Quick Answer

Yes, you can register as a sole trader in the UK by completing HMRC Self Assessment and then managing the follow-through properly. In practice, that means choosing the structure first, submitting accurate registration details, securing your UTR when it arrives, and keeping clean records from day one. The article’s core operating rule is simple: separate business finances, maintain evidence for each transaction, and verify live rules before acting on VAT, visa, or cross-border tax form requirements.

The 'Business-of-One' Blueprint: How to Register as a UK Sole Trader for Global Operations#

What to confirm before you start#

If you want to register as a UK sole trader, the path is straightforward: confirm the structure fits, complete registration through Self Assessment, then stay on top of ongoing filing obligations.

Use this guide if you're a UK-based independent professional, or you're registering in the UK and want to work with clients in the UK or abroad without guessing your way through setup.

Choose the structure before you file#

Choose the structure before you file anything. GOV.UK puts this first for a reason. A sole trader is a type of business where you work for yourself and make the business decisions personally. If you are about to register as a UK sole trader, the real first move is checking whether that structure fits your risk, income pattern, and how you plan to operate.

Register through the right tax route#

Register through the right tax route. HMRC is the UK tax authority. Self Assessment is the process used to report income that is not fully taxed through payroll, and your UTR is the 10-digit tax reference HMRC issues when you register for Self Assessment. HMRC screens and wording can change, so verify the live GOV.UK process before you submit anything.

One early checkpoint matters more than many people think. You can start trading before registering, but that does not remove the obligation to register when the rules apply. If you earn more than £1,000 from self-employment in a tax year running from 6 April to 5 April, you generally need to tell HMRC by 5 October after that tax year ends. Miss that and you may face penalties.

Keep your evidence pack clean from day one#

Keep your evidence pack clean from day one. Before you begin, keep your key records organized. After registration, expect to file Self Assessment tax returns, and expect your UTR by post in around 15 days, or longer if you live overseas. If that 10-digit reference has not arrived, do not assume your setup is finished.

Treat the rest of this article as a checklist-led guide, not legal advice. The next section helps you make the structure decision before you commit.

If you want a deeper dive, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

The First Strategic Choice: Is a Sole Trader Structure Right for You?#

Make this decision before you register: a sole trader setup fits best when your risk is genuinely low, you want the simplest admin path, and your target clients are comfortable buying from an individual. Reconsider it if one project failure could become expensive, your profits are stabilizing, or your buyers expect an incorporated supplier.

Stress test your liability, not just your enthusiasm#

As a sole trader, you are the only owner and legally responsible for all parts of the business, including debts. If the business cannot pay, that exposure does not stay inside a separate legal entity.

Focus on downside, not intention. In lower-risk work with tight scopes, disputes may stay around non-payment or limited rework. In higher-risk work, such as strategic advisory, software delivery, client data handling, ad-spend management, or contracts with IP warranties, the potential downside can exceed the project fee.

A practical checkpoint: review your last three proposals or contracts and flag indemnities, liability caps, data protection clauses, refund exposure, and insurance requirements. If those terms are unclear to you, treat your risk as not low.

Decide whether you value simplicity now or planning flexibility later#

Sole trader tax reporting is often simpler because business profit is taxed on you personally. That can help in year one when you are still validating your offer.

The tradeoff is future flexibility: other structures can offer different planning options once profit is steady and you are not withdrawing everything for personal use. For UK decisions, verify live GOV.UK figures for Income Tax bands, National Insurance, Corporation Tax, dividend tax, and the VAT threshold before choosing.

Check your market through a procurement lens, not a branding lens#

If you mainly sell to smaller firms, agencies, startups, or direct clients, legal form may not be the deciding factor. If you target larger organizations, procurement requirements can be stricter.

Check your market directly: review ten target clients, or one recent RFP/vendor form, for legal-entity fields, insurance requirements, onboarding documents, and supplier compliance checks. If incorporated status appears repeatedly, treat that as a commercial signal.

| Decision area | Choose sole trader if | Reconsider if |

|---|---|---|

| Liability exposure | Your projects are low consequence and contract terms are narrow | One failed project could create a serious claim, refund, or debt |

| Tax posture | You want the simplest setup while revenue is still uneven | Profits are becoming steady and you want more planning flexibility |

| Client fit | You mainly sell to solo-friendly buyers and smaller firms | Your target buyers favor or require incorporated suppliers |

| Contract complexity | Your terms are short, clear, and manageable | Your agreements include heavier indemnity, data, or delivery obligations |

If two or more rows land in the reconsider column, pause before filing and compare structures in Sole Trader vs. Limited Company: A Guide for UK Freelancers. Related: Understanding the UK's Statutory Residence Test (SRT).

