Quick Answer

A Section 962 election can reduce current-year U.S. tax and preserve cash by letting an individual U.S. shareholder use corporate-style tax and foreign tax credit rules on CFC inclusions. It usually fits best when profits will stay in the company, foreign tax support is strong, and you can handle the added filing, tracking, and later distribution modeling.

The Section 962 Election: A Strategic Diagnostic for Global Founders#

A Section 962 election lets an individual U.S. shareholder calculate current-year CFC inclusion tax using corporate-style rules under Section 11, including corporate-style foreign tax credit mechanics under Sections 960(a) and 960(d), rather than staying fully on the ordinary individual path. The main tradeoff is timing. It may improve current-year cash retention, but later distributions can still trigger additional U.S. income to the extent earnings and profits exceed tax already paid under the election. Use it as a screening tool before you run a full model.

First, confirm scope and eligibility. You generally need to be a U.S. shareholder with 10% or more ownership, and the foreign corporation must be a CFC with more than 50% U.S. shareholder ownership. This is also a year-wide election made by filing a statement with your return. If you elect, it applies across all CFCs with relevant inclusions for that year.

Decision Gate 1. Will you keep cash in the company?#

This election is often most useful as a timing tool when cash stays in the business. Good fit: you expect to retain and reinvest profits for operations, hiring, inventory, or expansion over a multi-year period. Weak fit: you expect near-term personal distributions for living costs, debt service, or personal investing.

Decision Gate 2. What does your foreign-tax profile look like?#

The election gets harder to analyze when the foreign-tax side is thin or poorly documented. Good fit: your CFC pays foreign income tax, and your records can support credit computations. Weak fit: foreign taxes are minimal, unclear, or poorly documented.

If your planning depends on a specific exception or breakpoint, do not guess from old summaries. Keep a placeholder in your model until you confirm the current-year rule.

Decision Gate 3. Does your personal U.S. tax position justify the admin load?#

Even when the tax model looks favorable, the filing burden can erase the practical benefit. Good fit: corporate-style treatment may create meaningful current-year relief, and you can maintain corporation-by-corporation support files and distribution tracking. Weak fit: expected benefit is small, and the added filing and recordkeeping burden is likely to outweigh it.

| Decision gate | Good fit | Weak fit |

|---|---|---|

| Keep cash in the company | Expect to retain and reinvest profits for operations, hiring, inventory, or expansion over a multi-year period | Expect near-term personal distributions for living costs, debt service, or personal investing |

| Foreign-tax profile | Your CFC pays foreign income tax, and your records can support credit computations | Foreign taxes are minimal, unclear, or poorly documented |

| Personal U.S. tax/admin load | Corporate-style treatment may create meaningful current-year relief, and you can maintain corporation-by-corporation support files and distribution tracking | Expected benefit is small and the added filing and recordkeeping burden is likely to outweigh it |

For Section 962 electing individuals, Section 250 deduction calculations are handled through Form 8993. In 2026, also expect terminology overlap: Code text uses "net CFC tested income," while IRS forms and instructions still commonly use "GILTI."

| Path | Immediate cash impact | Future distribution consequence | Recordkeeping burden | Usually safer when |

|---|---|---|---|---|

| Elect | May reduce current-year U.S. tax through corporate-style computation and foreign tax credit mechanics | Later distributions can create additional gross income beyond tax already paid under the election | Higher: election statement, corporation-by-corporation inclusion support, and distribution tracking | You plan to reinvest earnings and can support ongoing compliance |

| Do not elect | Simpler current-year treatment, may preserve less cash now | No Section 962-specific distribution layer | Lower | You expect near-term distributions or limited current-year benefit |

Use this diagnostic to screen for fit, then test it against modeled scenarios before filing. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

The Framework in Action: Two Real-World Scenarios#

The easiest way to pressure-test the election is to map it to your actual cash behavior. If you mostly reinvest, run a full model. If you mostly distribute, run the same model with extra attention to later distributions and tracking assumptions.

Scenario 1. You are reinvestment-first#

If your company earns your modeled income amount and you plan to keep most cash in the business, model both paths with a focus on current-year cash retention and later distribution consequences. Your first checkpoint is foreign tax credit support.

Do not assume a foreign tax is creditable. The credit requires 4 tests, including legal liability, paid or accrued, legal and actual liability, and income tax or tax in lieu of one. Some foreign taxes can still be noncreditable. Build your file with foreign tax records, proof of payment, and support showing the amounts were legally owed, including whether any amount is refundable.

