Quick Answer

Yes - use a fixed sequence: residency tracking first, foreign-account reporting second, and payment-route tuning last. Keep a weekly country log for tests such as the U.S. Substantial Presence Test, run FBAR as its own annual cycle, and set contract boundaries so you do not act as a dependent agent for a client. Once those controls are in place, require each invoice to reconcile through payment confirmation and final ledger entry before you optimize FX timing, spreads, or provider choice.

The hard part of managing money across currencies is not shaving a few basis points off a wire. There is endless advice about the cheapest way to move money, with fintech comparisons down to the decimal. That focus can distract from the real risk. You wake up at 3 AM wondering whether you missed a compliance rule you did not even know applied, and whether that mistake could put the business at risk.

This is not a guide for a backpacking digital nomad. It is for the CEO of a business of one. Your financial life is operational, not casual. You are directing cash flow, controlling risk, and building a global business where the cost of getting it wrong is much higher than a bad exchange rate.

While other people argue about FX spreads, you are thinking about accidental tax residency, FBAR exposure, or permanent-establishment risk that could damage an important client relationship. That is the real stress of working across borders: financial and legal systems that were not built for the way you work.

The goal is simple: give you a practical way to stay in control. We will move past fee comparisons and build a financial setup that holds up under scrutiny. But before you improve tools and pricing, deal with the risks that can break the whole thing.

The Three Silent Risks That Can Wreck Your Career#

If you want control, start with the three risks that can do the most damage: tax residency, foreign-account reporting, and permanent-establishment exposure. You can have clean invoicing, reasonable FX, and healthy cash flow and still create a serious problem if one of these is ignored.

Step 1. Track tax residency like an operating metric#

Do not leave this to a year-end estimate. A single 183-day rule is not enough across jurisdictions because day counts, ties, and intent can all matter. Track where you slept, where you worked, what ties you created, and what evidence supports each point.

| Jurisdiction | Signals to watch | Records to keep | Weekly action |

|---|---|---|---|

| U.S. | Substantial Presence Test: at least 31 days in the current year and 183 days across a weighted 3-year count | Passport stamps, flight records, lodging receipts, calendar with overnight location | Recalculate current-year days and the weighted 3-year total, including 1/3 and 1/6 prior-year weighting |

| UK | Day count and sufficient ties interact; the number of UK days affects how many ties matter | Lease or hotel records, family location, UK workdays, accommodation access | Log UK days and any tie changes, including accommodation, family presence, or regular work there |

| Canada | Residency is fact-based and considers residential ties, not days alone | Home access, spouse or dependants location, provincial connections, bank and utility records | Note new significant residential ties and flag them before a long stay becomes a settled pattern |

| Australia | The 183-day test also considers usual place of abode and intention | Travel history, lease, visa details, evidence of home outside Australia | Review days plus whether your living pattern indicates Australia became your usual base |

Escalate early. If a country is becoming a repeat work location or your local ties are increasing, speak with a cross-border tax professional before you cross a threshold you have verified for that jurisdiction. Add the current thresholds for the jurisdictions you use most to your own tracking sheet.

Step 2. Run foreign-account reporting as an annual compliance cycle#

If you are a U.S. person, treat FBAR as a separate annual filing cycle. FinCEN Form 114 is filed electronically through the BSA E-Filing system, and it is not filed with your federal tax return.

Start an account inventory in January and keep it current. Include bank accounts, brokerage accounts, mutual funds, and other foreign accounts that may be reportable. Do not assume a fintech account is excluded, and do not assume every platform account is always reportable. Document each inclusion decision.

For each account, track the institution, account number, country, owner, business or personal status, and highest annual balance. The trigger is aggregate value across foreign financial accounts exceeding $10,000 at any time in the calendar year, regardless of whether the accounts produced taxable income.

Treat deadlines as operational. FBAR is due April 15, with an automatic extension to October 15. Add a March checkpoint to confirm highest balances and inclusion decisions, then retain records for generally five years from the FBAR due date. Add filing-trigger notes only after you verify definitions and exceptions that apply to your account setup. Do the same for penalty detail.

Step 3. Put permanent-establishment controls into your contracts and working habits#

PE risk is managed in two places: in the contract and in daily behavior. Treaty analysis commonly looks at fixed-place-of-business exposure and whether a dependent agent habitually concludes contracts.

In contracts, keep your status clearly independent. Avoid terms that give you authority to conclude relevant contracts on the client's behalf. Also avoid wording that presents you as the client's local representative.

