Quick Answer

To perform a business valuation for a small agency, use a risk-first system: build a clean evidence pack, choose methods that match your operating model, and triangulate SDE, EBITDA, and DCF. Then stress test assumptions and document your reconciliation logic. The most useful valuation is one you can defend and reuse quarterly to improve cash reliability, reduce payment risk, and guide better operating decisions.

Your Agency Is Not a Multiple It Is a System You Can Control#

Treat valuation for a small agency as a risk control system, not a headline multiple, and you are more likely to protect agency value before you ever start selling a business.

You can hit revenue goals and still lose value when cash flow breaks, collections drift, or payment risk sits unmanaged in your contracts.

Picture a small team that closes strong projects but waits on late invoices and absorbs disputed payments. Revenue looks fine, but risk rises, confidence drops, and the valuation story weakens.

You are the CEO of a small business. Valuation is one of the few dashboards that forces you to connect delivery, cash, and risk in one operating view.

Business valuation is the current value of your business based on forecasted profits or cash flows. As an operator, the practical rule is simple: value follows reliable cash movement, not just booked earnings.

| Control area | What goes wrong | What protects downside |

|---|---|---|

| Cash flow reliability | You book profit but collect late | Tight payment terms and escalation rules |

| Collections quality | Aging invoices pile up | Weekly collections cadence and owner visibility |

| Payment risk | Chargebacks, holds, and disputes surprise you | Clear scope, acceptance criteria, and release triggers |

Run the risk first loop#

- Choose the method that matches your business shape. Start with SDE when you run an owner-led agency. Add market comparables and precedent transactions as your operating model becomes more institutional. Use DCF when you can defend future cash flow assumptions.

- Pressure test assumptions before you trust the number. Run base, upside, and downside logic. Check whether your collection behavior supports your growth story.

- Translate valuation into operating controls. Convert weak points into contract terms, invoice timing rules, and payment workflows you can enforce every month.

Expected outcome: a defensible valuation, a short assumptions log, and a concrete control list you can review quarterly once your inputs are ready.

Use this as operational guidance for 2026 planning. Market conditions and program details vary by jurisdiction and provider setup, so adapt implementation to your local reality. If you need to tighten margins before this process, review How to Manage Project Profitability for Your Agency.

What You Need Before You Start This Valuation#

Prepare a complete evidence pack before you model anything, because a small-agency valuation only holds up when your earnings, risk, and compliance inputs line up.

This section turns the risk-first idea into a repeatable intake process. Build the pack first so you are not debating an EBITDA multiple or target agency value with weak documentation.

Before you start, create one folder for valuation inputs and one assumptions log to update each quarter.

| Prep component | What to collect | Why it matters for defensibility |

|---|---|---|

| Earnings baseline | P&L, owner pay detail, debt notes, asset notes | Supports SDE adjustments and an Asset-Based Valuation floor |

| Method rationale | One-page memo on your primary method (for example, Market Approach) | Shows why you chose the method, not just the result |

| Payment risk evidence | A/R aging report, delay patterns, payout friction notes | Connects accounting profit to real cash flow reliability |

| Tax and compliance records | W-8, W-9, 1099 workflow notes, VAT validation records | Reduces diligence gaps for lenders, buyers, or partners |

- Step 1 Gather earnings inputs. Pull your current P&L and document owner compensation clearly. SDE is a cash flow based earnings measure built for owner-operated businesses, so keep your owner pay adjustments explicit and repeatable. Add debt and asset notes so you can anchor downside with Asset-Based Valuation if cash flow quality looks unstable.

- Step 2 Write your method memo. In a short note, state your primary valuation method and explain why it fits your situation. Keep support files beside that memo. If you cannot explain your method in plain language, your valuation will not survive review during financing or when you start selling a business.

- Step 3 Collect payment risk evidence, not just accounting outputs. Export an A/R aging report that groups unpaid invoices by days outstanding, then mark recurring delay patterns. Add notes on account-opening compliance checks, including CIP, since these checks require collecting identifying information before an account is opened. Use your own records to show whether those checks affected payout timing in your workflow.