Scenario 2. You are distribution-first#

If your company earns your modeled income amount and you expect regular near-term personal distributions, treat this as a modeling exercise, not an automatic win. You still compare immediate-year results, and you also need a later distribution model plus clean tracking of relevant amounts.

If you rely on a credit that later fails review or is redetermined, your downside risk increases. In that case, the added administration may outweigh the modeled benefit.

| Comparison point | Reinvestment profile without election | Reinvestment profile with election | Distribution-first profile without election | Distribution-first profile with election |

|---|---|---|---|---|

| Immediate-year impact | Model with your modeled income amount and your verified current rate | Model the same income under the election path; compare only after credit eligibility screening | Model current year assuming near-term payouts | Can differ in the model; verify assumptions |

| Later distribution impact | Model expected distributions under this path | Model later distributions explicitly and compare outcomes against taxes already modeled under the election | Model payout timing explicitly | Model frequent payouts explicitly under the same assumptions |

| Foreign tax credit availability | Do not assume availability | Test eligibility under the 4-test screen; where relevant, account for Section 951A category income as a separate Form 1116 category | Do not assume availability | Same eligibility risk, with more sensitivity if projected benefit depends on credit support |

| Tracking burden | Define your baseline tracking process | Maintain year-by-year records for electing-year amounts and distributions | Define tracking for payout-heavy years | Expect more frequent tracking updates when distributions are frequent |

| Verification checkpoints | Confirm source tax records exist | Confirm records can support review; check Schedule C (Form 1116) and Foreign Tax Redeterminations items when foreign tax numbers change | Confirm distribution timing assumptions | Confirm you can sustain ongoing tracking and revisit filings when foreign tax inputs change |

A quick way to model this yourself#

Start with the few inputs that actually move the result, then compare the two paths side by side.

- Inputs to gather: your modeled income amount, expected personal distributions in the near term, foreign tax records, proof of payment, and refund rights.

- Outputs to compare: immediate-year U.S. result under both paths, whether any foreign tax credit appears supportable after the 4-test screen, and modeled later distribution outcomes.

- Weak-fit signal: weakly documented foreign taxes, uncertainty around whether taxes were legally owed, or a projected benefit that disappears after adding distribution effects and compliance workload.

The practical takeaway is straightforward: decide only after you test your assumptions, credit eligibility, and redetermination risk in your own model. Validate the result with an international tax professional before you file.

We covered this in detail in A Guide to Getting a 'PTE' (Pass-Through Entity) Tax Election.

The Strategic Trade-Offs: A Deeper Look#

The decision is less about whether the election lowers tax in one year and more about whether it still looks good after you account for distributions, credits, and recordkeeping. In practice, that often comes down to your operating model: reinvestment-first versus regular personal withdrawals.

Where the upside comes from in the current year#

In the inclusion year, §962 lets an individual U.S. shareholder compute tax on §951(a) inclusions using corporate-rate mechanics. A §962 electing individual may also determine a Section 250 deduction on Form 8993. Deemed-paid foreign tax credit mechanics under §960 via §962 may apply when supported.

| Term | Meaning |

|---|---|

| Section 250 deduction | A deduction mechanism that may reduce certain inclusion-related amounts, determined for §962 electing individuals on Form 8993 |

| Deemed-paid foreign tax credits (via §960/§962) | Certain foreign taxes can be treated as if a domestic corporation received the amounts |

| PTEP | Previously taxed earnings and profits, meaning foreign-company earnings already included in a U.S. shareholder's income |

| E&P | Earnings and profits, the foreign corporation tax-accounting measure determined under rules substantially similar to domestic-corporation rules |

Keep those definitions in view while you model. Use current filing-year authority for Section 250 inputs. If your modeled benefit is credit-driven, confirm your foreign-tax positions are supportable in your filing records.

Where regret usually shows up in later years#

This is the step people skip, and it is where weak elections often reveal themselves. Model the later distribution before you call the election a win.

Outside the §962 override, §959 generally prevents the same PTEP from being taxed again. But §962(d) can require gross-income inclusion when distributed E&P exceeds the amount of tax previously paid under chapter 1.