The Registration Blueprint: Securing Your UK Business Identity#

Treat this as a three-step job: confirm you need to register, complete HMRC registration cleanly, then secure your UTR and use it correctly.

| Stage | Main check | Key detail |

|---|---|---|

| Need to register | Register for Self Assessment if you earn more than £1,000 from self-employment in a tax year | Tax year runs 6 April to 5 April; if you need to complete a tax return for the previous year, tell HMRC by 5 October |

| HMRC access | Have your National Insurance number ready and make sure you can sign in | Use Government Gateway or GOV.UK One Login; if Self Assessment became inactive, reactivate it before filing |

| UTR | Secure and store your 10-digit UTR | HMRC usually sends it by post in around 15 days, or longer if you are overseas |

Confirm you need to register#

You must register for Self Assessment as a sole trader if you earn more than £1,000 from self-employment in a tax year (6 April to 5 April). You can start trading before you register, and you can choose to register earlier.

The key deadline is HMRC's rule: if you need to complete a tax return for the previous year, you must tell HMRC by 5 October. If you register late when registration is required, you may get a penalty.

Prepare your HMRC access and submit once#

Use HMRC's Self Assessment route, and prepare before you start so you can finish in one pass.

- Have your National Insurance number ready.

- Make sure you can sign in with Government Gateway or GOV.UK One Login (or create sign-in details during the process).

- If you already use Self Assessment for another reason, register again as a sole trader.

- If you had Self Assessment before and it became inactive, reactivate it before filing to avoid delays.

Once you submit, check that your registration confirmation is in place.

Secure your UTR and use it properly#

After registration, HMRC usually sends your 10-digit UTR by post in around 15 days (longer if you are overseas). Store it securely and keep the original letter.

You will need your UTR for your Self Assessment tax return, and HMRC uses it to identify you. If you cannot find it, check your Personal Tax Account, the HMRC app, and HMRC letters first, then contact HMRC.

Common mistakes to avoid

Missing the 5 October notification point, assuming an existing Self Assessment setup already covers sole trader registration, and filing without reactivating an inactive account can all create delays or penalties. Also keep HMRC sign-in details private. HMRC says not to share them, including with a tax agent.

You might also find this useful: The Best Business Bank Accounts for UK Sole Traders.

Beyond Registration: Building Your Compliance Firewall#

After registration, your compliance strength comes from three controls you set up now: a business-only account, a bookkeeping system you will actually maintain, and a live calendar for tax obligations.

| Control | What it covers | Details named |

|---|---|---|

| Business-only account | Separate business money from personal spending | Pay client income in, pay business costs from it, label owner draws clearly, and reconcile monthly |

| Bookkeeping system | Keep records current with minimal friction | Selection criteria include bank feeds, receipt capture, invoicing and payment tracking, tax-year reporting, and accountant access |

| Compliance calendar | Track tax obligations early | Set it now, then verify current UK rules directly with HMRC before relying on the dates or thresholds |

Use one account only for business flows#

Use one account only for business money so every transaction has a clear purpose.

- Pay all client income into this account.

- Pay business costs from this account (for example software, contractors, domain renewals, travel, and work equipment).

- Transfer money to yourself as a clearly labeled owner draw, instead of paying personal spending from business funds.

- Keep personal spending out of this account.

- Reconcile monthly against invoices, receipts, and statements.

Your monthly check is simple: every incoming payment matches an invoice or agreement, and every outgoing payment has a receipt or clear business note.

Choose bookkeeping software for fit, not familiarity#

Pick software based on workflow fit, not brand familiarity. The core test is whether it helps you keep records current with minimal friction.

Use these selection criteria:

- Bank feeds

- Receipt capture

- Invoicing and payment tracking

- Tax-year reporting

- Accountant access

Before committing, confirm it can keep the full record set together: invoices, receipts, contracts, statements, and tax correspondence linked to transactions.