- Step 4 Assemble tax and cross-border compliance records. Use W-9 records to confirm TIN collection for information reporting. Keep W-8BEN records when requested by a withholding agent or payer. Track your 1099 process with current-year rules. IRS guidance includes $600 and $2,000 (for payments made after December 31, 2025), and threshold language can vary by form and period in 2026 planning. For EU cross-border activity, use VIES for VAT validation checks within EU scope.

Expected outcome: a practical, audit-ready prep pack you can reuse. It should make each valuation faster, clearer, and easier to defend.

Which Valuation Method Fits Your Agency Right Now?#

Choose methods that match how your agency actually operates, then triangulate them, because one headline multiple rarely gives a defensible business valuation.

With your prep pack in place, you can choose methods with fewer blind spots. Pick a primary lens, test it, and keep downside protection in view.

Use a practical method decision tree#

| Current agency profile | Primary method | Role in your decision |

|---|---|---|

| You run an owner-led agency and owner pay drives results | Seller's Discretionary Earnings (SDE) | Best starting point because SDE includes owner compensation |

| Your management structure and costs look more institutional | EBITDA view | Helps you compare performance without owner compensation in the earnings line |

| You can defend forward cash flow assumptions in writing | Discounted Cash Flow (DCF) under an Income-Based Valuation lens | Converts forecast quality into a present value view |

| You found truly similar firms with enough comparable data | Market Comparables | Use as a sense-check, not the final answer |

| Revenue quality looks unstable or forecasts carry high uncertainty | Asset-Based Valuation | Sets a conservative floor for downside framing |

Run method selection in five steps#

- Step 1 Start with SDE or EBITDA based on owner role. Use SDE when owner effort still anchors delivery and growth. Consider an EBITDA perspective when leadership and cost structure operate beyond one owner. Verification point: your choice clearly explains owner compensation treatment.

- Step 2 Add DCF only when assumptions are defensible. Use DCF when you can justify growth, risk, and timeline assumptions in plain language. If assumptions feel weak, do not force precision. Verification point: you can explain each key assumption without hand waving.

- Step 3 Cross-check with Market Comparables. Match on business model, client mix, and concentration before you trust any comparison. Example: two agencies report similar margin levels, but one depends on a single client, so you should not treat them as equivalent comparables. Verification point: you documented differences that affect agency value.

- Step 4 Set an Asset-Based floor. Use this floor to frame downside when future earnings look uncertain. Verification point: your floor value remains logically below your upside case.

- Step 5 Record one method memo before selling a business. Summarize why methods differ and which number drives decisions today. If you need cleaner forecast inputs first, tighten delivery economics in How to Manage Project Profitability for Your Agency. Verification point: another operator can read your memo and reproduce your method logic.

Step 1 Build a Clean Earnings Baseline You Can Defend#

Normalize owner compensation and one-off items before anything else, because your valuation only works when earnings reflect real operating performance.

| Task | What to do | Why it matters |

|---|---|---|

| Adjust owner pay | Reflect what it would cost to replace the role at market wages | Can materially change your cash flow view and your EBITDA baseline |

| Remove one-off gains and losses | Remove nonrecurring effects from normalized earnings | Helps you model sustainable performance |

| Separate predictable and volatile revenue | Tag each revenue stream by predictability and collection behavior | Shows which earnings are more reliable |

| Log payment-friction events | Track paused payouts, temporary holds, reserve events, and extra diligence before money moved | Links forecast assumptions to operating signals |

Once you've chosen your methods, the work becomes input quality. This step keeps valuation from turning into opinion when a buyer, lender, or advisor asks you to show your math.

Normalize earnings before you model#

- Step 1 Adjust owner pay to replacement economics. Owners often overpay or underpay themselves, so your baseline should reflect what it would cost to replace the role at market wages. This adjustment can materially change your cash flow view and your EBITDA baseline.

- Step 2 Remove one-off gains and losses. Normalized earnings remove nonrecurring effects so you can model sustainable performance. Example: you had a one-time legal cleanup expense tied to a legacy contract. Keep it documented, but do not let it define forward earnings.

