Quick Answer

Start with a three-lens check: cashflow impact, operating load, and strategic risk. To price software licensing well, compare perpetual, seat-based, usage-based, and hybrid models using expected-month and peak-month invoice scenarios, then lock renewal and downgrade terms in writing. Use concrete checkpoints from vendor terms, such as Salesforce’s 90-day renewal change window and whether cancellation still leaves a paid period before deactivation, so your quoted price reflects real contract behavior.

The real cost of software is not the headline price. The license and pricing model shape your cashflow, your day-to-day workload, and how hard it is to change course later. If you focus only on sticker price, you miss the tradeoffs that matter.

This guide gives you a practical way to evaluate a deal through three business lenses: CFO, COO, and CEO. Used together, they move the conversation from "What does it cost?" to "Can we afford it, run it, and trust it?"

The CFO Lens: Capital Expense (CAPEX) vs. Operating Expense (OPEX)#

Start with cashflow risk, not the sticker price. The right deal is the one your margins can absorb if users spike, usage jumps, or renewal terms lock you in at the wrong time.

| Vendor example | Topic | Grounded detail |

|---|---|---|

| Atlassian | Seat billing and cancellation | Monthly bill is based on the highest seat count reached during the billing cycle; added seats are prorated; removing seats mid-cycle does not reduce that period's bill; after cancellation, a paid subscription is deactivated 15 days after the end of the current subscription period |

| Salesforce | Auto-renew | Auto-renew contracts renew for the same term and services unless change requests are submitted before the 90-day deadline; the renewal window begins 90 days before the Contract End Date |

| Microsoft Enterprise Agreement | True-up | True-up is annual and reconciles added products, services, users, and devices at pre-agreed terms and pricing |

Step 1. Define your budget tolerance. In U.S. tax language, the IRS distinguishes capital expenditures from currently deductible business expenses. A perpetual license gives you the right to use the software indefinitely, so it behaves more like an upfront capital commitment.

A SaaS subscription can spread cost into monthly or annual billing, which may be easier on cash than a large upfront payment. In the IFRS cloud-arrangement agenda decision fact pattern, the right to receive SaaS access is treated as a service, not a software asset. The practical question is simple: can you absorb a large upfront payment, or do you need the cost to stay inside a predictable operating budget?

Step 2. Forecast your volume variability honestly. Seat-based, usage-based, and hybrid pricing each break in different ways. With seat-based billing, the common failure mode is user creep. Atlassian's monthly rule is a useful example. The bill is based on the highest seat count reached during the billing cycle, added seats are prorated, and removing seats mid-cycle does not reduce that period's bill.

With usage-based pricing, the risk is invoice volatility because charges rise with consumption. A hybrid model softens that with a fixed fee, included usage, and separate overage charges. Ask for one invoice example for an expected month and one for a peak month. A contract that explains the base price clearly but stays vague on overages, seat resets, or downgrade timing is a red flag.

| Model | Cashflow pattern | Levers to negotiate | What to verify now |

|---|---|---|---|

| Perpetual license | High upfront payment | Installments, support renewal notice, maintenance pricing basis | Upfront amount, upgrade rights, ongoing support cost |

| Seat-based subscription | Predictable base, but seat creep risk | Billing cadence, highest-seat versus end-of-period billing, downgrade timing | Does mid-cycle seat removal lower the invoice? If not, when does it reset? |

| Usage-based | Low entry cost, variable invoices | Usage alerts, spend cap, overage rate card | Meter definition, invoice timing, overage math |

| Hybrid fixed fee + overage | Stable base with variable tail | Included usage, overage terms, rollover or true-up, downgrade rights | Included units, reset date, exact overage trigger |

Step 3. Model renewal exposure before you negotiate price. Auto-renew is where manageable OPEX turns into trapped spend. Salesforce says auto-renew contracts renew for the same term and services unless change requests are submitted before the 90-day deadline. The renewal window begins 90 days before the Contract End Date.

If your contract includes a true-up, pin down the frequency and price in writing. Microsoft Enterprise Agreement true-up is annual and reconciles added products, services, users, and devices at pre-agreed terms and pricing. Do not rely on a sales email. Get the renewal window, overage rules, and downgrade language into the contract or order form.

