Quick Answer

Invest in farmland by first matching the vehicle to your liquidity needs, desired control, and willingness to handle admin. Publicly traded REITs and ETFs are usually the simplest for liquidity and low workload, platform deals offer deal-level selection without operating land, and direct ownership offers the most control but requires the most diligence, lease oversight, and ongoing management.

Phase 1: The Strategic Assessment - Which Farmland Vehicle Fits Your Business-of-One?#

Choose the vehicle before the property. The right path depends on your liquidity needs, how much control you want, and how much admin work you are willing to carry. If you need easy exits and very little operational burden, direct ownership is often not the right starting point.

Step 1. Audit your real constraints#

Start with your actual limits, not with a listing or a pitch deck. This quick self-check will narrow the field fast:

- Can you leave this capital tied up for years?

- Do you want property-level control or portfolio exposure?

- Will you review offering documents and operator reporting yourself?

- Can you handle legal, tax, and on-the-ground follow-up when needed?

If direct ownership is on your shortlist, reality-check the budget early. USDA reports a 2025 average farm real-estate value of $4,350 per acre, so 100 acres is about $435,000 before financing, closing costs, diligence, and improvements. Treat that as a planning screen, not a valuation rule.

Step 2. Compare vehicles by the frictions you will actually feel#

Most mistakes here come from focusing on return stories while ignoring the day-to-day frictions. Compare the vehicles on the parts you will actually live with after you invest, and keep these distinctions in view from the start:

| Vehicle | Control | Liquidity | Fee visibility | Tax complexity | Admin workload |

|---|---|---|---|---|---|

| Direct ownership | High | Typically lower than exchange-traded vehicles | Varies with financing, diligence, and carrying costs | Case-specific | Higher; property diligence is checklist-driven |

| Crowdfunding platforms | Usually investor-level rather than operator-level control | Often constrained (resale limits can apply) | Varies by offering; document review is essential | Case-specific | Depends on offering and reporting |

| Private funds | Low; adviser generally controls investment decisions | Often low (private placements are highly illiquid) | Can be harder to evaluate quickly | Case-specific | Depends on fund terms and reporting |

| Publicly traded REITs | None at asset level | High; generally easier to buy/sell on exchanges | Varies; review public documents | Case-specific | Lower than property-level ownership |

| ETFs | None at asset level | High during market hours | Varies; review fund documents | Case-specific | Lower than property-level ownership |

- Not all REITs are interchangeable. Publicly traded REITs are generally easier to trade, while non-traded REITs are illiquid; SEC guidance notes liquidity events may take more than 10 years, and upfront fees can be as high as 15% of offering price.

- If an offering uses Regulation Crowdfunding, transactions must go through an SEC-registered intermediary, offerings are capped at $5 million in a 12-month period, and purchased securities generally cannot be resold for one year.

- Private offerings may require accredited-investor status; one SEC standard is net worth of more than $1 million, excluding your primary residence.

Step 3. Match yourself to a likely path#

At this point, look for fit, not optionality. Direct ownership fits best when control is the priority and you can absorb the work that comes with it. It suits you if you want property-level decision authority. It is a poor fit if you need liquidity or want minimal diligence, because farm evaluation is often checklist-driven.

| Path | Fits when | Poor fit when |

|---|---|---|

| Direct ownership | Control is the priority and you can absorb the work that comes with it; you want property-level decision authority | You need liquidity or want minimal diligence |

| Crowdfunding-style offerings | You want deal-level selection without operating the land yourself; you want to choose specific opportunities but stay out of day-to-day operations | You assume "passive" means no paperwork, no monitoring, or no follow-up |

| Publicly traded REITs and ETFs | Liquidity and low admin matter most; you want market access and simpler portfolio handling | Your goal is property-level control, or you are treating non-traded REITs as if they had stock-like liquidity |

Crowdfunding-style offerings work when you want deal-level selection without operating the land yourself. They can make sense if you want to choose specific opportunities but stay out of day-to-day operations. They are a weak fit if you hear "passive" and assume that means no paperwork, no monitoring, or no follow-up.

Publicly traded REITs and ETFs are usually the most practical route if liquidity and low admin matter most. They fit when you want market access and simpler portfolio handling. They do not fit if your goal is property-level control, or if you are treating non-traded REITs as if they had stock-like liquidity. Pick your likely vehicle now, but keep the choice provisional until Phase 2 confirms the diligence and compliance side.

If you want a deeper dive, read Japan Digital Nomad Visa: A Guide to the New 2025 Program.

Phase 2: The Deep Dive - A Professional-Grade Due Diligence & Compliance Checklist#

Do not commit capital until this checklist is complete. This is the phase that turns a good idea into a controlled decision, with clear points where you either proceed, renegotiate, or walk away.

