Quick Answer

To invest in ETFs as a German resident, first choose a broker that fits your tax status, offers clear annual tax reporting, and provides the required KID for the ETF you want. Then decide whether you want source-level German tax handling, build around one broad ETF core or a small ETF set, and use a Sparplan if you want automated recurring purchases.

Why ETFs are the Bedrock of a Global Professional's Portfolio in Germany#

If you want a portfolio you can actually maintain, use broad ETFs as your default core. For many Germany-based professionals, broad ETFs take less ongoing effort than building a single-stock portfolio while still giving you built-in diversification and often lower fee drag than higher-cost active funds.

An ETF is a fund traded on an exchange, and it usually tracks an index instead of relying on a manager to pick holdings. A Depot is your securities custody and administration account at a bank or broker. An ETF-Sparplan is an automated recurring ETF purchase for a fixed amount and interval. Steuereinfach is market shorthand, not a formal legal status here. In practice, it usually means a setup where German capital-income tax handling is automated at source and your Freistellungsauftrag can be applied.

| Option | Maintenance burden | Diversification | Fee drag | Compliance/admin workload |

|---|---|---|---|---|

| Broad ETFs | Low: one or a few funds can cover broad markets | Built in across many holdings | Usually lower; ETFs are typically bought on exchange without front-end loads | Usually simpler when tax handling is done at source and allowance orders are integrated |

| Single stocks | High: you research, monitor, and rebalance yourself | Lower unless you build a larger basket | Varies, with more investor decisions and higher concentration risk than broad ETFs | Can involve more manual tracking of transactions and outcomes |

| Active funds | Medium to high: manager-driven portfolio changes | Varies by mandate | Higher costs matter because higher-cost funds must outperform lower-cost funds just to match net returns; cited UCITS retail costs range from about 0.5% to 2% depending on fund type | Product, fee, and documentation checks matter more |

That is why ETFs are the practical default for many residents. It is not because other options are always wrong, but because the operating burden is usually lower.

Before you pick a broker app, pick your tax workflow. Germany's quoted withholding structure on capital income is 25% plus a 5.5% solidarity surcharge component. A Freistellungsauftrag can apply the Sparer-Pauschbetrag at source, EUR 1,000 for singles and EUR 2,000 for jointly assessed partners. If your setup supports that flow clearly, ongoing admin is usually lighter.

Choose a steuereinfach-style route if your priority is lower admin and source-level handling. Consider a non-German broker route only if you need specific access or eligibility and can accept more reconciliation work. This can include cases where income falls under ELSTER's KAP-INV path for investment income not subject to domestic withholding.

Before you fund anything, make two checks:

- Confirm the broker provides clear annual tax reporting, including dividends, sales, and withheld tax details.

- Confirm the products include the required KID (Key Information Document), which is limited to 3 pages under PRIIPs rules.

If year-specific tax treatment details are unclear, pause and verify before you execute. Before you move on to broker selection, make four decisions up front:

- Decide whether you want source-level German tax handling or a more manual filing path.

- Decide whether you will start with one broad ETF core or a small ETF set.

- List the broker documents you require upfront: tax statement format, Freistellungsauftrag support, and KID availability.

- Set your planned contribution rhythm so you can evaluate Sparplan support in the next step.

With that core setup in place, the next job is choosing a broker that does not create avoidable tax or reporting work. Related: Tax Implications for an Australian Resident Owning a US LLC.

The Global Professional's Broker Framework#

Broker choice here is a compliance filter, not a price contest. Pass the legal, tax, reporting, and exit checks first, then compare fees.

Pick your path before you compare brokers#

Decide which path applies to you, then use that checklist only:

- Germany-resident, non-US investor: prioritize German tax handling and local document quality.

- US person in Germany: prioritize US-person acceptance and cross-border reporting outputs first, then local tax handling.

| Criterion | Pass: Germany-resident non-US investor | Pass: US-person investor | Verify before opening |

|---|---|---|---|

| Regulatory status | Broker is authorized or notified for the service you will use | Same | Confirm in BaFin's company database |

| Tax handling model | Broker can explain that capital-income tax is withheld and remitted at source (Abgeltungsteuer model) | Helpful, but not sufficient on its own | Ask for the exact dividend and sale tax workflow in writing |

| Product eligibility docs | Required KID/BIB is available before you can contract for in-scope retail products | Same | Open target product pages and confirm KID/BIB access before ordering |

| Reporting quality | Annual tax-certificate process is clear and certificates are issued by 30 June of the following year | Statements and exports support cross-border filing | Request sample statements or a reporting index before opening |

| Transfer-out process | Broker can process securities transfer-out in line with the 3-week benchmark, or provide an interim delay notice | Same | Ask for transfer-out steps and delay communication policy in writing |

| Support responsiveness | Support gives clear, specific written answers | Critical for US-person edge cases | Send pre-sale compliance questions and evaluate the written reply |