Keep an adjustment log that another operator can follow. Verification point: they can read it and recalculate the same earnings baseline.

Tie revenue quality to payment reliability#

- Step 3 Separate predictable revenue from volatile revenue. Tag each revenue stream by predictability and collection behavior, then carry that into your valuation assumptions. This helps show which earnings are more reliable.

- Step 4 Log payment-friction events. Track paused payouts, temporary holds, reserve events, and cases where KYC or AML checks required extra diligence before money moved. Some providers can pause transfers until verification is completed, and timelines vary by flow and provider. Document what happened in your operation instead of guessing.

Verification point: each forecast assumption links to a specific operating signal, not a generic average.

Expected outcome for Step 1:

- A clean earnings baseline for business valuation.

- A defensible SDE and EBITDA bridge.

- A risk log that connects payment behavior to valuation confidence.

If margin noise still clouds your baseline, tighten delivery economics first with How to Manage Project Profitability for Your Agency.

How Do You Stress Test Assumptions Before You Trust the Number?#

Stress test your valuation with multiple DCF scenarios, reconcile outputs across methods, and document why each assumption deserves trust before you act on the number.

With a clean earnings baseline, you can now test whether the model holds up under pressure. This is where valuation shifts from a spreadsheet output into a decision framework you can defend.

Run the stress test in five steps#

| Step | Action | Key note |

|---|---|---|

| Build DCF cases | Create upside, base, and downside views with explicit growth, margin, and timing assumptions | Tie each assumption to observed collection behavior, client terms, and delivery capacity |

| Pressure test continuity claims | If projected performance differs from historical performance, write the reason and the failure condition | Reflect slower inflows when approval cycles slow cash conversion |

| Apply DLOM with a rationale | Use DLOM when your agency has weaker marketability than comparable transactions | List the specific transfer frictions that justify the adjustment |

| Reconcile, do not average | Compare DCF results against other valuation views before assigning weights | Write one reconciliation note that explains the final valuation conclusion |

| Lock a rerun checklist | Record what would force a model refresh | Keeps agency value tracking current instead of reactive |

- Step 1 Build DCF cases. Create scenario views, for example upside, base, and downside, with explicit growth, margin, and timing assumptions. Discounted Cash Flow (DCF) turns forecast cash flows into present value, so tie each assumption to observed collection behavior, client terms, and delivery capacity.

- Step 2 Pressure test continuity claims. If projected performance differs from historical performance, write the reason and the failure condition. Example: you win a larger retainer, but longer approval cycles slow cash conversion, so your base case should reflect slower inflows even with higher booked revenue.

- Step 3 Apply DLOM with a rationale. Use a Discount for Lack of Marketability (DLOM) when your agency has weaker marketability than comparable transactions. Do not drop in a standard percentage. List the specific transfer frictions that justify the adjustment.

- Step 4 Reconcile, do not average. Compare DCF results against other valuation views, including market-approach evidence from comparable transactions. If values spread widely, investigate the driver before assigning weights. Then write one reconciliation note that explains the final valuation conclusion.

- Step 5 Lock a rerun checklist. Record what would force a model refresh so agency value tracking stays current instead of reactive.

| Re-run trigger | Why it matters | Required action |

|---|---|---|

| Major client churn or concentration shift | Changes cash flow durability assumptions | Rebuild scenario probabilities and method weights |

| Rising payout failures or slower collections | Lowers confidence in forecast cash timing | Update DCF timing and downside case severity |

| Material operating or compliance changes that affect onboarding speed | Can change continuity and execution risk | Revise continuity assumptions and risk memo |

Verification point: another operator can read your memo and reproduce your assumptions, reconciliation logic, and final range before you start selling a business. If you want a quick next step, try the free invoice generator.

Step 3 Turn Valuation Into a Get Paid System#

Convert valuation assumptions into enforceable payment rules so cash collection is more predictable, auditable, and compliant.

