Quick Answer

Start by opening an incident file, logging each failed departure attempt, and saving third-party proof such as government notices and carrier messages. For tax residency during crisis situations, do not rely on a generic day-count myth or visa status alone. Build one consistent filing packet with a facts summary, evidence index, and aligned dates across returns. If two countries may both claim residence, verify current treaty wording and get professional review before you file.

Trapped Abroad? Turn Tax Anxiety into a Strategic Advantage#

If you get stuck abroad, the order of decisions matters. Handle your safety first, then do tax-compliance triage. Residency exposure is country-specific and often turns on physical-presence tests. If two countries can both treat you as resident, treaty tie-breaker rules are applied step by step until one result is conclusive.

Do not rely on a generic "183-day rule." The rules are not uniform. For example, the U.S. Substantial Presence Test uses 31 days in the current year plus 183 days across a 3-year formula. The UK can treat 183 days or more in a tax year as automatic residence, and exceptional-circumstances treatment is capped at 60 days and is not automatic.

| Approach | Likely outcome | Audit defensibility | Stress level |

|---|---|---|---|

| Reactive approach | Missed day counts, weak explanations, late cleanup | Low, because records are incomplete or scattered | High |

| Documented approach | Clear timeline, cleaner filing position, easier professional support | Higher, because records are organized and traceable | Lower |

