Quick Answer

A foreign-issued life insurance policy can create three separate U.S. tax issues: Section 4371 excise tax on premiums, Section 7702 income-tax classification, and reporting on Form 720 and possibly FBAR or Form 8938. Keep those tracks separate, verify the policy contract and issuer, and document the premium payment chain before deciding what to file.

Start here if you own a foreign life insurance policy#

If you own a foreign-issued policy as a U.S. taxpayer, separate the work into three lanes. One is potential IRC Section 4371 excise tax. Another is income-tax classification under IRC Section 7702. The third is potential reporting obligations, including Form 720 and, depending on your facts and thresholds, FBAR and Form 8938. Keeping those lanes separate is the easiest way to avoid filing mistakes.

This guide is for U.S. citizens and resident aliens, including globally mobile freelancers and consultants. If that is you, worldwide income is still in scope even while you live abroad. A foreign-issued policy can still create U.S. tax or reporting work.

Before you decide anything, pull the actual documents: the policy contract, insurer identity, issuing jurisdiction, and current statements. Do not rely on memory when classification or filing duties are in question.

| Track | Core question | Authority or form | What to confirm |

|---|---|---|---|

| Excise tax | Could Section 4371 apply to premiums paid to a foreign insurer or reinsurer? | IRC Section 4371, Form 720 | Issuer status, policy facts, premium payments |

| Income-tax classification | How is the contract treated for U.S. tax purposes? | IRC Section 7702 | Contract terms and classification facts |

| Reporting | Do foreign-account or foreign-asset reporting rules also apply based on ownership and thresholds? | FBAR, Form 8938 | Account or asset values, ownership, applicable thresholds |

Use one lane to answer one lane. Form 720 does not resolve income-tax classification. Section 7702 treatment does not by itself resolve Section 4371 exposure. Reporting duties can still exist even when there is no current taxable income from the policy.

This is an operational guide, not legal advice. If treaty relief may apply, treat it as a procedural claim that must be established through the IRS exemption process, not as automatic. If your facts are mixed or unclear, involve a qualified tax professional such as an attorney, CPA, or enrolled agent before you file. For related context, see A Deep Dive into the Foreign Tax Credit (Form 1116).

Confirm whether this topic applies to you#

Use a simple stop rule at the outset: if you cannot document your taxpayer status, policy type, and issuer location, pause before making filing assumptions.

Confirm your taxpayer status#

Confirm your taxpayer status for the year and keep the documents behind the status you are using. If that is still unclear, stop here and resolve status first.

Confirm what the contract is and who issued it#

Read the policy contract itself to confirm what the contract is and who issued it. In this context, a policy of insurance can include an annuity contract, a policy of reinsurance, or an indemnity bond, not just something labeled life insurance.

For IRC Section 4371, applicability depends on three required elements: a policy of insurance, insurance of a U.S. risk, and issuance by a foreign insurer or reinsurer. Use the contract, current statements, and insurer correspondence to verify product type and issuer facts before you move forward. The IRS Foreign Insurance ATG can help with terminology, but it is not binding law.

Stop if you cannot prove policy type or issuer location#

Apply a hard stop if you still cannot prove policy type or issuer location from documents. Offshore insurance products can be technical and individualized, and insurance is not defined by federal statute for tax purposes, so classification can be unclear.

Before you proceed, gather the items below:

- the full policy contract

- the insurer's legal name

- the issuing jurisdiction shown in contract documents or insurer correspondence

- any rider or schedule that changes payout mechanics

- recent statements showing the contract is in force

If any of those core facts are missing, the next step is document collection, not filing improvisation. Related: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Gather the minimum document set before making tax calls#

Once you know this topic may apply, build a minimum evidence file before you make any tax call. That file should let you test policy classification, payment path, and overlapping reporting without guessing.

| File component | What to include |

|---|---|

| Core policy records | Full contract, riders or schedules, premium statements, cash-surrender or cash-value history, and insurer correspondence showing the legal issuer name and jurisdiction |

| Prior filings | Form 720, Form 8938, FinCEN Form 114, and any related foreign-asset disclosures already filed |

| One-page fact sheet | Policy owner, insured person, beneficiary if relevant, premium payer, funding account, remittance path, insurer jurisdiction, and any intermediary jurisdiction |

| Source-quality notes | IRS forms, instructions, and primary IRS pages as primary materials; the IRS Foreign Insurance ATG as context only |

| Unknowns list | Unresolved cash-surrender status, uncertain true issuer, or unclear funding path |

Collect the core policy records#

You need the full contract, riders or schedules, premium statements, cash-surrender or cash-value history, and insurer correspondence showing the legal issuer name and jurisdiction.