Step 4. Choose terms that protect margin. If your user count and revenue are steady, an annual commitment can make sense. In Microsoft's Enterprise Agreement context, the company describes this structure as helping reduce initial costs and forecast annual software budget requirements. If demand is lumpy, monthly billing, hard usage alerts, and clear downgrade rights usually matter more than a small discount that traps you for a year.

Before you sign or renew, check your renewal date, the auto-renew notice window, seat or usage reset rules, and post-cancellation access. One concrete checkpoint: Atlassian says a paid subscription is deactivated 15 days after the end of the current subscription period after cancellation.

Related: The Best Payment Gateways for SaaS Businesses. Want a quick next step as you review software licensing costs? Try the free invoice generator.

The COO Lens: Calculating the True Total Cost of Ownership (TCO)#

After cashflow, look at operating load. A lower sticker price is a worse deal if the tool adds admin work, creates integration friction, or makes switching hard later.

Step 1. Map the work the software creates around the work#

Start from your real workflow, not the product demo. For most freelancers and small teams, that includes onboarding clients or teammates, setting permissions, connecting billing or project tools, reconciling invoices, handling renewals, and exporting data for reporting or handoff.

List every non-billable task the tool adds each month. Include onboarding workload, billing operations, and support touchpoints. If annual pricing offers a 10-20% discount, weigh that against the flexibility of monthly billing when you may need to pivot or cancel with 30 days' notice.

Before signing, ask for the plan terms and billing documents that show how charges, renewals, support access, and data export actually work. If features are clear but billing ownership, support path, or exit details are vague, treat that as TCO risk.

Step 2. Estimate the hidden operating drag#

TCO is an operating-cost check, not just the subscription line item. Hidden cost usually shows up where people, process, and technology meet, so pressure-test these three buckets:

- Admin overhead

Count the time you spend managing seats, handling access issues, chasing receipts, reviewing overages, and managing renewals. For rightsizing, login activity alone is weak evidence; feature-level usage is more useful when available.

- Integration burden

If the product does not connect cleanly to your accounting, PM, CRM, or delivery stack, you pay through manual work or extra tools. Integration complexity is a recurring hidden-cost driver, and bad assumptions often appear late.

- Switching risk

Validate the exit path now, not at cancellation. Confirm what data you can export, in what format, and whether migration support is included or separately charged.

| Cost area | Low sticker price, high ops drag | Higher sticker price, lower ops drag |

|---|---|---|

| Admin overhead | More manual seat cleanup, invoice chasing, and guesswork rightsizing | Clearer billing controls, stronger usage visibility, less monthly intervention |

| Integration burden | More CSV/manual handoffs and add-on tools | Cleaner integrations and fewer process workarounds |

| Switching risk | Export and migration obligations unclear until late | Export path and migration responsibilities clearer up front |

Step 3. Compare vendors on total operating load#

Compare options on what they cost to run, not just what they cost to buy. Use this short workflow before approval:

- Map your current process.

- Estimate monthly operational drag for each option.

- Flag lock-in risk in export and migration terms.

- Choose the vendor with the lower total operating load at your expected usage.

If usage visibility, billing terms, or exit obligations are not clear in writing, treat that as a real operating-cost risk.

You might also find this useful: How to Price a UI/UX Audit for a SaaS Company.

The CEO Lens: Mitigating Strategic Risk#

Before you approve a license, confirm three things in writing: you can exit with your data, the vendor can support continuity, and your compliance duties are covered if something goes wrong.

Step 1. Lock down your data exit before you sign#

Treat data ownership as contract language you can enforce, not a sales claim. Your agreement should state how data is exported, what support is included, whether access continues after termination, and who must do what during handover.

| Point | What to confirm | Article detail |

|---|---|---|

| Export format and method | The actual export method and format in the contract, order form, DPA, or product documentation | Where portability applies, the standard is a structured, commonly used and machine-readable form |

| Export support | Whether export is self-serve, support-assisted, or paid professional services | If support is required, define scope in writing before signature |

| Access window after termination | Whether read-only access continues after termination and for how long | Do not assume a default 30/60/90-day window if the contract is silent |

| Delete-or-return obligation | Whether the processor deletes or returns data at end of service | For personal data, your terms should give you control over that choice |

Check these four points:

- Export format and method

Confirm the actual export method and format in the contract, order form, DPA, or product documentation. Where portability applies, the standard is a "structured, commonly used and machine-readable form," but do not assume CSV, JSON, API export, or any specific format unless it is explicitly stated.