Build a compliance calendar early#

Set your compliance calendar now, then verify current UK dates, thresholds, and rules directly with HMRC before relying on it.

| Compliance item | What to track now | Current date/rule |

|---|---|---|

| Self Assessment filing | Filing deadline and prep lead time | Current HMRC filing deadline pending official verification |

| Tax payment | Payment deadline and reserve target | Current HMRC payment deadline pending official verification |

| National Insurance | Contribution type, thresholds, and whether action is needed to protect your contribution record | Current National Insurance rules, thresholds, and rates pending official verification |

| Payments on account | Whether you are in scope and when advance payments fall due | Current payments-on-account trigger and dates pending official verification |

For National Insurance, make a yes/no decision each year on contribution treatment based on current rules, especially in lower-profit years. For payments on account, treat it as cash-planning risk first: reserve funds as income arrives so advance payments do not become a surprise.

Failure points and prevention

Mixed finances: enforce the one-account rule from day one.

Late records: schedule a fixed weekly admin block to post receipts and clear uncategorized items.

Missing reserves: move a set percentage of each payment into a separate tax pot.

Ignored notices: review each HMRC message when received and update your calendar immediately.

Once these controls are in place, cross-border invoicing is easier to manage because your core records are already clean.

This pairs well with our guide on Sole Trader vs. Company: A Guide for Australian Freelancers.

Operating Globally: Invoicing International Clients Like a Pro#

Cross-border invoicing stays clean when you follow the same order every time: confirm client status first, issue the invoice second, and store the evidence pack with the transaction.

| Area | First check | Records or control mentioned |

|---|---|---|

| EU invoicing | Classify the client as business (B2B) or non-business before applying invoice and tax treatment | Keep the signed contract, contracting-entity confirmation, and business-status evidence with the invoice record |

| US client tax forms | Confirm whether the client wants foreign-status documentation or US-person documentation, then verify the exact form requirement | Keep the client request email, submitted form copy, contract, invoice, remittance advice, and any withholding notice together |

| Multi-currency operations | Pick contract currency on purpose and define fee handling and deduction rules before invoicing | Follow one conversion policy and reconcile invoice total, gross received, fees deducted, and GBP booked amount monthly |

EU invoicing: separate B2B and non-B2B before you send#

For EU clients, do not draft from assumptions. First classify the client as business (B2B) or non-business, then apply the invoice and tax treatment only after you verify the current rule for that case.

Use one invoice template with this checklist:

- Your legal name and the client's legal name

- Invoice number and invoice date

- Service description and service period

- Currency and payment terms

- Any tax identifier or tax wording required once the rule is confirmed

If your verified outcome requires reverse-charge wording, confirm the current wording requirement from official guidance before using it on an invoice.

Keep proof of classification with the invoice record: signed contract, contracting-entity confirmation, and the business-status evidence you relied on. This step matters because different systems can require very different treatment. For example, Australia separates non-resident GST into standard and simplified pathways, and simplified registration does not allow tax invoices or GST credits.

US client tax forms: verify the request before you sign#

For US clients, send a form only after you confirm what status they want certified and what you are actually eligible to certify. In practice, confirm whether they are asking for foreign-status documentation or US-person documentation, then verify the exact form requirement before submission.

Keep these documents together in one file trail:

- Client request email

- Submitted form copy

- Contract

- Invoice

- Remittance advice and any withholding notice

Do not hard-code rates or outcomes in your template; verify the current form and withholding context for your case from official or client-provided records before use.

Multi-currency operations: set policy in contract, then reconcile to books#

Pick contract currency on purpose. If your costs are mostly in GBP, GBP billing can reduce conversion noise; if the client requires another currency, define fee handling and deduction rules in the contract before invoicing.

Then choose one conversion policy and follow it consistently:

- Convert on receipt

- Convert on a fixed monthly date

- Hold foreign currency to a defined reserve level

Reconcile monthly across four lines: invoice total (billing currency), gross received, fees deducted, and GBP booked amount.

| Payment setup | Fees visibility | Admin burden | Record-keeping clarity |

|---|---|---|---|

| Bank transfer | Can be unclear unless remittance details are complete | Low to medium | Good if gross and charges are both visible |

| Platform wallet | Fees and FX can be bundled in payout data | Medium | Lower unless you export detailed reports |

| Multi-currency account | Usually clearer across receipt, hold, and conversion | Medium | Strong when receipt, conversion, and payout records are stored together |

Use this final control checklist each month:

- Verify client legal entity and status before first invoice

- Store evidence with the invoice record, not only in email

- Confirm currency and fee responsibility in the contract

- Reconcile gross, fees, and converted GBP separately

We covered this in detail in Get a UK UTR as a Freelancer Without Mixing UK and Australia Rules.

