Quick Answer

Report foreign rental income on your U.S. tax return on Schedule E (Form 1040), Part I, if you are a U.S. citizen or resident alien unless a specific exclusion clearly applies. Start with gross rent, then deductible expenses, then depreciation, keep each amount tied to source records, and evaluate any foreign tax credit separately with support that matches the same income stream and period.

You still report it even if the property is abroad#

When dealing with us tax on foreign rental income, start conservatively: treat reportability and treatment as unresolved until primary IRS authority for your facts says otherwise.

That opening stance prevents a common mistake. Many people rely on summaries that are useful but not controlling. Internal Revenue Bulletin synopses are reader aids, not authoritative interpretations. FederalRegister.gov prototype pages are informational and not the official legal edition. A Regulations.gov item marked proposed rule is still a proposal. If you miss that distinction, later calculations can rest on the wrong premise.

To keep that from happening, separate research from filing support. Helpful summaries can point you to an issue, but they should not become the final support for a filed position. Keep them in your research notes if you want, but build the return around primary instructions and final rule text.

Use a filing sequence you can defend rather than chasing shortcuts. Build support first, report only what you can tie to primary instructions, and flag unresolved items before submission. A practical way to keep this clean is to keep one working file with three blocks: authority notes, number support, and unresolved questions. When those three blocks stay aligned, final review is faster and less stressful. It also makes later review easier because a second pass can see the path from authority to worksheet to filed number without guessing what you meant.

That structure also helps when the issue is not whether rent exists, but how a specific item should be treated. If a question comes up about a tax payment, a mixed-use expense, or whether an amount belongs in a credit analysis at all, you want the answer in the file, not only in your memory. A tight file lets you see which issues are settled, which are mechanical, and which still need judgment.

- Classify authority before income. Confirm you are using final instructions or final rules, and note dates when guidance changed.

- Set evidence standards now. If a position cannot be tied to primary form instructions or final rule text, mark it unresolved.

- Keep scope tight. This article focuses on compliant rental-income reporting and related filing decisions, not aggressive positions.

Making the file look formal is not the goal. Making each later decision easier is. When reportability is settled first, you spend less time reworking numbers that never should have been excluded or credited in the first place. You also avoid a common end-of-process problem: discovering that a number was built on a summary page you cannot actually defend.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

What to prepare before you touch your return#

Prepare your records before you enter any numbers, and claim only lines you can fully trace.

| Prep item | What to include | Key rule |

|---|---|---|

| Evidence folder | Leases, rent receipts, expense invoices, and proof of foreign tax paid or accrued, labeled by country, property, and period | Build one folder for the tax year before entering numbers |

| USD conversion log | Date, local amount, exchange rate, USD result, and rate source | Form 1116 reports amounts in U.S. dollars, except where Part II says otherwise |

| Credit vs. deduction choice | Decision on whether qualified foreign taxes will be claimed as a credit or a deduction | If you choose the credit, it applies to all qualified foreign taxes for that year |

| Related filing tracks | Possible state exposure, including California/FTB when relevant, plus foreign returns and coverage periods | Flag them at the start |

| Verification check | One source document tied to the same period and income stream | Run it on every deduction and credit line |

The fastest way to slow down a filing is to start typing into software before the paper trail is organized. Build the file first, then calculate, then enter. That order sounds simple, but it keeps you from fixing the same issue in multiple places later.

- Build one evidence folder for the tax year with leases, rent receipts, expense invoices, and proof of foreign tax paid or accrued, labeled by country, property, and period.

- Keep a USD conversion log you can defend.

Form 1116reports amounts in U.S. dollars, except where Part II says otherwise, so track date, local amount, exchange rate, USD result, and rate source. - Decide credit vs. deduction early for qualified foreign taxes. You can choose either path for the year, but if you choose the credit, it applies to all qualified foreign taxes for that year.

- Flag related filing tracks at the start: possible state exposure (including California/FTB when relevant), plus foreign returns and coverage periods.