Due diligence is the legal, structural, and financial review you run before and after an offer so issues surface before closing. Skipping these fundamentals increases execution risk, so keep a dated diligence file from day one with records, deal documents, notes, and your decision log.

Verify legal, structural, and financial exposure first#

Start here because unresolved legal, structural, or financial issues can change deal economics before you compare returns. Work through this pre-commit checklist:

- Confirm parcel identity and ownership records, including the legal description and county records.

- Review GIS maps, subdivision records, and county data to verify property details before committing.

- Evaluate assessed values and comps to pressure-test pricing.

- Identify environmental flags and access issues early, and document what must be resolved before closing.

- Assign ownership of open diligence items and keep decision points documented.

Proceed only when you can clearly state the key risks, what is resolved, and which findings would trigger renegotiation or a walk-away decision.

Interrogate the platform and sponsor, not just the farm#

In a platform deal, evaluate operator governance and execution risk alongside the land. Ask these questions in writing:

| Area | Ask in writing |

|---|---|

| Decision-making | Who makes acquisition and asset-management decisions, and what is their relevant operating track record? |

| Fees | What fees apply across sourcing, management, administration, financing, and exit? |

| Investor rights | What investor rights exist in practice, and which decisions can be made without investor approval? |

| Exit path | What is the stated exit path, and what could delay it? |

| Reporting | What reporting cadence and operating detail will you receive beyond headline performance? |

Use a simple standard: if you cannot explain the fees, decision rights, and reporting mechanics in plain language, you are not ready to commit.