- Export support

Confirm whether export is self-serve, support-assisted, or paid professional services. If support is required, define scope in writing before signature.

- Access window after termination

Confirm whether read-only access continues after termination and for how long. Do not assume a default 30/60/90-day window if the contract is silent.

- Delete-or-return obligation

For personal data, your terms should give you control over whether the processor deletes or returns data at end of service.

A practical check is to request a sample export and the exact end-of-contract clause before you sign.

Step 2. Compare continuity signals you can actually verify#

Do not rely on "startup vs incumbent" labels. Compare vendors on continuity signals you can verify now.

| Signal | What you can verify now | Red flag |

|---|---|---|

| Roadmap clarity | Written roadmap themes, release cadence, or update notes | Direction is only verbal or vague |

| Support responsiveness | Presales/trial response times, named escalation path, support hours in contract | No escalation path or generic inbox only |

| Product change history | Public changelog/release notes and notice pattern for major changes | Breaking changes with little notice |

| Incident communication | Status page, prior incident notices, post-incident updates, contract notice clause | No clear notification process |

| Dependency risk | Disclosure of critical third parties, subprocessors, and component inventory (for example SBOM) where available | Vendor cannot explain key dependencies |

Before signature, run supplier due diligence and make sure cybersecurity requirements are in the contract, including participation expectations for incident planning, response, and recovery.