Run the non-US path#

For non-US residents, weak tax handling is a hard stop. If the broker cannot clearly explain source withholding and annual tax-certificate delivery, assume more manual filing work. Also confirm your target ETF has a KID or BIB where required for retail access.

Run the US-person path#

If you are a U.S. person, confirm account acceptance before you start onboarding. Foreign institutions may request citizenship details at account opening, so get that confirmed in writing early. Before you fund the account, require these outputs:

| Check | Threshold or requirement | Action |

|---|---|---|

| Account acceptance | Confirm account acceptance before onboarding; foreign institutions may request citizenship details at account opening | Get this confirmed in writing early |

| Year-end records | Year-end statements and records you can use for tax reporting | Require these outputs before you fund the account |

| Export fields | Account identifiers plus institution name, address, and account type in exports | Require these outputs before you fund the account |

| Account value history | History that lets you reconstruct maximum annual account value for FBAR reporting | Require these outputs before you fund the account |

| FBAR | Can apply once aggregate foreign accounts exceed $10,000 at any point in the year | Treat as a separate check from Form 8938 |

| Form 8938 | $200,000 / $300,000 for single or married filing separately, and $400,000 / $600,000 for joint filers living outside the US | Treat as a separate check from FBAR |

| PFIC exposure | If a product path could create PFIC exposure | Pause and verify before buying |

Treat FBAR and Form 8938 as separate checks. FBAR can apply once aggregate foreign accounts exceed $10,000 at any point in the year. Form 8938 thresholds for individuals living outside the US differ by filing status: $200,000 / $300,000 for single or married filing separately, and $400,000 / $600,000 for joint filers. If a product path could create PFIC exposure, pause and verify before buying.

Once the account path is clear, make sure US and German reporting rules do not collide. You might also find this useful: The Best Personal Finance Apps for German Residents.

The Compliance Gauntlet: Navigating US-German Tax#

If you are a U.S. person, this section applies in full. If you are a German tax resident who is not a U.S. person, the German tax-document terms still matter, but PFIC, Form 8621, FBAR, Form 8938, and Form 1116 may not apply in the same way.

Apply the U.S.-person gate first#

Start with status, not product. U.S. citizens and residents are taxed on worldwide income, including income from accounts in Germany. Your ETF account is therefore both an investing account and a U.S. reporting and tax input. Use one operating rule: if you cannot verify a fund's domicile and structure before buying, pause.

Screen PFIC exposure before you buy#

For U.S. persons, PFIC screening comes before portfolio construction. A foreign corporation can meet PFIC tests when passive income is 75% or more of gross income, or when passive assets are at least 50%.

Do not use shortcuts such as assuming every non-U.S. ETF is PFIC from these facts alone. Verify each target fund's legal structure and domicile, then keep evidence in a product log with ticker, identifier, issuer, and domicile proof. If a holding is PFIC, Form 8621 is filed per PFIC and can multiply across ownership chains.

Build your double-tax relief file as you go#

Treaty relief works in practice only if your records are filing-ready. Track income and withholding throughout the year, then map them to your U.S. return workflow. Track and retain:

- Gross dividends, interest, and realized gains

- German tax withheld, solidarity surcharge, and church-tax withholding if applicable

- Annual tax certificate, year-end statement, dividend notices, and sale confirms

- Any Freistellungsauftrag (FSA) or NVB documentation

For U.S. filing, foreign tax credit claims run through Form 1116 by income category and country, and the credit is limited by formula. If you take a treaty-based position beyond ordinary FTC treatment, ask whether Form 8833 disclosure is required. Keep separate account-reporting checks in view: FBAR has a $10,000 aggregate foreign-account trigger at any point in the year. Form 8938 uses a different threshold test, so keep a note to verify the current threshold before filing.