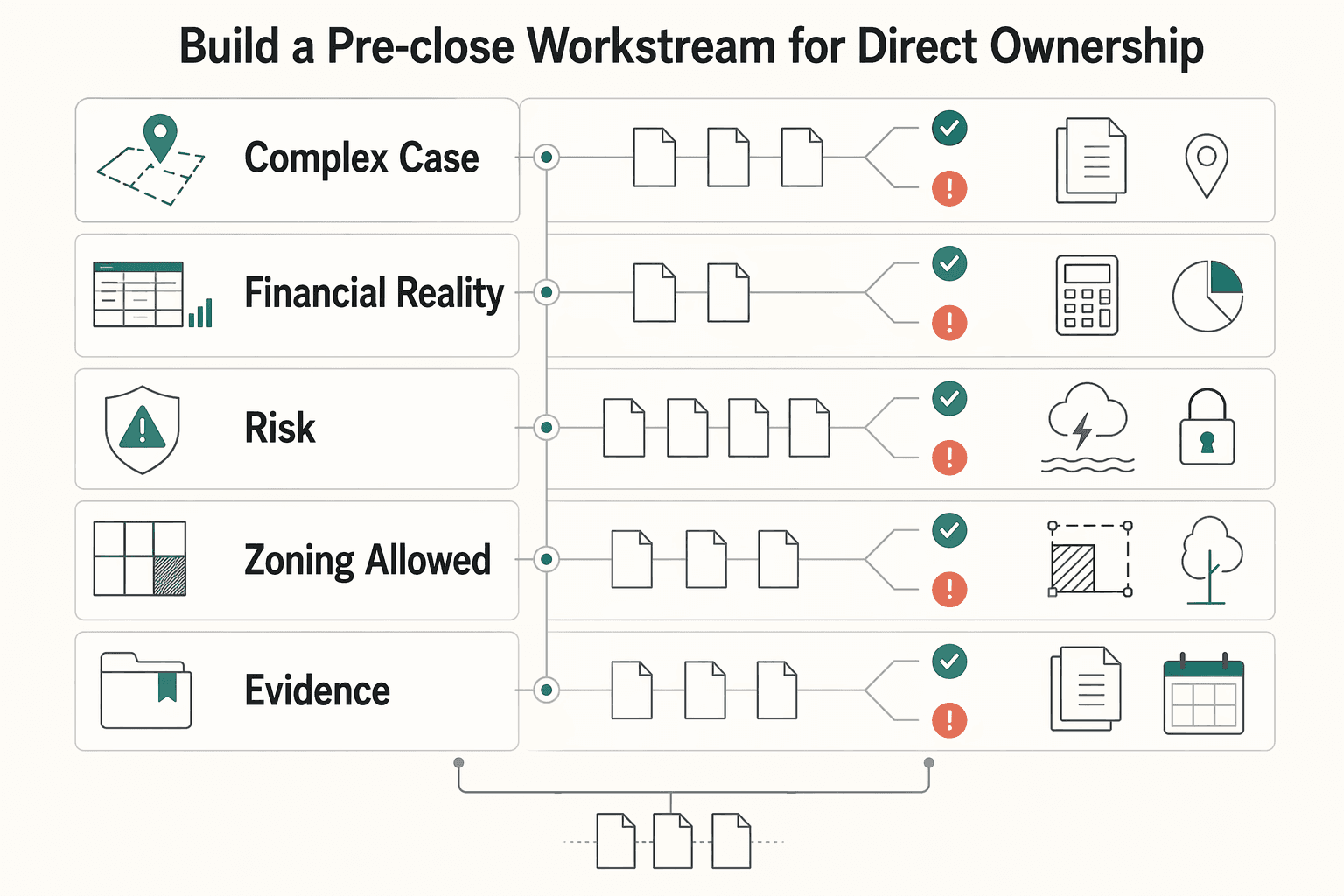

Build a pre-close workstream for direct ownership#

For direct ownership, treat diligence as a structured pre-close workstream. The goal is not to gather paper for its own sake. It is to surface any issue that could change price, terms, or your willingness to close. Build the file around five checks:

| Check | What to verify | Note |

|---|---|---|

| Legal rights and parcel identity | Ownership records, legal description, subdivision details, GIS mapping, and county data | Before you rely on the listing |

| Financial reality check | Assessed values and comps | Before you make or finalize an offer |

| Risk flags | Environmental flags and access issues | Before closing |

| Zoning and allowed use | Permitted uses with the relevant local authority | Affect what you can do and can influence future value |

| Documentation standard | Complete close-ready file | Unresolved issues are explicit and decision-ready |

If your file still shows unresolved risk around ownership, access, use constraints, or major risk flags, renegotiate terms or walk away. Finish this phase before you shift into ongoing asset management. Related: A Freelancer's Guide to Angel Investing and Venture Capital.

Before you lock capital into farmland, you can run invoicing and payout costs through the Payment Fee Comparison tool as part of your planning.

Phase 3: The Operational Plan - Managing the Asset#

After closing, the job is to prevent drift. Run each lane with clear owners, a fixed review rhythm, and pre-agreed escalation triggers.

Run direct ownership with lease governance#

For direct ownership, the lease is your primary control document, not just closing paperwork. A farm lease is a legal instrument, and a written lease gives you an auditable record of what was actually agreed. Use this direct-ownership checklist before and during operations:

- Confirm your signed lease file is complete and usable: parcel details, term, payment mechanics, reporting dates, and notice terms.

- Select an operator or manager who agrees to written controls, defined reporting duties, and clear issue escalation.

- Set approval rights in writing for lease amendments, major non-budgeted capital work, and changes in permitted use.

- Require an annual operator report; treat it as a communication control, not admin overhead.

- Standardize the reporting package so remittance detail, variance explanations, and key risk notes are documented consistently.

- Escalate early on drift: late or incomplete remittances, missing reports, repeated requests to change economics mid-season, or unexplained gaps between reported activity and received records.

Once the lease file is solid, choose the lease structure based on who carries risk and how much operational burden you want to keep:

| Lease type | Who carries production risk | Cash-flow predictability for you | Reporting burden for you | Typical conflict points |

|---|---|---|---|---|

| Cash rent lease | Tenant typically carries production, price, and cost volatility | High | Low to moderate | Rent timing, maintenance scope, land-use changes |

| Crop share lease | You and tenant share risk and upside | Low to moderate | Higher | Input-cost splits, revenue allocation, record quality, settlement timing |

| Flexible or hybrid rent | Risk and return are shared by formula | Moderate | Moderate to high | Formula interpretation, benchmark disputes, yield/price documentation |

Oversee crowdfunding sponsors with manager-level discipline#

In crowdfunding deals, the real operating task is sponsor oversight. You are not just waiting for distributions. These investments can lose some or all principal, so your control points are update quality, cash reconciliation, and document flow. Run this sponsor-oversight checklist:

- Define communication standards up front: update cadence, accountable contact, and official notice channel.

- Quality-check each update: what changed operationally, impact on investor outcomes, distribution status, and delay risks.

- Reconcile every distribution: sponsor notice, amount received, and portal/investor statement.

- Keep your own ledger of distributions, notices, and unresolved items.

- Confirm tax-document workflow before year-end and assign follow-up ownership; some structures may use Schedule K-1, but not all do.

- If the deal is Regulation Crowdfunding, verify it is through an SEC-registered intermediary.

- For Reg CF deals, account for the general one-year resale restriction and verify issuer reporting expectations, including Form C-AR timing, against current deal documents.

- Verify the exemption type for each deal; do not assume every farmland platform offering is Reg CF.

Review REITs and ETFs inside portfolio policy#

For REITs and ETFs, keep the process simple. Review them inside your broader allocation policy, not as stand-alone bets. This path cuts property-management workload, but concentration and liquidity risk still matter. Use this repeatable review routine at each portfolio check:

- Confirm position role: does it still match your intended use (income, diversification, inflation hedge, etc.)?

- Check concentration: has real-estate or farmland-adjacent exposure become oversized?