This is where the model turns into operations. If your downside case came from delays, disputes, or holds, your contracts and payout controls should target those exact failure points.

| Valuation risk signal | Operating control to deploy | Verification point |

|---|---|---|

| Late collections and disputes | Stronger scope acceptance and payment timing terms | Fewer exceptions reach manual escalation |

| Payout uncertainty | Virtual Accounts plus controlled payout runs (for example, ACH batches) | You can trace each inflow and release decision |

| Onboarding friction risk | KYC, KYB, and AML gated release rules | Forecast timing reflects compliance review steps that vary by provider and jurisdiction |

| Tax documentation gaps | W-8BEN, W-9, and 1099-NEC workflows | Diligence packet is complete on request |

Execute the payment control rollout#

| Control | What to implement | Operational note |

|---|---|---|

| Commercial terms and MoR | Define acceptance, invoicing triggers, dispute windows, and late-payment actions; evaluate a Merchant of Record model where supported | The MoR is legally responsible for processing customer payments and carries core financial, legal, and compliance liability |

| Virtual Accounts and payout runs | Assign Virtual Accounts and release funds through controlled payout runs instead of ad hoc disbursements | Improves payment identification and reconciliation |

| KYC, KYB, and AML gates | Collect and submit required onboarding data before allowing payout release, and document additional review flags | Build this timing into your forecast so DCF cash timing reflects operating reality |

| Tax readiness | Keep current W-8BEN records, W-9 records, and 1099-NEC reporting support | Use tax readiness as quality of earnings evidence |

- Step 1 Default stronger commercial terms and use MoR where supported. Set contract defaults that define acceptance, invoicing triggers, dispute windows, and late-payment actions. Where your provider and jurisdiction support it, evaluate a Merchant of Record (MoR) model, since the MoR is legally responsible for processing customer payments and carries core financial, legal, and compliance liability for those transactions.

- Step 2 Redesign money movement for visibility. Assign Virtual Accounts to improve payment identification and reconciliation, then release funds through controlled payout runs instead of ad hoc disbursements. Example: if a payment is risk-flagged, you can pause payouts on the affected connected account; both automatic and manual payouts are blocked, and in-flight payouts can remain pending for up to 10 days.

- Step 3 Tie release timing to compliance gates. Collect and submit required KYC and KYB onboarding data before allowing payout release, and document when checks flag potential money-laundering or fraud risk for additional review. Build this timing into your forecast so your DCF cash timing reflects operating reality, not ideal timing.

- Step 4 Package tax readiness as quality of earnings evidence. Keep current W-8BEN records for foreign individuals establishing foreign status for U.S. withholding, W-9 records for TIN collection, and 1099-NEC reporting support for nonemployee compensation workflows.

Expected outcome: you can defend valuation outputs with operating proof, not just model logic.

What Common Valuation Mistakes Hurt Small Agencies and How Do You Recover?#

Fix valuation errors by comparing more than one method, documenting marketability risk, modeling compliance delays, and tightening continuity plans before you trust the number.

After you turn valuation into a get paid system, run this recovery pass so your decisions reflect how cash actually arrives. This protects agency value before lender diligence or a sale.

| Common mistake | Recovery move | What to verify |

|---|---|---|

| One headline number | Re-run with multiple valuation methods | One-page assumptions memo explains gaps |

| No marketability adjustment | Add a case-specific DLOM note | Buyer transfer friction appears in the conclusion |

| Compliance treated as back office | Map KYC, KYB, and tax-information timing into forecasts | Confidence drops where delays cluster |

| Continuity plan is stale | Update Buy-Sell Agreement and insurance review | Exit terms and coverage still match reality |

- Step 1 Re-run method triangulation. Run more than one valuation method, then force the outputs to challenge each other. If one method lands far outside the others, name the exact assumption that caused the gap. Write a one-page memo with method choice, key drivers, and rerun triggers because no single formula fits every valuation case.

- Step 2 Document DLOM like an operator. Add a plain-language Discount for Lack of Marketability (DLOM) note that explains transfer friction, buyer pool limits, and ownership constraints. Do not drop in a default percentage. Your rationale matters more than copying a generic adjustment.