That means this is often a deferral tool, not a permanent tax erase. It tends to age better when you keep earnings in the company, and it can disappoint when you expect frequent near-term personal distributions.

| Lifecycle point | Without the election | With the election |

|---|---|---|

| Current-year inclusion | Taxed under individual-level rules | Computed using corporate-rate mechanics; Section 250 may apply via Form 8993 and deemed-paid foreign tax credit mechanics may apply if supportable |

| Later distribution | PTEP generally not included again under §959 | §962(d) can trigger gross-income inclusion when E&P is distributed |

| Compliance overhead | Generally lower tracking burden | Higher: election statement plus added E&P/PTEP, distribution, and foreign-tax support tracking |

| Cash-flow flexibility | Can be simpler for frequent payouts | Can be stronger if you retain cash and control payout timing |

Treat administration as part of the tax cost#

The filing burden belongs in the decision, not in a footnote. You make the election by filing a statement with your return for that year. The statement has required contents, and the election applies across all relevant CFCs for the year.

| Checkpoint | What to review |

|---|---|

| Validate assumptions | Expected distribution behavior, inclusions in scope, and filing-year Form 8993 inputs |

| Validate credit support | How foreign-tax support is documented and how later tax changes would be handled |

| Maintain records | Election statement, E&P/PTEP tracking, and a distribution ledger tied to electing years |

| Re-evaluate on triggers | New CFCs, ownership changes, payout-policy shifts, or post-filing foreign-tax changes |

| Escalate early | If the benefit only works under aggressive credit assumptions or your support file is incomplete |

Also treat the choice as sticky: revocation for that taxable year requires Secretary consent.

A risk-of-regret lens. The election usually holds up best when you have a real reinvestment horizon, limited personal draws, and records that support your credit positions over time. It tends to age poorly when withdrawals are frequent, foreign-tax support is weak, or the modeled benefit disappears once later distributions are included.

If your model depends heavily on credits, re-check it annually. IRS Notice 2025-77 describes a 10 percent foreign tax credit disallowance for certain foreign taxes tied to §959(a) distributions from §951A inclusions after June 28, 2025. Rerun filing-year assumptions when facts shift.

Advisor guardrails before the next filing cycle. Use the checkpoint table above before the next filing cycle to see whether the election still belongs in the plan.

For a step-by-step walkthrough, see A Deep Dive into 'Subpart F' Income for US Shareholders of CFCs.

Your Execution Checklist: Making the Election with Confidence#

Once you decide to proceed, treat execution like a control process. Build a filing-year-valid package, tie it to your CFC reporting, and keep records that will still make sense in later years.

Phase 1. Pre-filing prep.

Step 1. Confirm filing-year authority first. Pull the current instructions before drafting. For Form 5471, the reference point here is the Rev. December 2025 instructions. IRS also directs filers to check IRS.gov/Form5471 for post-publication updates, so do not rely on stale instructions or IRB synopses as authoritative interpretation.

Step 2. Build a CFC fact pack for each entity. Prepare one workpaper per foreign corporation with the data you will use in filing, including E&P and any foreign-tax support. Your deliverable should map cleanly to the schedules and statements used for sections 6038 and 6046 reporting.

| Step | Inputs you need | Output artifact | Common failure point |

|---|---|---|---|

| 1 | Current instructions, IRS developments page | Filing-year authority file | Using stale instructions or nonauthoritative summaries |

| 2 | Entity details, ownership data, E&P records, foreign-tax support | CFC workpaper by entity | Mixing entities or leaving support unmapped to reporting schedules |

Phase 2. Filing package assembly.

Step 3. Draft the election package and tie-outs. Prepare the election package for the year, add supporting calculations, and link everything to the current filing form or instruction you verify. Before filing, confirm the package reconciles to your Form 5471 reporting outputs.

Step 4. Clear attachment checkpoints before submission. If functional-currency QBUs are present, test whether Schedule G question 3b requires a "Yes" and a Forms 8964-TRA attachment count. If section 304 affects E&P, make sure your workpapers support Schedule G line 21b(1) (PTEP change) and line 21b(2) (other E&P change).

| Step | Inputs you need | Output artifact | Common failure point |

|---|---|---|---|

| 3 | Election draft, calculations, CFC workpapers | Final filing package | Package numbers not tied out to Form 5471 reporting |

| 4 | Form 5471 schedules, special-fact review | Attachment checkpoint sign-off | Missing Schedule G triggers or unsupported E&P entries |

Phase 3. Post-filing record maintenance.

Step 5. Lock and maintain the permanent file. Keep the exact filed package version, dated calculation files, and annual rollforwards. Maintain an operational control file with versioning, CFC-level workpapers, foreign-tax support, and PTEP tracking by year so later reporting stays consistent.

