Quick Answer

Yes - start your global equity plan remote team process with classification, then set cash-versus-equity rules, then issue only in approved countries. Use a hard gate for worker type (employee, EOR, or independent contractor), confirm the award path (such as stock options or RSU), and assign a named owner for taxable events. Keep “issued” separate from “accepted” in your records so grant delivery is verifiable.

Why classification, country approval, and cash-first rules define whether equity works#

You can build a global equity plan remote team strategy that helps you hire and retain strong people without pretending equity will solve cashflow problems. The goal is a plan you can actually run: one that treats equity compensation as upside, keeps near-term pay dependable, and avoids promises you cannot support across countries.

That balance matters because remote hiring expands your talent pool quickly. Once you are hiring beyond one local market, equity can become a real recruiting tool. It can help attract talent, improve engagement, and support retention by giving people a stake in the company. But cross-border grants bring legal and tax risk, and that risk can start early if offer terms are too loose or country-level requirements are unclear.

For freelancers, creators, and small teams, the useful question is not whether equity is powerful in theory. It is whether your business can offer it without weakening the basics people rely on every month: invoices paid on time, predictable payout timing, and compensation terms that do not push company risk onto workers who need cash to make rent. If someone depends on your payments for day-to-day living costs, cash reliability still comes first. Equity can strengthen the offer, but it should not be used to cover weak payment operations.

So this guide stays focused on practical decisions, not legal theory. Focus on what you can document and verify: who is an employee versus an independent contractor or EOR worker, what kind of award you intend to use, who approves changes to your plan, and who tracks taxable events once grants exist. Use a simple checkpoint here: if you cannot name the worker type, the proposed grant path, and the owner for compliance and tax monitoring, you are not ready to promise equity in an offer conversation.

There is also a hard limit to what any global process can do. Centralized tools and cleaner records can simplify administration and tax tracking, but they do not remove country-specific legal requirements. You may still need local counsel where employment law or tax treatment is unclear. That is not overkill. It is the difference between an offer that builds trust and one that creates a cleanup project later.

The sections that follow walk through the sequence that keeps this workable: classify the person correctly, decide when cash should outweigh equity, choose an award you can administer, and only then move into country compliance and grant operations.

Related reading: How to Create a Travel Policy for a Remote Team.

Want a quick next step for "global equity plan remote team"? Try the free invoice generator.

Gather Prerequisites Before You Issue Anything#

For a global equity plan remote team, start with a pre-issue record, not a grant template. You should be able to name who the worker is, what grant path you are considering, and who owns compliance before equity comes up in an offer.

| Pre-issue step | Required check | If unresolved |

|---|---|---|

| Define worker category | Classify each person as a direct employee, independent contractor, or Employer of Record (EOR) worker first | If any field is missing or disputed, hold the grant |

| Build country evidence pack | Capture role type and worker category; cash and equity compensation mix; expected grant type; known country tax steps and open questions; local paperwork requirements | If tax or compliance handling is unresolved, mark the case as review-required instead of approved |

| Confirm plan document and owner | Confirm which base plan document is in force and who runs operations against it | Approving grants without assigning post-issuance tax-event monitoring is a common failure point |

| Set verification gate | Document classification and local compliance assumptions in one place and have the named owner review them | If classification is unclear or local handling is still an assumption, do not issue yet |

Step 1. Define worker category before award mechanics. Classify each person as a direct employee, independent contractor, or Employer of Record (EOR) worker first. Global hiring creates legal and administrative complexity, and this classification drives how you handle grant operations. With an EOR, the third party is the official employer and handles employment administration, while you still manage day-to-day work.

Use a simple gate in your tracker: one worker type, one employing entity or contract owner, and one country of work per person. If any field is missing or disputed, hold the grant.

Step 2. Build a minimum country evidence pack. Map requirements before implementation decisions. It is harder and more expensive to unwind decisions after equity is already referenced in offers or records.