- Step 3 Pull compliance into forecast confidence. Mark where KYC, KYB, or tax-information gaps slow releases and collections, then lower confidence for those periods. Timing varies by provider and jurisdiction. Some payment rails pause payouts when required tax details are missing, and in rare cases holds can continue for up to 21 days. Example: you onboard a cross-border client, beneficial ownership details arrive late, and payout timing slips while verification completes.

- Step 4 Tie value to continuity documents. Reconcile valuation outputs with your current Buy-Sell Agreement and confirm roles, triggers, and pricing mechanics still match your operating model. Buy-sell terms may or may not fix value, depending on case facts. For a practical framework, see How to Create a Buy-Sell Agreement for a Partnership. Then review Key Person Insurance sufficiency so continuity holds if a critical operator exits, while you still get legal and tax review on policy details.

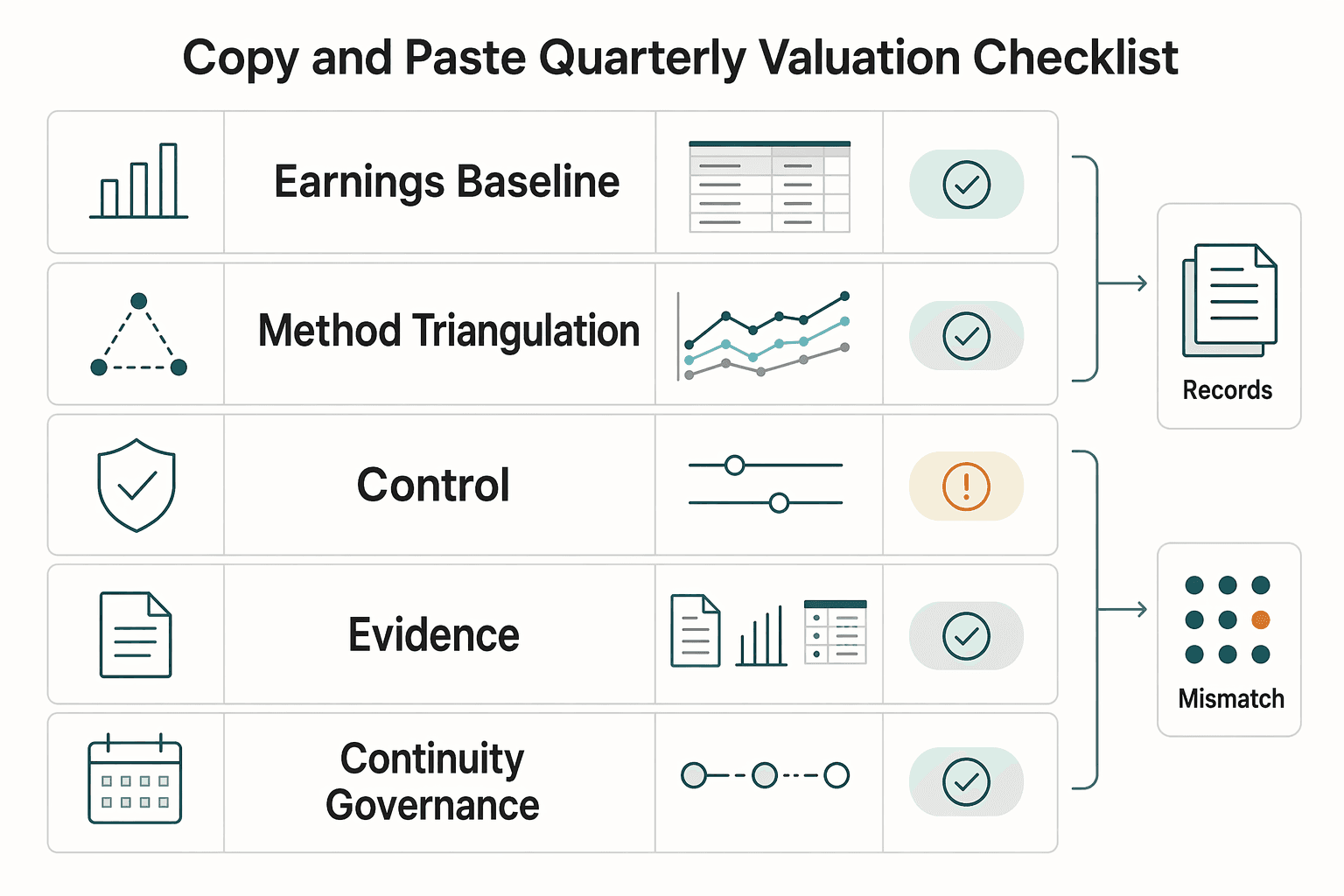

Copy and Paste Quarterly Valuation Checklist#

Run this five-step quarterly workflow to keep your small-agency valuation consistent, better documented, and tied to real cash flow behavior.

This checklist is the operational version of everything above. Keep it tight, run it on schedule, and your valuation stays connected to payment operations and decision-making before selling a business.

| Checklist block | What you update | Verification point |

|---|---|---|

| Earnings baseline | SDE and EBITDA adjustments | Clear change log for owner compensation normalization |

| Method triangulation | DCF plus Market Comparables review | One memo explains why valuation moved |

| Payment controls | Virtual Accounts and Payout Batches rules | Improved visibility and reconciliation review |

| Compliance and tax records | W-8BEN, W-9, 1099-NEC artifacts | Diligence folder is current and searchable |

| Continuity governance | Buy-Sell Agreement and Key Person Insurance | Ownership and transition risks match current operations |

- Step 1 Recalculate the earnings baseline. Update owner compensation adjustments first, then calculate Seller's Discretionary Earnings (SDE) and EBITDA. SDE reflects owner-operator cash flow earnings, while EBITDA isolates core operating profitability. Log each adjustment with a short reason and supporting file name. Expected outcome: your baseline supports a credible EBITDA multiple conversation.