- Run a verification check on every deduction and credit line: one source document, tied to the same period and income stream.

Good prep also means a consistent file structure. Keep source documents, working summaries, and unresolved notes separate enough that you never confuse a convenience summary with actual support. If several properties or currencies are involved, keep the same naming pattern across all of them so review does not turn into a scavenger hunt. The more uniform the structure, the less likely you are to duplicate a document, miss a period, or attach the right record to the wrong worksheet line.

It also helps to decide what counts as complete before you start calculations. A folder with a lease and a few invoices may feel close enough, but it is still incomplete if you cannot tie tax payments to the same covered period or if a rent summary does not match the receipts you plan to use. The goal is not perfection; it is having enough support that each line on the return can be defended without rebuilding the file under deadline.

If you cannot trace a line, remove it until fixed. Also resolve categorization early, because Form 1116 uses separate forms by income category. Waiting until the end to sort categories usually means rebuilding the foreign tax file when you are already trying to submit.

Before you calculate, keep a minimum packet per property: lease, rent summary, expense summary, tax payment proof, and a short note on open items. If that packet is incomplete, stop there rather than pushing partial data through the entire return. If a document is missing, note the exact gap instead of leaving a vague reminder. "Need proof of payment for this period" works. "Check later" is how open items disappear.

Step 1 decide what is reportable and what is not#

Start with this rule: if you are a U.S. citizen or resident alien, treat income as reportable unless a specific exclusion clearly applies.

The key distinction is income type. Form 2555 and the foreign earned income exclusion apply to foreign earned income, and claiming that exclusion still requires reporting the income on a U.S. return. Do not treat those earned-income rules as a blanket exclusion for rent.

A clean way to do this is to make a classification sheet before you do any math. List each income stream, label the type, note the preliminary treatment, and add the authority note that supports the decision. Do not group items based on where the cash landed. If rent and wages hit the same foreign account, they are still different income streams and need different analysis.

That classification sheet should be simple enough to read in one pass. One line per income stream is usually better than a single paragraph trying to describe everything at once. The point is not elegance. The point is to make it obvious which items belong in the rental file, which belong in an earned-income analysis, and which still need review before you make a filing call.

Use this quick triage before you exclude anything:

- Confirm filer status. If you are filing as a U.S. citizen or resident alien, keep worldwide-income treatment as your baseline.

- Classify each income stream. Separate rental receipts from wages, self-employment income, and other earned compensation.

- Apply FEIE tests only to earned income. Tax home and physical-presence-style FEIE qualification tests are not a general rule for rental exclusion.

- Document each exclusion decision. If support is unclear, keep the amount reportable until reviewed.

The practical test is simple: before you move an amount out of the reportable bucket, you should be able to explain why and point to the support in your file. If you cannot do both, leave it in for now. You can always narrow the reporting position later when the support is solid; it is much harder to defend a missing amount that was omitted on instinct.

A common way this goes wrong is treating life abroad as one tax bucket. A person may have rent from property, salary from work, and reimbursements or transfers moving through the same account. That may feel like one financial picture, but it is not one tax category. If you do not split the streams early, later steps get messy fast because conversion logs, credit analysis, and form placement all depend on correct classification.

Conservative reporting usually means more work up front, but unsupported omission creates bigger correction costs later. The output of Step 1 should be a clean reportable-vs-excluded map by income type, with unresolved items clearly flagged.

Step 2 turn raw property activity into defensible numbers#

Use a fixed order: gross rent, deductible rental expenses, then depreciation, and keep each line traceable to support. This aligns with Schedule E (Form 1040) and helps prevent capital recovery from getting mixed into current-year deductions.

Use one worksheet per property that mirrors the form: rents first, expense lines next, and depreciation in its own category. Schedule E totals expenses before netting, with line 20 flowing to line 21. A useful worksheet structure includes the period, local amount, USD amount, category, document ID, and a short note for anything unusual. If you keep that structure from the start, later tie-outs are much faster.

