Quick Answer

Start by confirming with documents whether your child is actually a U.S. citizen, then check the current-year IRS instructions to see whether filing or reporting is required. For a child born abroad, the safest approach is to separate citizenship status from tax filing, plan the right identifier early, inventory income and foreign accounts, and keep an annual memo and folder so banks, the IRS, or a CPA can follow your decisions.

You don't need a "tax hack" - you need a repeatable compliance playbook#

Treat this as an operations problem. Confirm status, confirm obligations, document the trail, and escalate fast when facts get fuzzy. You are the CEO of a business-of-one, and this is a recurring compliance workflow you want to run on rails instead of rebuilding from scratch every year.

The real risk for an expat family often does not show up as a dramatic tax bill on day one. It shows up as silent non-compliance. You assume your child is not a U.S. citizen, or you assume they are, you delay identifiers like a Social Security number, you miss a reporting requirement, and then you discover the problem later when a bank asks for documentation.

Step-by-step: the operator-grade decision system#

Step 1: Confirm U.S. citizenship (don't guess). Action: Write down the child's place of birth, both parents' citizenship, and anything that could affect status. Verification: You can point to evidence, not memory. Keep in mind: citizenship is determined by birth, parentage, or naturalization, not by intent. "We didn't mean to" does not protect you from compliance, and "we assumed they have it" does not prove it.

Step 2: Confirm IRS obligations for this year (separate "tax owed" from "filing required"). Action: List what could trigger a filing or reporting requirement: income sources, accounts, and who owns what. Verification: You can answer "What forms might apply?" without inventing thresholds. If you cannot, you have an escalation case.

Step 3: Document evidence like you will need it later. Action: Create a dated folder and a one-page memo stating what you decided and which documents support it. Include notes on birth and citizenship documentation and your identifier plan, for example if and when you will apply for an SSN. Verification: A future you, or a CPA, can reproduce the decision without re-interviewing your own life.

Step 4: Escalate when facts are unclear (pay for clarity). Action: If you cannot confidently validate the facts that determine citizenship status, or you see cross-border complexity you can't explain cleanly, book specialist help before you file.

Safe defaults (use these until you have facts)#

| Decision area | Unsafe default | Safe default |

|---|---|---|

| Citizenship | "We assume they are not a U.S. citizen." | Prove or disprove with documents, then act. |

| Identifiers | "We'll deal with SSN later." | Plan identifiers early to avoid blocking compliance. |

| Filing/reporting | "No tax due means nothing to do." | Check obligations, then document yes or no. |

| Recordkeeping | "Spreadsheet only." | Audit-ready folder + dated memo. |

Scenario to plan for: a foreign bank asks for a Social Security number under FATCA, and you realize you never nailed down status or kept a clean paper trail. Your playbook prevents that scramble because you already made the decision, logged the evidence, and set a reminder to revisit it annually.

Is your child actually a U.S. citizen at birth (or are you assuming)?#

Confirm your child's U.S. citizenship status with evidence before you do any tax or banking work in their name.

This is the first control to lock in, because the wrong assumption sends you into the wrong paperwork lane and the wrong IRS and banking answers.

A clean way to anchor your thinking: citizenship is determined by birth, parentage, or naturalization, not by intent. So "we didn't plan for U.S. citizenship" does not protect you, and "we assumed they have it" does not prove it.

Step-by-step: the "prove it" citizenship workflow (born abroad)#

Before you start (prerequisites): pull the child's foreign birth record and both parents' identity and status documents. You are building a fact set, not a story.

Step 1: Sort your child into the right lane (born in the U.S. vs born abroad). Do not mash these together. Anyone born on U.S. soil is a U.S. citizen under the 14th Amendment, regardless of their parents' nationality, except limited cases involving foreign diplomats. If your child was born outside the U.S., their U.S. citizenship status, if any, is not based on the 14th Amendment birth-on-U.S.-soil rule, and may depend on parentage or later naturalization.