- Step 2 Re-run valuation triangulation. Build a refreshed Discounted Cash Flow (DCF) model, then compare it to Market Comparables and your SDE and EBITDA results. DCF values projected future cash flows, while comparables pressure test your assumptions against similar firms. When numbers diverge, write the driver in plain language instead of averaging blindly. Verification point: one-page memo states what changed and what triggers a re-run.

- Step 3 Tighten payment risk controls. Review collection and payout friction, then tune Virtual Accounts routing and Payout Batches exception handling where your provider supports those controls. Virtual account structures improve visibility inside one core account, and batch workflows let you process many payouts in one run. Expected outcome: cleaner cash-timing assumptions in your valuation.

- Step 4 Verify compliance and tax artifacts. Confirm active records for W-9 (U.S. persons), W-8BEN (foreign beneficial owners), and 1099-NEC reporting data where nonemployee compensation applies. Verification point: your folder answers lender or buyer diligence quickly, and you pair forms with context-specific legal or tax review.

- Step 5 Align governance and continuity. Review your Buy-Sell Agreement against current ownership reality, then review Key Person Insurance policy details for critical operator risk. If you need a refresh on ownership transfer structure, use How to Create a Buy-Sell Agreement for a Partnership. Expected outcome: valuation outputs, continuity planning, and partner expectations stay aligned each quarter.

Run This Playbook Every Quarter to Increase Agency Value#

Run valuation as an operating rhythm, not just an exit project, so your planning stays grounded in current cash quality and risk.

You have the system. The only thing left is consistency. Treat valuation as a recurring control loop that keeps decisions sharp before growth bets, partner changes, or selling a business.

| Cadence | Core focus | Output |

|---|---|---|

| Quarterly review | Keep assumptions current and document risk drift early | Updated memo, action list, owner assignments |

| Annual deep refresh | Reframe strategy and major financing or exit choices | Full valuation pack for planning and diligence |

- Step 1 Refresh your valuation core. Recheck your current earnings and cash timing assumptions, then rerun your valuation model. Keep a short change log that explains what moved and why.