Keep the pack lean and complete enough for a yes/no decision:

- role type and worker category

- cash and equity compensation mix

- expected grant type (for example, stock options or a VSOP-style cash-linked plan)

- known country tax steps and open questions

- local paperwork requirements, including signer and language needs

If tax or compliance handling is unresolved, mark the case as review-required instead of approved.

Step 3. Confirm the governing plan document and operating owner. Before issuance, confirm which base plan document is in force and who runs operations against it. You need clear ownership for ESOP changes, taxable-event tracking, and localized signing flow.

Document handoffs if legal, finance, and HR split responsibilities. A common failure point is approving grants without assigning post-issuance tax-event monitoring.

Step 4. Set a hard verification gate before launch. No grant should move until classification and local compliance assumptions are documented in one place and reviewed by the named owner.

Use one enforcement rule: if classification is unclear or local handling is still an assumption, do not issue yet.

For a step-by-step walkthrough, see A Guide to Salary Bands and Compensation for a Global Remote Team.

Decide Cash Versus Equity With Explicit Rules#

Set one default rule and enforce it: if someone relies on this role for monthly living costs, lead with cash and treat equity as upside, not replacement.

Step 1. Set a written cash-first floor. Document a cash-equity trade-off policy before package discussions so offers are not negotiated ad hoc. Keep regular pay dependable, especially for people supporting themselves or a household from this role.

A practical guardrail is a capped salary swap that needs written exception approval above the cap. One published example uses 15% of salary as the maximum trade-off. Use that as a policy design reference, not a universal legal ratio.

For each offer, verify and record:

- base cash amount

- payment frequency

- award type (for example, stock options, NSO, or RSU)

- salary-to-equity trade percentage

- named approver for any exception

If the rationale starts to treat equity as a substitute for cash compensation, revise the offer.

Step 2. Use a role-based matrix, not manager preference. Pick a mix by role risk and pay predictability.

| Offer mix | Best fit | Main risk | Retention upside | Payment predictability |

|---|---|---|---|---|

| Cash-heavy | critical and client-facing roles; workers dependent on monthly income | higher near-term cash burn | lower than equity-heavy | high |

| Mixed | standard hires needing alignment and stable pay | confusion if rules are vague | moderate | medium to high |

| Equity-heavy | early-stage hires who can absorb volatility | worker cash strain and potential tax/cashflow friction | high when upside is credible | low |

Early-stage context can justify more equity in limited cases; for example, seed-stage packages may use a 1:2 cash-to-equity framing.

Step 3. Add a hard escalation trigger for payment reliability. If payroll or contractor payment reliability is unstable, pause expanded stock option or RSU offers until cash operations stabilize. Wages should be paid regularly, with a floor of at least monthly frequency.

Check actual payment records before approving broader equity usage. If consistency is unresolved, hold the expanded equity package and fix cash delivery first.

Step 4. Weigh equity tax timing before increasing equity-heavy mixes. Heavier NSO use can fit some early-stage constraints, but recipients may have income at grant under IRS guidance. That can create near-term tax and cashflow friction, especially when cash pay is already tight.

For critical roles, stronger cash certainty is usually safer even when equity is included. Operating rule: when payment reliability or tax handling is unclear, shift the mix toward cash.

Choose the Right Equity Award for Each Worker Type#

Pick the award your structure can legally grant and your team can explain clearly, then treat everything else as an exception. Most errors happen when equity is promised before confirming whether the worker is a direct employee, an Employer of Record (EOR) employee, or an independent contractor.

Before anyone promises options, RSUs, RSAs, or Phantom Units, confirm in writing:

- worker type and legal employer

- whether your plan documents support that award for that worker category

- country and taxable-event assumptions you can support

For EOR and contractor populations, make this a hard checkpoint. EORs legally employ the worker while your company directs day-to-day work, so direct-employee grant mechanics may not transfer as-is. If the check is incomplete, frame equity as subject to structure and local review, not as a committed grant.