In practice, watch for patterns that blur that independence. Keep workspace control on your side, and review high-concentration or long on-site arrangements when authority and local presence start to combine. Reuse these minimum controls for each client:

- No authority to habitually conclude relevant contracts for the client

- No regular use of workspace that appears to be a fixed place for the client's business through you

- Independent-contractor terms in the agreement, matched by daily working practice

- Early local tax review for long on-site patterns or country-specific delivery models

- Evidence pack: signed contract, scope, invoices, travel log, and proof your workspace and business costs are your own

Once those three risk areas are under control, the rest of your financial setup gets much easier to manage. If you want a deeper dive, read Separating Business and Personal Finances: An Important Step for LLCs.

Are You Building a System or Just Collecting Apps?#

Build a system, not a pile of apps. If you want to manage finances in multiple currencies without avoidable delays, treat invoicing, payment, and reconciliation as one connected record chain.

Fragmented setups often break at the handoffs. Invoice details drift from bank instructions, payment fields get retyped, and your books lose the fee or FX context you need later. That is how delayed cash flow, missing records, and needless payment friction show up.

Step 1. Map the invoice-to-cash workflow#

Start by defining the data that must survive each handoff. Then make sure you can trace one invoice ID from issue to ledger. If one invoice number cannot be traced end to end, you are still collecting apps.

| Stage | Data that must carry forward |

|---|---|

| Invoice | Client legal name, invoice number, invoice date, due date, currency, amount, tax treatment, payment reference |

| Payment | Payer name, receiving account, settlement status, amount received, currency received, fees, conversion details |

| Reconciliation | Same invoice ID linked to payment confirmation and final ledger entry |

Then compare the setup you actually run:

| Setup | Control | Error risk | Payment speed | Reconciliation effort | Audit readiness |

|---|---|---|---|---|---|

| Email invoice + manual bank details + spreadsheet | Low | High (retyping errors) | Can be slowed by corrections | Heavy manual matching | Weak unless you maintain a separate evidence pack |

| Separate invoicing app + separate payment app + manual exports | Medium | Medium to high at handoff points | Better, but exceptions are easy to miss | Recurring manual work | Mixed, depends on export discipline |

| Integrated invoice/payment/reconciliation flow | Higher | Lower (fewer re-entered fields) | Clearer status visibility with fewer avoidable stalls | Lighter, fewer unmatched items | Stronger, linked records by default |

Step 2. Tighten invoice checkpoints before send#

Your invoice is the first operational record in the chain, so check it before money moves. Keep anything unverified clearly marked as pending.

| Checkpoint | What to verify |

|---|---|

| Invoice fields | Confirm invoice number, currency, amount, and payment reference format before send |

| Beneficiary and payment details | Validate bank name or address, account number, IBAN, and Swift BIC |

| Source record | Keep one verified source record for payer legal details so fields are not repeatedly retyped across tools |

Do not pull legal names or payment details from chat messages. Take them from contract or onboarding records, or from another verified source, and keep that record with the invoice file.

Step 3. Choose payment controls that survive exceptions#

A multi-currency account can receive, hold, and send funds in different currencies. What matters is whether the controls still work when something goes wrong. Focus on five points:

| Control | What to confirm |

|---|---|

| Payout control | Where funds settle and who controls release or movement |

| Settlement visibility | Clear states for paid, pending, failed, and partial |

| Evidence capture | Invoice, payment confirmation, contract, delivery proof, and client approval stored together |

| Accounting sync | Fees, FX amounts, and payout dates preserved in your books |

| Exception handling | Defined steps for failed transfers, underpayments, duplicates, and short settlements |

Data quality matters more than most people expect. Up to 50 percent of incomplete or delayed payments are tied to basic data-entry mistakes, including bank name or address, account number, IBAN, and Swift BIC errors. Cost control also requires full-price visibility. Banks can charge up to 4% on international transfers, and some providers price through FX spread instead of an explicit fee.

Before you scale a route, run a low-risk end-to-end test. Confirm that the invoice ID, payer, amount, currency, fees, and payout date match across all records. Once the record chain works, you can think about currency strategy without adding more operational risk. You might also find this useful: How to Connect Wise to QuickBooks for Automatic Reconciliation.

Optimizing Your Currency Strategy#

Once your invoice-to-cash chain is traceable, protect timing next. Managing money across currencies reliably means choosing tools and conversion rules that keep obligations funded even when settlement times, holds, or FX pricing move against you.

