13/2026 labels this as a "Request for Certificate of Loss of Nationality of the United States." If you maintain a legal-reference page, log Public Notice 12954, Document Number 2026-04931, and 91 FR 12296.

Use that as a tracking reference. For legal reliance, verify against an official Federal Register edition rather than relying only on the FederalRegister.gov prototype page.

Plan timelines conservatively until the CLN is in hand#

Do not treat the appointment itself as the end of the process for planning purposes. Keep your status documents organized and accessible, and avoid deadline-critical assumptions until you have final CLN documentation.

Related: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Tax obligations after the oath and before full closure#

The consular oath and tax filing closure can run on separate timelines. Treat your consular timeline and your IRS or FinCEN filing timeline as related but separate, then reconcile filings year by year before you call the case complete.

Separate the State Department clock from the tax clock#

Start with a dated timeline: oath date, tax year, extension choice, and each filing still pending. For Form 8938, keep one rule front and center: it is attached to your annual return and filed by that return's due date, including extensions.

Checkpoint: if Form 8938 may apply, confirm the form shows the correct calendar year or tax year.

Build a filing matrix before you submit anything else#

Use one matrix so you can see what goes with the IRS return, what is filed separately with FinCEN, and what still needs fact-specific review.

| Item | What to verify now | Grounded point that matters most | Common failure mode |

|---|---|---|---|

| Form 8854 | Whether it applies in your facts | This section does not set a Form 8854 deadline or outcome; confirm your exact rule set before filing | Treating it as a late add-on after other filings are already framed |

| FinCEN Form 114 (FBAR) | Whether you have a separate FBAR obligation and complete account records | Filing Form 8938 does not replace FinCEN Form 114 when FBAR is otherwise required | Assuming FATCA reporting covered FBAR |

| Form 8938 | Whether your specified foreign financial assets exceed the applicable threshold for your filing posture | Thresholds are not one-size-fits-all; higher thresholds can apply to joint filers or U.S. taxpayers residing abroad | Applying a single threshold without checking filing posture |

| Schedule SE | Whether any self-employment issue remains fact-specific for the relevant period | No blanket post-renunciation Schedule SE rule is established here; review your facts directly | Using generic summaries for a fact-specific self-employment issue |

Two sequence rules reduce errors. Form 8938 and FBAR are separate obligations. Also, if you are not required to file an income tax return for the year, you do not file Form 8938 even if asset value is above a threshold.

Repair prior-year gaps before you frame the final year#

If earlier years are incomplete, pause closure. Your filing record should read as one coherent timeline across years, not a clean final year attached to unresolved prior years.

Checkpoint for each open year: keep the return copy, proof of filing, proof of payment, if any, extension proof, if any, and workpapers used for Form 8938 and FBAR analysis.

Escalate once public summaries stop being enough#

Use a clear "speak to a pro" trigger when facts get complex. That includes incomplete prior years, complex foreign accounts or entities, possible specified domestic entity treatment, filing-status changes, uncertainty about which Form 8938 threshold applies, or unresolved Schedule SE exposure.

Lowest-risk execution comes from consistency, not speed. Map obligations, verify which filings are separate, then close the tax side with records that match the year, forms, and facts.

Your post-renunciation evidence pack for audits and border friction#

Missing records create avoidable friction later. The safer move is to keep one audit-ready evidence pack from the start.

Build one indexed master folder#

Keep one indexed folder as your source of truth, anchored by your renunciation and filing trail. Include renunciation records, IRS filings, FinCEN confirmations, and travel-status records you may need to retrieve quickly.

Use a naming pattern you can scan fast, such as YYYY-MM-DD document-type jurisdiction, so retrieval is immediate under pressure.

Add four verification fields to every file#

Every key file should show four fields: date, jurisdiction, submission proof, and retrieval location. That is what turns stored documents into usable evidence.

For IRS and FinCEN items, keep both the filed document and its acceptance or transmission record, because FBAR submissions can be rejected when required elements are not recorded.

Preserve FBAR workpapers, not just the final form#

For FBAR, keep the decision trail that supports what you filed. The key threshold is $10,000 in maximum or aggregate foreign account value during the calendar year, and each account is valued separately before assessing the total.

Store the periodic account statements you used to determine maximum values when they fairly reflect the yearly maximum. For non-U.S.-currency accounts, keep the exchange-rate source you used when Treasury rates were unavailable. Keep notes for edge cases like fewer than 25 accounts with uncertain aggregate maximums where Item 15a ("amount unknown") applies. Keep reported rounding aligned with the filed form, for example, 15,265.25 recorded as 15,266.

Assign one owner and preserve exports#

Assign one clear owner for maintaining this archive so records do not get lost across advisors, inboxes, and platforms. If someone else files or stores a document, you should still keep your own copy.