Step 2: Collect the parent facts that drive the analysis. You cannot "vibes" your way through this. Capture, at minimum:

- Each parent's citizenship at the time of birth

- Each parent's immigration status, if relevant

- A travel and residence history, kept factual and dated

- Legal parentage facts and timing, especially if anything non-standard applies

Step 3: Write the one-page citizenship evidence memo (your internal control). Use this as your clean summary for a bank and a future CPA or attorney.

| Memo field | What to write | Verification |

|---|---|---|

| Child | Birth country, city, date. Registration details. | Copy of birth record |

| Parents | Citizenship and status at birth. | Passport or status docs |

| Presence | Dated travel and residence notes. | Tickets, stamps, school records |

| Outcome | "Confirmed," "Not confirmed," or "Pending specialist review." | Your reasoning + documents list |

Hypothetical scenario: a bank asks for your child's U.S. status and supporting documentation for onboarding. If you already maintain this memo, you answer confidently, or you escalate fast without scrambling.

Escalation trigger: if you feel uncertain about the applicable rules, legal parentage, or timing, pay for clarity before you file anything under the child's name or plan around downstream tax or immigration consequences.

What do you need to prepare before you touch a tax form?#

Prepare an audit-ready "Monday-morning packet" and record system before you touch a tax form.

Once you've validated, or escalated, your child's possible U.S. status, you shift from "Am I in scope?" to "Can I execute without stalling if the IRS or a financial institution asks for clarification?"

Step-by-step: build the Monday-morning packet (inputs you will reuse)#

Step 1: Collect child identifiers and location facts (do not overthink it). You are not proving anything yet. You are removing future friction. Pull the identity and residency documents you already have available, for example a foreign birth record, any local registration record, and any passport(s) already issued, plus the child's current address by jurisdiction.

Step 2: Collect parent facts a professional may ask for when assessing status. You already started this in the previous section. Finish it. Keep proof of U.S. citizenship, for example a U.S. passport, and a dated travel and residence history. Add marriage or divorce decrees if they affect legal parentage or naming consistency.

Step 3: Build a CPA-ready "fact matrix" (one page). This becomes your reusable intake sheet: country of birth, current country of residence (jurisdiction), planned travel, and expected worldwide income sources that could touch the child's profile, such as interest, gifts, and investment accounts. You hand this to a preparer without a two-hour backstory.

Hypothetical scenario: you open a child account abroad for school expenses. The bank asks for U.S. status evidence and a U.S. tax ID. If you maintain this packet, you answer fast, or you escalate deliberately instead of panic-searching your inbox.

Step-by-step: set your record system and reminders (safe defaults)#

Step 4: Choose a folder structure you can run every year. Use one folder per tax year, with three subfolders: IRS, U.S. Department of State (if you pursue documentation there), Banking. Label files with date + jurisdiction, for example 2026-02-14_US_consulate_receipt.pdf.

| Folder | What goes in it | "Done" check |

|---|---|---|

| IRS | Returns filed, or a memo explaining why not, notices, payment confirmations | You can reconstruct what you filed and why |

| U.S. Department of State | Status-related receipts and correspondence, if applicable | You can show a clean timeline |

| Banking | Statements, onboarding requests, ID verification docs | You can answer "where did the money go?" |

Step 5: Put calendar controls in place (and don't guess deadlines). Annual: "Review child tax filing + reporting status." Calendar-year filers generally face an April 15 due date per IRS guidance; fiscal-year filers are generally due 3 months and 15 days after the close of the fiscal year. Also: if you end up claiming the foreign earned income exclusion and/or the foreign housing exclusion or deduction, that's where Form 2555 comes in.

For some abroad situations, including certain APO/FPO addresses or filers using Form 2555, the IRS lists different mailing addresses depending on whether a payment is enclosed. Keep this reference in your folder:

| Situation | Timing or address | Note |

|---|---|---|

| Calendar-year filers | April 15 due date | Generally per IRS guidance |

| Fiscal-year filers | 3 months and 15 days after the close of the fiscal year | Generally due then |

| Mail-file from abroad, no check or money order | Austin, TX 73301-0215 | One IRS-listed address for certain abroad situations |

| Mail-file from abroad, with check or money order | P.O. Box 1303, Charlotte, NC 28201-1303 | One IRS-listed address for certain abroad situations |

| No IRS-listed abroad situation applies | Use the appropriate address listed in the instructions for Form 1040 | Follow current-year instructions |

Step 6: Keep payments audit-traceable. If you collect income through tools like Gruv, download transaction history, use consistent memo fields, and categorize cleanly. Do this to reduce reconstruction work later, not to "optimize" U.S. tax outcomes.

