Quick Answer

Use a rule-specific workflow to manually track physical presence days for FEIE: log every trip, verify dates with source records, and count only qualifying full foreign days inside a 12-month period. Test planned travel before booking, then confirm your final timeline matches Form 2555 Part III travel details before filing. If records conflict or day treatment is unclear, pause and get qualified tax advice.

Why Your Day-Count Spreadsheet Is a Ticking Time Bomb#

A spreadsheet is fine for capture, but it becomes risky as your final decision record when more than one day-count system applies. A common failure is not arithmetic. It is combining different legal clocks into one total and treating that total as if it means the same thing everywhere.

For FEIE physical presence, the IRS standard is specific: 330 full days during any 12 consecutive months. A full day is 24 consecutive hours, midnight to midnight, and time on or over international waters does not count as time in a foreign country. So a travel day that looks like "abroad" in your sheet may still fail FEIE counting.

| Framework | Counting logic | How the same trip day can be treated |

|---|---|---|

| FEIE physical presence test | Rolling 12-month window; 330 full foreign days required | Counts only if it is a full midnight-to-midnight day in a foreign country |

| U.S. substantial presence test | Calendar-year test with 31-day current-year and 183-day weighted 3-year thresholds | Presence in the U.S. at any time during the day generally counts, with limited transit exceptions |

| UK automatic UK test (SRT) | Resident if 183+ days are spent in the UK in the relevant tax year | The same day is evaluated inside the UK tax-year total, not your FEIE window |

| Schengen short-stay rule | Rolling 180-day lookback (90/180 rule) | Each new entry is judged against the prior 180 days, so older days dropping out changes your position |

That is why one "days abroad" column creates hidden risk. The same March trip can reduce FEIE-qualifying days, increase U.S. presence, affect a UK tax-year count, and change Schengen status at the same time.

Evidence quality matters just as much as counting logic. Your log or diary helps, but the IRS emphasizes that no single record stands on its own. Your entries are stronger when they reconcile to third-party records such as travel tickets and related documents.

Use this guardrail: reconcile every trip promptly, and flag overnight travel, transit, and same-day U.S. arrival days for manual review. If you have cross-border residence conflicts, ambiguous day classification, or the downside of a counting error would be high, escalate early to a CPA, enrolled agent, or attorney.

If you want a deeper dive, read 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Step 1: Establish a Bulletproof System of Record#

Start by separating evidence from calculation. Your spreadsheet can stay as an index, but each location or day entry should be treated as a claim. Each claim should link to supporting records, a consistent time standard, and a written day-definition rule.

Use this evidence hierarchy for every trip, then keep the checklist with it so the process stays consistent:

- Official records first: pull from the issuing source, and for U.S. government records confirm

.govandHTTPS. - Third-party records second: keep timestamped records that corroborate movement events.

- Personal log last: use it to explain gaps or context, not as your primary proof.

- Save original files before renaming or annotating.

- Record source, retrieval date, and what event or date window each file supports.

- Mark entries as provisional when support is missing or conflicting.

- Keep conflicts visible. Do not overwrite one record with another.

| Control point | What spreadsheet-only tracking misses | Where errors happen | What your process must include |

|---|---|---|---|

| Source authority | All rows look equally reliable once typed | Memory or convenience overrides stronger records | Required source tier per entry: official, third-party, personal |

| Timestamp quality | Dates copied without clock context | Cross-border travel and midnight boundaries can create mismatches | Stored original timestamps plus one chosen ledger timezone |

| Rule-specific day treatment | One date logic reused everywhere | Different travel-day categories treated inconsistently | A day-definition matrix for each rule you track |

| Corroboration | Entries are detached from proof | Single incomplete artifact treated as final | Linked evidence for each material travel event |

| Exception handling | Edge cases hidden in notes or colors | Unclear classification left unresolved | Explicit exception flag and review step before final count |

Before you count anything, create a day-definition matrix with the rule name and governing period, ledger timezone, how a day is counted for that rule, the tie-break document when records conflict, and any exception notes. Do not infer FEIE-specific day-count rules from this framework alone; confirm those definitions from the authority governing the rule you are applying.