Decode German tax terms on your broker documents#

Once your holdings pass screening, your broker paperwork becomes the bridge between German withholding and your filing process.

| Term | Why it matters | Action you take |

|---|---|---|

| Abgeltungsteuer / Kapitalertragsteuer | German capital income is generally withheld at 25% plus 5.5% solidarity surcharge; church tax follows the same at-source handling logic. | Reconcile broker-reported withholding to your income records and pass both gross income and tax paid to your preparer. |

| Freistellungsauftrag (FSA) / NVB | Eligible amounts can be excluded from withholding, and institutions report used exemption amounts annually to BZSt. | Keep copies of submitted FSA or NVB records and flag reduced withholding in your tax handoff. |

| Sparer-Pauschbetrag | This affects how much capital income is taxed at source. | Confirm the current-year amount before filing or updating instructions. |

| Vorabpauschale | Taxable deemed investment income can arise even without a cash distribution. | If you hold accumulating funds, capture broker entries and timing notes. For 2026 references: basiszins 3.20% (reference date 2 January 2026), deemed receipt 4 January 2027. |

Year-end compliance checklist#

At year-end, aim for one complete file rather than a scramble across portals and emails. Use this checklist:

| Checklist item | Related detail |

|---|---|

| Annual tax certificate | year-end account statement |

| Dividend notices | sale confirmations |

| ETF inventory | issuer and domicile evidence |

| Record of German withholding | solidarity surcharge, and church tax if shown |

| FSA or NVB records | if used |

| Vorabpauschale entries | if applicable |

| Highest annual account value | for FBAR review |

| Form 8938 | verify the current threshold |

| PFIC review flag | for any holding that may require Form 8621 |

After the reporting path is under control, portfolio design gets much simpler. If you want a deeper dive, read Can Digital Nomads Claim the Home Office Deduction?. Before you lock in your ETF process, sanity-check your foreign-account reporting workflow with the FBAR calculator.

Designing Your Resilient Portfolio#

Your portfolio is usually more resilient when you place assets by spending currency, account tax treatment, and reporting workload, in that order.

Map spending and tax exposure before you pick funds#

Start with liabilities, not products. Ask which currency funds your life, which jurisdiction is likely to tax the income or withdrawals, and which expenses must stay stable in the next few years.

If your medium-term spending is mostly in EUR, anchor your cash reserve and most of your stabilizing sleeve to EUR needs. If you expect meaningful USD liabilities, keep a USD sleeve for those liabilities instead of leaving the mismatch unmanaged. This matters most in the defensive part of the portfolio, where stability is the point.

Asset location is a tax decision as much as an investment decision, because account type changes treatment. In Germany, capital income under EStG §32d is generally taxed at 25%, and a Freistellungsauftrag can apply the Sparer-Pauschbetrag at withholding. The figures used here are EUR 1,000 individual and EUR 2,000 jointly assessed. Use this placement note in your worksheet: [Verify current tax handling for your account type, fund structure, and any cross-border credit interaction before final placement.]

Choose a compliant structure for your status#

A simple structure helps only if it is actually usable in your legal and tax context.

If you are a U.S. person, keep the three-fund concept on a U.S.-screened track: U.S. total stock, international total stock, and total bond market. The priority is not elegance. It is staying within holdings you already screened for domicile and PFIC exposure.

If you are not a U.S. person, do not copy U.S.-centric fund lists by default. For German retail execution, confirm a PRIIPs key information document, the Basisinformationsblatt, is available before you transact. Before your first buy, verify domicile, legal structure, and KID availability, then keep the supporting broker or PDF records.

| Sleeve | Role in portfolio | Main risk contribution | Rebalance trigger | Implementation notes |

|---|---|---|---|---|

| Global equities | Long-term growth | Largest drawdowns and equity volatility | Weight drifts outside your chosen band, or new cash materially changes mix | U.S. persons: use only pre-screened compliant holdings. Non-U.S. residents: confirm KID availability and local tax handling. |

| Bonds or defensive fixed income | Stability and spending support | Interest-rate risk and possible currency mismatch | Stabilizer no longer matches planned spending currency | Align this sleeve with the currency of near- and medium-term liabilities where possible. |

| Cash reserve | Short-term obligations and tax debits | Inflation drag and low return | Refill after tax payments, large purchases, or income shocks | Hold enough for expected tax debits, planned draws, and emergency expenses. |