If you use ISO language, be precise. Under U.S. Section 422, ISO treatment is connected to employment by the corporation, includes a 10-year term condition, and applies a $100,000 annual first-exercisable value limit before excess is treated as nonstatutory.

| Award type | Typical fit by worker type | Admin burden | Recipient clarity | Tax/reporting checkpoint |

|---|---|---|---|---|

| Stock options | Usually direct employees when plan docs support share purchase rights | Medium | Medium | Employee-only variants may not fit EOR/contractor structures |

| RSU | Employee populations where share delivery after restrictions is workable | Medium | High | RSUs are not treated as property under IRC Section 83 at grant |

| RSA | Employee cases where restricted stock is intentionally issued | Medium to high | Medium | 83(b) election may be available for RSAs |

| Phantom Units | Cases where actual share issuance is not workable or not preferred | Medium | High | Cash-settled design shifts burden to payout and reporting later |

Set one default path and one exception path:

- Default: standard hires get your primary award type under the existing plan.

- Exception: EOR workers, contractors, or countries with unresolved tax/structure questions require documented legal review before offer-stage promises.

Related: How to Structure an Employee Stock Option Plan (ESOP) for a US Startup.

Build a Country Compliance Map You Can Operate Weekly#

Treat this as an execution gate, not a reference doc: if a country is not clearly approved for the worker type and award type in your tracker, do not promise or issue the grant.

That rule matches the risk. Cross-border equity can trigger local tax, securities, reporting, currency, and payroll-withholding obligations, and outcomes can change based on worker type and structure. In EOR setups, equity handling still depends on where the person lives and how the equity is structured.

Step 1. Create one country tracker with legal, tax, and operational ownership in the same row. Each row should tie together jurisdiction, worker type, legal employer, proposed award type, plan eligibility, owners for employment-law and tax checks, local tax handling for taxable events, final approver, current status, and an evidence link.

If a row has no owner or no evidence, treat it as not reviewed.

Step 2. Use a status model that drives clear actions across recruiting, finance, and legal.

| Status | What it means in practice | Offer and grant rule |

|---|---|---|

| Draft | Country is in scope, but assumptions are incomplete or unverified | No promise of equity awards |

| Legally reviewed | Local legal or tax review is complete, but internal approvals or operating steps are still open | Do not issue yet |

| Approved for offers | Worker classification, plan eligibility, and local tax handling are confirmed for a specific worker type and award | Offer language may include approved equity |

| Paused | Earlier approval is no longer reliable because facts changed or a question is unresolved | Freeze new offers and grants |

| Restricted to specific equity awards | Country is usable only for named award paths or worker types | Use only the listed path |

Keep legally reviewed separate from approved for offers: legal viability alone is not operational readiness.

Step 3. Tie grants to hard pre-issuance checks. Before issuance, confirm worker classification, plan eligibility, and local tax handling for taxable events in the country row. If any one is missing, the grant is blocked.

Also recheck that the offer record still matches the row (worker type, legal employer, and allowed award). If it no longer matches, move the jurisdiction to paused or restricted until re-reviewed.

Step 4. Audit the map monthly against your actual hiring footprint. Compare the tracker with signed offers, pending hires, location changes, and newly added countries. If expansion is outpacing review, freeze new equity promises in those jurisdictions until rows are complete.

As volume grows, replace disconnected spreadsheets with connected workflows so HR, payroll, and equity records stay aligned in one operating view.