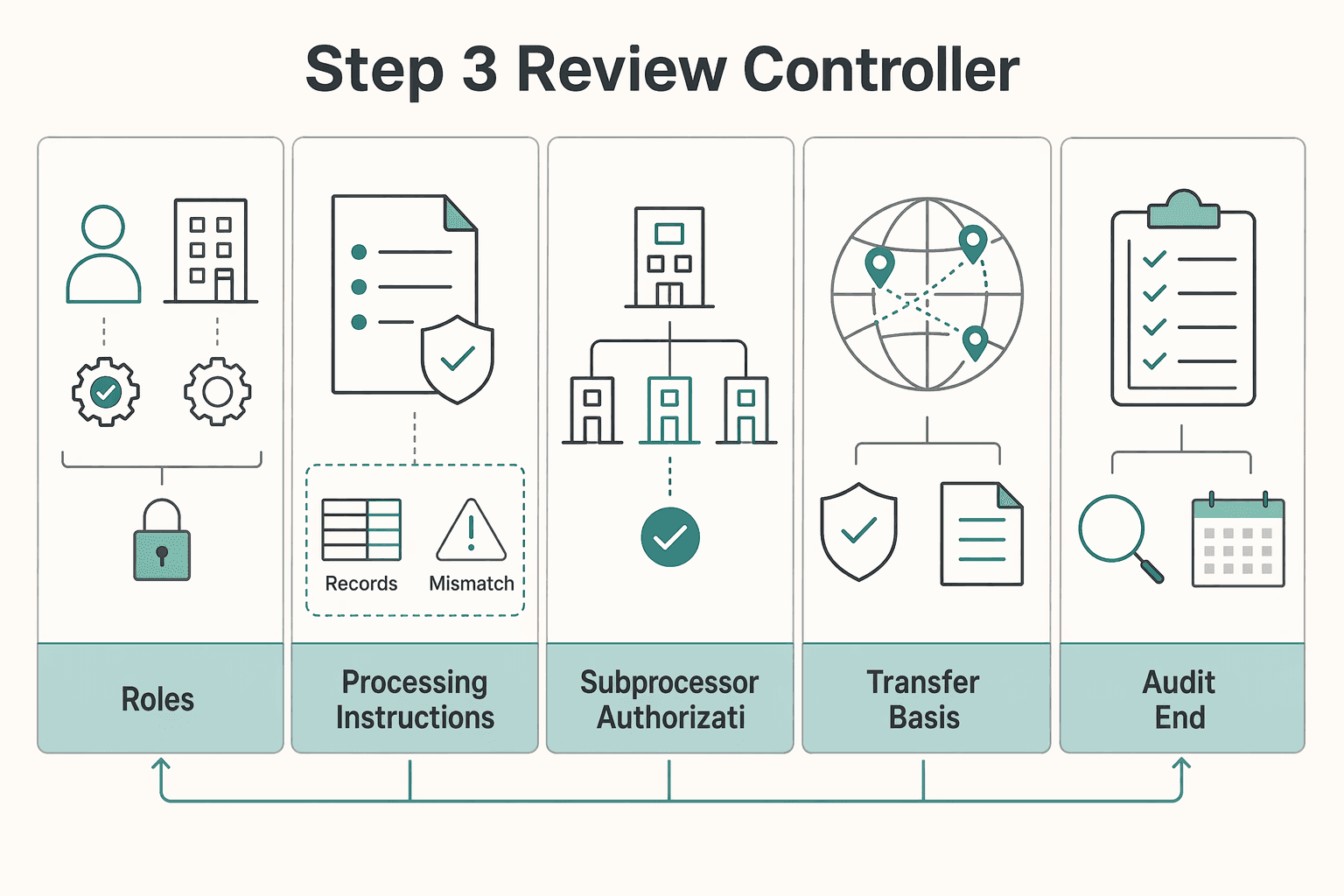

Step 3. Review controller, processor, and transfer terms like an operator#

If you decide why and how personal data is processed, you are the controller; if the vendor processes it for you, the vendor is the processor. That makes the DPA core deal paper.

| Term area | What to confirm | Grounded detail |

|---|---|---|

| Roles | Whether you are the controller and the vendor is the processor for the relevant personal data | If you decide why and how personal data is processed, you are the controller; if the vendor processes it for you, the vendor is the processor |

| Processing instructions | The DPA binds processing to your documented instructions, including international transfers | The DPA is described as core deal paper |

| Subprocessor authorization | Whether prior specific or general written authorization is required | With general written authorization, require notice of additions or replacements |

| Transfer basis | Whether the vendor relies on an adequacy decision or appropriate safeguards | If neither is available, transfer options narrow to limited derogations |

| Audit and end-of-contract terms | Whether audit or inspection terms and end-of-contract terms are included | Your DPA should include both |

| Incident notice | Whether incident-notice language works for your obligations | Where applicable, GDPR Article 33 sets a 72-hour outer limit after awareness |

Your DPA should bind processing to your documented instructions, including international transfers, and include audit/inspection terms plus end-of-contract terms. If subprocessors are allowed, require prior specific or general written authorization; with general authorization, require notice of additions or replacements.

For cross-border transfers, verify whether the vendor relies on an adequacy decision or appropriate safeguards. If neither is available, transfer options narrow to limited derogations. Recheck over time because adequacy status can change.

Also confirm incident-notice language is workable for your obligations. Where applicable, GDPR Article 33 sets a 72-hour outer limit after awareness.

Pre-sign risk gate Approve only if all three are yes:

- Data exit readiness: export method confirmed, handover support defined, post-termination access window stated, delete-or-return clause present.

- Business continuity confidence: roadmap evidence on file, escalation path tested, incident communication history reviewed, dependency disclosure acceptable, internal threshold pending contract/source-record verification.

- Compliance documentation completeness: DPA executed, subprocessor notice mechanism confirmed, transfer basis documented, audit and end-of-contract terms present, internal documentation threshold pending contract/source-record verification.

For a step-by-step walkthrough, see How to Handle Client-Paid Software Subscriptions in Your Bookkeeping.

Your Software Stack is Your Strategic Foundation#

Use the CFO/COO/CEO check as a pre-sign go/no-go gate. Approve only when budget impact, operating burden, and strategic/legal exposure are documented in signed terms, not vendor collateral.