For residency confusion that can derail your matrix, keep this handy: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Does your child have a U.S. tax filing obligation this year (and what's the safe default if you're unsure)?#

If your child is a U.S. person, for example a U.S. citizen, assume there may be a U.S. filing obligation and use current-year IRS instructions to confirm whether a return is required.

With your Monday-morning packet built, you can stop guessing and run a clean decision sequence. The goal is not to optimize. The goal is to avoid silent non-compliance in your yearly workflow.

Step-by-step: the decision sequence (write each answer into your yearly memo)#

Step 1: Inventory every income source and account (no vibes). List wages, gigs, bank accounts, brokerage accounts, education accounts, and anything held "for" the child by a relative or trust-like structure. If you cannot name the account, you cannot evaluate the obligation.

Step 2: Classify each item as earned vs unearned (then stop). This classification tells you which IRS rules you need to check.

| Income or activity | Earned vs unearned (operator label) | Why you care |

|---|---|---|

| Wages from a job | Earned | Different rules can apply than for investment income |

| Self-employment (odd jobs, online work) | Earned | May create separate tax and reporting complexity |

| Interest/dividends | Unearned | Common for child accounts abroad, easy to overlook |

| Capital gains | Unearned | Often shows up only when you sell |

| Trust distributions | Unearned (often) | Frequently triggers professional escalation |

Step 3: Verify current-year filing thresholds and forms on IRS instructions. Do not rely on blog numbers. Pull the instructions for the year you file, confirm thresholds for your child's income types, and record exactly what you referenced, title + tax year, in your memo.

Step 4: Confirm dependency and credit positioning before you file. Decide whether you, or someone else, will claim the child as a dependent, then verify how that interacts with any credits you plan to claim. Do not assume eligibility. Document the decision and the reason.

Step 5: Choose a safe default when facts look fuzzy. File conservatively or pay for professional confirmation. You are managing downside risk. A missed required filing creates messy cleanup later.

Hypothetical scenario: your expat family opens a child investment account abroad for school. You see small dividends and one sale. You cannot tell whether the income belongs to the child or you. You escalate and document the question rather than guessing.

Escalation triggers (when you stop DIY)#

Escalate if you see any of the following:

- Investment accounts in the child's name, especially outside the U.S.

- Any foreign trust-like structure or distributions

- Ambiguity about whether income belongs to the child vs the parent

- Household strategy interactions, for example parents planning the Foreign earned income exclusion (FEIE). The IRS makes this point clearly: the exclusion applies only if you qualify and you file a tax return reporting the income. Do not treat FEIE as a "no filing required" shortcut.

Quick FEIE sanity check (if FEIE is part of the plan)#

If you are leaning on FEIE as part of the household plan, keep these IRS basics in your memo:

| FEIE item | Rule or amount | Note |

|---|---|---|

| Physical presence test | 330 full days during any period of 12 consecutive months | Days need not be consecutive; the IRS notes you can count days abroad for any reason, so long as your tax home is in a foreign country |

| 2025 FEIE cap | Lesser of foreign income earned or $130,000 per qualifying person | If two married individuals both qualify, as much as $260,000 together for 2025 |

| 2026 FEIE cap | $132,900 per person | 2026 tax year |

| Housing limitation | Generally 30% of the maximum FEIE | Housing amount limitation is $39,000 for 2025 and $39,870 for 2026 |

Citizenship paperwork vs taxes: what should you do first (CRBA, SSN, ITIN)?#

Run the citizenship paperwork and the tax and identifier workstreams in parallel, and decide upfront which identifier you will use in each process.

You have sequencing decisions to make, and this is where globally mobile families lose weeks. They start one workflow, often citizenship documentation, and accidentally stall the other, the U.S. tax workflow, because they never locked the ID plan.