Step 1. Pick your primary tool by payout reliability first#

Do not choose based on headline FX alone. Start with when funds are actually available, whether total pricing is clear before you send, and whether the records land cleanly in accounting.

| Option | Settlement speed reality | Spread and fee transparency | Accounting integration | Hold or freeze risk signals | Support check |

|---|---|---|---|---|---|

| Fintech multi-currency account with direct accounting sync (for example, Wise) | On SWIFT gpi routes, timing is corridor-dependent. BIS reports SWIFT gpi routes from under 5 minutes on the fastest paths to more than 2 days, with an 8h36m average and 1h38m median. | Capture quoted rate, explicit fee, and expected recipient amount before you approve. | Wise supports direct setup with Xero and QuickBooks. | In the UK, payment/e-money balances may be safeguarded rather than deposit-insured; FCA states these funds are not directly protected by FSCS. | Test escalation on a low-risk case before routing critical payments. |

| Payment wallet or processor (for example, PayPal) | Funding can appear fast, but availability can still be delayed by holds; PayPal discloses funds are usually held for up to 21 days in some cases. | Review gross amount, processor fee, conversion fee or spread, and withdrawal fee separately. | PayPal Connector syncs the majority of PayPal transaction data into QuickBooks Online. | Reserves and holds can apply when refund or chargeback exposure is higher; a reserve is a temporary hold on part of your funds. | Confirm hold, beneficiary, and payout issues can be resolved in writing, not chat only. |

| Bank account for local rails and outbound transfers | In the U.S., instant rails can be near real time on supported networks (FedNow requires received funds to be available within seconds), while ACH can settle on a future business day. | Check whether correspondent or bank-side deductions can apply on cross-border routes. | Validate export quality and field mapping before month-end dependence. | Protection depends on institution and jurisdiction, and differs from payment-firm safeguarding. | Get written cut-off times and escalation contacts for failed or returned transfers. |

| FX broker for planned conversions | Execution is trade-specific, not universal. It can be useful for scheduled conversions rather than your whole receivables flow. | Require all-in pricing and trade confirmation before funding. | Confirm trade confirmations and settlement refs can be retained with accounting records. | Verify registration before deposit; in the U.S., use NFA BASIC and confirm CFTC registration where relevant. | Confirm a named contact and same-day post-trade confirmation process. |

Run a practical test. Keep the quote, transfer confirmation, recipient confirmation, and accounting entry together. If the fee, FX rate, payout date, or invoice ID does not reconcile cleanly, the route is not ready for production.

Step 2. Build a natural hedge you will actually follow#

Natural hedging works best as an operating control, not a prediction strategy. Match revenue and costs by currency where you can so you are not forced to convert at the wrong moment. Do not assume this alone removes FX risk.

| Decision | Use when |

|---|---|

| Hold | You have a known same-currency liability due within your verified policy window and base-currency runway is already covered |

| Convert | That currency has no near-term use or home-currency obligations fall inside your verified policy window |

| Split | Part covers same-currency costs and the remainder should move to operating currency to protect payroll, tax, or owner-draw timing |

Use a repeatable monthly routine so the decision does not depend on mood or headlines:

- Map the last 90 days of income by currency, client, and expected payment date.

- Match recurring costs by currency where operationally sensible (contractors, software, rent, tax set-asides, travel in that currency).

- Define conversion triggers tied to upcoming liabilities and runway, using your own verified policy limits.

- Record who can approve conversions and where approval is logged.

Then apply that same rule each cycle so holding or converting stays tied to real obligations, not rate guesses. Keep a short conversion log with the date, pair, amount, quoted rate, provider, hold or convert or split decision, reason, and approver. That makes decisions easier to defend when cash flow gets tight.

Step 3. Match the route to the payment scenario#

For routine client receipts, use the route with the fewest handoffs and the cleanest reconciliation. A direct accounting connection can be worth more than a slightly better headline FX quote if it saves you from manual cleanup.

For contractor payouts, verify the recipient-side outcome before release, not just your send amount. In U.S. remittance contexts where required, disclosures must reflect exchange rate, fees, and taxes in the amount received. Use that same discipline even when the rule does not apply: capture the quote, verify beneficiary data, and confirm the credited amount.

For large one-off transfers, treat each one as a controlled exception. Compare at least two quotes in the same time window, request total fees plus expected recipient amount in writing, and complete counterparty checks before prefunding. If you use a broker, run registration checks. If you use a fintech or payment firm, remember safeguarding is not the same as deposit insurance. In the UK, FCA safeguarding-rule changes take effect on 7 May 2026.