Use the verified current timeliness rule for your filing calendar, and refresh the file when ownership, payout policy, or foreign-tax facts change.

| Step | Inputs you need | Output artifact | Common failure point |

|---|---|---|---|

| 5 | Filed return package, calculation set, CFC workpapers, foreign-tax support, PTEP history | Permanent control file and annual rollforward | No version control or incomplete year-by-year PTEP tracking |

You might also find this useful: What is the 'Mark-to-Market' Election for PFICs?.

If withholding documentation is relevant to your filing process, run it through the W-8 Form Generator so your election-year records are easier to review.

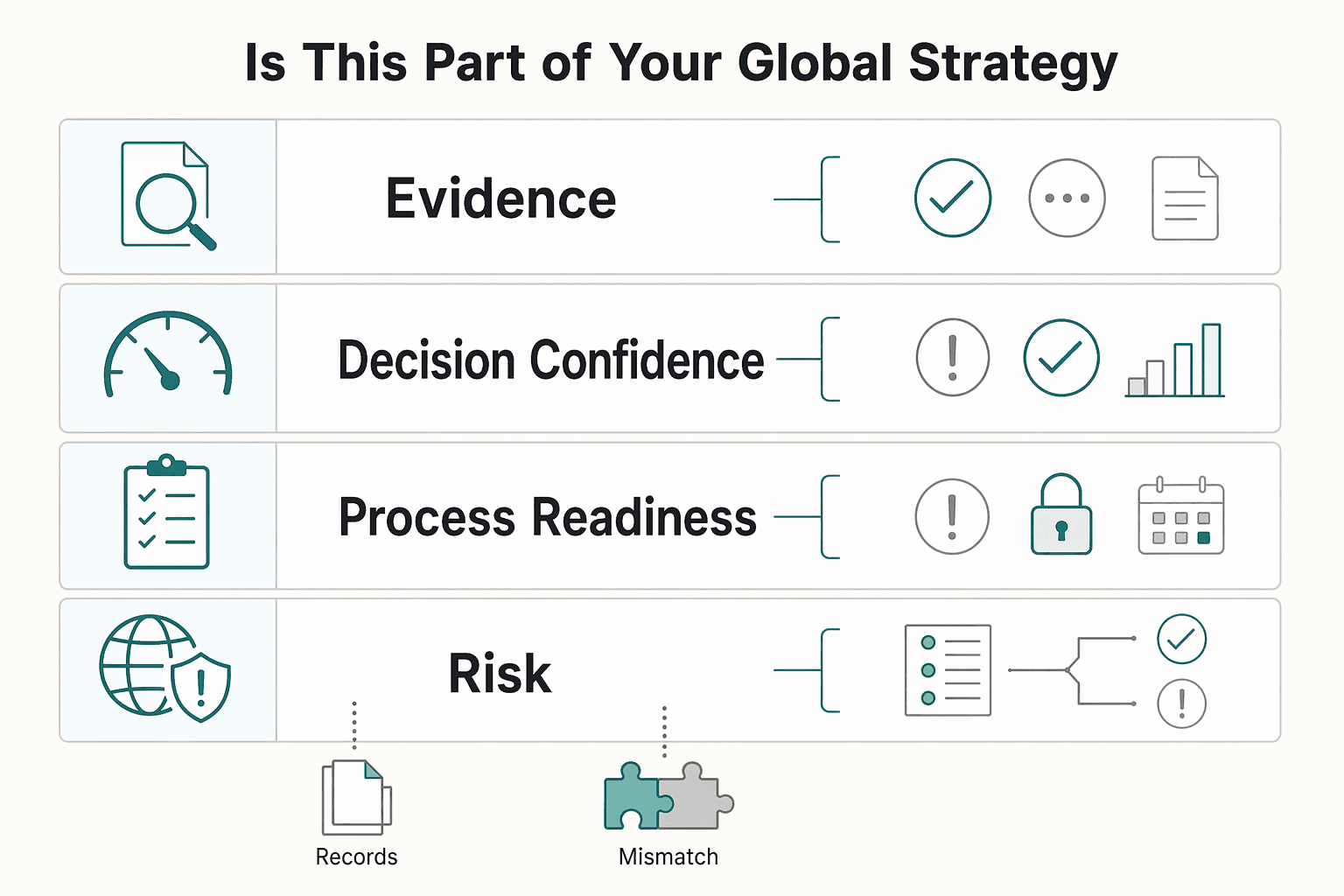

The Final Verdict: Is This Part of Your Global Strategy?#

Based on the limited usable evidence here, the practical default is no-go for a self-directed decision. The material here suggests Section 962 may be used to cushion a potential "double-tax blow," but it does not provide enough support for detailed mechanics or a broad fit test.