Do not begin with a net figure from a summary if the underlying detail exists. Starting from gross rent forces you to classify expenses instead of letting them disappear inside a single net number. That matters because once a capital item or personal charge is buried in an expense total, it is harder to detect and harder to fix.

A simple build order helps. Enter all gross rent by period first. Then enter expenses by category. Then isolate depreciation instead of letting it disappear into a catchall number. That order keeps the worksheet readable. When you review the file later, you should be able to see how the property performed before deductions, how deductions were grouped, and where special review items still sit.

- Enter gross rent first using one consistent, documented reporting approach.

- Classify expenses before totals so capital items do not slip into current deductions.

- Track fair rental days and personal use days as they occur.

- Map each worksheet line to one document ID before it flows into

Schedule E (Form 1040).

The main failure mode is mixing personal or vacation spending into rental deductions without clear allocation support. A related error is claiming full mixed-use vehicle interest when only the business-use portion is deductible on Schedule E. Another common breakdown is letting an unclear item sit in the worksheet with no note, then forgetting why it looked unusual during review.

Track mixed-use facts while they are still fresh. If an expense touches both personal and rental use, the worksheet should show that it needs allocation or review. If support covers only part of the expense, book only the supported portion until the rest is resolved. The file should make conservative treatment obvious, not hide it. That is especially useful when you return to the file after time has passed and no longer remember why a line was reduced.

It also helps to separate "known amount" from "final treatment." You may know a payment happened without yet knowing whether it belongs in a current deduction, should be capitalized, or needs allocation. Put that uncertainty in the note column instead of forcing the item into a category just to make the worksheet balance. Fast decisions made under pressure tend to create the exact rework you were trying to avoid.

Keep a short exceptions note for unclear items, including capitalization questions or unusual use periods, and mark them for review instead of forcing a quick call. A good exceptions note is brief but specific: what the item is, why it is unclear, and what needs to happen before it can be finalized.

If rent was collected over several periods, make that period structure clear in the worksheet. If an expense invoice covers a different period from the rent you are matching against, mark that difference. If a receipt is incomplete or hard to read, note that before the detail is lost. These are small controls, but they keep later review grounded in actual support instead of memory.

Checkpoint before Step 3: you can trace each rent, expense, and depreciation line from worksheet to source in under two minutes. If that test fails, the worksheet is not done yet.

Step 3 file it in the right place and tie it through the return#

File rental real estate activity on Schedule E (Form 1040), Part I, and do not finalize the return until every entered amount ties back to your worksheet and source records.

Data entry should be the last stage, not the first. By the time you touch Schedule E, the classification work, conversion work, and support file should already be stable enough that you are mostly transcribing confirmed numbers rather than making judgment calls on the fly.

Pre-submit sequence:

- Enter rents, expense categories, and the net result in Part I, and keep depreciation on its own line.

- Trace each

Schedule E (Form 1040)amount to the USD worksheet and source document ID. - Mark unresolved technical items as

UNKNOWNin your working file and route them for professional review. - Confirm form boundaries: if the activity is renting personal property as a business, it may belong on Schedule C instead of Schedule E.

After entry, compare more than the bottom line. A net result can look right even when a rent number is understated or an expense category is overstated. Review the composition of the result line by line so the form tells the same story as the worksheet. If the worksheet says one thing and the form output suggests another, stop there. Do not assume the software put everything where you intended.

If you use software, do not rely only on interview screens. Review the actual form output before filing so you can see where the numbers landed. This is especially useful when you are checking that depreciation remained separate and that nothing unexpected moved into the wrong category. Interview screens can hide placement choices behind plain-language prompts, while the form itself shows the final result you are responsible for.

A simple review method is to keep the worksheet and the generated form side by side and compare them in the same order the form presents the lines. That prevents skipped categories and reduces the temptation to jump around the file. It also makes it easier to catch a small mismatch before it affects a larger total.