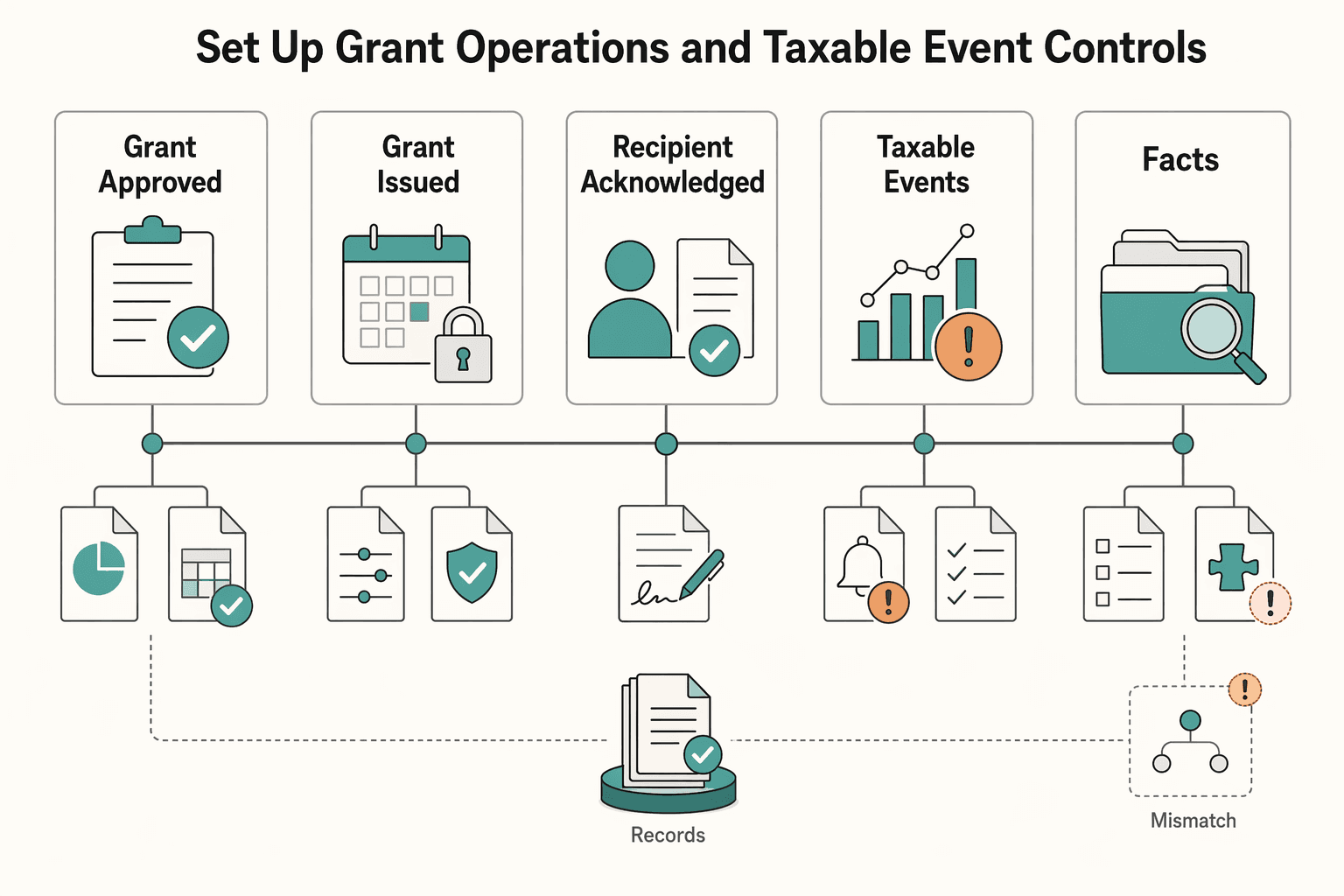

Set Up Grant Operations and Taxable Event Controls#

After a country row is approved, run grants through a controlled workflow: one source of truth, one fixed sequence, named taxable-event ownership, and a written exception path.

| Stage | Control point |

|---|---|

| grant approved | Approval is recorded before issuance |

| grant issued | Do not treat "issued" and "delivered" as the same thing |

| recipient acknowledged | If acknowledgement is missing in your employee equity portal, the grant is still operationally incomplete |

| taxable events monitored | Each grant record should state what event is monitored, who reviews it, and where reporting artifacts are stored |

| reporting artifacts stored | Payroll notes, tax memos, or recipient notices should be stored so they are not missed later |

Step 1. Centralize every award in one operating record. Keep stock options, RSUs, RSAs, and Phantom Units in the same system, even when legal documents differ. For each grant, track recipient, worker type, legal employer, country, award type, approval date, issue date, vesting terms, and the owner for taxable-event monitoring.