Run a strict personal-business firewall#

If you run a business, mixed account flows create avoidable tax and documentation problems. Keep investment funding on the personal side only, with a traceable transfer trail from business to personal accounts. Use these controls:

| Control | Detail |

|---|---|

| Separate bank accounts | Keep business revenue and personal spending in separate bank accounts, even where a separate business account is not always legally required |

| Consistent transfer method | Move funds from business to personal through one consistent method and memo format, for example owner draw or salary-equivalent, based on your setup |

| Broker funding source | Fund your broker only from your personal account, not directly from client receipts |

| Record storage | Store transfer confirmations, monthly statements, annual tax certificates, and contribution notes together for at least the general 3-year IRS assessment period, and longer when basis support requires it |

| U.S.-person balance tracking | Track year-end balances and highest annual account values as you go: FBAR and Form 8938 are separate filing regimes, and foreign brokerage accounts can be in scope once foreign accounts exceed $10,000 in aggregate for FBAR |

A common failure mode is mixed account flows. They blur source-of-funds evidence, slow tax prep, and turn routine compliance checks into reconstruction work.

The questions below tend to come up once broker setup, tax status, and portfolio structure meet real life. We covered related ground in How to Invest Your HSA Funds.

Conclusion: Invest with Confidence, Not Anxiety#

Many costly surprises are avoidable before you place the order. If you want fewer surprises when you invest in ETFs in Germany, apply three rules in order: broker fit first, filing rules second, portfolio discipline third.

Put broker fit before fees#

Choose the broker that matches your real profile, not just the cheapest headline pricing. Confirm it accepts your citizenship and tax status, and keep onboarding evidence if FATCA questions come up.

Then confirm documentation quality: annual tax certificates, withholding records, and clear statements. If German capital-income withholding is handled at source for your case, that step is automated by the payer. If you plan to use a Freistellungsauftrag, verify the allowance for the filing year before you rely on it. The draft guidance here uses EUR 1,000 single and EUR 2,000 joint, but recheck for the year you file.

Master the few rules that change your filings#

If you are a U.S. person, FBAR can apply once aggregate foreign accounts exceed $10,000 at any point in the year. The due date is April 15 with an automatic extension to October 15. Form 8938 is separate and can apply at different thresholds, so verify the current trigger for your status.

If investment income was not subject to domestic withholding, check whether KAP-INV applies in ELSTER. Do not assume treaty relief applies automatically when timing or classification is unclear. Verify against the Germany-U.S. treaty documents.