Checkpoint: pick any number on Schedule E (Form 1040) and trace it to worksheet and evidence in under two minutes.

If a late edit changes one figure, rerun the full tie-out so rents, expenses, depreciation, and net result still match your records. Late changes are where quiet mismatches start. One update in the worksheet can affect the return, the credit analysis, and the review notes. Treat those changes as a chain, not as isolated edits.

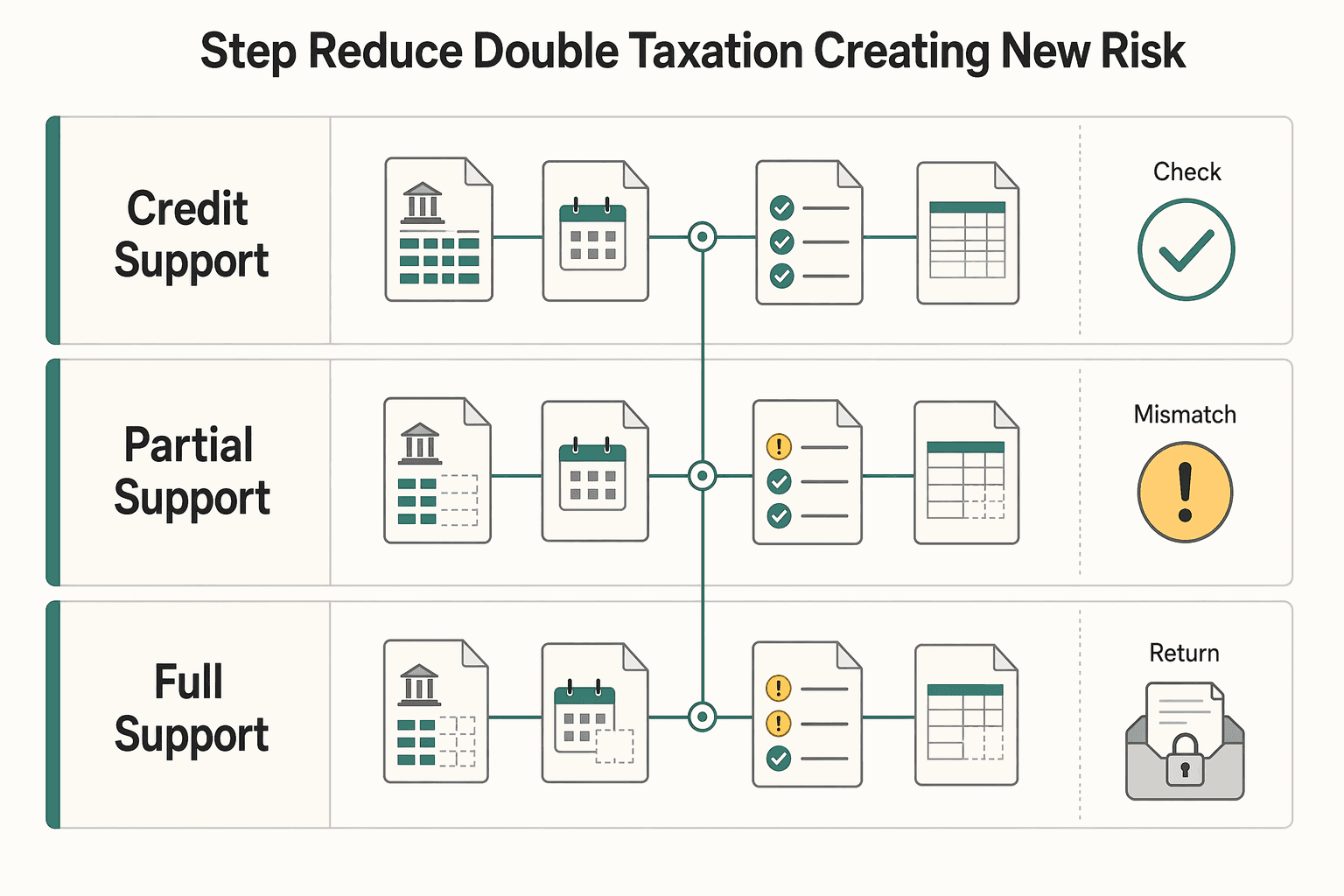

Step 4 reduce double taxation without creating new risk#

Use a strict rule before you file: claim a foreign tax credit only when the foreign tax is clearly tied to the same foreign rental income stream in your U.S. return.