Do not treat screenshots or marketing summaries as enough. If you cannot trace the in-force policy to signed contract documents and recent statements, stop and finish document collection first.

Cash value is a key checkpoint. IRS Form 8938 guidance includes foreign-issued insurance or annuity interests with cash-surrender value as a reportable asset type, subject to the form's rules and thresholds. IRS FBAR materials also include insurance or annuity policies with cash value among covered account types. Do not assume every policy automatically triggers either filing.

Pull prior filings that may already reflect this policy#

Pull prior filings that may already reflect the policy: Form 720, Form 8938, FinCEN Form 114, and any related foreign-asset disclosures already filed.

Use that review to spot treatment drift and contradictions before they repeat across years. Form 720 is used to report and pay listed excise-tax liability. FBAR is filed with FinCEN rather than the IRS. IRS guidance is also clear that Form 8938 and FBAR can both be required.

Create a one-page fact sheet#

On one page, list the policy owner, insured person, beneficiary if relevant, premium payer, funding account, remittance path, insurer jurisdiction, and any intermediary jurisdiction.

This matters for Section 4371 because liability attaches when premium payment is transferred to the foreign insurer or reinsurer. If payment moved through a business account, family member, or intermediary, flag that clearly.

Add source-quality notes and keep an unknowns list#

Add source-quality notes so you know what can support your position. Treat IRS forms, instructions, and primary IRS pages as primary materials. Treat the IRS Foreign Insurance ATG as context only, because it is explicitly not an official pronouncement of law.

Keep an "unknowns" list, such as unresolved cash-surrender status, uncertain true issuer, or unclear funding path, and do not fill gaps with assumptions. Keep records that support return positions, claims, and exemptions for at least 4 years. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