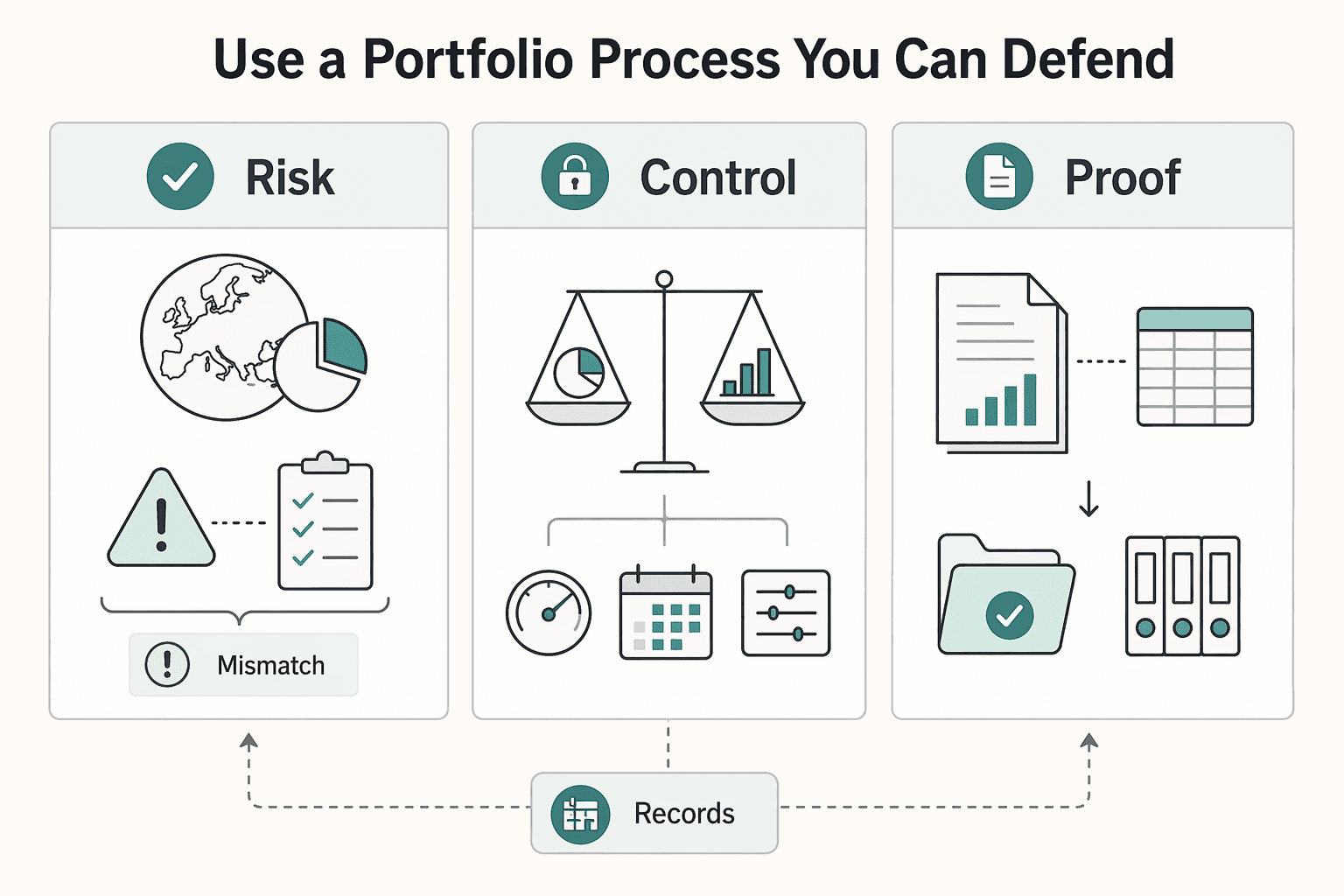

Use a portfolio process you can defend#

Build a portfolio you can explain and maintain over time. Not every ETF fits every investor, and active versus passive alone does not predict returns.

If you are a U.S. person, screen non-U.S. funds for PFIC risk before buying, because PFIC treatment can mean ordinary income treatment plus an interest charge. For cleaner records, keep personal investing cashflow separate from business inflows.

Before your next ETF order, run this quick check:

- Broker fit is confirmed for your profile, with tax statements, withholding records, and onboarding evidence available.

- Reporting records are ready: annual statements, account-balance records, current threshold checks, and any PRIIP KID or fund documents used in your decision.

- Funding records are clear about which money is used for personal investments.

You do not need perfect certainty. You need a repeatable process that controls eligibility, tax handling, and documentation risk before the trade settles.

For a step-by-step walkthrough, see How to Invest in Farmland. Once your investing rules are set, make your cashflow side just as reliable with Gruv for freelancers.

Frequently Asked Questions

Can a US citizen open a brokerage account in Germany?

Sometimes, but only if the broker accepts your status. Some brokers restrict U.S. persons, so confirm eligibility before onboarding and keep the policy text or support reply. Choose the broker that gives you clear compliance records, not just the lowest fees.

How are ETFs taxed in Germany for American expats?

If you live in Germany, capital income is generally taxed through withholding, and a steuereinfach broker usually automates that withholding and remittance. Steuereinfach is market shorthand, not a legal category, so verify treatment for your account and fund type. Keep annual tax documentation and withholding evidence for your U.S. records.

Do I need to report my German brokerage account on FBAR?

If you are a U.S. person, FBAR can apply once aggregate foreign accounts exceed $10,000 at any point in the year. Form 8938 is separate and does not replace FBAR. Track your highest balances and keep statements organized.

How do I avoid double taxation on my investments between the US and Germany?

Your main tool is usually the foreign tax credit for qualifying foreign income taxes. Align German withholding records to the relevant U.S. tax year and keep broker tax documents with your account statements. Get help if timing or classification is unclear.

What is the *Vorabpauschale* and how does it affect US tax returns?

Vorabpauschale is a German pre-determined tax basis that may apply when fund shares rise in value even if no payout was made. Check annual statements for withholding on non-distributing holdings and keep the broker evidence. Escalate if U.S. timing, PFIC, or Form 8621 treatment is involved.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

Tax Implications for an Australian Resident Owning a US LLC

There is no one-size-fits-all shortcut for US LLC tax decisions across Australia and the United States. Setting up a US Limited Liability Company (LLC) is one step; getting the tax treatment right in both systems is where risk starts. If you are handling **australian owning us llc tax** decisions, treat this as a classification and documentation problem first, not a shortcut hunt. If you run a business of one, your job is to pick the defensible path and keep the paperwork tight.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.