Step-by-step: two lanes, one control log#

Step 1: Open two lanes in your tracker (Status + Ability to file). Treat this like ops, not paperwork.

| Lane | Outcome you want | Typical dependency | Your operator artifact |

|---|---|---|---|

| Citizenship documentation (Status + proof) | Proof of status (if applicable) | U.S. government process, requirements vary | "Citizenship documentation folder" + submission log |

| Tax/identifier (Ability to file/claim) | An identifier the IRS can match cleanly | Identifier rules are fact-specific | "Tax ID plan" memo for the filing year |

Step 2: Start the citizenship documentation lane. If you are pursuing a Consular Report of Birth Abroad (CRBA) or other status documentation, verify current requirements directly with the relevant U.S. government office, for example a U.S. embassy or consulate where applicable, before you book, show up, or submit anything. Do not rely on someone else's checklist from a different country.

Step 3: Build a submission log and keep it updated. Include: date submitted, appointment date, reference numbers, what you provided, and PDF copies of every document and receipt. This log becomes your audit trail when a bank, school, or agency asks, "Where are you in the process?"

Step-by-step: the identifier decision that prevents IRS churn#

Step 4: Choose your tax identifier plan (then document it). Decide which identifier you intend to use on any IRS filings, for example an SSN or an ITIN, and write down the plan for your specific facts. Do not assume an identifier "will be fine" without checking current IRS guidance for your situation.

Step 5: Before you file anything with the IRS, run this practical check:

- Which ID will the return use (SSN vs ITIN)?

- Will that ID arrive in time for your filing cycle?

- If not, what is your documented plan, for example filing an extension only if you confirm you qualify and you follow current-year IRS instructions?

Hypothetical scenario: you book a consular appointment months out, but your child has activity, like investment income, in an overseas account now. You keep the tax decision moving, document the identifier status, and escalate for advice if needed instead of waiting on the citizenship paperwork timeline.

Separate but related (Social Security taxes): if you are working across borders, Social Security "Totalization" agreements can assign coverage to one country and exempt you from Social Security taxes in the other. When U.S. coverage applies under an agreement, SSA can issue a U.S. Certificate of Coverage as proof of exemption from the foreign country's Social Security taxes.

If you are dealing with citizenship status changes: the IRS describes relinquishing U.S. citizenship and the tax impacts as serious matters involving irrevocable decisions, and suggests considering legal counsel.

Security default: store SSN/ITIN scans in encrypted storage. Do not paste identifiers into email threads, chat logs, or unencrypted notes.

Build an audit-ready documentation pack (so future-you doesn't have to reconstruct your life)#

Build one "audit pack" per year that captures your decisions, the evidence behind them, and the status of citizenship, IDs, and accounts.

Once you run the citizenship lane, CRBA, passport, social security number, alongside the U.S. tax lane, you need one place where both workstreams reconcile. This pack turns a recurring compliance problem from a fire drill into a repeatable ops cycle.

Before you start (your standard for "done")#

Your goal is not paranoia. Your goal is low-stress repeatability.

Your pack should answer, in plain English: What did we decide, based on what evidence, under which jurisdiction, and when do we revisit?

Verification point: if a bank, a school, or a future CPA asks "prove it," you can respond by sharing a dated PDF bundle, not a story.

