Quick Answer

Confirm eligibility before you invest: check HDHP status on the first day of each month you want to count, choose FEIE or FTC before funding, and correct any ineligible amount with a custodian return-of-excess request by the filing deadline including extensions. Then select a provider using costs, investing access, and transfer workflow rather than brand alone. Keep reimbursements tied to receipts, proof of payment, and service dates, and file Form 8889 whenever you take HSA distributions.

Before You Invest: Bulletproofing Your HSA for Global Compliance#

Your first job is compliance, not fund selection. Before you decide how to invest your HSA, first confirm eligibility, decide your tax treatment, and make sure the account setup will not create avoidable cross-border reporting issues. Use these terms precisely:

- FEIE (Foreign Earned Income Exclusion): a voluntary election to exclude qualifying foreign earned income from U.S. gross income.

- FTC (Foreign Tax Credit): a credit that reduces U.S. tax liability for qualifying foreign income taxes.

- "HSA-eligible income": useful shorthand, but not an IRS legal term. The IRS standard is whether you are an eligible individual.

- Excess contribution: an HSA contribution above the applicable limit that requires correction to avoid additional tax exposure.

Step 1. Confirm you are an eligible individual#

Check eligibility month by month before you fund anything. What matters is not whether you were eligible at some point in the year. What matters is whether you were eligible on the first day of each month you want to count.

You must be covered by an HSA-qualified HDHP on the first day of each month you want to count. You also must have no disqualifying other coverage, not be enrolled in Medicare, and not be claimable as another taxpayer's dependent.

| Test | What to verify now | What to keep in your file |

|---|---|---|

| HDHP deductible | For 2026: at least $1,700 self-only or $3,400 family. For later years, verify the current threshold. | Summary of Benefits and Coverage, policy certificate |

| HDHP out-of-pocket maximum | For 2026: no more than $8,500 self-only or $17,000 family. For later years, verify the current threshold. | Summary of Benefits and Coverage, insurer schedule |

| First-day-of-month coverage | HDHP is active on the first day of each month counted for contributions. | Effective-date notice, monthly coverage record |

| No disqualifying other coverage | No non-permitted additional coverage that breaks HSA eligibility. | Other policy documents, benefit elections (if relevant) |

| Medicare and dependency status | Not enrolled in Medicare and not claimable as another taxpayer's dependent. | Medicare status record, tax support file |

If these checks pass, apply the annual limit. For 2026, the full-year contribution cap is $4,400 (self-only) or $8,750 (family); apply that limit based on your eligible months.

Step 2. Decide tax treatment before contributing#

Make the return-position decision before you move cash. FEIE and FTC work differently, and you cannot claim FTC on income excluded under FEIE. Use this flow:

- Confirm you are an eligible individual under the rules above.

- Decide your return approach for the year before funding.

- If FEIE is part of the plan, review HSA contribution treatment with your preparer before contributing.

- If FTC is your path, still complete all HSA eligibility checks first.

A failure mode is funding first, then discovering at filing time that your eligibility months or return treatment did not support the contribution.

Step 3. Correct an ineligible contribution immediately#

If you contributed and later find you were ineligible for part or all of it, treat it as a correction right away. Ask the custodian for a return of excess contribution for the affected tax year.

| Item | Required action | Timing or effect |

|---|---|---|

| Return of excess contribution | Ask the custodian for a return of excess contribution for the affected tax year | Use the custodian's correction process rather than a standard distribution |

| Excess amount | Withdraw the excess by your return due date, including extensions | Avoid the additional 6% tax |

| Related earnings | Withdraw related earnings too | Report those earnings as other income |

| Late correction | If excess amounts come out after the due date, including extensions | That distribution is taxable even when used for qualified medical expenses |

| Records | Keep confirmation | The confirmation should show the amount, earnings, and tax year |

- To avoid the additional 6% tax, withdraw the excess by your return due date, including extensions.

- Withdraw related earnings too, and report those earnings as other income.

- If excess amounts come out after the due date, including extensions, that distribution is taxable even when used for qualified medical expenses.

Do not take a standard distribution and assume it fixed the issue. Use the custodian's correction process and keep confirmation of the amount, earnings, and tax year.