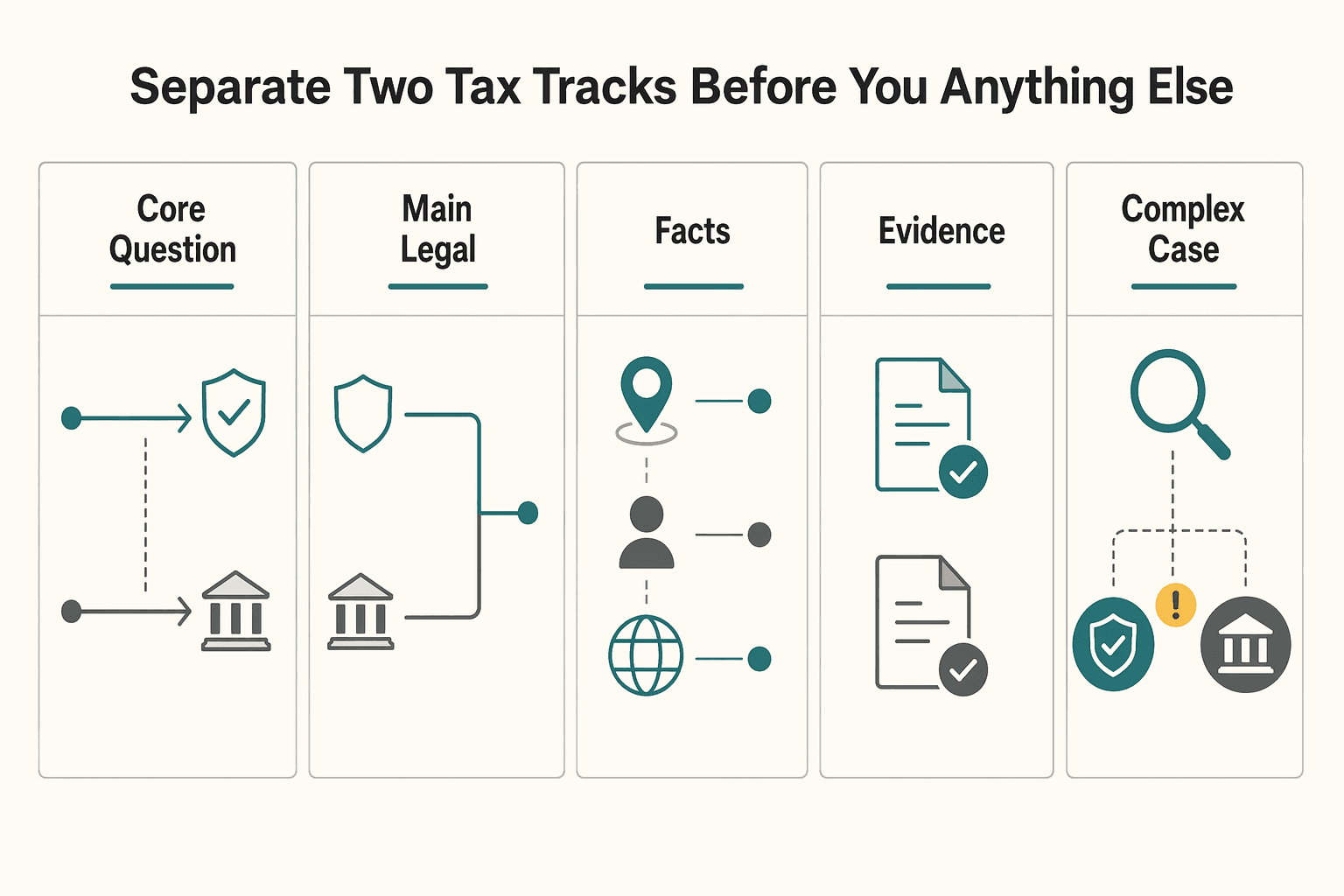

Separate the two tax tracks before you do anything else#

Before you start applying rules, split the issue into two parallel questions. Track A is premium-level excise-tax exposure under IRC Section 4371. Track B is income-tax classification under IRC Section 7702. Treating one track as if it answers the other is where many mistakes begin.

| Decision point | Track A: IRC Section 4371 excise tax | Track B: IRC Section 7702 income-tax classification |

|---|---|---|

| Core question | Did premiums paid to a foreign insurer or reinsurer create U.S. federal excise-tax exposure? | Does the contract qualify as a life insurance contract for federal income-tax purposes? |

| Main legal hook | IRC Section 4371 applies tax to certain insurance-related instruments issued by foreign insurers or reinsurers. For life, sickness, accident, and annuity contracts under Section 4371(2), the statute states 1 cent on each dollar of premium paid. | Section 7702 defines "life insurance contract" for federal tax purposes. A contract must satisfy the cash value accumulation test, or meet guideline premium requirements plus the cash value corridor requirement. |

| What makes it live | Issuer status, U.S.-risk facts, and who paid the premium are key. Regulations for life and annuity scope refer to risks tied to a U.S. citizen or resident. | Contract terms and policy economics drive the analysis. If the contract fails Section 7702(a), Notice 2007-15 says income on the contract can be treated as ordinary income. |

| Known vs unknown | The Foreign Insurance Audit Techniques Guide says foreign insurance excise-tax analysis requires three elements, but the ATG also says it is not an official pronouncement of law and cannot be relied on as legal authority. Use it as a checklist, then anchor conclusions in the Code, regulations, and your records. | The statute provides the test, but foreign product labels do not settle the result. A policy marketed abroad as life insurance may still require full Section 7702 analysis. |

| Practical output | The return path is Form 720, with foreign insurance tax listed as IRS No. 30. Keep records that support contract details, premium payments, remittance proof, transfer dates, and payer identity for at least 3 years from when any tax became due. Escalate if issuer status, U.S. risk, or payment chain is unclear. | The output is income-tax return treatment analysis, not Form 720. Keep contract terms and policy value history supporting Section 7702 treatment. If support is weak or missing, get professional review before filing. |

Apply one hard rule: never assume paying excise tax settles income-tax treatment, and never assume Section 7702 qualification removes all excise-tax questions. These are parallel tracks.