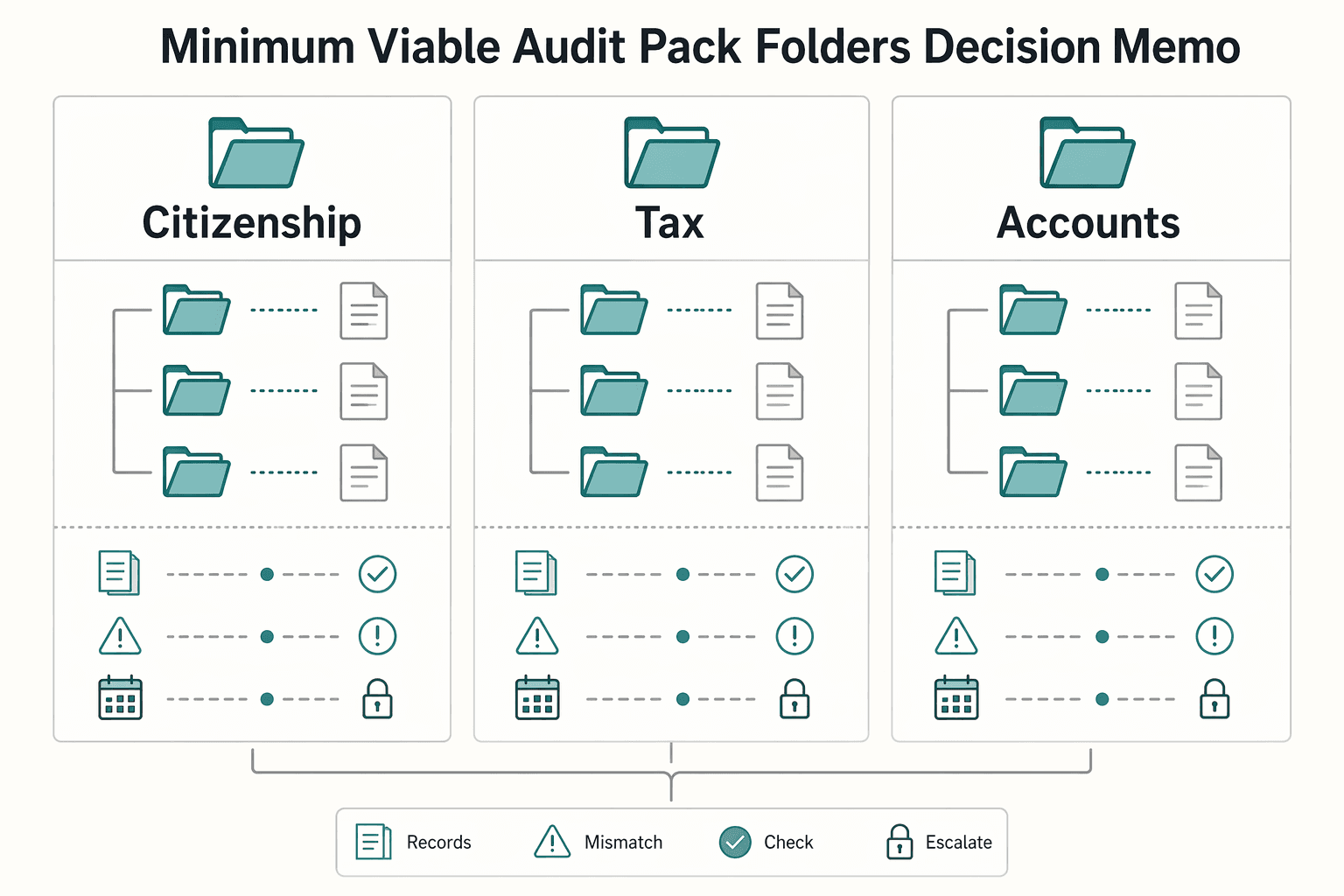

Step-by-step: minimum viable audit pack (folders + decision memo)#

Step 1: Create a single annual folder with three subfolders (Citizenship, Tax, Accounts). Use consistent file names with dates and jurisdictions.

| Folder | What to store | Outcome you get |

|---|---|---|

| Citizenship | Consular Report of Birth Abroad (or submission log), passport evidence, parent eligibility evidence as requested, consulate receipts | You can prove status, or prove "pending" with receipts and dates |

| Tax | Filed returns (or a memo explaining why none filed), IRS correspondence, proof of SSN or ITIN status | You can defend your filing decision and match IRS records cleanly |

| Accounts | Annual statements for relevant foreign financial accounts tied to the child | You can evaluate and support Form 8938 (and related FATCA) reporting decisions without reconstruction |

Step 2: Write a 1 to 2 page "Decision Memo" and update it yearly. Keep it tight:

- Citizenship assumption: confirmed vs pending, plus the evidence you rely on

- Filing obligation determination: what you checked in current-year IRS instructions

- Reporting determination: whether you attach Form 8938 to the annual return when required. The IRS says you use it to report specified foreign financial assets over the appropriate threshold, and you attach it to your annual tax return. Also note: the IRS says if you do not have to file an income tax return for the year, you do not have to file Form 8938 regardless of asset value. Capture that logic explicitly.