The safest mindset is that each claimed credit amount needs its own support story. You should be able to show what the foreign charge was, what period it covered, whether your file treats it as paid or accrued, and how it connects to the rental income reported in the United States. If any link in that chain is weak, the claim should shrink to the supported amount or wait.

Start by classifying taxes correctly. The credit is generally for foreign income, war profits, or excess profits taxes, not every charge on a foreign statement. Then confirm source matching: the credit can offset U.S. tax on foreign-source income, not U.S.-source income. Descriptions matter here. A foreign document can contain several charges that look similar, so keep the description and, if needed, a translated description with the support file.

A disciplined workflow helps here. First identify the foreign tax item. Then match it to a covered period. Then match that period to the income stream in your U.S. file. Only after you can see those links should the amount move into the credit calculation. That sequence reduces the chance that a tax payment gets claimed simply because it appears on a foreign statement with the property name on it.

| Support level | Filing move | Tradeoff |

|---|---|---|

| No credit support | Do not claim the credit | Higher current tax, lower adjustment risk |

| Partial support | Claim only the documented portion tied to the same covered period | Lower current benefit, cleaner defense |

| Full support | Claim the full amount only when payment, period, and income linkage all match | Maximum supportable claim |

This table is not about being timid for the sake of it. It is about avoiding a weak claim that creates more cleanup work than the benefit was worth.

If you choose credit treatment for qualified foreign taxes for the year, apply that treatment consistently. Form 1116 is generally used, and mechanics matter: report amounts in U.S. dollars except where the form says otherwise, use a separate form for each income category, and check only one category box per form. Do the category split before finalizing totals so you do not have to break apart a combined number later.

Keep the documentation path simple. For each amount you plan to claim, keep the foreign record, the USD conversion entry, the covered period, and the worksheet reference to the related income stream together. If those records are scattered across several folders, the credit may still be valid, but your ability to prove it quickly gets worse. That is a risk you can control before filing.

Check the FEIE boundary before filing. If income is excluded under Form 2555, do not claim a foreign tax credit for taxes tied to that excluded income. Keep the earned-income file and the rental-income file distinct enough that the same amount is not pulled into both analyses by accident. Separate labels help here. So does a short note explaining why a given tax item belongs in the rental credit file rather than the earned-income file.

Checkpoint before submit: for each credit amount, keep the foreign tax record, translated description if needed, matching period coverage, and a direct tie to the same income period in your U.S. file.

Step 5 handle related compliance layers people forget#

A clean Schedule E does not finish the job; you still need a separate information-reporting check before you file.

International reporting mistakes often happen at the end because the income return feels complete. That is exactly when you should pause. Reporting the income correctly and satisfying separate information-reporting rules are related tasks, but they are not the same task.

Start with Form 8938. It is attached to your U.S. tax return, it is threshold-based, and the threshold depends on filer type. A common baseline for some filers is aggregate specified foreign financial assets above $50,000, while higher thresholds can apply for some joint filers and taxpayers living abroad. If you are not required to file an income tax return for the year, Form 8938 is not required for that year.

Pre-submit sequence:

- Confirm whether you are a specified individual and whether an income tax return is required.

- Inventory potentially reportable items, including foreign financial accounts and other specified foreign financial assets.

- Apply the threshold rules that match your filing status and residency facts.

- Treat

FBARandForm 8938as separate reporting tracks, and document each status separately. - Escalate early if ownership structure, treaty position, or multi-country residency makes the filing posture unclear.