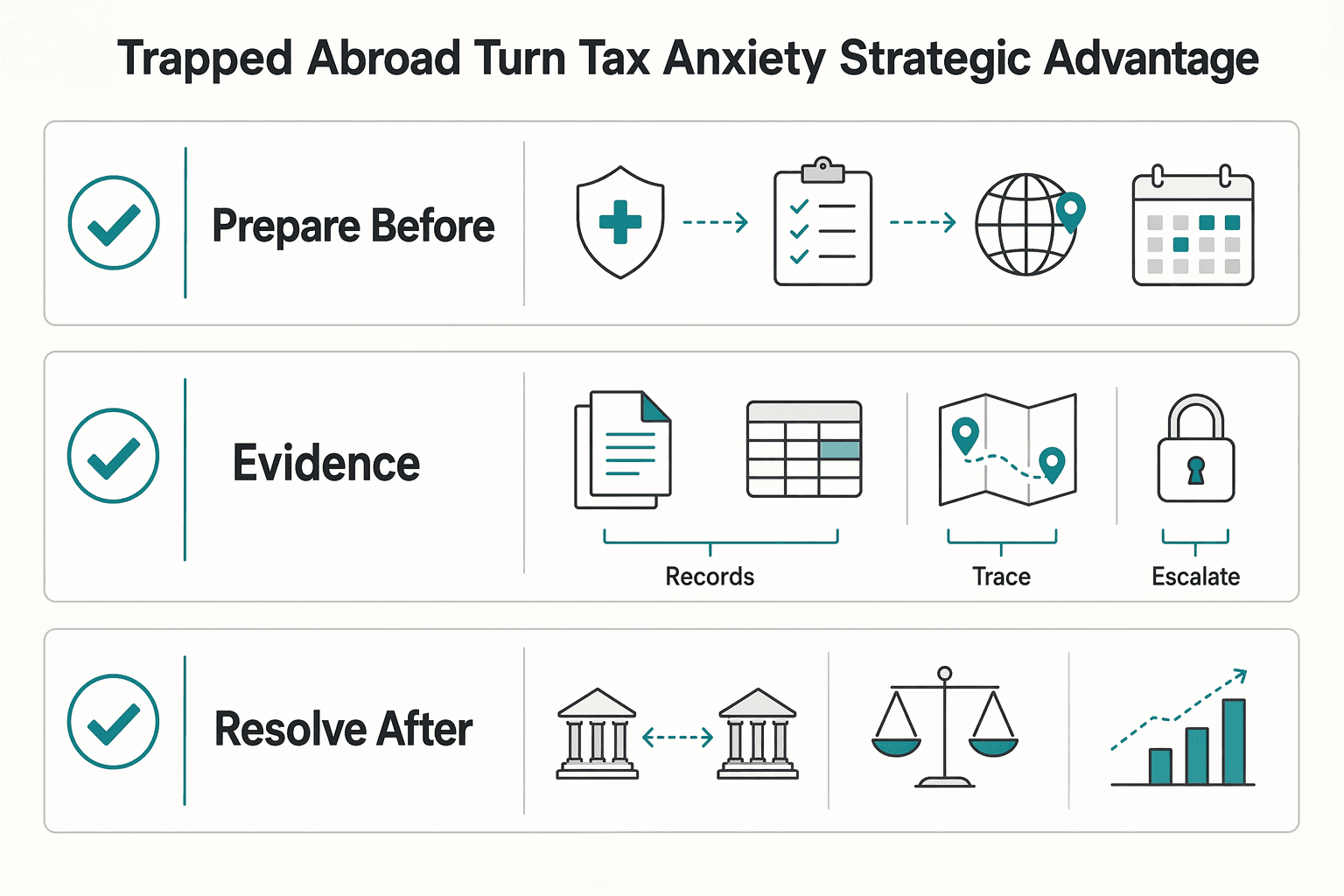

Use this article as a three-phase guide:

- Prepare before disruption.

- Document during disruption.

- Resolve after disruption.

In Phase 1, you'll map the countries that matter, identify the exact tests that apply, and set up a file you can defend later. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2026.

Phase 1: Pre-Crisis Fortification (Build Your Compliance Go-Bag)#

Before you travel, build an evidence-ready baseline. If disruption happens later, a file that was already complete and organized is easier to review than one reconstructed afterward.

Step 1. Map the countries that could matter#

Start with the countries that can realistically affect your filing position, then verify each row with current official rules or qualified professional advice before you rely on it. Treat every threshold, exception, and test as unverified until confirmed for your exact facts and tax year.

| Jurisdiction | Trigger type to verify | What can create exposure | What can support your position | Action owner |

|---|---|---|---|---|

| Home country | Residence, departure, or ongoing-tie rules. Confirm current thresholds and definitions. | Facts local rules may treat as ongoing connections. | Records documenting your timeline and connections. | You; adviser if unclear |

| Current long-stay country | Presence, registration, or filing triggers. Confirm current thresholds and definitions. | Facts local rules may treat as taxable presence. | Entry/exit records, status records, housing/work records. | You |

| Frequent fallback country | Repeated-stay or cumulative-presence rules. Confirm current thresholds and definitions. | Patterns local rules may aggregate across stays. | Travel log, passport records, bookings, payment records. | You |

| Client-heavy country | Source-of-income, work-presence, or registration triggers. Confirm current thresholds and definitions. | Facts tied to where work was performed and related activity. | Contracts, calendar, invoices, business correspondence. | You; adviser if risk is unclear |

Step 2. Keep proof of the ties you intend to maintain#

Your file should show where your life and operations were anchored before disruption. Build a pre-travel checklist so those facts are easy to verify later, and keep only records that are current and consistent.

| Tie category | Possible records to organize |

|---|---|

| Home ties | lease/deed; utility records; property records; home insurance; accommodation confirmation |

| Economic ties | business registration; banking activity; payroll/dividend records; pension records; active client contracts tied to your base |

| Personal ties | household location records; school records; medical-provider records; active memberships |

| Administrative ties | tax notices; license records; voter records where applicable; insurance policies; mailing-address evidence |

Relevance varies by jurisdiction.

Step 3. Use one log and one evidence system#

A single source of truth is the practical control that keeps the rest of this process from falling apart. Use one movement log, one file structure, and one monthly check to reduce reconstruction errors when details are harder to verify later.

- Keep one travel log for border crossings, overnight location, booking changes, and work location.

- Keep one folder structure, for example:

year > country > month > travel/housing/work/tax/correspondence. - Run a monthly reconciliation: compare your log against passport records, travel confirmations, payment records, and accommodation records.

