Quick Answer

A freelancer or small team should read a balance sheet as a point-in-time view of assets, liabilities, and equity, then use it to judge liquidity, obligations, tax readiness, and growth timing. Start by classifying each line correctly, keeping business and personal items separate, tying major lines to records, and confirming Assets = Liabilities + Equity before making decisions.

Forget Accounting Class. This is Your Business Command Center.#

Use your balance sheet as a dated decision dashboard, not an accounting exercise. It shows what your business owns, what it owes, and what is left on that date. Use it to make better calls on cash safety, client risk, tax readiness, and growth timing.

If you want to understand how to read a balance sheet in practice, start with the right frame. This is a snapshot, not a month-long or year-long story. It should help you answer operational questions quickly. Can you absorb delayed client payments? Are upcoming obligations fully visible? Are your records ready for tax prep? Is now the right time to commit cash to new spending?

This guide is educational, not legal or tax advice. Tax and legal treatment is jurisdiction-specific, so confirm treatment with a qualified advisor. Keep estimates tied to current records, because records support financial statements and you remain responsible for what is reported.

| Bucket | Freelancer examples | Decision it informs |

|---|---|---|

| Assets | Bank balances, unpaid client invoices, funds held in payment platforms | How much liquidity you actually have if cash inflow slows |

| Liabilities | Credit card balances, loans, known tax obligations, supplier bills | What claims on your cash are already building |

| Equity | Residual value after liabilities | Whether your business position is strengthening or being drained |

Use this review cycle each time:

- Gather records. Pull current bank statements, platform balances, open invoices, debt balances, and your latest tax estimate.

- Normalize currency. Convert foreign-currency amounts into one reporting currency using a consistent method required by your reporting framework, and confirm tax treatment with a qualified advisor.

- Classify items. Place each line under assets, liabilities, or equity, then confirm the statement reconciles to Assets = Liabilities + Equity.

- Evaluate risk signals. Check for thin cash versus near-term obligations, cash stuck in receivables, and estimates that no longer match records.

What a "Business-of-One" Balance Sheet Is (And What It's Not)#

A business-of-one balance sheet is a point-in-time position statement. It shows what the business owns, what it owes, and the residual interest on that date. It should always reconcile to Assets = Liabilities + Equity. It is not an income statement, not a cash flow statement, and not a complete tax filing.

Step 1. Classify each line by rule, not instinct#

Use the rule that fits the line item. Assets are resources the business owns. Liabilities are obligations the business owes. Equity is what remains after liabilities are subtracted from assets.

For current classification, use the 12-month checkpoint. Does it convert to cash, or require settlement, within 12 months?

| Line item | Include | Where it goes | Why |

|---|---|---|---|

| Multi-currency cash in business accounts | Yes | Asset | It is cash the business controls |

| Unpaid client invoices | Yes | Asset (typically accounts receivable) | Customers owe the business for services already delivered |

| Software commitment for future service | Maybe | Liability only if already owed | A future subscription is not automatically a present obligation |

| Tax provision | Maybe | Liability | Include when a present obligation exists and outflow is probable |

| Equipment used in the business | Yes | Long-term asset | Equipment is generally not readily converted to cash |

| Owner draws | Maybe | Verify by entity type | Treatment differs by entity type |

Step 2. Keep business and personal items separate#

Keep a hard boundary between business and personal items. Personal, living, and family costs do not belong on the business statement, and mixed-use items should be split before classification. If you cannot support the business portion with records, exclude it until verified.

Also separate accrual obligations from already paid costs. If an obligation is contingent or unverified, do not recognize it on the balance sheet yet. Mark it as pending verification instead.

Step 3. Tie major lines back to records#

Do not use the statement for decisions until every major line ties back to records. Match cash to account records, receivables to issued invoices, and liabilities to documented obligations. If it does not balance, or a line has no support, fix that first.

Local accounting and tax treatment can differ by country, state, and entity structure. Where rules vary, mark the current treatment as pending local advisor verification before using it for decisions.