| Criteria | Likely fit | Likely poor fit |

|---|---|---|

| Evidence quality | You have current, case-specific tax analysis from a qualified advisor. | You are relying on generic summaries or incomplete excerpts. |

| Decision confidence | You can document why this election fits your exact facts this year. | You cannot validate the outcome for your specific facts. |

| Process readiness | You are prepared to follow advisor-led filing and recordkeeping requirements. | You want to proceed without specialist review. |

| Risk tolerance | You are comfortable pausing until facts are fully verified. | You need a quick yes/no based on limited information. |

Step 1. Treat this as an advisor-required decision. Do not make a go/no-go call from this excerpt alone.

Step 2. Verify current-year requirements with a qualified advisor. Confirm applicability, filing approach, and implications for your exact facts before acting.

Step 3. Keep your records audit-ready. Maintain clear documentation of the analysis and final decision path.

Related: A Guide to the Global Intangible Low-Taxed Income (GILTI) Regime. If you want audit-ready payment and payout records while you execute this tax strategy, talk to Gruv.

Frequently Asked Questions

What are the pros and cons of a Section 962 election?

The main potential advantage is better current-year cash retention through corporate-style computation and foreign tax credit mechanics. The main tradeoffs are added filing and recordkeeping and the possibility that later distributions create additional U.S. income. It works best when cash stays in the company and your records are strong.

When should you consider it?

Consider it when retaining and reinvesting profits is a priority, your CFC pays foreign income tax, and your records can support the credit analysis. Re-check current filing-year rules before filing. If you expect near-term personal distributions, it is usually a weaker fit.

How does it affect GILTI tax?

Its effect should be modeled, not assumed. For Section 962 electing individuals, Section 250 deduction calculations are handled through Form 8993. For foreign tax credits, individuals use Form 1116 and corporations use Form 1118, so re-check the current filing-year instructions before you file.

Is it permanent?

Treat it as a filing-year decision. The election is made by filing a statement with your return for that year, and revocation for that taxable year requires Secretary consent. Re-verify the current guidance each year.

Who is eligible to make it?

You generally need to be a U.S. shareholder with 10% or more ownership, and the foreign corporation must be a CFC with more than 50% U.S. shareholder ownership. Confirm eligibility under current filing-year rules for your specific ownership and entity facts. Do not assume eligibility from ownership alone.

Do foreign taxes automatically offset the U.S. tax?

No. Foreign taxes help only if they are creditable and supported by records. The article says the IRS requires tests including legal liability, paid or accrued, legal and actual liability, and income tax or tax in lieu of one. Some taxes can still be noncreditable even then.

What happens when you distribute earnings after making the election?

Later payouts should be modeled separately, not assumed. The article says Section 962(d) can require gross-income inclusion when distributed earnings and profits exceed the amount of tax previously paid under the election. That is why the election is often a timing tool rather than a permanent tax erase.

What if the foreign tax numbers change later?

Assume later changes may require you to revisit your credit position. The article points to Foreign Tax Redeterminations and Schedule C on Form 1116 when foreign tax numbers change. Your file should be detailed enough to support updates if amounts are adjusted later.

Does this election avoid U.S. tax?

No. It does not automatically eliminate U.S. tax. Your outcome still depends on whether foreign taxes are actually creditable and on later-year facts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

What Is a Controlled Foreign Corporation (CFC) for a U.S. Shareholder?

**If your foreign company might raise a CFC question for U.S. tax purposes, do not guess.** Get to a documented yes or no with a qualified advisor. In practice, that means confirming three things in order: how the entity is being treated for the U.S. tax review, how ownership and control are being analyzed, and what compliance or filing steps, if any, apply this year. Keep those frameworks separate, too. NYSE "[controlled company](https://www.sec.gov/Archives/edgar/data/1977102/000119312523254724/d507917d424b4.htm)" language in SEC materials is not the same as U.S. tax CFC analysis, and mixing them creates false confidence fast.

GILTI for U.S. Founders Abroad: A 3-Step Playbook

You need to make three decisions, in order. First, whether you are in scope. Second, which inputs create a current inclusion. Third, whether default treatment, a Section 962 election, or a structuring conversation is the right next move. If the global intangible low-taxed income, or GILTI, rules apply, your goal is a clear scope decision, a supportable exposure model, and a defined point where you escalate.