You're Not Just Registered - You're Ready to Scale#

Registration is your foundation. Scaling works when your records are provable, your cash position is clear, and each new market check happens before you expand.

What you should have in place now#

- Registration status and reference record: Keep your registration confirmation and any official tax reference notice you already hold in one live file. This is your first proof set when a client or authority asks for evidence.

- Banking separation (operational control): Keep business cash movement separate from personal spending so inflows, outflows, and owner transfers are easier to trace.

- Bookkeeping workflow: Maintain a current ledger or software export so you can answer income and expense questions quickly.

- Retrieval test: You should be able to pull a contract, invoice, payment proof, and matching expense record within minutes.

What to monitor each month#

Check invoices issued against cash received, track unpaid balances, and confirm each expense still has supporting documentation. Reassess sole trader vs limited company when liability exposure, contract complexity, or admin burden increases, since a sole trader is legally responsible for business debts.

| Area | Reactive operations | Structured operations |

|---|---|---|

| Cash visibility | You estimate from the bank balance | You reconcile invoices, payments, and owner transfers |

| Compliance readiness | Records are spread across inboxes and apps | Each client or tax event has one complete evidence pack |

| Client-facing professionalism | Documents are assembled late | References, invoices, and confirmations are ready quickly |

Before you add international volume#

Your current setup does not automatically satisfy another country's registration rules. For example, in Australia, GST registration can be required at $75,000 turnover, and once required, registration must be completed within 21 days; non-residents may choose standard or simplified GST registration, and simplified registration issues a 12-digit ARN but does not provide an ABN or GST credits.

Before you expand, run one scale-readiness check: audit your evidence pack, fully reconcile last month, and verify the first registration trigger in the next market. For a step-by-step walkthrough, see Choosing an Eenmanszaak in the Netherlands as a Sole Trader.