Assessing Your Financial Resilience: Can You Survive a Crisis?#

Resilience comes down to one question: can your balance sheet absorb a common shock without breaking near-term obligations? Start with a conservative runway calculation, then test it against delayed cash, client loss, and FX movement.

Step 1. Define usable liquidity and burn rate#

Use a strict Runway Ratio: Runway Ratio = usable liquid assets / monthly burn rate

For this section, usable liquid assets include cash on hand, demand deposits, and qualifying cash equivalents that are readily convertible to known cash amounts with low value volatility. Keep receivables out of this numerator. They may be current assets, but they are not the same as cash on hand today. Also exclude cash restricted from being exchanged or used to settle a liability for at least 12 months after the reporting period.

Treat burn rate as an operating metric, not a formal GAAP or IFRS line item. It is the monthly pace of cash depletion in a loss period. Include unavoidable operating cash outflows you must keep paying, such as committed contractors, rent, software, loan payments, and taxes already due. Exclude non-cash items and optional investments not yet committed.

If you need a minimum owner transfer to keep operating full time, track it as a documented overlay instead of burying it in operating costs.

Checkpoint: Calculate runway twice: first with cash and cash equivalents only, then again with self-segregated reserves removed. If the second result changes your decisions, liquidity is tighter than it looks.

Step 2. Place yourself in a decision band#

Use decision bands that fit your business, not a universal cutoff. If you need hard numeric thresholds for policy or reporting, keep the threshold pending policy or advisor verification until you have a current source.

- Fragile: one late invoice, one adverse FX move, or one surprise bill could cause a missed near-term obligation or reserve breach.

- Stable: current liquidity covers near-term obligations, and a routine payment delay does not immediately break the plan.

- Strong: you can absorb at least one modeled shock and still meet near-term obligations without breaching reserve policy.

Step 3. Age receivables and adjust the forecast#

Receivables aging should change how much trust you place in your cash forecast. In a 2024 small-business payments report cited by the Boston Fed, 80% of respondents reported challenges in sending and receiving payments. Treat delayed cash as a normal risk, not an exception.

Use aging buckets to adjust forecast treatment and escalation:

| Aging bucket | Cash forecast treatment | Follow-up cadence | Escalation step |

|---|---|---|---|

| Current to 30 days | Include in near-term cash only when invoice is issued, accepted, and consistent with client payment history | Review during each forecast cycle | Confirm receipt and approval status when timing matters |

| 31 to 60 days past due | Remove from high-confidence next-30-day cash unless payment timing is confirmed | Increase follow-up intensity versus current invoices | Escalate from reminders to direct collection discussion with decision-maker |

| 61 to 90 days past due and older | Treat as low-confidence cash or exclude from runway support | Maintain active follow-up until resolution or reclassification | Consider formal escalation, including collections handoff where appropriate |

Checkpoint: Each past-due invoice should have an owner, last-contact date, and dispute status. Without that, your forecast is probably overstating liquidity.

Step 4. Stress-test three common shocks#

Run all scenarios in one base-currency view anchored to your functional currency.

| Shock | Test |

|---|---|

| Late payment shock | Move one expected receipt into the next aging bucket and remove it from the next 30-day cash forecast. Recalculate runway and identify which payables become uncovered first. |

| Client loss shock | Remove expected inflows from your largest client for the test period. Day-one runway may look unchanged, but obligations over the next 30 to 90 days can deteriorate quickly. |

| FX movement shock | Retranslate foreign-currency cash, receivables, and payables after an adverse rate move, then rerun runway and near-term obligations. FX effects on monetary items can flow through profit or loss. Operationally, the key question is whether usable liquidity shrank against bills due soon. |

Step 5. Set a reserve and currency policy you can run#

Keep the policy simple enough that you will actually follow it.

- Reserve segregation: keep emergency or tax reserves in separate accounts, or at minimum separate balance-sheet lines.

- Base-currency policy: track cash exposure in one base currency aligned to your functional currency.

- Rebalance trigger: define when foreign-currency holdings have drifted enough to require rebalancing, with the threshold pending policy or advisor verification.

- Review cadence: review runway, aging, and FX exposure on a fixed schedule and after major invoice delays, client loss, or contract changes.