For Track A, verify the premium-by-premium transfer date, foreign recipient, and who made payment. Regulations tie return-based payment responsibility to the person who pays the premium and attach liability when payment is transferred. For Track B, verify that you can support Section 7702 treatment from contract terms and policy data. If you cannot, treat the issue as unresolved and escalate before filing.

Close this step with a two-line file memo:

- "Section 4371 status: pass, fail, or unresolved; Form 720 action if applicable."

- "Section 7702 status: supportable, unsupported, or unresolved; income-tax review required if unresolved."

For a step-by-step walkthrough, see A guide to the Foreign Account Tax Compliance Act (FATCA) for individuals.

Run the IRC Section 4371 applicability test in order#

For Track A, use a strict go/no-go rule: you need document support for all three IRC Section 4371 elements. If even one element is unclear, do not treat the result as "no tax"; mark it "unresolved" and escalate.

Confirm there is a policy of insurance#

Start with the insurer-issued contract as your core evidence. The IRS Foreign Insurance Audit Techniques Guide says a policy of insurance may include a policy of reinsurance, an indemnity bond, or an annuity contract. It also describes a policy as the printed document issued by the insurer.

Your checkpoint is practical: identify the parties and the operative terms in the actual contract. If you only have a brochure, portal screenshot, broker email, or transfer memo, treat this element as unresolved.

Test the U.S. risk element without guessing#

Treat this element as high-priority and evidence-driven. U.S. risk is one of the three required elements, and all three must be present for foreign insurance excise tax to apply.

Build a compact evidence pack from records you already have, such as the policy, application, schedules, endorsements, insurer correspondence, and a one-page fact sheet with owner, payer, remittance path, and jurisdictions. If those records conflict or leave material gaps, mark this element unresolved and escalate before concluding the element is met.

Verify the issuer is a foreign insurer or foreign reinsurer#

Confirm the legal issuing entity, not just a brand name or sales channel. Reinsurance can add a second layer, and the ATG describes reinsurance as the first insurer transferring the same risks to another insurer, with the second insurer as the reinsurer.

Match the legal entity named in the policy to the premium recipient and related contract documents. If names do not align across the policy packet, bank instructions, and servicing communications, treat the element as unresolved until the chain is clear.

Record pass, fail, or unresolved for each element#

Write the decision in your file so the analysis is auditable, using a table like this:

| Element | Status | Evidence to cite |

|---|---|---|

| Policy of insurance | Pass / Fail / Unresolved | Insurer-issued contract, issue date, named parties, contract terms |

| U.S. risk | Pass / Fail / Unresolved | Policy schedules, application, endorsements, jurisdiction facts, insurer correspondence |

| Foreign insurer or foreign reinsurer | Pass / Fail / Unresolved | Legal issuer name in policy, premium remittance details, related contract documents |

Use the ATG as an operational checklist for the three-element test, not as binding authority. Anchor your conclusion in your own records, and if any box is unresolved, escalate before making a go/no-go decision.

Classify the policy under IRC Section 7702 and screen for PFIC exposure#

Once the Section 4371 screen is done, open a separate income-tax track. The excise result does not decide whether the contract qualifies as life insurance under IRC Section 7702, and mixing those questions can create avoidable errors.

Separate the Section 7702 question from the excise question#

Treat IRC Section 7702 as a standalone classification exercise. For federal income-tax treatment, the contract must satisfy a Section 7702 statutory path. That is a different question from whether premiums are exposed to excise tax under IRC Section 4371.

Build this file from the insurer-issued contract, riders, and annual cash value statements. If your file is mostly marketing materials or portal summaries, mark the classification unresolved and escalate. Use the Foreign Insurance ATG as a fact-gathering aid only, not as controlling law.

Test whether the contract can be supported under IRC Section 7702#

Start with the two statutory routes and identify which one the contract is meant to satisfy:

- Cash value accumulation test.

- Guideline premium requirements plus cash value corridor.

Your job is to confirm support, not to reverse-engineer actuarial calculations. If the records do not clearly support either route, do not assume qualification.