Frequently Asked Questions

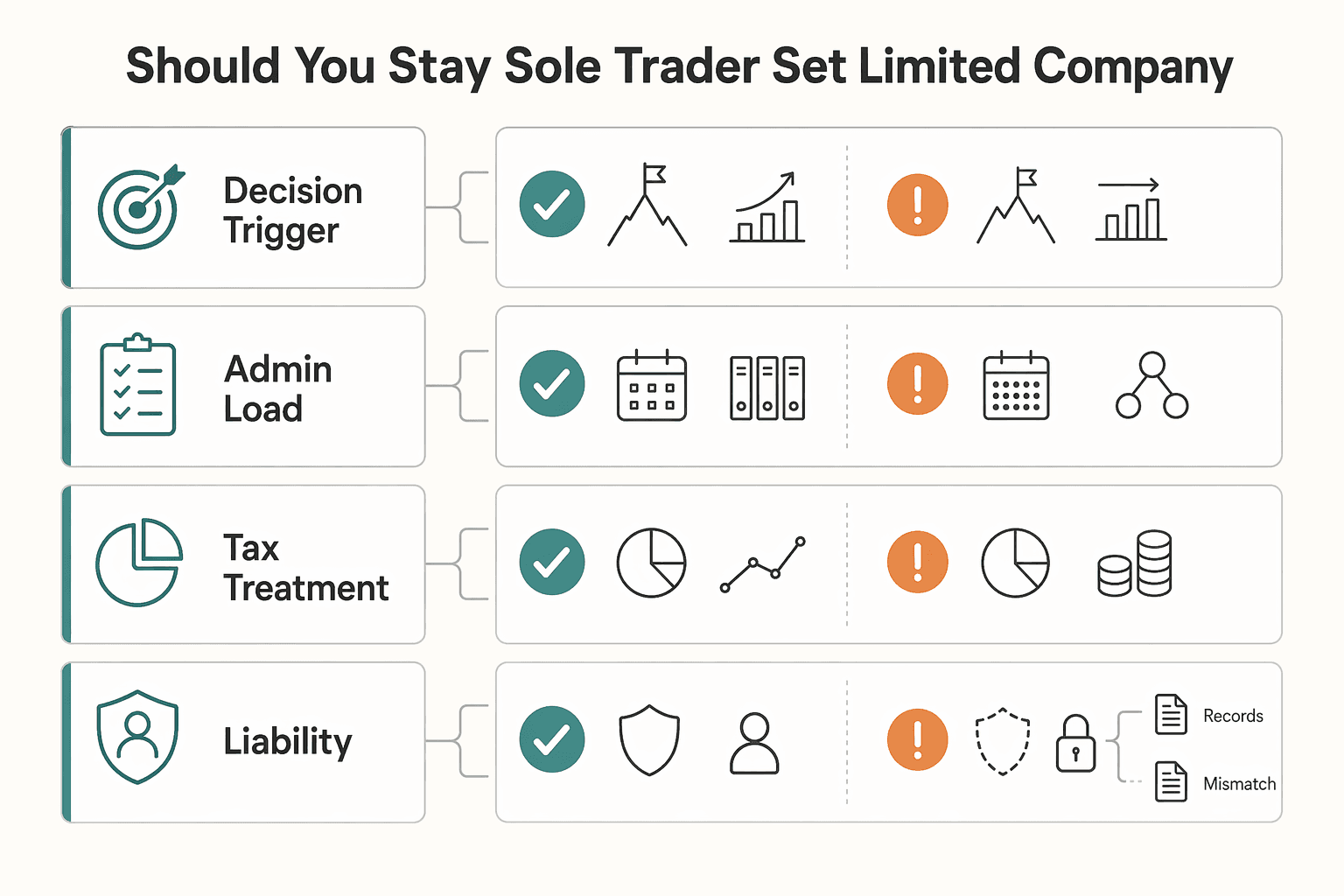

Should you stay a sole trader or set up a limited company?

Treat this as a scoping checklist and verify current UK guidance before acting. Use the quick table below to frame your decision, then read the deeper comparison in Sole Trader vs. Limited Company: A Guide for UK Freelancers. | Decision point | Sole trader | Limited company | |---|---|---| | Decision trigger | Confirm whether this route fits your current risk and admin tolerance | Confirm whether this route better fits your client, contract, and growth setup | | Admin load | Verify current filing and record-keeping duties in UK guidance | Verify current filing and record-keeping duties in UK guidance | | Tax treatment | Verify current personal tax treatment for your case | Verify current company and personal tax treatment for your case | | Liability | Verify current legal exposure for your exact setup | Verify current legal separation and any guarantee-related exposure for your setup |

Do you need a separate bank account as a sole trader?

It is still a cleaner operating choice to open one early and keep your records tidy with four basics: all client payments into one account, owner transfers labelled clearly, monthly statements saved as PDFs, and each expense matched to a receipt or invoice.

What if you register late with HMRC?

Confirm the current HMRC deadline and any consequences from official HMRC guidance before planning your filing, then save your submission confirmation, start-date evidence, first invoice, and first payment record together.

Do you need a UTR before you can operate?

Do not guess what reference HMRC or a client form actually needs. Check the exact notice or request, and if a form asks for a UTR, copy it only from an HMRC document you already hold rather than substituting another ID or made-up value in a signed form.

How should you handle EU business client invoices?

Verify the client's business status and the live wording requirement from official or source records before invoicing. Keep the supporting file with the invoice record: signed contract, client legal entity confirmation, and any VAT or registry check you used.

Can you trade on a visa in the UK?

Confirm your exact permission with UKVI before you start trading, and keep the visa decision notice, status share code record, or adviser email in your onboarding file so you can show why you believed self-employment was permitted.

What are Class 2 and Class 4 NICs, and how should you plan for them?

This pack does not verify current Class 2 or Class 4 thresholds or rates. Confirm the live National Insurance thresholds and rates from official HMRC guidance before using them in a forecast, then reconcile your estimate to your filed Self Assessment rather than relying on monthly guesswork.

What is the most common paperwork mistake after you register as a UK sole trader?

Avoid mixing tax, banking, and client evidence across inboxes and folders. Keep one record set per client or tax event with the contract, invoices, payment proof, expense documents, and any HMRC notice or Self Assessment reference that relates to it.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- abr.gov.au/business-super-funds-charities/applying-abn/...trusted

- ato.gov.au/businesses-and-organisations/international-t...trusted

- ato.gov.au/businesses-and-organisations/international-t...trusted

- community.ato.gov.au/s/question/a0J9s0000001Dmq/p-00029303trusted

- taxconfident.campaign.gov.uk/small-businesses-and-tax/ways-we-collect-tax...trusted

- gov.uk/become-sole-trader/register-sole-traderexternal

- gov.uk/find-utr-numberexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

Sole Trader vs Limited Company UK for Freelancers

If you need a practical starting rule, choose sole trader for a faster start and lighter admin. Choose a limited company when legal separation and company-level compliance are worth the extra work.