If you do only one thing, calculate runway from truly usable liquidity, not optimistic receivables.

Planning for Strategic Growth: Can You Afford to Invest in Yourself?#

Once you know your business can absorb a shock, the next question is whether it can safely fund a new move. A growth investment is usually affordable when your balance sheet can absorb the timing gap between spending now and collecting cash later. Headline ROI is not enough if cash flow breaks first.

Step 1. Choose and label the debt-to-equity version before you use it#

Start by naming which Debt-to-Equity convention you are using, because the numerator is not universal. The SEC educational convention uses total liabilities / owner equity, while CFA materials use total debt / owner equity. Those inputs are not interchangeable.

For a business-of-one, owner equity is the residual net-worth figure: assets minus liabilities. If equity is negative, or near zero, D/E can become unstable as a decision tool. Treat that as a warning and shift to a cash-first approval decision.

If you use the SEC-style version, liability inputs can include current obligations such as vendor payables, taxes, interest, rent, utilities, and payroll-related accruals due within one year, or the operating cycle if longer. If you use the CFA-style version, the numerator is narrower. It covers interest-bearing short- and long-term debt, excluding accounts payable and accrued expenses.

Checkpoint: Label the metric directly in your sheet, for example, D/E (SEC-style) or D/E (debt-only). If you cannot confirm what is included in the numerator, do not compare periods.

Step 2. Put the ratio in a decision band, not a generic "good" zone#

A ratio alone should not approve a purchase, loan, or hire. Use action bands tied to your own history, and to peers where relevant. Treat numeric cutoffs as unverified until they are checked against policy or advisor records.

| Ratio condition | What it usually means | Action |

|---|---|---|

| Negative or near-zero equity | Small accounting changes can make D/E extreme or not decision-useful | Do not approve debt-funded growth from this ratio alone; use runway, near-term obligations, and collections quality first |

| Below internal low-risk threshold | Balance sheet may support added commitments if cash timing also works | Proceed to the investment screen |

| Between low-risk and escalation threshold | Capacity may exist, but timing and downside need closer review | Require a written payback case and delayed-payment stress test |

| Above escalation threshold | Added obligations may crowd out taxes, payables, or reserves | Delay, reduce scope, or restructure |

| Thresholds not yet verified | No grounded cutoff exists for your case | Threshold pending policy or advisor verification |

Red flag: if the ratio looks acceptable mainly because gross receivables are high but aging quality is weak, real capacity is probably lower than it appears.

Step 3. Screen the investment like a repayment problem#

Before you approve a course, equipment purchase, subcontractor expansion, or financed software commitment, treat it like a repayment problem:

| Screen item | What to check |

|---|---|

| Expected revenue impact | Define the mechanism, such as higher rates, more billable capacity, or access to a new client tier, not just "this should help." |

| Payback window | Set a dated base case and delayed case for when incremental gross profit covers the cost. |

| Downside risk | Test what happens if demand is slower, delivery slips, or collection is delayed. |

| Cashflow strain | Run a money-in, money-out view across your near-term cash cycle. |

Under accrual accounting, income is generally recognized when earned and expenses when incurred, even when cash has not moved. A project can improve reported profit and still weaken liquidity.

Step 4. Model a subcontractor hire through timing states#

A simple state model will tell you more than a generic ROI estimate. In this example, the expected client invoice is 10,000 and subcontractor cost is 4,000.

| Stage | Balance-sheet effect | What to watch |

|---|---|---|

| Commitment signed | There may be no immediate payable if services are not yet incurred | Do not book a full liability just because you plan to spend |

| Subcontractor performs and invoices | Accounts payable rises by 4,000; expense reduces earnings/equity | First real obligation that can pressure cash |

| You complete work and invoice client | Accounts receivable rises by 10,000; revenue increases earnings/equity | Receivable quality matters more than face value |

| You pay subcontractor | Cash falls by 4,000; accounts payable falls by 4,000 | Liquidity tightens even if the project is profitable on paper |

| Client pays | Cash rises by 10,000; accounts receivable falls by 10,000 | Timing mismatch closes only here |

If payment is delayed, receivables can stay recognized while cash stays tight. That is the core growth risk. Profitability can look fine while liquidity deteriorates.