The common failure is not just missing a form. It is assuming that because the rental income appears on Schedule E, every related international filing question is automatically settled. It is also common to borrow a threshold that applied to someone else and force it onto your own facts. Both mistakes come from skipping the separate review.

A simple control is a one-page status grid with required, not required, and escalated, plus a short reason for each item. Keep that grid in the same return file so the final status does not live only in memory or a separate message thread. If your facts change during review, update the grid right away rather than waiting until the end. A stale status sheet is almost as bad as having none because it makes the file look settled when it is not.

This step is also where you make sure no open international item is hiding behind a completed income return. If something is unclear, write it down plainly and route it for review. Silence is not resolution.

Common mistakes and how to recover before filing season closes#

You can still recover late if you fix one error path at a time and keep only positions you can document.

| Mistake | Recovery | Follow-up |

|---|---|---|

| Using FEIE logic to exclude rental activity | Map rental activity back to Schedule E (Form 1040), and use Form 2555 only for foreign earned income analysis | Review whether any foreign taxes were incorrectly paired with excluded income and rerun the tie-out from the worksheet forward |

| Inconsistent USD conversions across rent and expenses | Rebuild one conversion ledger and recalculate end to end | Retie every affected entry to that ledger and review the whole chain if one major total changed |

| Weak support for the foreign tax credit | Limit the credit to documented amounts and rebuild Form 1116 with clean separation by income category, with country-by-country detail where applicable, in U.S. dollars | Reconcile period coverage before claiming the amount |

| Treating FBAR/FATCA as covered just because income is reported | Run a separate final FinCEN and Form 8938 review before filing | Record whether each track is complete, not required, or escalated |

- Mistake: using FEIE logic to exclude rental activity.

Recovery: Map rental activity back to Schedule E (Form 1040), and use Form 2555 only for foreign earned income analysis. The 330 full days in 12 consecutive months test is a FEIE qualification route, not a broad filing exemption. After remapping, review whether any foreign taxes were incorrectly paired with excluded income and rerun the tie-out from the worksheet forward. Do not stop once the income is back on the right form; make sure all related calculations now reflect that correction.

- Mistake: inconsistent USD conversions across rent and expenses.

Recovery: Rebuild one conversion ledger, recalculate end to end, and retie every affected entry to that ledger. The fix is not finished until the same conversion logic appears everywhere the property numbers flow. If the rebuilt ledger changes one major total, assume downstream totals changed too and review the whole chain instead of only the line that first looked wrong.

- Mistake: weak support for the foreign tax credit.

Recovery: Limit the credit to documented amounts and rebuild Form 1116 with clean separation by income category, with country-by-country detail where applicable, in U.S. dollars. If the period coverage does not match the income in your U.S. file, reconcile that before you claim the amount. Where support is only partial, file the partial claim you can defend rather than stretching to a full number that the file cannot carry.

- Mistake: treating FBAR/FATCA as covered just because income is reported.

Recovery: Run a separate final FinCEN and Form 8938 review before filing. Record the result in writing so the file shows whether each track is complete, not required, or escalated. The written result matters because memory is least reliable at the end of filing season, which is exactly when overlooked items tend to slip through.

The order of repair matters. Fix classification first, then conversions, then credit support, then related information reporting. If you reverse that order, later corrections can force you to redo the earlier work because the numbers or categories changed underneath it.

If you change classification, conversion, or credit support, rerun all downstream tie-outs. Partial fixes are where late errors multiply. The file should show one corrected story from the top, not a mixture of old and new judgments stitched together under deadline pressure.

Checkpoint before submission: corrected Schedule E mapping, one USD conversion ledger, Form 1116 support by category (and country where applicable), and written status for FinCEN and Form 8938 review.

Copy and paste filing checklist#

Use this as your final pre-submit gate: make sure every number is traceable, every form choice is intentional, and every gray area is either documented or escalated.