- Flag penalties as a risk-control note: the IRS says failure to report foreign financial assets on Form 8938 may result in a $10,000 penalty, and up to $50,000 for continued failure after IRS notification

Step 3: Standardize your money trail if you get paid globally. Save invoices, payout confirmations, and bank credits. If you use Gruv for collections or payouts, export your transaction history, where enabled, into the same annual pack so your documentation stays consistent with your transaction records.

Hypothetical scenario: you apply for a CRBA, then a foreign bank asks why your child shows U.S. indicia. You hand them the dated pack, receipt, status memo, and ID plan, instead of scrambling across inboxes.

Escalation trigger: if you cannot write the memo without lots of "I think," stop and pay for a consult. That uncertainty usually signals a real rule boundary, not a documentation problem.

Do foreign accounts trigger FBAR/FATCA reporting for your child?#

Yes, foreign accounts can trigger separate reporting (FATCA/Form 8938 and possibly the FBAR), depending on the rules and thresholds that apply. In particular, Form 8938 is tied to whether the taxpayer must file a U.S. income tax return for the year.

Your audit-ready pack makes this manageable. You run an accounts inventory, make two explicit decisions, and document them once.

Before you start: separate "tax return" from "information reporting"#

Treat tax filing and information reporting as two different workstreams with different rules.

Under FATCA, the IRS says certain U.S. taxpayers holding financial assets outside the U.S. must generally report those assets using Form 8938, and you attach Form 8938 to the taxpayer's annual tax return. The IRS also says if you do not have to file an income tax return for the year, you do not have to file Form 8938, regardless of the value of those assets.

Separately, the IRS notes you may also have to file FinCEN Form 114, titled the Report of Foreign Bank and Financial Accounts (FBAR). Do not assume Form 8938 "covers" FBAR, or vice versa.

| Reporting item | What it is | How it connects | Safe operator note |

|---|---|---|---|

| FBAR (FinCEN Form 114) | A report about foreign bank and financial accounts | The IRS notes you may also have to file it, in addition to Form 8938. | Verify definitions and thresholds for your year. Do not guess. |

| FATCA (Form 8938) | IRS reporting of specified foreign financial assets over the appropriate threshold | You attach it to the annual tax return. The IRS says thresholds sit at $50,000 in general, but can run higher in some cases. | Missing it may result in a $10,000 penalty, up to $50,000 for continued failure after IRS notification. |

Step-by-step workflow (write the decision into your memo)#

Step 1: Inventory every "child-linked" account. List any account where your child acts as owner, signatory, or beneficial holder. Include "kid" savings accounts and education savings products if your jurisdiction uses them. Log it first, classify it second.

Step 2: Pull statements and capture the relevant year-end and peak values you may need for reporting. Save PDFs into your "Accounts" folder. Then document your currency conversion method. Pick one method and stick to it year after year.

Step 3: Make two decisions: FBAR yes/no, Form 8938 yes/no. For Form 8938, anchor on the IRS rule: it's attached to the annual tax return when required, and only if your assets exceed the appropriate reporting threshold.

Step 4: Write it down like an operator. In your decision memo, add: account list, balances, method, and the conclusion.

Hypothetical scenario: your expat family opens a local account in your child's name for school fees. You later realize the child may be treated as a U.S. taxpayer. Your memo already shows what you checked and why you reported, or did not.

Safe defaults: If you feel uncertain about definitions or thresholds, pay for confirmation. Also avoid opening accounts in the child's name abroad unless you can explain the operational need and accept the reporting footprint.

The failure modes: common mistakes and the recovery playbook (no shame, just systems)#

If FEIE is part of the mistake, run one clean recovery sprint that gets you back to a documented baseline you can maintain.

If something already went sideways, the win is not moral purity. The win is getting back to a clean, documented baseline that you can maintain.

Before you start: freeze the situation (so you stop compounding errors)#

Step 1: Create a "Recovery" subfolder for the current year. Drop in every draft return, filed return, extension, filing confirmation, and any IRS notices. Outcome check: you can answer, "What did we submit, when, and what did we claim?"