Step 4. Verify account domicile before assuming FBAR/Form 8938 relief#

This is where structure matters more than branding, because you may get reporting relief only if the account setup supports it.

| Account structure | Article note | What to confirm |

|---|---|---|

| U.S.-located institution | An account maintained by a U.S.-located institution is generally not foreign for FBAR purposes | Confirm where the account is actually maintained |

| Foreign branch of a U.S. financial institution | IRS guidance lists these accounts among non-reportable accounts for Form 8938; FBAR may be different for that same branch setup | Confirm the branch structure in the account agreement |

| Another offshore entity | Reporting treatment can change with the structure | Do not rely on the provider name alone |

For FBAR, the core test is where the financial institution is located. An account maintained by a U.S.-located institution is generally not foreign for FBAR purposes.

For Form 8938, some domestic-account setups are excluded, and IRS guidance also lists accounts at a foreign branch of a U.S. financial institution among non-reportable accounts. FBAR may be different for that same branch setup.

Do not rely on the provider name alone. Confirm the account agreement and where the account is actually maintained, whether that is a U.S. institution, a foreign branch, or another offshore entity. Reporting treatment can change with the structure.

Before you move to provider selection, confirm the following:

- Plan qualification: HDHP thresholds, first-day coverage, and no disqualifying coverage are documented.

- Tax-treatment choice: your return path is set before contribution timing and amount.

- Account domicile: institution location and account structure are verified for FBAR/Form 8938 analysis.

- Recordkeeping: plan records, contribution records, and any excess-correction paperwork are stored together.

Related: Tax Implications for an Australian Resident Owning a US LLC. Before you fund anything, run a quick FEIE check so your HSA contribution plan matches your tax-year strategy: Use the FEIE calculator.

Choosing Your Command Center: The Best HSA Providers#

Choose the provider that keeps your HSA easy to operate over time: clear costs, usable investing access, clean cash movement, and solid records. The wrong choice usually shows up later as avoidable fees, forced cash parking, reimbursement friction, or a painful transfer when you need to switch.

A scorecard works better than brand preference because it forces you to compare the parts that actually affect long-term use. Use a 100-point screen:

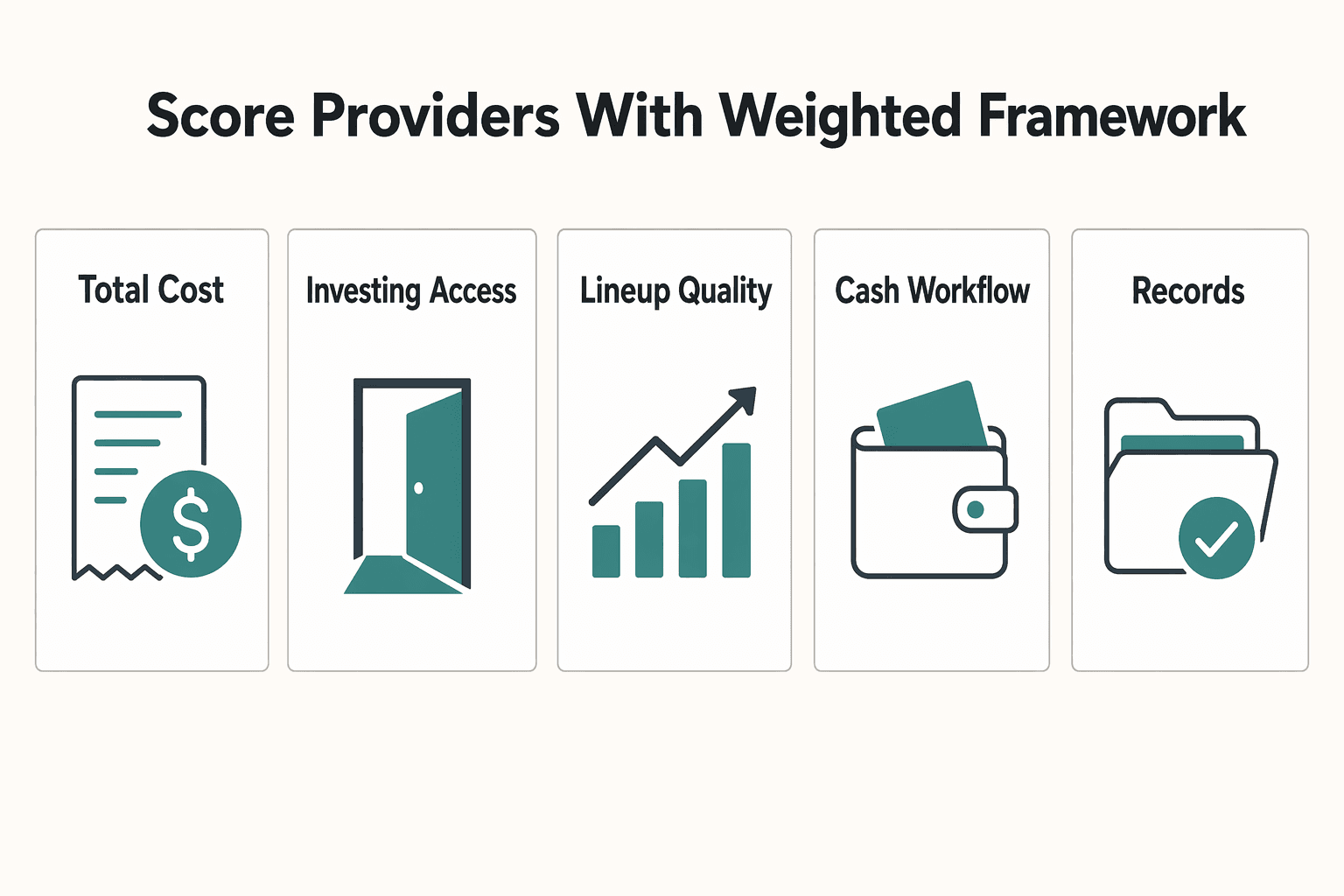

Step 1. Score each provider with a weighted framework#

| Criterion | Points | What to verify |

|---|---|---|

| Total cost | 30 | Maintenance, opening and closing, investing-related fees, and any cash-balance condition tied to brokerage access |

| Investing access | 25 | What you can invest in, when access starts, and whether thresholds or upgrades apply |

| Investment lineup quality | 20 | Whether the options are actually usable for your plan |

| Cash-management workflow | 10 | Recurring contribution and sweep capabilities if you rely on automation |

| Contribution and reimbursement operations | 10 | Clear contribution history and a clean reimbursement record trail |

| Tax-record handling | 5 | The records and forms needed to report HSA activity on Form 8889 |

- 30 points: Total cost. Verify maintenance, opening and closing, investing-related fees, and any cash-balance condition tied to brokerage access.

- 25 points: Investing access. Verify what you can invest in, when access starts, and whether thresholds or upgrades apply.

- 20 points: Investment lineup quality. Check whether the options are actually usable for your plan, not just numerous.

- 10 points: Cash-management workflow. Verify recurring contribution and sweep capabilities if you rely on automation.

- 10 points: Contribution and reimbursement operations. Confirm clear contribution history and a clean reimbursement record trail.

- 5 points: Tax-record handling. Confirm the records and forms you need to report HSA activity on Form 8889.

Step 2. Compare finalists using verification fields, not static claims#

HSAs are portable, so switching is possible, but it still creates work. Confirm current policy before you build a large balance.

| Provider or finalist | Confirm current posted fees | Confirm investing access | Confirm transfer and portability workflow | Usually a better fit when |

|---|---|---|---|---|

| Fidelity | Verify current disclosures, including any investing or cash-balance conditions | Verify available vehicles, minimums, and account structure | Verify transfer steps, forms, and whether full or partial moves are supported | You confirm current terms and workflow match your priorities |

| Lively | Pricing page currently lists $0 monthly maintenance, opening, and closing fees; verify current policy | Lively states broad Schwab access; pricing currently states optional Schwab brokerage access is $24 annual fee or $3,000 minimum cash balance; verify current policy | Verify current transfer process, required forms, and how assets move | You want automation features and the current Schwab terms fit your workflow |

| Any other provider | Verify current disclosures line by line | Verify available vehicles, thresholds, and timing | Verify portability rules before building a large balance | It clears the same standards on cost, access, and operations |

If you are deciding between Fidelity and Lively, run the same checks on both. Add any other provider that meets the same standard.

Step 3. Validate operating details before committing#

The account establishment date is not a minor detail. Only expenses incurred after you actually establish the HSA are qualified for reimbursement.

For reimbursements, keep records that show distributions were used for qualified medical expenses. In practice, that means keeping receipts, invoices, proof of payment, and a simple reimbursement log. Treat investment risk plainly too. Investment balances can carry market risk and are not FDIC-insured.

Step 4. Run a self-funding operations checklist#

Once the provider passes your screen, make sure the day-to-day mechanics work before you rely on the account:

- Link your funding account. Confirm initial transfers settle correctly.

- Schedule contributions. Enable recurring transfers if they fit your cash flow. If you plan to use sweeps, verify the live setting first.