Pick one authoritative time source for your ledger and keep it consistent across tools and records. The term "Authoritative Time Source" appears as checkpoint AU.L2-3.3.7 in CMMC Level 2 Assessment Guide Version 2.13; use it here as a consistency control, not as tax law. A short glossary also helps, so labels like local date, recorded timestamp, and counted day stay consistent.

Once that structure is in place, run the same operating routine every time:

- Capture: save records as travel happens.

- Reconcile: compare log entries against higher-tier records while details are fresh.

- Flag exceptions: isolate judgment calls, missing proof, and unresolved conflicts for review.

Talk to a pro when records conflict and you cannot reconcile them, when day classification is unclear, or when a small counting change could alter your filing or residency position.

We covered this in detail in The 'Physical Presence Test' Waiver: A Guide for US Expats in War Zones or Civil Unrest.

Step 2: Implement a Proactive 'What-If' Planning Model#

Use your ledger before you book, not just after you travel. Test the trip, then decide whether to proceed, adjust, or defer based on compliance risk.

Treat each trip as a scenario#

Enter the proposed itinerary with dates, jurisdictions, and timestamps. Then run one decision pass across all three clocks:

- FEIE eligibility: you need 330 full days in foreign countries during 12 consecutive months, and a full day is 24 consecutive hours, midnight to midnight. The 330 qualifying days do not have to be consecutive. Day count alone is not enough because your tax home must be in a foreign country.

- Visa/stay limits: for Schengen short stays, test 90 days in any 180-day period, with the 180-day lookback rechecked before each day of stay.

- Local residency exposure: day rules are not universal. The UK generally uses end-of-day (midnight) presence, with exceptions, and 183 days or more in a tax year means UK residence under the first automatic UK test. Canada residency can depend on broader residential ties, not only day totals.

| Plan option | Clocks pressured | Buffer status | Safest action |

|---|---|---|---|

| Original 3-week trip | FEIE 12-month window, Schengen 90/180 | Thin on both | Defer or shorten |

| Shortened 10-day trip | Schengen | Moderate | Proceed if your traveler status fits the rule set |

| Move trip outside current window | Local residency analysis | Stronger on FEIE and Schengen | Proceed after local review |

Treat every proposed trip as a scenario, not just a calendar event. That habit makes it easier to spot when a small date shift changes more than one rule at once.

Automate rolling-window checks#

Your process should recalculate FEIE and any 90/180 lookbacks for each proposed travel day, keep one ledger timezone, and flag borderline travel days for manual review. It should also flag travel time on or over international waters, which does not count as foreign-country time for FEIE.

| Process control | What the article says |

|---|---|

| Rolling windows | Recalculate FEIE and any 90/180 lookbacks for each proposed travel day |

| Ledger timezone | Keep one ledger timezone |

| Borderline travel days | Flag borderline travel days for manual review |

| International waters | Flag travel time on or over international waters; it does not count as foreign-country time for FEIE |

After each scenario change, verify that moving one flight date updates all affected lookback windows, not just the visible trip block. If outputs conflict, a rule is ambiguous, or your buffer is narrow, pause booking and get professional review before travel.

You might also find this useful: Qualifying for the FEIE with Physical Presence or Bona Fide Residence.

Before you lock in flights, run your draft itinerary through the Tax Residency Tracker so your day-count decisions stay consistent and easy to audit.