Step 2: Write a one-page "date of discovery" memo. Use plain language: what you believed, what you learned, and what changed. Outcome check: future-you, or a CPA, can reconstruct intent and timeline in five minutes.

Recovery playbook by failure mode (run the steps that match your situation)#

Step 3: If you assumed FEIE meant "I don't have to file," stop and correct that. A common misconception is thinking excluded income doesn't need to be reported. To claim the foreign earned income exclusion, you still file a tax return reporting the income and claim the exclusion on the return.

Step 4: If you "kind of qualified" and hand-waved the test, re-run eligibility from first principles. At a minimum, the IRS ties the FEIE to having foreign earned income and a tax home in a foreign country. Then you generally qualify under a category like bona fide residence, uninterrupted period including an entire tax year, or the physical presence test. Document what you're relying on and what you're not.

Step 5: If you used the physical presence test and your day count is fuzzy, rebuild it cleanly. The physical presence test is based only on how long you're physically present in a foreign country or countries: 330 full days during any period of 12 consecutive months. Days do not need to be consecutive. This test does not depend on the kind of residence you establish, your intent to return to the U.S., or the nature and purpose of your stay abroad. Rebuild the timeline and keep the working paper.

Step 6: If you over-excluded (or guessed the cap), re-check the limits and redo the math. For tax year 2025, the maximum FEIE is the lesser of foreign earned income or $130,000 per qualifying person. For tax year 2026, the maximum exclusion is $132,900 per person. If both spouses qualify and choose the exclusion, the IRS notes they can exclude as much as $260,000 for the 2025 tax year.

Step 7: If you tried to "also exclude housing" without a real calculation, re-check the housing limitation. The limitation on housing expenses is generally 30% of the maximum foreign earned income exclusion. The housing amount limitation is $39,000 for 2025 and $39,870 for 2026. If you don't have a defensible worksheet, rebuild it.

| Failure mode | Recovery action | Escalate when |

|---|---|---|

| "FEIE means I don't have to file" | File, or amend, with the income reported and the exclusion claimed properly | You have multiple years affected or missed filings |

| Physical presence test guessed | Rebuild a day-by-day timeline to support 330 full days in a 12-month period | Travel patterns are complex and you can't confidently support the count |

| "Intent/residency type should count" | Remove narrative reasoning and anchor only to the IRS test requirements | Your eligibility hinges on facts you can't document |

| Over-excluded income | Recompute using the per-year maximum exclusion amounts | You're near or above the annual cap |

| Housing amount hand-waved | Recompute using the general 30% limitation and the stated housing amount limitation | You claimed a large housing amount without a clear worksheet |

Hypothetical scenario: you skipped filing because "it's excluded anyway," or you counted travel days loosely and assumed intent would save you. Your recovery sprint gives you one folder, one timeline, one memo, and a corrected return position you can actually defend.

Run this yearly, stay calm: the compliance system that scales with your mobility#

Run the same yearly sequence for Form 8938 (FATCA) and, if applicable, FBAR so foreign-asset reporting stops feeling like a moving target. The point is not to become a tax encyclopedia. The point is to run a tight system you can execute even when you move countries, open new accounts, or switch clients.

Before you start (set up your control center)#

Treat this like ops. Create one folder per tax year with three subfolders: Tax Return, Foreign Assets, Accounts. Then add a living document called "Decision Memo" where you log what you decided and why.

Step-by-step annual runbook (copy/paste)#

Step 1: Confirm whether you're filing an annual income tax return this year. This matters because Form 8938 must be attached to the taxpayer's annual tax return. And per IRS guidance: if you do not have to file an income tax return for the tax year, you do not have to file Form 8938, regardless of the value of your specified foreign financial assets.

| Step | Decision or action | Anchor rule |

|---|---|---|

| 1 | Confirm whether you're filing an annual income tax return this year | If you do not have to file an income tax return for the tax year, you do not have to file Form 8938 |

| 2 | Inventory specified foreign financial assets | Pull year-end statements and supporting records to value and describe them |

| 3 | Decide whether Form 8938 applies | In general, the IRS notes the value must exceed $50,000 to be reportable, and thresholds can be higher in some cases |

| 4 | If you're a specified domestic entity, check the entity thresholds | Exceeds $50,000 on the last day of the tax year or $75,000 at any time during the tax year |

| 5 | Run FBAR as a separate yes/no decision | You may also have to file FBAR (FinCEN Form 114), which is separate from Form 8938 |

| 6 | Save filings, statements, receipts, and a dated memo | Set a recurring calendar reminder to review accounts and records |

Step 2: Inventory what you may need to report. List your specified foreign financial assets and pull year-end statements and any supporting records you'll need to value and describe them.