- Document each contribution. Save confirmations and statements in one place.

- Handle reimbursements with evidence. Reimburse only post-establishment qualified expenses and keep supporting records with each transaction.

- Capture tax reporting records. Keep contribution and distribution records, and file Form 8889 to report HSA activity.

If you want a broader refresher on account rules before choosing a custodian, see A Guide to Health Savings Accounts (HSAs).

Deploying Your HSA as a Strategic Asset#

Use your HSA as two buckets: near-term medical cash and long-term invested assets. That split keeps you flexible without losing sight of the rules that make the account valuable.

Step 1. Split the account into medical cash and long-term investments#

Do not invest the full balance by default. Keep enough cash in the HSA for likely near-term out-of-pocket costs, then invest the rest.

That split matters because HSA treatment depends on qualified medical expenses and documentation. Under IRS rules, qualified expenses generally follow the medical and dental deduction standard and can include expenses for you, your spouse, or your dependent at the time incurred. They also must be incurred after the HSA was established. Keep your HSA establishment date in your records folder.

Step 2. Run a pre-payment checklist every time#

Before you pay or reimburse from the HSA, confirm all five points below. This is the simplest way to avoid turning a clean reimbursement into a recordkeeping problem later.

- The expense fits the IRS medical and dental standard.

- The expense was incurred after your HSA was established.

- The expense was not already paid or reimbursed from another source.

- Your file includes supporting records such as a receipt or invoice, proof of payment, and the date of service.

- Your payment trail is complete from the original invoice through the settled amount.

Deferred reimbursement into later tax years can be allowed for qualified expenses incurred in the current year, as long as the expense was incurred after the HSA was established and your records are complete.

Step 3. Choose pay-now vs reimburse-later based on cash flow#

The right choice depends less on theory and more on what protects your cash position without weakening your records. Use the HSA now when the expense is qualified and paying out of pocket would strain your cash buffer, force debt, or require selling investments at the wrong time.

Pay out of pocket when the bill is manageable, you want to keep more of the HSA invested, and you can maintain a clean reimbursement file for later.

Step 4. Compare withdrawal types before retirement planning decisions#

The core question is whether the withdrawal is qualified, not just your age. Before you file or lock in long-term assumptions, verify the current rule text.

| Withdrawal scenario | Tax and penalty treatment | What to verify |

|---|---|---|

| Qualified medical expense, after HSA establishment | Verify current rule. | Meets IRS medical and dental standard; for you, spouse, or dependent at time incurred; not reimbursed elsewhere |

| Non-qualified withdrawal before age 65 | Generally treated as taxable income; additional 20% tax applies unless an exception applies | Verify current rule; check death or disability exceptions if relevant |

| Non-qualified withdrawal at or after age 65 | Age 65 is an exception to the additional 20% tax; verify current income-tax rule before making IRA-style comparisons | Confirm current treatment before IRA-style comparisons |

| Qualified medical expense at or after age 65 | Verify current rule. | The same qualification and documentation standards apply |

Step 5. Sequence HSA and Solo 401(k) contributions by constraints#

A one-participant 401(k) follows standard 401(k) rules, so the practical choice comes down to contribution room, expected healthcare spending, and tax planning.

For 2026:

- HSA limit: $4,400 (self-only) or $8,750 (family), plus $1,000 catch-up at age 55+.

- 401(k) employee elective-deferral limit: $24,500.

Use this as a planning sequence to test, not a universal rule:

- Fund enough HSA cash for expected near-term qualified medical costs.

- If cash flow is stable and records are strong, consider maximizing HSA room to preserve deferred reimbursement flexibility.

- Allocate additional savings to 401(k) when your goal is higher current-year retirement deferral beyond the HSA cap.

Keep the operating cadence simple: contribute on schedule, invest only above your medical cash floor, document each qualified expense when it happens, and review allocation regularly. If you cannot match a distribution to a dated, complete expense file, do not treat it as qualified.

For a step-by-step walkthrough, see How to Choose a Beneficiary for Your Life Insurance and Retirement Accounts.

Your HSA: From Anxiety to Asset#

Your HSA becomes an asset only when you use it inside the rules: confirm monthly eligibility before contributing, document expenses before reimbursing, and know when tax-free treatment applies versus when tax still applies. Think of the account in three practical uses:

- Global qualified medical spending: you can reimburse qualified medical expenses incurred after the HSA was established, including for U.S. taxpayers living abroad where IRS rules are generally the same, but each expense still must meet qualified-expense rules for you, your spouse, or a dependent.