CFO lens: Budget impact Treat price as a lifecycle cashflow decision, not a first-invoice decision. A lower upfront subscription can still create risk through usage charges, overages, or egress fees, and implementation costs may require separate accounting review depending on the arrangement. Go/no-go check: document month-one cash outflow, modeled worst-case variable monthly charge, renewal timing, and verify any escalation threshold from contract and finance source records before use.

COO lens: Operating burden (TCO) Assume Total Cost of Ownership includes ongoing work, not just license fees. Before approval, assign and document who owns setup, training, admin, meter tracking, and exit export in the order form, SOW, or master agreement. Go/no-go check: if ownership is unclear, pause approval until responsibilities are explicit.

CEO lens: Strategic and legal exposure If personal data is involved, require executed processor terms and confirm your own technical and organisational controls. Check portability and exit terms before signature, including export format and handoff conditions. Go/no-go check: collect the evidence pack up front: executed agreement, order form, DPA, security exhibit, and export terms. A SOC 2 report can support review, but it does not replace contract language.

| Red flag | Required action before approval |

|---|---|

| Spend, prepay, or implementation cost crosses threshold pending contract/source-record verification | Route to finance approver and document cashflow impact |

| Meter, overage, or egress terms are vague | Get written definitions and a capped-charge scenario |

| No DPA, weak export terms, or portability unclear | Do not approve until contract language is fixed |

Apply this on the next decision cycle: review active agreements, prioritize renewals with auto-renew risk, unclear usage charges, or weak exit terms, and run the same checklist across the full stack.

If you want a deeper dive, read How to Calculate Your Billable Rate as a Freelancer.

Frequently Asked Questions

How do you choose between a perpetual license and a subscription?

Start by separating licensing from pricing. A perpetual license can fit when you can absorb a one-time upfront payment and want indefinite use. If perpetual terms are not the best fit for your cashflow, compare subscription terms carefully before signing. In the agreement, confirm license scope, access rights, payment timing, renewal terms, and post-termination access.

What costs get missed most often?

The usual misses include add-ons, additional products, and usage-linked factors that can increase price (such as database or contact growth). In practice, TCO can end up far above the sticker price once direct and indirect costs are counted, sometimes in the 5-8x range. Check the agreement for included services, add-on lists, usage meters, overage treatment, and pricing thresholds.

Which pricing model is easiest to operate day to day?

There is no universally easiest model. Pricing models define how software usage is charged, so day-to-day fit depends on your usage patterns, billing predictability, and internal admin capacity. Before signing, test each option against likely usage changes and contract controls.

How do you handle renewal and auto-renew risk?

Treat renewal mechanics as a contract issue, not an admin detail. The risk is not just surprise spend; it can also include access disruption at a bad time. Confirm the renewal term, auto-renew language, notice clause, and what read-only access or data export support is available after termination.

What should you confirm before agreeing to enterprise-tier terms?

Ask for proof, not labels, and get key commitments in writing. If you are buying through California's SLP, confirm that listed contract pricing is a ceiling, solicit a minimum of three contractors, and award on lowest cost or best value. If only one reseller responds, document why in the file. For spend over $2 million, confirm whether prior approval through the SLP exemption request path is required.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- dgs.ca.gov/PD/Resources/Page-Content/Procurement-Divisi...trusted

- edpb.europa.eu/sme-data-protection-guide/international-data...trusted

- irs.gov/businesses/small-businesses-self-employed/ta...trusted

- irs.gov/publications/p551trusted

- legislation.gov.uk/eur/2016/679/article/28trusted

- ifrs.org/content/dam/ifrs/supporting-implementation/a...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Calculate a Freelance Rate You Can Actually Get Paid On

A workable rate is not the neat number a calculator produces. It is the number that still works after you account for real billable capacity, non-client time, scope drift, and the gap between sending an invoice and receiving cleared cash. Start with hourly math even if you do not plan to bill hourly, then turn that number into a quote with clear `payment terms`.

The Best Payment Gateways for SaaS Businesses

**Choose your gateway stack by cashflow risk first, then optimize for features and price.** If you want the best payment gateway for SaaS, start where money can stall, not where brand buzz is loudest. You are the CEO of a business-of-one, which means a payout delay or a payment hold is not an inconvenience. It is an operating event.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.