- Reset cash-flow expectations: REIT distribution requirements (such as distributing at least 90% of taxable income) are not a guarantee of stable spendable cash flow.

- Review ETF fit using NAV and holdings overlap.

- Trigger rebalance when weight drifts outside target, overlap rises, or the holding's role changes from diversifier to concentrated bet.

- If using non-traded REITs, treat the position as illiquid capital and size accordingly; exits may take more than 10 years.

You might also find this useful: Tax Implications for a UK Resident Owning a US LLC.

Your Final Decision: An Empowered Choice#

Proceed only when all three are true: the vehicle fits your liquidity and control needs, your risk review is complete, and you can handle the ongoing oversight. If one is unresolved, wait.

| Path | Control | Liquidity | Effort | Oversight burden |

|---|---|---|---|---|

| Publicly traded REIT | Low | Usually highest | Low | Low |

| Regulation Crowdfunding deal or private placement | Medium | Usually limited | Low to moderate | Low to moderate |

| Direct ownership | High | Usually very limited | High | High |

Decision checklist before you commit capital#

- Vehicle fit: Separate publicly traded REITs from non-traded REITs, because the liquidity risk is different. For platform offerings, confirm whether the deal is Regulation Crowdfunding or a private placement. Crowdfunding securities generally cannot be resold for 1 year, and private placements should be treated as highly illiquid. For direct purchases, do not use the $4,350 per acre 2025 U.S. average as local pricing; regional values vary widely.

- Diligence completeness: Confirm who operates the farm, how landlord and tenant decisions are split, what lockup or redemption rules apply, and which documents define your rights. If it is a Regulation Crowdfunding deal, verify the transaction is through an SEC-registered intermediary.

- Operating capacity: Be honest about your ability to monitor statements, operator reporting, lease terms, and follow-through tasks after you invest.

Go, wait, or pass#

- Go: Your vehicle fit is clear, your diligence file is complete, and you have the time and process to oversee the investment.

- Wait: The path may fit, but you still need to confirm local valuation, operator quality, or exit terms.

- Pass: You need ready liquidity but are considering a non-traded or private structure, or you want direct ownership without the capacity for lease, operator, and compliance follow-through.

Before you invest, write down your assumptions, document why you chose this path over the other two, and set a monitoring cadence. For a step-by-step walkthrough, see How to Invest Your HSA Funds.

As you finalize your go-or-wait decision, tighten the rest of your money workflow with Gruv finance tools. That can help reduce avoidable payment friction.

Frequently Asked Questions

1. What is the easiest way to invest in farmland?

The easiest route depends on what you need most. Publicly traded farmland REITs and ETFs are usually the simplest if liquidity and low admin matter most, while platform deals, agricultural land funds, and direct ownership involve different tradeoffs. Compare lockup and exit terms before you commit.

2. How much money do you need to start?

There is no universal minimum, so verify the entry requirement for the specific vehicle. The article cites platform deal examples at $10,000 to $15,000 and many private farmland funds at $1 million minimum, often with 10-year lockups. Direct ownership depends on the property and market, and REIT or ETF minimums depend on current brokerage and share-price requirements.

3. What are the hidden risks?

The main risks are often buried in documents rather than truly hidden. Review production and market volatility, debt-related pressure, regulatory-change risk, and lockup terms. If key terms are unclear, pause before investing and consider professional financial advice.

4. Is farmland a good investment for expats?

Treat this as compliance-first, not return-first. The provided grounding does not establish expat-specific tax treatment for farmland income or FEIE applicability. Before investing, have a qualified cross-border adviser review the setup and filing obligations in each jurisdiction.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ag.purdue.edu/commercialag/home/paer-article/is-farmland-a...trusted

- ers.usda.gov/topics/farm-economy/land-use-land-value-tenu...trusted

- ers.usda.gov/topics/farm-economy/land-use-land-value-tenu...trusted

- extension.iastate.edu/agdm/wholefarm/html/c2-20.htmltrusted

- extension.psu.edu/farmland-assessment-checklisttrusted

- investor.gov/introduction-investing/general-resources/new...trusted

- investor.gov/introduction-investing/general-resources/new...trusted

- irs.gov/pub/irs-pdf/i1065sk1.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

A Freelancer's Guide to Angel Investing and Venture Capital

**Build a decision system that protects your operating cash first, then treat angel investing as an optional use of true surplus.** If you are considering angel investing as part of broader wealth building, you need controls that keep "startup investing" from quietly raiding rent, taxes, or payroll. Knowledge feels productive, but constraints keep you solvent. As the CEO of a business-of-one, your job is to protect the operating cash that keeps the machine running.

Tax Implications for a UK Resident Owning a US LLC

When people search **uk resident owning us llc tax**, they often start with the wrong question. You do not win by chasing a clever position. You win by running a compliant system that can handle the way the US and UK classify LLC income differently, with records you can defend.