Step 4. Keep immigration and tax analysis separate#

Do not assume immigration permission answers your tax questions. Treat immigration permission and tax analysis as separate checks unless qualified advice confirms how they interact in your case.

| Do not assume | Safer default |

|---|---|

| A valid visa settles your tax position | Review tax exposure separately |

| A tax filing position confirms immigration compliance | Review immigration status separately |

| One set of documents is enough for both | Keep records organized in separate, clearly labeled sets |

Final check: you should be able to hand over one jurisdiction table, one travel log, and one evidence folder that another person can review quickly without guesswork.

You might also find this useful: What Happens if You Overstay Schengen Visa Rules?.

Phase 2: In-Crisis Triage (Your Immediate Documentation & Risk-Assessment Plan)#

Once disruption starts, your job is to build contemporaneous records of what happened, what actions you took, and what changed over time. Open an incident file immediately and keep updating it as facts change. In this phase, process matters as much as the final document.

Step 1. Open the incident file and secure third-party proof#

Create one dated folder as soon as disruption starts, for example: year > country > crisis-event > official-notices / travel / consular / medical / work / correspondence / log. Aim for clear, dated, third-party-backed records that someone else can audit without guesswork.

| Evidence item | Why it matters | Minimum acceptable proof | Where to store it |

|---|---|---|---|

| Government notice | Establishes the external event context and timeline | Screenshot or PDF showing issuing authority, URL, and access date | official-notices |

| Carrier disruption | Connects the disruption to your failed departure attempts | Cancellation notice, rebooking refusal, refund record, or itinerary change notice | travel |

| Personal departure-attempt log | Shows your documented response over time | Dated entries with route attempted, carrier/contacted party, channel, and result | log |

| Consular communication | Shows you sought official support or direction | Email thread, case reference, or dated call summary | consular |

| Medical constraint | Documents case-specific inability to travel | Dated clinician note or medical record stating travel limits | medical |

Step 2. Run a first-response flow#

The first few actions matter because booking portals change, links expire, and details are harder to reconstruct later. Treat this as a flexible checklist, not a rigid script, and keep notifications factual: where you are, why departure failed, whether work continues, and any temporary scope limits pending review.

| Action | What to do |

|---|---|

| Save originals first | Download notices, booking records, emails, and related files before portals update or links expire |

| Log intent to depart | Record planned departure, disruption details, and each failed attempt |

| Notify affected parties | Inform clients, employers, and advisors whose contracts, delivery, or reporting may be affected by your location |

| Preserve originals plus backups | Keep a read-only raw folder and a separate working folder for summaries and notes |

Step 3. Screen business-presence risk before operating as usual#

This is a common place to create unnecessary risk. Do not assume temporary presence automatically creates or removes legal or tax exposure. Use this quick screen and escalate early if needed.

| Checkpoint | If "yes" | Immediate mitigation |

|---|---|---|

| Are you acting with authority in client-facing commercial decisions from the crisis location? | Potential exposure may increase and needs review | Limit role to delivery-only tasks until reviewed |

| Are you signing contracts, amendments, or SOWs while there? | Potential exposure may increase and needs review | Pause local signing or route execution through your normal home-base process in writing |

| Are you negotiating commercial terms from that location on an ongoing basis? | Potential exposure may increase and needs review | Reduce/stop local negotiation activity and document temporary limits |

| Is revenue-critical work continuing under changed facts? | Operational and compliance risk may concentrate | Escalate to an advisor promptly |

Step 4. Capture work-location facts for later analysis#

For later legal, tax, and contract review, document physical work location explicitly instead of trying to infer it later from invoices or client addresses. Record where work was actually performed, not only who paid you.

| Client location vs work-performed location | Immediate stance | Next step |

|---|---|---|

| Client in Country B, work performed in Country A | Document both locations and avoid assumptions | Current jurisdiction-specific treatment pending official tax/legal/source-record verification. |

| Client in Country A, work performed in Country A | Still document dates, activities, and changes | Current jurisdiction-specific treatment pending official tax/legal/source-record verification. |

| Multiple client countries, work performed from one crisis location | Track location facts by engagement and date | Current jurisdiction-specific treatment pending official tax/legal/source-record verification. |

Keep daily location notes aligned with your calendar, invoices, and deliverables. Document any no-work periods as clearly as work periods.