- Step 2 Convert findings into operating controls. Review where Merchant of Record (MoR) fits your workflow if you need one entity to carry key transaction financial, legal, and compliance responsibilities. Review where Virtual Accounts fit if you need cleaner money movement tracking without multiplying physical accounts. Apply each control only where provider and jurisdiction support it.

- Step 3 Pressure test execution risk before it compounds. Run one practical scenario each quarter: a client segment shifts, payout friction rises, and cash arrives later than forecast. Then decide the fix in writing, such as routing changes, revised payout gates, or contract updates, and assign an owner. Verification point: you can show exactly how each fix supports cash flow quality.

- Step 4 Lock the next cycle now. Schedule your next quarterly run today, then schedule an annual deep refresh for strategic planning. If you want a companion process for margin discipline, pair this with How to Manage Project Profitability for Your Agency. Repetition builds confidence in your numbers and supports better strategic planning. If you want to confirm what's supported for your specific country or program, Talk to Gruv.

Frequently Asked Questions

How do I value a small agency without relying on one multiple?

Triangulate instead of anchoring on one headline number. Run Seller's Discretionary Earnings (SDE), an EBITDA multiple view, and Discounted Cash Flow (DCF), then compare the outputs side by side. Keep a short assumptions memo that explains why the outputs differ and which risks drive the spread.

Should I use SDE, EBITDA, or DCF for an owner-led agency?

Start with SDE when owner involvement drives day-to-day economics, because SDE captures owner-operator cash flow reality. Use EBITDA to evaluate operating profitability on an earnings-before-interest, taxes, depreciation, and amortization basis. Use DCF when you can defend forward cash flow assumptions, timing, and risk. Expect different results, then reconcile them instead of forcing one answer.

Which assumptions matter most in an agency valuation model?

Prioritize assumptions that change cash flow quality, not just top-line growth. Stress test collection timing, receivables conversion, and marketability risk because value drops when earnings stay tied up in accounts receivable. If you apply a marketability adjustment, document the case facts that justify it.

What documents make a valuation defensible to a lender or buyer?

Build a file another operator can audit quickly. Include normalized earnings workpapers, method outputs, forecast assumptions, and a reconciliation note across SDE, EBITDA, and DCF. Keep the work objective and documented. Add support for key judgments, including your marketability rationale and payment reliability evidence, so a buyer can follow your logic during diligence.

How does payment reliability affect agency valuation in practice?

Payment reliability changes how much confidence a buyer gives your earnings. When cash gets stuck in receivables, those earnings carry less practical value and your forecast quality declines. Stronger collection performance generally supports stronger agency value because cash arrives on time and risk stays visible.

When should I apply a discount for lack of marketability?

Apply Discount for Lack of Marketability (DLOM) when case facts indicate limited marketability for a private-company interest. Treat DLOM as a case-specific judgment, not a fixed percentage you paste into every model. Document the facts, then show how that judgment affects your valuation conclusion.

How often should a small agency update its valuation system?

Use a regular cadence that fits how quickly your business changes; quarterly can be a practical operating rhythm if you track value for planning or a potential sale. Re-run sooner after major changes in client mix, owner role, or cash collection behavior. Quarterly updates are a control choice, not a universal legal requirement.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Health Insurance Comparison for Long-Stay Moves

Use focused time now to avoid expensive mistakes later. Start with a practical `digital nomad health insurance comparison`, then map your route in [Gruv's visa planner](/tools/visa-for-digital-nomads) so we anchor policy checks to your real plan before pricing pages pull you off course.

Manage Agency Project Profitability With Cashflow Checkpoints

Invoiced revenue can look healthy while cash is still unavailable. That gap is where a project that looks profitable can start to pressure routine operating costs such as payroll, rent, utilities, and equipment.

How to Create a Buy-Sell Agreement for a Partnership

**Treat your buy-sell agreement for partnership as core operating infrastructure, not paperwork for later.** Freelancers and consultants move fast on client delivery, but shared ownership risk keeps running in the background until one partner leaves, becomes disabled, goes bankrupt, or goes through a divorce.