Step 5. Run a pre-commit check before you lock in#

Before you lock in a growth commitment, run this short check:

- Contract terms clearly define deliverables, acceptance, and invoice trigger.

- Deposit or staged billing brings in cash before your largest outgoing payment.

- Receivables quality is validated: approved invoice, no dispute, known payment behavior, clear follow-up owner.

- A delayed-collection case still protects reserves and near-term obligations.

If any item fails, shrink scope, renegotiate terms, or wait. Growth built on weak collections is usually a liquidity risk, not durable expansion.

Mitigating Catastrophic Risk: Are You Safe From the Tax Man?#

Growth only helps if tax obligations do not quietly consume the same cash twice. You reduce tax risk when you book the obligation before the bill arrives and move matching cash out of day-to-day spending. This is a cash flow control, not a fear tactic. If future tax money sits in operating cash, your balance sheet can overstate what is truly available.

Step 1. Define the three tax lines correctly#

Use three separate labels, because they do different jobs.

| Line | Meaning | Tracking note |

|---|---|---|

| Tax provision | Estimate of tax on profit already earned when settlement is probable, even if timing or amount is still uncertain. | Keep Tax provision as a separate liability line. |

| Current tax payable | Unpaid current or prior-period tax amount recognized as a liability. | Keep Current tax payable as a separate liability line. |

| Restricted cash in the availability sense | Cash you do not treat as available for general operations. | Track the cash side as Tax reserve cash or a similar internal label unless your accountant confirms a formal classification under your reporting basis. |

In practice, keep Tax provision and Current tax payable separate on the liability side. Track the cash side as Tax reserve cash or a similar internal label unless your accountant confirms a formal classification under your reporting basis.

Step 2. Separate reserve cash from operating cash#

Move tax-reserve cash into a separate account your business does not use for routine spending. That account is an internal control choice, not a universal legal requirement.

For U.S. readers, this is an in-year control, not just year-end cleanup. The system is pay-as-you-go, and late or insufficient estimated payments can trigger penalties even if you later receive a refund. For 2026 planning, key IRS estimated-tax dates are April 15, June 15, September 15, and January 15 (following year).

Checkpoint: At close, confirm reserve cash is at least equal to the current provision. If not, log the shortfall and the transfer date to close it.