Equity management software can help if it truly centralizes cap table records, grants, and compliance workflow details. The practical test is whether your process can import cap table data, issue grants, and retain audit-trail and tax-rule notes without pushing teams back to spreadsheets. Verification point: for one live grant, confirm approval, grant document, recipient identity details, and country-specific notes are visible in one record.

Step 2. Lock the order of operations before issuance. Keep statuses distinct and move each grant through the same sequence:

- grant approved

- grant issued

- recipient acknowledged

- taxable events monitored

- reporting artifacts stored

Do not treat "issued" and "delivered" as the same thing. If acknowledgement is missing in your employee equity portal, the grant is still operationally incomplete. Checkpoint: status should show the exact stage in this chain, not just "granted."

Step 3. Assign taxable-event monitoring to a named owner, not a generic team label. Compliance mistakes are a major cost risk in equity programs, so each grant record should state what event is monitored, who reviews it, and where reporting artifacts are stored.

If you use country-aware tooling, apply it during grant processing so issues are flagged early. Use automation to support filings, tax-rule handling, and audit trails, but keep human review in the loop. Failure mode to watch: issuance is complete, but later payroll notes, tax memos, or recipient notices are never stored.

Step 4. Define the exception procedure for incomplete data or missed deadlines. Make ownership explicit: one person freezes status, one person fixes records, and one approver re-authorizes progression.

Use strict triggers:

- incomplete recipient data: no issuance

- missing acknowledgement: no "delivered" status

- missing reporting artifact: pause related follow-on actions until complete

That discipline is usually cheaper than repairing errors after they spread across a remote team.

Publish a Plain-Language Equity Explainer for the Team#

Publish one plain-language explainer, then layer country and role-specific addenda, and do not treat a grant as fully delivered until the recipient acknowledges it in your equity portal.

Step 1: Write one global explainer in plain language. Define your ESOP as a plan that lets workers hold company ownership, define vesting as the timeline for when awarded shares become available, and state what equity is not (for example, not immediate cash and not the same as salary).

Step 2: Keep country detail in addenda. Use country addenda for likely taxable events and local paperwork expectations, since tax, securities, and reporting requirements differ by jurisdiction and compensation policies can vary by local law. Keep the wording careful: explain what people may need to review or sign, without promising legal or tax outcomes. For stock options, note that income recognition can occur when the option is received, exercised, or disposed of, depending on the facts.

Step 3: Separate guidance by worker type. Provide versions for direct employees, EOR populations, and independent contractor populations so each person can see what applies to their role and what still needs local review.

Step 4: Require portal acknowledgement before "delivered" status. Platform acceptance is a standard part of grant delivery workflows, and many companies require some acceptance process (2025 survey data: 7% reported they do not require consent, implying most do). Keep "issued" and "accepted" as separate statuses. Verification point: open one live grant and confirm the record shows the explainer, the country addendum, and the acknowledgement date.

Avoid the Common Mistakes That Break Trust#

Trust usually breaks when offers, worker status, and records drift out of sync. Use these four checks to catch that early and recover fast.

| Mistake | Recovery |

|---|---|

| Promising grants before local employment-law review | Pause new offers in that jurisdiction, review grant language and admin flow, then reissue corrected terms with a documented exception path |

| Using one template for every worker type | Split communications and acknowledgements for direct employees, Employer of Record workers, and independent contractors |

| Tracking grants but not taxable events | Backfill records beyond issuance and vesting, then assign one clear owner for event monitoring across legal, HR, payroll, and tax |

| Framing equity as a cash substitute | Reset policy to a cash-first floor for critical contributors, and position equity as upside rather than near-term pay replacement |

1) Mistake: Promising grants before local employment-law review. Recovery: Pause new offers in that jurisdiction, review grant language and admin flow, then reissue corrected terms with a documented exception path. Global equity and employment law often overlap, so check materials against current updates, not old assumptions. Keep one audit note per correction with what changed, who approved it, and why.