For a step-by-step walkthrough, see How to Manage 'Días de Ausencia' for Spanish Tax Residency.

Before you move to filing, consolidate your entry/exit timeline and supporting documents in one place with the Tax Residency Tracker.

Phase 3: Post-Crisis Resolution (How to File and Communicate with Confidence)#

In this phase, the goal is straightforward: file one consistent, evidence-backed position across every document so your residency story does not conflict across returns, attachments, or disclosures.

Step 1. Build a filing packet from your incident file#

Your incident file is raw material, not the final product. Convert it into a short filing packet that a reviewer can follow quickly. If written explanations are allowed, attach one and keep it factual and easy to audit.

| Packet item | What to include | Final check before filing |

|---|---|---|

| Facts summary | Arrival date, intended departure date, failed departure attempts, return date, and any no-work or reduced-work periods | Reconcile every date against passport stamps, tickets, calendar records, and invoices |

| Evidence index | Numbered list of third-party records (official notices, carrier messages, consular contacts, medical records, work correspondence) | Confirm each item shows source, date, and file location |

| Legal basis framing | Current rule, treaty text, or authority guidance pending official tax/legal/treaty/source-record verification. | Verify the tax year and confirm you are using the current guidance version |

| Short cover narrative | Neutral 5-8 sentence explanation of what happened and the filing position you are taking | Make sure the same narrative appears across all forms, attachments, and advisor notes |

Step 2. If treaty text may matter, verify the current text and document uncertainty#

If dual-residency risk exists, work from the treaty text itself, not memory. Use only the treaty wording and year/version you can verify. If the text or evidence is unclear, state that uncertainty plainly and escalate before filing.

| Treaty checkpoint | What to document | If evidence is mixed or conflicting |

|---|---|---|

| Provision you believe may apply (as written in the treaty) | Quote the exact text and note the year/version used | State the conflict plainly and escalate before filing |

| Facts tied to that provision | List the dated records you are relying on | Keep uncertainty explicit rather than forcing a confident conclusion |

| Cross-form consistency | Keep one worksheet mapping statements across forms and attachments | Pause before filing until conflicts are reconciled |

Year control is mandatory. The ATO states some guidance is year-specific and instructs you to confirm you are using the correct year before making decisions. The ATO also says it may take your reliance on its guidance into account if that guidance is incorrect or misleading.

Step 3. File obligations in parallel, then reconcile before submission#

Residency position and filing obligations run on parallel tracks. Before you submit anything, run this control list:

| Control item | Before submission |

|---|---|

| Domestic return position | Complete and date-consistent |

| Foreign return or disclosure items | Triggered by your facts are identified and prepared |

| Extension payment items | Handled separately from filing extensions |

| Estimated tax obligations | Reviewed and updated where required |

| Final reconciliation | Dates, addresses, and residency position match across all filings |

If California applies, use the 2025 Form 540NR instructions as an anchor checkpoint. April 15, 2026 is the file-and-pay date to avoid penalties and interest, and October 15, 2026 is the file or e-file date to avoid the late filing penalty. Use FTB 3519 for automatic extension payment details.

If you were living or traveling outside the U.S. on April 15, filing and payment dates differ, and weekend or holiday due dates move to the next business day. California also lists 2026 estimated payment dates (April 15, June 15, September 15, January 15, 2027) and notes the general withholding thresholds (90% rule and $500/$250 balance-due thresholds).

Step 4. Escalate early when risk or records are not clean#

Do not wait until filing week if the facts are messy. Escalate to a cross-border advisor before filing if any of these apply:

- Dual-residency risk is real and treaty application is not clear.

- Authority guidance is conflicting, changed by year, or unclear for your facts.

- Records are incomplete, dates conflict across documents, or your narrative changed over time.

Final gate: if two filings require different answers, prepare a written explanation before you submit.

Related: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Conclusion: From Compliance Anxiety to Empowered Control#

Crises are unpredictable, but your compliance response is not. When residency becomes a real issue, the practical path is to document fast, organize evidence, and explain your facts consistently.