- Retirement healthcare reserve: you can leave funds invested for long-term medical costs, with tax-free earnings and tax-free qualified medical distributions.

- Post-eligibility flexibility: even after you are no longer eligible to contribute, you can still take distributions under the normal distribution rules.

| Asset outcome | Primary use | Tax treatment | Key risk if misused | Simple decision rule |

|---|---|---|---|---|

| Global qualified medical spending | Reimburse qualified medical costs incurred after HSA establishment | Not taxed when used for qualified medical expenses | Poor records or nonqualified expenses can make distributions taxable | Reimburse only when you can match the receipt, payment proof, and service date |

| Retirement healthcare reserve | Keep balances invested for future medical needs | Earnings are tax free; qualified medical distributions are not taxed | Invested balances may require a sale before cash is available | Keep near-term reimbursement cash uninvested if your provider requires share sales first |

| Post-eligibility flexibility | Use HSA funds after contribution eligibility ends | Nonqualified distributions are generally taxable; additional 20% tax generally applies unless an exception applies, including age 65 | Confusing penalty-free with tax-free on nonmedical withdrawals | After 65, expect income tax on nonmedical withdrawals even when the additional 20% tax no longer applies |

Before you rely on this strategy, verify your baseline. For each month you count, confirm HDHP coverage on the first day of the month, no disqualifying coverage, no Medicare enrollment, and that you are not claimable as a dependent. For 2026, confirm your plan still qualifies as an HDHP, with a minimum deductible of $1,700 self-only / $3,400 family and a maximum out-of-pocket limit of $8,500 self-only / $17,000 family.

If Medicare enrollment is later backdated, contributions made during the retroactive coverage period are excess contributions.

Keep your file audit-ready. Save receipts, invoices, payment proof, and account records showing the HSA existed before the expense and that amounts were not double-counted elsewhere. If you took HSA distributions, file Form 8889 even if you have no taxable income.

Action checklist:

- Verify now: month-by-month eligibility, HDHP qualification, Medicare status, and current-year contribution limits

- Document ongoing: receipts, proof of payment, contribution records, and any investment sale-to-cash timing before reimbursement

- Review annually: total contributions against 2026 limits ($4,400 self-only / $8,750 family), distribution support, and Form 8889 completeness

You might also find this useful: How to Invest in Farmland. If you want cleaner payment operations and tax-ready records where applicable while you execute this plan, review Gruv's freelancer workflow: See Merchant of Record for freelancers.

Frequently Asked Questions

Can you contribute to an HSA while living abroad?

This grounding pack does not establish HSA eligibility rules. What it does confirm is that FEIE is not automatic: you must be a qualifying individual with foreign earned income and file a U.S. return reporting that income. Form 2555 also includes a foreign tax credit or deduction checkpoint. FEIE calculations depend on timing, part-year qualification requires proration, and the 2026 annual maximum is $132,900 before required adjustments; if you claim a foreign housing exclusion, calculate that first.

Do you need to report an HSA on FBAR or FATCA?

Confirm FBAR and FATCA treatment for HSAs with a qualified tax adviser.

How should you choose an HSA provider if you are self-employed?

Confirm selection criteria for an HSA provider with the relevant authority or a qualified adviser.

How do you fund an HSA when you are self-employed?

Confirm HSA funding workflows for self-employed filers with the relevant authority or a qualified adviser.

Can you use HSA money for medical expenses incurred abroad?

Confirm HSA qualified-expense rules for expenses incurred abroad with the relevant authority or a qualified adviser.

HSA or Solo 401(k): which should you fund first?

Confirm current-year contribution limits and sequencing rules for HSA versus Solo 401(k) contributions with the relevant authority or a qualified adviser.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

HSA Strategy for Self-Employed Global Professionals Abroad and in Retirement

This guide treats an **HSA**, or health savings account, as a three-part asset with current IRS rules setting the edges. In practice, a health savings account can serve as your medical reserve, a cross-border buffer, and a long-term tax-favored account for future qualified medical expenses.

Tax Implications for an Australian Resident Owning a US LLC

There is no one-size-fits-all shortcut for US LLC tax decisions across Australia and the United States. Setting up a US Limited Liability Company (LLC) is one step; getting the tax treatment right in both systems is where risk starts. If you are handling **australian owning us llc tax** decisions, treat this as a classification and documentation problem first, not a shortcut hunt. If you run a business of one, your job is to pick the defensible path and keep the paperwork tight.