If you use tools like Gruv where enabled, preserve exports and immutable records at filing time. Relinquishing U.S. citizenship and its tax impacts are serious and irrevocable, and your documentation should be managed to that standard from day one.

Mistakes that create expensive cleanup and how to recover#

Expensive cleanup usually comes from sequence errors, not one bad form. If you plan to renounce US citizenship, stop when something is unclear, confirm what is actually complete, and rebuild missing proof before moving forward.

| Mistake | Recovery move | Grounded detail |

|---|---|---|

| Operating from one summary page | Save the exact pages you relied on, with access date and URL | If instructions seem to conflict, ask your question in writing and save the reply |

| Leaving nationality and travel documentation for later | Pause and get qualified legal advice before making decisions about relinquishment | Keep your current status documents and your post-renunciation documentation plan |

| Treating CLN status as tax closure | Start with a filing inventory: what was filed, what was accepted, what still needs support, and which dates tie to expatriation | If foreign account maximums exceed $10,000, an FBAR must be filed |

| Weak records and missing chronology | Rebuild chronology first with consular correspondence, receipts, oath-related records, the CLN, Form 8854, FBAR confirmations, and the workpapers behind those filings | For each item, keep date, jurisdiction, submission proof, and retrieval location |

Stop operating from one summary page#

Do not treat one summary page as your full execution checklist. Confirm that you are using the exact current instructions for the forms and filing systems you plan to follow before you submit or assume the next step.

Recovery move: save the exact pages you relied on, with access date and URL, in your master folder. If instructions seem to conflict, ask your question in writing and save the reply.

Do not leave nationality and travel documentation for later#

Do not leave nationality and travel documentation records for later. If your situation is unclear, pause and get qualified legal advice before making decisions about relinquishment.

The IRS is explicit on this point: consider legal counsel before deciding to relinquish U.S. citizenship. As a practical checkpoint, keep your current status documents and your post-renunciation documentation plan in your records.

Keep CLN status separate from tax closure#

A CLN is a major milestone, but it is not tax-and-reporting completion. Recovery starts with a filing inventory: what was filed, what was accepted, what still needs support, and which dates tie to expatriation.

On the IRS side, Form 8854 instructions include the "Date of relinquishment of U.S. citizenship." On the FinCEN side, FBAR has its own requirements. If foreign account maximums exceed $10,000, an FBAR must be filed. Keep submission and acceptance evidence, not just drafts, because filings can be rejected when required elements are missing.

If prior years are incomplete, use an actual compliance path instead of backfilling from memory. The IRS relief procedures for certain former citizens are designed for people who want to come into compliance and may matter if you are trying to avoid covered expatriate treatment under section 877A.

Rebuild weak records into a dated chain of proof#

When records are weak, rebuild chronology first. Start with consular correspondence, then add receipts, oath-related records, the CLN, Form 8854, FBAR confirmations, and the workpapers behind those filings.

Use one verification rule for each item: date, jurisdiction, submission proof, and retrieval location. For FBAR workpapers, FinCEN allows periodic account statements to support maximum-account-value calculations. Keep those statements and keep calculation logic consistent with the filed return, including rounding, for example, $15,265.25 to $15,266, and entering 0 when a calculation is negative. If you had fewer than 25 accounts and could not determine aggregate maximum values, document whether item 15a ("amount unknown") was used.

A tidy folder of drafts is not enough. Cleanup gets faster when every critical step is tied to dated, retrievable acceptance evidence.

For a step-by-step walkthrough, see Renouncing US Citizenship Without Tax Filing Mistakes.

What changes operationally after CLN approval#

CLN approval ends your U.S. nationality status, but it does not automatically end every follow-through task. Once the Department of State issues your Certificate of Loss of Nationality (CLN), the renunciation is approved, while tax and documentation actions may still continue.

Confirm what ended and what still follows#

Your nationality status changes with CLN issuance. Your tax obligations may not end on that same timeline. The IRS states that IRC 877 and 877A expatriation rules can still apply after renunciation. Which rules apply depends on your expatriation date, including IRC 877A for expatriations on or after June 17, 2008.

Use one consistency check across your file:

- Match the expatriation date across your CLN, Form 8854, and supporting tax records.

- Confirm whether Form 8854 includes certification of 5 years of U.S. federal tax compliance.

- If relevant, validate covered-expatriate triggers such as $2 million net worth and listed income-tax-liability thresholds, for example, $206,000 for 2025.

Plan U.S. re-entry logistics early#

After CLN approval, U.S. re-entry requirements can vary, so do not book around assumptions from your prior status. Check entry requirements early and build lead time.

Before filing or traveling, confirm core identity fields are consistent across your passport and application documents. Visa document-data errors can occur and may require correction through consular or KCC coordination.