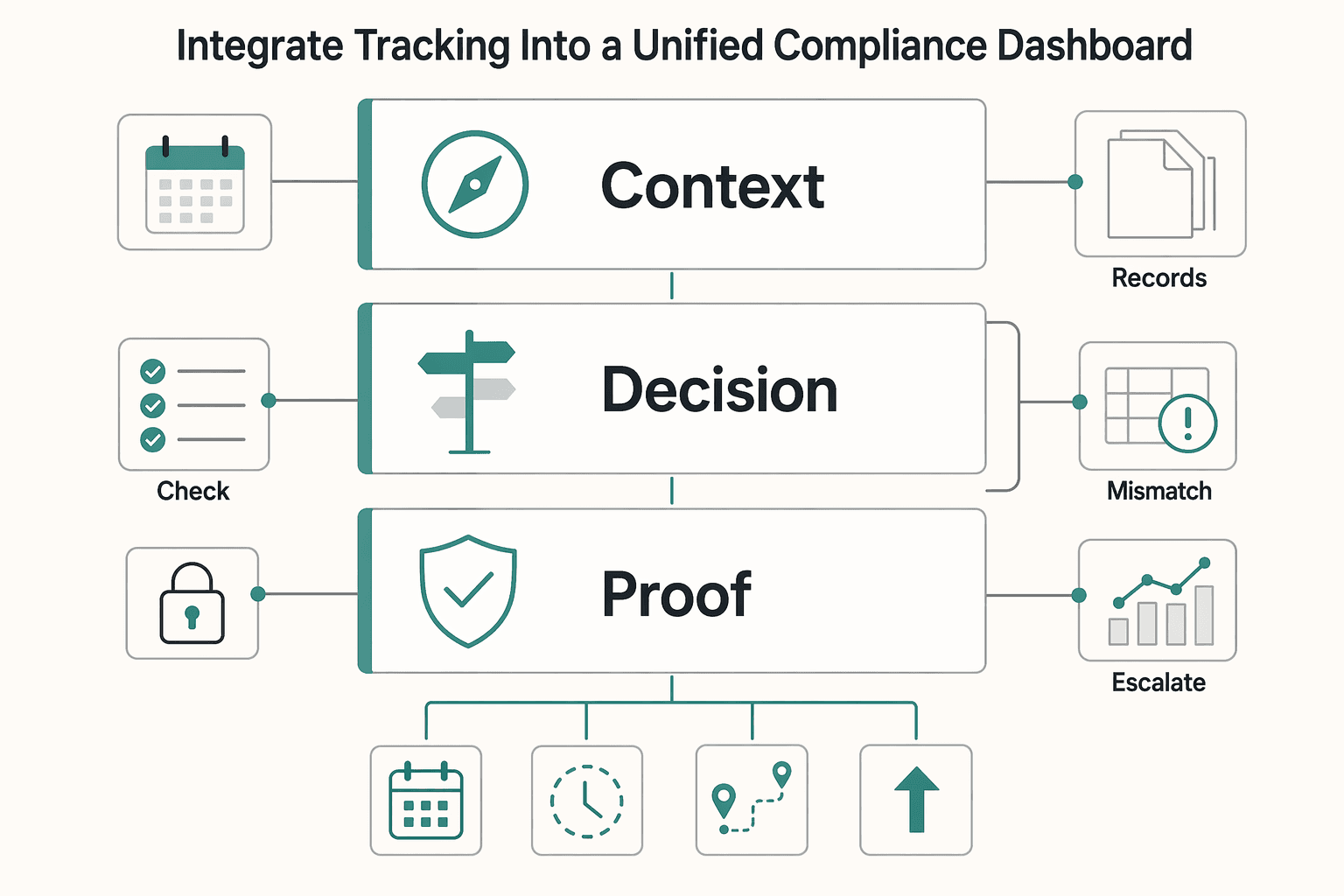

Step 3: Integrate Tracking into a Unified Compliance Dashboard#

Run this as a weekly operating rhythm, not a passive log. Your tracking system should end in a clear action for each planned trip: book, defer, reroute, or escalate.