2) Mistake: Using one template for every worker type. Recovery: Split communications and acknowledgements for direct employees, Employer of Record workers, and independent contractors. Worker-status determination is not optional, and misclassification risk is real when teams treat unlike worker relationships as if they were the same. If you have U.S. exposure, keep your process aligned with the DOL's January 10, 2024 final rule (effective March 11, 2024).

3) Mistake: Tracking grants but not taxable events. Recovery: Backfill records beyond issuance and vesting, then assign one clear owner for event monitoring across legal, HR, payroll, and tax. For stock options, taxable income can arise at grant receipt, exercise, or disposal, so your controls need to track those moments. Use your reporting calendar as a live control, not a year-end scramble.

4) Mistake: Framing equity as a cash substitute. Recovery: Reset policy to a cash-first floor for critical contributors, and position equity as upside rather than near-term pay replacement. Equity can be part of compensation, but it should not be used to mask weak cash reliability.

Conclusion#

The plan that holds up is the one you can run every week without guessing. If worker type, country status, or compliance ownership is still unclear, pause new commitments until those fields are filled in and owned.

- Classify each person before you promise anything. Mark every worker under the hiring model you are actually using, and do not treat Employer of Record (EOR) and Contractor of Record (COR) arrangements as interchangeable.

Checkpoint: your tracker should show worker type, country, hiring model, legal employer (where applicable), and start date for every active person.

- Use written role rules for compensation and terms. Do not let managers improvise country by country or person by person. A simple written rule is enough if it helps you apply the same starting position to similar roles and forces exceptions into review instead of hallway decisions.

Red flag: if two similar hires got different treatment and nobody can point to an approved exception note, your policy is already drifting.

- Pick a default documentation path and document exceptions. You need one standard route your team understands, plus an exception path for cases where worker type or country review requires a different document set or a pause.

Checkpoint: each live record should link to the current document version, acceptance status, and any exception approval.

- Validate country compliance constraints before finalizing terms. Managing global hiring brings legal, administrative, and compliance complexity, so never assume a country is "good to go" just because you hired there once. Keep a country map with simple statuses such as draft, reviewed, approved, paused, or restricted, and block finalization until the status is clear.

Failure mode: teams often promise terms in offer conversations first and discover the country-specific issue after the fact.

- Assign one records owner for each case. One person on your side must own the record, even when an EOR handles part of the employment burden. With an EOR, remember the provider is the official employer and may handle payroll, tax compliance, and local labor law compliance, while your business still manages the person's day-to-day work and must keep its own approvals, communications, and stored records straight.

Checkpoint: that owner can open one record and show core dates, current status, and stored artifacts without asking three other teams.

- Publish a plain-language explainer and collect acknowledgements. Use one global explainer, then add worker-type or country notes where needed. A process is not fully delivered until the recipient has acknowledged the materials and you have stored that acknowledgement.

If you want one practical next step, audit a single live record today. If you cannot confirm the worker type, country status, current document version, and named records owner in under five minutes, tighten the process before the plan gets bigger.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- dol.gov/agencies/whd/flsa/misclassificationtrusted

- dol.gov/agencies/whd/flsa/misclassification/rulemakingtrusted

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- hbs.edu/managing-the-future-of-work/Documents/Buildi...trusted

- ilo.org/ilo-helpdesk-questions-and-answers-business-...trusted

- ilo.org/international-labour-standards/international...trusted

- irs.gov/taxtopics/tc427trusted

- irs.gov/publications/p525trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

How to Structure an Employee Stock Option Plan (ESOP) for a US Startup

If you searched for **employee stock option plan esop**, stop and sort out the label first. In startup conversations, people often say "ESOP" when they mean a stock option plan or option pool. A formal **Employee Stock Ownership Plan (ESOP)** is different. It is often discussed as a business transition option for owners, while startup stock options are commonly used to give employees a stake in the business.

Competitive Benefits for International Contractors Without Misclassification Risk

As an independent professional, your most valuable asset is not your client list. It is your autonomy. That independence is fragile, and it is protected by deliberate business structure, not by hope. Build that structure to protect your autonomy, signal professionalism, and help you operate as a resilient Business-of-One.