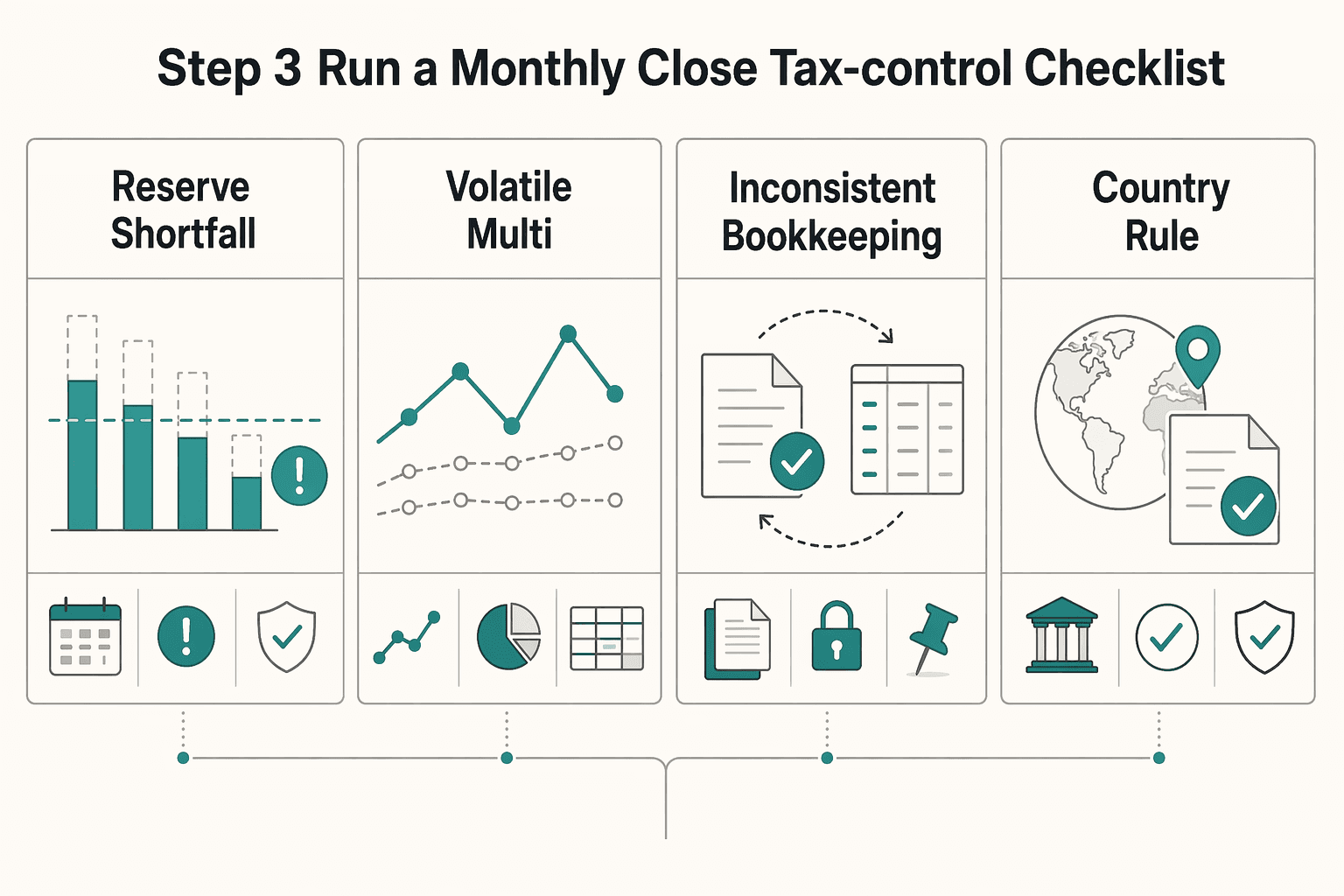

Step 3. Run a monthly close tax-control checklist#

Use the same sequence each month:

- Estimate taxable profit from current books.

- Update the tax provision for profit earned to date.

- Compare provision versus tax-reserve cash.

- Flag any gap, whether shortfall or unusual overfunding.

- Trigger the corrective transfer rule in your close window.

Many breakdowns start with record quality, not the concept itself. If records are incomplete or classifications are inconsistent, the provision is unreliable. Keep support for income, deductions, and credits organized. For U.S. filers, records must support reported items.

| Risk signal | What it means | Required action |

|---|---|---|

| Reserve shortfall | Protected tax cash is below the estimated obligation | Transfer the gap from operating cash, cut discretionary outflows, and recheck upcoming payment dates |

| Volatile multi-currency income | Tax estimate may be wrong if conversion is inconsistent | Recalculate using a consistent reporting-currency method; for U.S. returns, report amounts in U.S. dollars |

| Inconsistent bookkeeping | Provision may be wrong because profit inputs are wrong | Pause decisions based on current numbers; reconcile and rebuild support files |

| Country rule not yet verified | Filing cadence, threshold, or payment logic may be wrong | Threshold pending primary authority or advisor verification |

Step 4. Add a cross-border verification rule#

If you operate across countries or currencies, do not hardcode local thresholds, due dates, or safe-harbor assumptions from memory. Treat those rules as pending until they are checked against a current primary source or advisor record.

A practical close note is: Estimated payment rule: threshold pending primary authority or advisor verification. That keeps the balance sheet decision-useful. Tax reserve cash is not operating cash, and estimated and confirmed tax liabilities stay clearly separated.

Before locking your monthly tax provision, keep your cross-border residency evidence in one place with the Tax Residency Tracker.

Unlocking Your Life Goals: How to Prove Your Stability to Lenders and Visa Officers#

The same balance sheet that helps you operate also becomes your evidence file when someone else is judging your stability. For mortgage and many visa or residency reviews, a believable file usually shows four things clearly: liquidity, equity trend, liability burden, and tax compliance readiness.