Use one dashboard as your single source of truth for travel logs, scenario checks, and supporting records. Tie day-count status to decision impact with explicit placeholders, such as Tax-sensitive item: verify any current exclusion amount before using it and Cash-flow risk (internal estimate): review reserve changes with your advisor if status weakens.

Build from disciplined inputs#

Good dashboard output depends on disciplined inputs. For each trip segment, capture the travel events, supporting evidence, and jurisdiction tags you may need later:

| Input | What to capture | Decision value |

|---|---|---|

| Travel events | departure and arrival details plus segment notes | keeps timeline logic current when plans change |

| Evidence files | tickets, confirmations, travel-history exports, and other proof | supports reconciliation when records conflict |

| Jurisdiction tags | country or region and your internal review labels | keeps one segment usable across multiple rule checks |

Attach evidence to each segment, not just the overall trip. That makes it easier to review one disputed day without reopening the whole timeline.

Make document governance operational#

Document handling needs to be part of the process, not an afterthought. Use a consistent internal filename pattern and keep it the same across uploads. Reconcile regularly so the dashboard line, calendar record, and attached proof match before you approve new travel decisions.

| Document control | What the article says |

|---|---|

| Filename pattern | Use a consistent internal filename pattern and keep it the same across uploads |

| Regular reconciliation | Reconcile regularly so the dashboard line, calendar record, and attached proof match before you approve new travel decisions |

| Official sites | If you use U.S. government records, verify the site is an official .gov domain and uses HTTPS, and only share sensitive information on official, secure websites |

If you use U.S. government records, verify the site is an official .gov domain and uses HTTPS, and only share sensitive information on official, secure websites.

Keep views and outputs decision-first#

Your weekly dashboard should show your current working eligibility assumption (pending verification), weak points, missing proof, conflicting records, borderline cases, planned trips that may increase compliance or cash-flow risk, and one action label per scenario: book, defer, reroute, escalate.

| Dashboard item | What to show |

|---|---|

| Eligibility assumption | Current working eligibility assumption (pending verification) |

| Weak points and proof gaps | Weak points, missing proof, conflicting records, and borderline cases |

| Trip risk | Planned trips that may increase compliance or cash-flow risk |

| Action label | One action label per scenario: book, defer, reroute, escalate |

Strategy layer and escalation guardrail#

The point of the dashboard is to answer practical questions before you commit: Can this trip proceed without creating a documentation gap? Which booking changes risk most if status shifts? Where is the next ambiguity in tax treatment or residency exposure?

If the answer depends on a rule you cannot interpret confidently, stop and talk to a qualified professional.

For a step-by-step walkthrough, see How to Track Your Schengen Days: A Practical Guide.

From Anxiety to Autonomy: Your Path Forward#

The path forward is practical: keep one reliable record, test plans before you commit, and do one final review before filing. When anxiety spikes, avoidance can take over, so a repeatable routine matters. This workflow supports decision-making, but it is not a legal determination of FEIE eligibility.

Step 1: Maintain your record every week#

Keep one current record, not a memory rebuild. Outcome: each new movement is logged with dates and the source you used. Failure to avoid: treating the sheet itself as truth instead of a record you still need to verify.

Step 2: Test travel before you book it#

Check proposed dates against your current filing plan before you commit. Outcome: a clear decision to book, revise, or pause for verification. Failure to avoid: booking on assumptions and discovering later that one unverified date changes your plan.

Step 3: Review one filing dashboard before you file#

Before filing, bring your count, open questions, and supporting files into one view. Outcome: a packet you can explain without rebuilding the timeline under pressure. Failure to avoid: relying on a final number when underlying dates still conflict.

If records conflict, you cannot explain why a day was included or excluded, or eligibility is unclear, pause DIY tracking and involve a qualified tax professional before filing or booking additional travel.

The process is repeatable: run your weekly log review, apply the pre-booking check to each trip, and complete a pre-filing review before you rely on your count.