Use a conservative rule here: if qualification cannot be supported, treat annual income inclusion risk as live until reviewed. IRS guidance states that if a contract does not meet Section 7702, contract income for the year is treated as ordinary income to the policyholder.

Screen for PFIC exposure when the structure looks investment-heavy#

Run a separate PFIC screen if the documents suggest direct or indirect exposure to a foreign corporation. Under IRC Section 1297, PFIC status is based on either the 75 percent passive-income test or the 50 percent passive-asset test.

Do not assume every foreign life insurance policy is a PFIC. But do not ignore PFIC risk when the structure includes a foreign corporate layer or entity-level investment reporting.

If shareholder treatment may exist, Form 8621 risk is live. Direct or indirect PFIC shareholders must file, and filing is required per PFIC.

| Likely policy pattern | Section 7702 read | PFIC red flags | Documents needed for defensible treatment |

|---|---|---|---|

| Protection-focused policy with limited cash value features | May be simpler, but still needs support under a Section 7702 route | No clear foreign corporate ownership in the current file | Full policy, riders, annual statements, insurer correspondence |

| Cash value policy with insurer support for qualification | Potentially supportable if records show the applicable Section 7702 route | Wording that points to underlying entities or ownership interests | Policy, cash value history, insurer support for the intended Section 7702 route |

| Investment-heavy arrangement with foreign corporate exposure | May remain unresolved without deeper review | Direct or indirect foreign corporate ownership indicators, entity-level statements | Full contract packet, ownership documents, entity statements, PFIC and Form 8621 review if applicable |

Record pass, fail, or unresolved for both tracks#

Write both decisions in your memo: one line for Section 7702 and one line for PFIC screening, each marked pass, fail, or unresolved, with supporting documents listed.

If either line is unresolved, keep the income-tax issue open. If the policy, statements, and ownership records do not align, escalate before filing on an assumed treatment.

You might also find this useful: A Deep Dive into PFIC Rules for US Expats Investing Abroad.

Decide who is responsible for payment and filing#

Do not leave Form 720 ownership vague. If your IRC Section 4371 three-element screen is live, you need one clear answer on who files, who pays, and who keeps proof.

Map the actual premium payment chain#

Start with money movement, not policy language. Your key question is who actually paid the premium and where funds left the U.S. side of the chain.

| Checkpoint record | What to match |

|---|---|

| Premium notice or billing statement | One real premium used as the checkpoint |

| Bank or wire confirmation | The sending account |

| Broker or platform remittance record | Any intermediary or broker |

| Insurer receipt or account posting | The foreign insurer that received the premium |

Write one line from source to destination: policy owner, funding account, any business entity, any intermediary or broker, and the foreign insurer that received the premium. Form 720 instructions say filing applies when a party is liable for, or responsible for collecting, listed excise tax, so identify all parties before assigning responsibility.

Use one real premium as the checkpoint and match the records below:

- premium notice or billing statement

- bank or wire confirmation showing the sending account

- broker or platform remittance record

- insurer receipt or account posting

If these records do not tell one consistent payer story, treat filing responsibility as unresolved.

Identify the likely filer, then flag gray areas early#

In many cases, the likely filer is the party making the premium payment. Use that as a practical starting point, not as a blanket legal rule.

If records show one clean path from a U.S. person or entity to the foreign insurer, that party is your first Form 720 candidate. If multiple parties touch the funds, do not assume the filer; document why your selected filer is the most defensible based on payment records. Keep the cadence in view: Form 720 is quarterly, not a one-time annual cleanup.

Separate insurer statements from actual tax liability#

If the foreign insurer says it "handles the tax," treat that as a claim to verify. Insurer communications do not automatically transfer legal filing or payment liability.

Ask for proof you can retain, not reassurance: what they remitted, the basis they relied on, the period covered, and evidence that payment was made. If they cannot provide that, keep liability open. Treat the Foreign Insurance ATG as a fact-gathering aid here, not as controlling law.

Assign one named owner and document the control#

Assign one named person to own the quarterly calendar, payment confirmation, and proof retention.

Keep a minimum evidence pack: remittance map, responsibility memo, filed Form 720 copies if any, payment confirmations, and insurer correspondence you relied on. The control test is simple: can that owner produce a full quarter file without rebuilding it from inbox searches?