Use the three phases as a working recap:

-

Build before you move. Keep baseline records ready before anything goes wrong. If you had to explain where you lived, worked, and intended to return on short notice, you should be able to pull dated records quickly from one organized system.

-

Document while events are happening. Save key records as events unfold, such as official restriction notices, carrier cancellations, passport stamps, relevant medical records, and a dated departure-attempt log. When facts are mixed, timestamped third-party records are usually stronger than a retrospective narrative.

-

File and explain with discipline. When your filing process allows it, attach a short factual statement and evidence index instead of waiting for questions. Check for consistency across dates, addresses, travel history, and your residency position in every filing document.

This is where avoidable errors often start. Return-processing issues affect millions of taxpayers, and confusion in responding to notices and letters is a known problem. If your records conflict or two jurisdictions could reasonably read the same facts differently, do not guess just to finish quickly.

The practical default is simple. Document early, keep evidence organized in one place, protect sensitive tax information from loss, breach, or misuse, and escalate to a qualified cross-border advisor when facts are mixed across jurisdictions. That will not remove every uncertainty, but it can lower stress, reduce avoidable mistakes, and support clearer decisions during a crisis.

For a country-specific example, see A Guide to Tax Residency in Brazil for Digital Nomads.

If your facts point to possible dual-residency or business-structure risk, get a second review on your plan through Gruv contact.

Frequently Asked Questions

If you were stuck longer than planned, are you automatically a tax resident there?

No automatic answer is supported here. Tax residency rules are jurisdiction-specific, and treaty application is fact-specific. Confirm current rules with the relevant tax authorities before filing.

What evidence is strong if your extended stay was involuntary?

Keep dated, consistent records from reliable third-party documents and follow the requirements of the tax authority handling your filing.

Does your visa decide your tax status?

Check immigration requirements and tax rules separately for each jurisdiction involved.

Should you wait for a tax authority to ask questions before you explain what happened?

No universal rule is established here. Follow the instructions for the specific return or notice in your jurisdiction, and keep your timeline and records consistent.

If you are a U.S. person abroad, do your U.S. filing duties stop during a crisis?

No. U.S. citizens and green card holders must file U.S. federal income tax returns while abroad. Crisis relief is separate and depends on disaster relief that the IRS has formally authorized and announced.

How do you verify whether IRS disaster relief applies to you?

Check the IRS disaster pages in two steps. First, confirm eligible localities in “Around the nation.” Then confirm the specific guidance notice and postponed dates in the guidance-by-date list. Do not assume one disaster notice applies to your case without matching your facts to the exact notice.

Who can qualify for IRS disaster relief in messy or cross-border facts?

A clear category is an affected taxpayer, including an individual whose principal residence is in a covered disaster area, and a spouse if filing jointly. You may also qualify from outside the area if required records are located in a covered disaster area. Verify both the covered area and the IRS notice details.

What should you do if two countries might both treat you as resident?

If both countries may claim residence, review the applicable treaty text and escalate for professional advice before filing.

When should you involve a cross-border tax professional?

Consider involving one before filing when residency treatment is unclear, records conflict across jurisdictions, or your filing position could differ between countries.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- delcopa.gov/sites/default/files/2025-03/ComprehensiveCri...trusted

- ftb.ca.gov/forms/2025/2025-540nr-booklet.htmltrusted

- irs.gov/individuals/international-taxpayers/substant...trusted

- irs.gov/newsroom/tax-relief-in-disaster-situationstrusted

- taxpayeradvocate.irs.gov/wp-content/uploads/2024/12/ARC24_MSP.pdftrusted

- taxpayeradvocate.irs.gov/wp-content/uploads/2020/08/Volume-1.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

What Happens if You Overstay the Schengen 90/180 Day Rule?

**If you are worried about a Schengen overstay issue, treat it as an operations problem and run a documented timeline.** Think of yourself as running a business of one, with mobility as part of the system. A small counting error can disrupt more than a trip. It can affect relocation timing, client delivery, and re-entry plans at the same time. For remote professionals, travel in Europe rarely sits in isolation. Flights, housing, contracts, and immigration steps usually lock together.