Related: Tax Home vs. Abode: A Critical Distinction for the FEIE.

As a final check before filing, use the FEIE Calculator as a planning aid to pressure-test assumptions and prepare focused questions for your tax professional.

Frequently Asked Questions

What is the best way to track physical presence for multiple countries at once?

Start by naming the rule owner for each count before you pick a tool, because one trip can be treated differently across tests. For the IRS physical presence test, your log must support 330 full days in foreign countries during a 12-month period and match what you report in Form 2555 Part III. A simple sheet can work only if you verify entries against source records before you rely on the count.

How do I count travel days for tax residency?

First identify the rule owner, then confirm that rule’s day definition, then log and verify before you rely on the result. For the IRS physical presence test, a counted day is 24 consecutive hours from midnight to midnight in a foreign country, and time on or over international waters does not count. Use your source records to confirm each included day, and for a deeper walkthrough see The Physical Presence Test: A Day-by-Day Guide for the FEIE.

How can I plan future travel without violating residency rules?

Start with the filing outcome you need to protect, then test your planned trip against that target before booking. For FEIE under the physical presence test, check whether your plan still leaves you with 330 full days in foreign countries within a 12-month period; those days do not need to be consecutive. If entry, exit, or transit dates are not verified, treat the plan as tentative and escalate before you commit.

Is a spreadsheet good enough to track physical presence days?

First decide whether your sheet is only a memory aid or a filing decision tool. A spreadsheet is usable for simple cases when every trip is backed by source documents and you can produce the Form 2555 Part III travel details on demand. It is not enough when your count is close, records conflict, or you cannot explain why a day was included or excluded.

What documents should I keep as proof of my physical location?

Start by collecting enough information to support your Form 2555 qualifying period and Part III travel schedule, then reconcile conflicts before filing. Keep records that let you verify arrival and departure dates and location for each trip. Escalate to a qualified tax professional if key arrival or departure dates conflict or remain incomplete, and remember you can attach an additional page or statement if you need more space for travel details.

How do I reconstruct my travel history if I haven't been tracking it?

Start by gathering available records and marking uncertain dates as unverified until reconciled. Rebuild your timeline around arrival and departure dates, fill gaps where possible, and flag unresolved dates for another check before you rely on the count. Escalate to a qualified tax professional if entry or exit records conflict, large gaps remain, or missing dates affect whether you reach 330 full days, because incomplete requested information can lead to disallowance.

What filing details matter most once my count is ready?

Start by confirming your final count supports the FEIE path you are actually claiming. For the physical presence test, attach Form 2555 to Form 1040 or 1040X and include the beginning and ending dates of your 12-month qualifying period plus the Part III travel schedule. If both spouses qualify, each spouse files a separate Form 2555, and Form 2350 can extend time to file but not time to pay taxes.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- dhs.gov/ai/use-case-inventory/cbptrusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AssessmentGuideL2v2...trusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AssessmentGuideL2.pdftrusted

- dot.ca.gov/-/media/dot-media/programs/design/documents/...trusted

- eur-lex.europa.eu/eli/reg/2016/399/oj/engtrusted

- home-affairs.ec.europa.eu/policies/schengen/border-crossing/short-stay...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/instructions/i2555trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

The Physical Presence Test: A Day-by-Day Guide for the FEIE

Start with one objective: qualify for the Foreign Earned Income Exclusion through the Physical Presence Test using facts you can prove, not assumptions you hope survive review. This is not a loophole hunt, and it is not just a math exercise. The goal is a filing position that is clear, repeatable, and defensible.

Tax Home vs. Abode: A Critical Distinction for the FEIE

**If you earn across borders, FEIE only works when your facts support a [foreign tax home](https://www.irs.gov/individuals/international-taxpayers/foreign-earned-income-exclusion-tax-home-in-foreign-country) and no U.S. abode for the period you claim on Form 2555.**