Escalate early if personal and business accounts are both used, multiple entities fund the same policy, or payer identity changes by quarter. If the file supports more than one payer story, mark it unresolved and get professional review before the next quarter closes.

Related reading: How to Handle Tax on Employee Stock Purchase Plans (ESPP) as an Expat.

Build a quarterly evidence pack you can defend#

Build the file each quarter, not at year end. A defensible pack should let someone trace one premium from the policy record to the transfer event to Form 720 treatment without guessing at your assumptions.

Create one folder per quarter and keep a fixed structure#

Use the same folder structure each period. Include Form 720 workpapers, premium remittance records, policy statements, insurer correspondence, and a short decision memo.

Make sure each file shows which policy, which premium, which foreign insurer, and which transfer date. That transfer evidence is central because liability under IRC Section 4371 attaches when the premium payment is transferred.

Keep source documents, not just summaries. Store bank confirmations, broker remittance notices, and insurer receipts, and retain required records for at least 3 years from when any part of the tax became due.

Reconcile policy records to return totals and log assumptions#

Reconcile policy-level data to reporting-level totals each quarter so every Form 720 amount can be traced. For each premium you include or exclude, capture:

- policy or contract identifier

- gross premium paid

- foreign insurer identity

- transfer date

- reporting treatment and reason

Log any assumptions tied to IRC Section 4371 or IRC Section 7702 in plain language. If someone reviews the file later, they should be able to see why a premium was included, excluded, or classified the way it was.

Track treaty questions as open items with owners and deadlines#

If an income tax treaty may affect treatment, track it as an open item with a named owner and deadline. Do not treat a premium as exempt just because the insurer is in a treaty country or appears on an IRS list.

The IRS states that exemption can depend on whether a closing agreement was in effect for that period. It also says published lists are not conclusive proof of valid closing-agreement status. If that status is unverified before filing, keep the issue open and escalate.

Preserve traceability if you use Gruv workflows#

If you use Gruv workflows where enabled, retain exports, timestamps, and audit trails showing who updated payment-path records, classification notes, or filing decisions.

Treat Gruv records as supporting evidence, not as a substitute for required legal recordkeeping. The final check is simple: one quarter folder should show the full chain from policy premium to transfer event to reported treatment, including unresolved treaty or classification items.

If FBAR tracking is part of your broader tax workflow, run a quick records check with the FBAR Calculator.

Handle overlapping reporting without double counting or omission#

Use one sequencing rule here: classify the policy first, test each form separately, then reconcile the totals before filing. That avoids the two common mistakes: assuming one form covers another or reporting the same policy inconsistently across forms.

Finish policy classification before mapping any form#

Do not start in Form 8938 or FBAR. Start with the policy facts: owner, cash-value or account-like features, insurer, and your federal classification.

Before you populate any form, make sure your contract, current statement, and decision memo can answer two questions clearly. Does the policy have cash value or similar account value? Is it already being reported elsewhere for federal purposes? If either point is unclear, resolve it first.

Test Form 8938, FBAR, and FATCA logic separately#

Form overlap is common, but the filing duties are separate. Filing Form 8938 does not replace FBAR, and FBAR, FinCEN Form 114, is filed with FinCEN rather than with the IRS.

| Filing item | What it is | What to test from your policy file |

|---|---|---|

| Form 8938 | IRS form filed with your tax return for specified foreign financial assets when thresholds are met | Whether the policy is in scope and whether your threshold is met. For unmarried or MFS filers living in the U.S.: more than $50,000 at year end or more than $75,000 at any time. For unmarried or MFS filers living outside the U.S.: more than $200,000 at year end or more than $300,000 at any time. |

| FBAR (FinCEN Form 114) | Foreign account report filed through FinCEN | Whether the policy is an insurance or annuity product with cash value that falls within FBAR account scope, and whether aggregate foreign accounts exceeded $10,000 at any time during the calendar year. |

| FATCA for U.S. taxpayers | Regime requiring certain U.S. taxpayers to report foreign financial assets to the IRS on Form 8938 | Treat this as Form 8938 logic, not as a substitute for separate FBAR testing. |

Also apply Form 8938 anti-duplication rules where they apply. That is Form 8938-specific and does not remove the need to test FBAR separately.