If a provider cannot clearly explain delayed, partial, or compliance-reviewed transfers, do not send critical cash through it. Strong currency operations are about dependable arrival, not just the lowest spread. Related: Should Your Freelance Business Accept Credit Cards?.

Before you lock your currency workflow, map your travel and work footprint in one place with the Tax Residency Tracker. That helps you make FX decisions without creating compliance surprises.

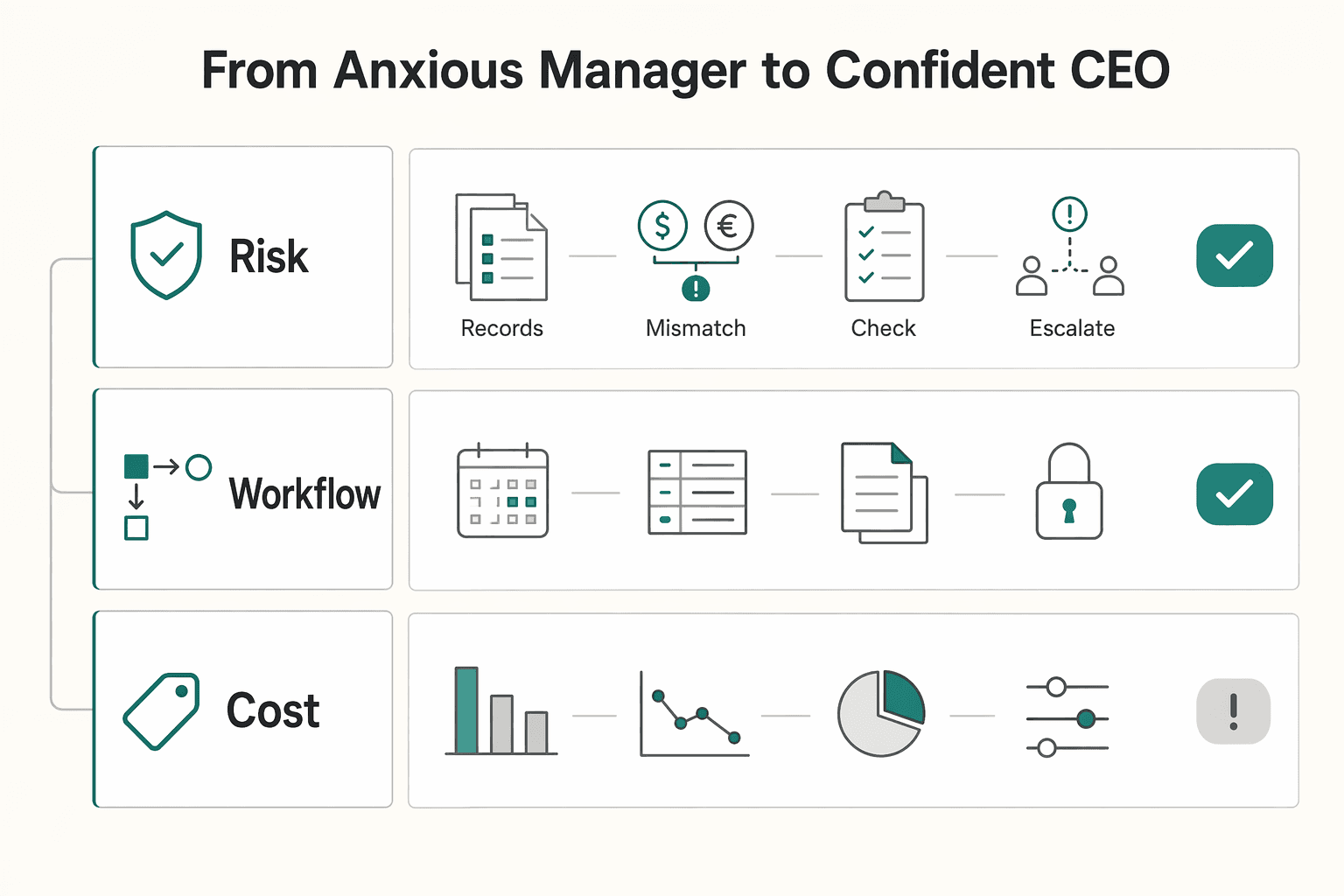

From Anxious Manager to Confident CEO#

Confidence comes from repeatable rules, not constant monitoring. To handle multiple currencies with less friction, use this order every time: risk first, workflow second, cost third.