Re-check status-dependent admin records#

Revisit accounts and systems that track citizenship or tax status, and update records that still reflect your former status. Keep your CLN available as proof of status if requested, and keep confirmation that updates were accepted. This helps prevent repeated follow-up requests caused by stale profile data and makes post-renunciation admin work more predictable.

Final checklist before you commit#

Proceed only when each checkpoint is documented, not assumed. If any item is unclear, pause and get qualified international tax or legal advice before proceeding.

Verify the current official process for your case#

- Confirm the current process through official U.S. government channels for your location.

- This section does not establish the legal test, booking workflow, CLN timing, fees, or post-renunciation travel outcomes, so treat those as verify-before-acting items.

- Save the exact page URL, date checked, and any written official response in your records.

Clear nationality and travel risks before you proceed#

- Do not move forward with unresolved questions about non-U.S. nationality status, visa access, or near-term U.S. travel implications.

- If any of those points are still hypothetical, stop and escalate before taking further action.

Keep tax closure separate from nationality steps#

- IRS states U.S. citizens must report and pay U.S. tax whether they live in the United States or abroad.

- Assign clear ownership for open tax work, for example, return gaps and record collection, so nothing is left implicit.

- If prior-year compliance is incomplete or covered expatriate risk is in play, escalate to a specialist.

Validate Form 8938 and FBAR logic#

- Form 8938 applies to certain taxpayers with specified foreign financial assets above thresholds. Do not treat

$50,000as a universal rule because higher thresholds can apply for joint filers and some taxpayers residing abroad. - Form 8938 must be attached to your annual return and filed by that return's due date, including extensions, and it requires the correct calendar year or tax year.

- Filing Form 8938 does not replace FBAR (FinCEN Form 114).

- If you are not required to file an income tax return for the year, Form 8938 is not required.

Build the evidence pack before committing#

- Keep official process communications, identity records, filed returns, Form 8938 copies, FBAR confirmations, and IRS correspondence in one retrievable system with backups.

- For each file, keep the date, submission proof, and retrieval location.

We covered this in detail in A Guide to Filing Your Final US Tax Return After Renouncing Citizenship.

If your final checklist still has execution gaps, contact Gruv to confirm whether our compliance-gated money workflows and audit-ready records fit your post-renunciation operations.

Frequently Asked Questions

Can I renounce U.S. citizenship while physically in the United States?

Do not rely on a blog-level yes or no for this point. Use Travel.State.Gov's relinquishing-nationality page and the “Find U.S. Embassies & Consulates” path to confirm the current process with the post handling your case. If an answer skips that verification step, treat it as low confidence.

Is renouncing U.S. citizenship reversible?

Do not make this decision assuming you can reverse it later. This section does not have sourced support to give a legal yes or no on reversibility, so verify directly with current U.S. Department of State guidance. For high-stakes family or travel consequences, confirm with counsel before you schedule anything.

What is a Certificate of Loss of Nationality (CLN), and when is it final?

This section does not provide a sourced finality rule or timeline for CLN issuance. Treat those points as items to verify from current State Department materials for your specific case. Operationally, keep your official State records and related correspondence organized in one permanent file.

What is the difference between renouncing citizenship and losing citizenship involuntarily?

This section is not sourced to define that legal boundary in detail. If your facts are not straightforward, do not rely on summaries. Get case-specific legal advice before acting.

Do I still have U.S. tax filing obligations after taking the oath?

This section is not sourced to determine your filing outcome after the oath. If your history is complex, get a professional review before you treat the process as complete.

Can I receive Social Security benefits after renunciation?

This section does not claim benefits are guaranteed or denied based on renunciation alone. What is supported is that SSA Totalization Agreements are meant to prevent dual social security taxation and help cover workers who split careers between the United States and an Agreement country. When U.S. coverage applies under an agreement, SSA says a Certificate of Coverage is proof of exemption from foreign social security taxes.

What are the biggest risks if I handle this process in the wrong order?

A practical risk is moving forward on assumptions instead of verified process steps. For SSA Certificate of Coverage requests, required fields must be completed to submit, and incomplete information can prevent an accurate and timely decision. Use the portal status checkpoints (including “Received”), allow 90 business days before following up, and if a certificate is issued, allow up to two additional weeks for mailing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- common.usembassy.gov/en/renounce-citizenshiptrusted

- federalregister.gov/documents/2026/03/13/2026-04931/schedule-of-...trusted

- federalregister.gov/documents/2019/08/14/2019-17142/inadmissibil...trusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/individuals/international-taxpayers/expatria...trusted

- irs.gov/individuals/international-taxpayers/relief-p...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

Build a Freelance Media Kit That Reduces Client Friction

Treat your media kit as a buyer decision tool, not a design exercise. If a prospect can spot fit, proof, and the next action quickly, you cut a lot of avoidable back and forth before a call is scheduled. That is this document's job.