- Confirm filing scope. If you are filing as a U.S. citizen or resident alien, confirm worldwide-income reporting is applied and your foreign rental activity is included.

- Lock your base numbers. Freeze your USD ledger and make sure rent, expenses, and any claimed depreciation all have support in your working papers.

- Tie numbers across the return package. Confirm rental-related figures are consistent everywhere they appear in your U.S. return.

- Run the FEIE boundary check. If

Form 2555is in your file, confirm it is used only for foreign earned income and housing exclusion/deduction calculations. - Validate foreign tax credit mechanics. If you claim a

foreign tax credit, confirmForm 1116is in U.S. dollars, uses one income-category box per form, and separates countries or territories as required. - Review parallel reporting items. Check

FBARandForm 8938separately, and mark each as complete, not required, or escalated. - Flag state exposure and unresolved items. Add a short state note, including

California/FTBstatus when relevant, and escalate unresolved residency, treaty, or ownership issues. - Apply an authority filter. If a position relies on informal summaries, check it against current IRS forms/instructions; treat LB&I practice unit language as informational, not binding law.

A few final operating rules make this checklist work better in practice. Do not leave placeholders in the file once you start final review. Do not let an unsupported number survive just because the net result looks reasonable. And if an unresolved item is still marked UNKNOWN, make an explicit choice to escalate it rather than letting it disappear in the last round of edits.

One more practical step helps: review the checklist in the same order every time. Start with scope, then numbers, then form placement, then credits, then parallel reporting. A fixed order makes omissions easier to spot because you know what should come next. It also keeps the final review from turning into random spot checks that miss the actual weak point.

Final check before submitting: pick five random numbers from the return and run a two-minute trace test for each back to worksheets and source records. If one fails, pause and fix the chain first.

Frequently Asked Questions

Do I owe U.S. tax on foreign rental income if I already pay tax abroad?

Yes, you still generally have U.S. reporting duties. U.S. citizens and resident aliens are taxed on worldwide income, and foreign tax paid may support a credit or deduction path but does not remove filing duties by itself. The safer approach is to report the rental activity first, then evaluate whether double taxation can be reduced with support you can defend.

Where exactly do I report foreign rental income on my U.S. return?

Report foreign rental real estate activity on Schedule E (Form 1040), Part I. Keep the worksheet, conversions, and source records aligned so each rent, expense, and depreciation amount can be traced back without guesswork. A correct form with weak support is still a fragile filing position.

Does FEIE or the foreign housing exclusion let me exclude rental income?

Do not assume that rental income can be excluded that way. Form 2555 is used for the foreign earned income exclusion and housing exclusion or deduction for qualifying foreign earned income, and that income is still reported on a U.S. return. Keep rental activity separate from wages, self-employment income, and other earned compensation.

Can I claim the foreign tax credit on rental income every time?

No, not automatically. You need correct Form 1116 mechanics, including separate forms by income category, one category per form, and U.S. dollar reporting except where Part II says otherwise. You also need support tying the foreign tax to the same rental income stream and covered period in your U.S. file.

Do I need FBAR or Form 8938 if the property is foreign but income is on Schedule E?

Treat them as separate checks from income reporting. Form 8938 is threshold-based, and FBAR should be reviewed on its own track before filing. A foreign property and a completed Schedule E do not by themselves answer whether an information return is required.

When should I hire a CPA or tax attorney instead of filing solo?

Get professional help when Form 2555 eligibility is unclear, Form 1116 categorization is uncertain, or your support is incomplete across forms. It is also worth escalating when ownership structure, treaty position, or multi-country residency makes the filing posture unclear. A short pre-filing review can be safer than fixing a preventable amendment later.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Confidentiality vs. NDA: What's the Difference for Freelancers?

You are not really choosing a label. You are choosing a structure and timing that fit the relationship and the phase of work. The point isn't "clause vs. NDA" - it's using the right tool at the right point in the engagement.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.