| Focus | Reactive manager | Confident CEO |

|---|---|---|

| Risk | Decision: waits for issues to surface. Signal watched: urgent client requests and month-end surprises. Default action: scramble after the fact. | Decision: define controls before work starts. Signals watched: open exceptions and missing documentation. Default action: escalate early and document. |

| Workflow | Decision: add tools ad hoc. Signal watched: reconciliation breaks at month end. Default action: manual cleanup. | Decision: keep one operating record across invoices, balances, conversions, transfers, and statements. Signal watched: reference and statement gaps. Default action: fix the record before volume grows. |

| Cost | Decision: optimize conversion cost first. Signal watched: quoted FX and fees only. Default action: switch routes frequently. | Decision: optimize cost only after risk checks and clean reconciliation are stable. Signal watched: clean close process plus fee trends. Default action: tune routes without breaking controls. |

Step 1. Set defaults before each deal#

Define your standard billing and payment workflow, and document when exceptions are allowed. Before you send anything, confirm that invoice details, receiving details, and internal references are complete and match your operating record.

Step 2. Keep records current#

Keep records current even when nothing feels urgent. Maintain an account register with owner, account identifier, open/close date, and stored statements where applicable. Track unusual requests and boundary exceptions in one place, then escalate before work proceeds.

Step 3. Run a fixed review cadence#

Use a fixed cadence so the work happens before it feels urgent:

- Weekly: review unpaid invoices by currency, verify transfer references posted correctly, and file new statements or confirmations.

- Monthly: reconcile balances by currency, review account-register completeness, and review exceptions that need approval.

The result is practical, not performative: documented rules, clean records, and review habits that keep finance admin from pulling you away from the work that matters.

For a step-by-step walkthrough, see How to Use QuickBooks Online to Manage Multiple Currencies as a Freelancer.

If you want one system for invoicing, collections, conversion, and payouts with traceable records, review Gruv for freelancers.

Frequently Asked Questions

Do I need a separate bank account in every country I work with?

Usually no. Start with a multi-currency account so you can receive, hold, convert, and send funds from one platform instead of opening separate accounts in each country. Before you commit, verify that you get local account details in the countries you invoice and a single dashboard for balances and transfers. If either is missing, you may end up doing more manual reconciliation and admin work later.

When should I convert instead of holding the currency?

Start with fees and near-term obligations, not rate guesses. Foreign-currency spending can include extra transaction fees, so check total cost before you convert. Keep the quote, fee breakdown, and transfer confirmation together so decisions are easier to reconcile later.

Why do international payments still get delayed after I hit send?

Payment timing can vary by route, so "sent" and "available to the recipient" are not always the same event. Where possible, route through local rails like ACH or SEPA instead of relying on a SWIFT path, which can reduce reliance on costly international routes. Keep your send confirmation and the recipient's receipt together in case the payment needs follow-up.

Which is better for me: a multi-currency account or a traditional bank account?

Use a multi-currency account when you need multiple currencies in one place, local receiving details in multiple countries, and integration with accounting tools such as QuickBooks, Xero, or Sage. Use a traditional bank account when your main need is a domestic operating account. The deciding criteria are visibility and control: balances, fees, references, and payout records should stay clear without manual patching.

How do I stop reconciliation from turning into cleanup work?

Start with setup checks before volume increases: confirm you can see balances and transfers across currencies in one dashboard and that your account integrates with tools like QuickBooks, Xero, or Sage. If either control is missing, expect more manual cleanup later.

When should I hand this off to tax or compliance help?

Escalate as soon as you suspect a filing, reporting, or residency trigger in any jurisdiction. Verify the actual rule instead of assuming a threshold. Bring an evidence pack on day one: account list, statements, transfer log, provider names, balances by currency, and account control details.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ato.gov.au/individuals-and-families/coming-to-australia...trusted

- bis.org/cpmi/publ/swift_gpi.pdftrusted

- cftc.gov/LearnAndProtect/AdvisoriesAndArticles/Custom...trusted

- congress.gov/bill/114th-congress/house-bill/2029trusted

- consumerfinance.gov/rules-policy/regulations/1005/interp-31trusted

- federalreserve.gov/boarddocs/supmanual/cch/cch.pdftrusted

- hbs.edu/ris/Publication%20Files/21-096_3317d99c-a5fb...trusted

- imf.org/-/media/files/publications/fandd/article/202...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

Should Your Freelance Business Accept Credit Cards?

Offer card payments, but stay in control of how money reaches you. The goal is not a smoother checkout screen. It is predictable cash you can use to run the business.

How to Connect Wise to QuickBooks for Automatic Reconciliation

**Use a risk-first Wise to QuickBooks setup to tighten transaction visibility and make reconciliation more predictable.**