Before You Start#

Pull records for matching periods before you package anything. A balance sheet shows assets, liabilities, and equity, but reviewers typically check whether those numbers reconcile with bank, tax, and income documents.

Step 1. Define the four signals reviewers are actually assessing#

Start with the signals reviewers usually assess.

Liquidity is your ability to meet obligations with available funds when needed. Reviewers care about funds you can actually use to cover obligations, not just one strong balance snapshot.

Equity trend is the direction of equity across multiple reporting dates. A consistent pattern across statements is usually more persuasive than a single strong snapshot.

Liability burden is debt relative to income. In mortgage review, this is commonly expressed as debt-to-income, monthly debt payments divided by gross monthly income, so liabilities should line up with income records.

Tax compliance readiness means you can produce official tax evidence when requested, such as return, account, or wage-income transcripts, or non-filing verification where applicable. Reviewers often check documentation completeness, not just headline numbers.

Step 2. Map your balance sheet to mortgage underwriting concerns#

A strong balance sheet does not guarantee approval. It helps when it answers underwriting concerns directly and stays consistent across the full document packet.

| Concern | Evidence | How to present it |

|---|---|---|

| Income reliability | Balance sheets across multiple dates, plus income records and tax returns | Use the same reporting windows across documents. If income varies, explain the pattern briefly instead of smoothing it away. |

| Liquid reserves | Cash and near-cash assets tied to recent bank statements | Match each cash line to statement balances. Keep reserved tax cash clearly separated from general operating cash. |

| Equity position | Equity totals across multiple statement dates | Show trend direction over time, not only the latest value. Explain major swings if they exist. |

| Liability burden | Liability lines plus monthly debt obligations used in DTI review | Separate business debt, personal debt, and tax obligations. If a liability was cleared after period-end, include proof. |

Consumer prep guidance expects a cross-document packet with income, tax, and bank records, and self-employed files may also require business-level records. If one document conflicts with another, reviewers can treat the file as less reliable.

Step 3. Build a parallel proof file for visa or residency review#

Use the same logic for immigration review: show financial self-sufficiency, source-of-funds clarity, and coverage for ongoing obligations. In U.S. immigrant-visa processing, required financial evidence, including Affidavit of Support where applicable, can affect case timing, and officers may still request additional documents beyond baseline guidance tools.

Structure your file in three blocks:

- Financial self-sufficiency: current balance sheet, liquid assets, and income records.

- Source-of-funds clarity: bank statements matched to tax records, contracts, payroll records, or sale documents as relevant.

- Ongoing-obligation coverage: recurring liabilities, tax obligations, and support commitments shown against available resources.

Do not guess jurisdiction thresholds. Use a note like Jurisdiction threshold pending local advisor verification. If a U.S. Affidavit of Support applies, treat it as an enforceable support obligation that may continue until citizenship or 40 qualifying quarters, usually 10 years.

Step 4. Run a pre-submission consistency check#

Before submission, make sure your file tells one clear story:

- Reconcile statement dates so balance sheet, bank records, and income records refer to the same period, or clearly bridge period-end changes.

- Align every cash line to account records, and label restricted or reserved cash separately.

- Confirm the same risk story appears across the balance sheet, income records, tax documents, and supporting notes.

When this check passes, your file reads as one coherent record instead of a stack of disconnected documents.

Related: How to Get a Certificate of Residence (Form 6166) from the IRS.

Conclusion: You Are the CEO of "Me, Inc."#

Use your balance sheet as an operating decision tool. It is a point-in-time statement of financial condition. Its job is to help you decide what to protect now, what to correct, and what to do next.

The core terms map directly to decisions. Assets show what you control, and current assets show what can convert to cash within 12 months. Liabilities show what you owe, especially obligations due in the next 12 months. Equity shows your residual position after liabilities. Liquidity answers the execution question: can you fund assets and meet financial obligations?

Apply those terms as checks, not just labels. For resilience, test whether liquid resources cover near-term obligations. For growth readiness, test whether a planned spend still lets you meet current liabilities. For documentation readiness, test whether each major line ties back to records so the file is reviewable and consistent.