Step 3: Decide whether Form 8938 applies (FATCA lane). Form 8938 is used to report specified foreign financial assets when the total value exceeds the appropriate reporting threshold. In general, the IRS notes the value must exceed $50,000 to be reportable, and thresholds can be higher in some cases.

Step 4: If you're a "specified domestic entity," check the entity thresholds. Certain domestic corporations, partnerships, and trusts formed or used to hold specified foreign financial assets may have to file Form 8938 if the total value exceeds $50,000 on the last day of the tax year or $75,000 at any time during the tax year.

Step 5: Run FBAR as a separate yes/no decision. The IRS notes you may also have to file FBAR (FinCEN Form 114), which is separate from Form 8938.

| Lane | What it is | Where it goes | Safe default |

|---|---|---|---|

| FATCA / Form 8938 | Reporting specified foreign financial assets (when thresholds are met) | Attached to annual tax return | No return required means no Form 8938 |

| FBAR (FinCEN Form 114) | Foreign account reporting | Separate from IRS return | Treat as a separate yes/no decision |

Step 6: Save artifacts and set reminders. Save filings, statements, and receipts, plus a dated 1 to 2 page memo capturing your decisions. Set a recurring calendar reminder to review accounts and records so you're not scrambling at filing time.

Hypothetical: you open a new account abroad mid-year. Your system forces a regular accounts check, so you capture statements early and decide, in writing, whether Form 8938 or FBAR applies.

Frequently Asked Questions

Does a U.S. citizen child born abroad owe U.S. taxes?

Maybe. Whether a child born abroad owes U.S. tax or has to file depends on the child's facts for the year, not just where they were born. Document what you checked, and get professional confirmation when you are unsure.

If my child was born abroad, are they automatically a U.S. citizen?

No, do not assume that. A child born outside the U.S. may or may not be a U.S. citizen depending on parent facts and documentation. Treat it as a proof question and confirm status through the appropriate official process.

What should parents do first: citizenship paperwork or tax filing?

Do both in parallel. Keep the citizenship status lane moving while you also check income, accounts, and annual filing needs, and lock the identifier and recordkeeping plan early so records stay consistent. If timing gets tight, file conservatively and keep clean documentation.

What is an “Accidental American” child, and what does it change for taxes?

An "Accidental American" child usually has potential U.S. citizenship because of parentage or birth circumstances despite living abroad and not identifying as American. For taxes, the practical step is to confirm status with evidence first. Then map filing and reporting obligations from that status.

When should I talk to a tax professional about my child’s U.S. tax situation?

Talk to a professional when you cannot confidently separate parent income from child income or when the cross-border facts are not clean. Common triggers include investment income in the child's name, multiple years potentially affected, and foreign-asset reporting questions. Paying for confirmation is often cheaper than cleanup later.

Do foreign bank accounts for my child trigger FBAR or FATCA reporting?

They may. Treat FBAR and FATCA/Form 8938 as separate reporting decisions, and remember that Form 8938 is attached to the annual tax return when required. If the child does not have to file an income tax return for the year, they do not have to file Form 8938 regardless of asset value.

Can I claim the Child Tax Credit if my child was born abroad?

Maybe. Eligibility for the Child Tax Credit depends on the specific requirements and how you file, not simply on the fact that the child was born abroad. Verify the current-year rules for your facts before you claim it.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

The Best Software for Creating Case Studies

**Treat case studies like a system, not a one-off design task, and you can win clients with consistency instead of guesswork.** If you have searched for the best software for case studies, you have probably seen mixed lists that lump content tools together with legal case-management products. That overlap wastes time and leads to uneven outputs.