Your baseline control is simple. The statement must balance under Assets = Liabilities + Equity, and cash lines should reconcile to account records for the same date. Good records help you monitor business progress and prepare financial statements. In U.S. borrowing, SBA Form 1919 requires requested information for eligibility determination, and SBA Form 413 is used to assess repayment ability and creditworthiness. In U.S. immigrant-visa processing, missing financial evidence can delay the case.

| Goal | Balance-sheet signal | Next action |

|---|---|---|

| Stay resilient | Liquid resources versus near-term obligations | Reduce discretionary outflows and assign cash to upcoming obligations |

| Invest in growth | Equity position and current-liability coverage after planned spend | Stage the spend and confirm near-term obligations remain covered |

| Pass external review | Cross-document consistency across balance sheet, bank, tax, and income records | Build one dated evidence pack and explain any period-end changes |

Run this monthly cadence: Review the statement, reconcile it to records, act on one decision. That is how you operate as the CEO of "Me, Inc.".

For a step-by-step walkthrough, see How to Read a Cash Flow Statement.

If you want to operationalize this balance-sheet discipline in day-to-day invoicing and payouts where supported, explore Merchant of Record for Freelancers.

Frequently Asked Questions

What is a balance sheet for a freelancer or small business owner?

A balance sheet is a point-in-time statement of assets, liabilities, and equity. Assets are what you control, liabilities are what you owe, and equity is what remains after liabilities are settled from assets. First confirm that Assets = Liabilities + Equity before using any ratio or decision.

How should you show multi-currency accounts on the statement?

Use one reporting currency for the full statement and apply it consistently. Keep each account's original-currency amount, then convert using a documented, date-stamped method that matches the applicable rules. If totals do not reconcile to bank records, tax forms, and your conversion log, rebuild the conversion trail before relying on the file.

What counts as liquid assets, and why do they matter most?

Start with cash and near-cash balances. Current assets may convert to cash within 12 months, but not every current asset belongs in your runway number. Compare current assets with current liabilities due within the next 12 months to assess near-term resilience.

Which ratios matter most for a business-of-one?

Use the Runway Ratio and Debt-to-Equity Ratio. Runway Ratio equals usable liquid assets divided by monthly burn rate, and Debt-to-Equity Ratio equals total liabilities divided by total equity. If runway falls or debt-to-equity rises because of short-term borrowing, pause new commitments and retest after collections and liabilities are updated.

How can this statement help with lenders, visas, or compliance review?

It helps when every major line can be tied to evidence. Prepare a dated balance sheet with matching bank records, tax records, income evidence, and a brief explanation of major period-end changes. For U.S. self-employed lending, reviewers generally look at a two-year history, and visa reviews can still require extra documents beyond baseline guidance.

How do you account for future tax liability on the balance sheet?

Treat unpaid current tax as a liability, often shown as Provision for Income Tax. Tie the provision to profit earned to date, tax already paid, and your filing jurisdiction's rules, then reconcile it to your payment records. In U.S. workflows, estimated tax generally applies when you expect to owe $1,000 or more, and the year is split into four payment periods.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- fdic.gov/capital-markets/liquidity-and-funds-managementtrusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/faqs/small-business-self-employed-other-busi...trusted

- sba.gov/business-guide/manage-your-business/manage-y...trusted

- sba.gov/business-guide/manage-your-business/pay-taxestrusted

- sec.gov/files/balancesheet-building-blocks.pdftrusted

- sec.gov/about/reports-publications/investorpubsbegfi...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

How to Get a Certificate of Residence (Form 6166) from the IRS

Start with purpose, not paperwork. Before anyone opens Form 8802, get clear on why the foreign payer or tax authority wants a U.S. residency certificate. That answer drives almost everything that follows: whether you should file at all, how the request should be framed, what tax period matters, and how much lead time you really need. If the reason stays vague, the rest of the process gets expensive fast.

The Best Bank Accounts for Freelancers in Germany

Pick the account that protects cashflow and keeps records clean when client behavior gets messy, not the one with the nicest app.