Reconcile the same data under different form logic#

Run one cross-form checkpoint before filing: same data, different form logic. Owner, policy number, insurer, and valuation support should match across workpapers even when form rules and timing tests differ.

Your file should show which value was used on each form, which date convention applied, and why. This is where you catch contradictions before they turn into filing errors.

Flag California only when residency makes it relevant#

Do not let federal form assumptions flow into state treatment automatically. Based on this section's sources, do not treat California as having a direct FBAR or Form 8938 equivalent.

If California or FTB exposure exists, add a state note with residency periods and when policy-related income or events occurred. California residents are taxed on worldwide income, and part-year treatment splits worldwide income while resident from California-source income while nonresident.

This pairs well with our guide on How to Handle Tax Form 8938 Without Missing FBAR.

Common failure modes and how to recover fast#

Many issues start when one shortcut is used for two different tax tracks. A practical recovery path is to recheck classification, rebuild quarterly controls, then reconcile filings from one evidence pack before you file or amend.

| Failure mode | Recovery |

|---|---|

| Treating all foreign policies the same | Rerun IRC Section 7702 and IRC Section 4371 separately |

| Filing once and forgetting later quarters | Install recurring Form 720 controls and update your evidence pack each quarter |

| Relying on marketing summaries when sources conflict | Re-anchor to primary IRS and IRC materials, and label unknowns clearly |

| Missing cross-form consistency | Reconcile Form 8938, FBAR, and supporting records before submission |

- Failure mode: treating all foreign policies the same. Recovery: rerun IRC Section 7702 and IRC Section 4371 separately.

IRC Section 7702 and IRC Section 4371 answer different questions, so do not treat one result as a substitute for the other. The IRS audit guide says Section 4371 applies only when all three elements are present, including U.S. risk and issuance by a foreign insurer or reinsurer. Document each track as pass, fail, or unresolved. If a Section 4371 element is not proven, mark it unresolved instead of assuming there is no excise issue.

- Failure mode: filing once and forgetting later quarters. Recovery: install recurring Form 720 controls and update your evidence pack each quarter.

Form 720 is quarterly, not annual. Keep deadlines on your calendar for April 30, July 31, October 31, and January 31, and refresh your file each quarter with premium records, payer name, policy number, and the current decision memo. If you missed periods, rebuild the history quarter by quarter first, then decide what to file or correct. If you made the premium payment, do not rely only on an insurer note that it "handles tax," because the regulation places primary return responsibility on the payer.

- Failure mode: relying on marketing summaries when sources conflict. Recovery: re-anchor to primary IRS and IRC materials, and label unknowns clearly.

When guidance conflicts, anchor first to the Internal Revenue Code and IRS filing materials. The Foreign Insurance Audit Techniques Guide can help with context, but it says it is not an official pronouncement of law and cannot be relied on as binding authority. If a point is still unclear after primary-source review, record it as unknown and escalate only that issue.

- Failure mode: missing cross-form consistency. Recovery: reconcile Form 8938, FBAR, and supporting records before submission.

Use one consistency check: same owner, same policy, same source records, separate filing tests. IRS states that Form 8938 does not replace FBAR, and FBAR is filed with FinCEN rather than with the IRS. Confirm that insurer name, policy number, and valuation support align across workpapers, then run each threshold test separately and determine whether either or both filings are required. Treat any value you cannot reproduce from support records as a stop-and-fix signal.

Need the full breakdown? Read How to Fill Out Form 1116 (Foreign Tax Credit).

Know when to bring in a professional#

Bring in a professional as soon as your position depends on interpretation more than on clear documentation.

Bring in help when you cannot document all 3 IRC Section 4371 elements#

Your file should clearly show pass, fail, or unresolved for a policy of insurance, insurance of a United States risk, and issuance by a foreign insurer or reinsurer. If any element is unproven, stop and get specialist review.

Also confirm product type before you conclude anything. In this context, a policy can include reinsurance, an indemnity bond, or an annuity contract.

Get review when interpretation carries the result#

If your outcome depends on interpretation beyond what your policy documentation and the three IRC Section 4371 elements clearly establish, do not file on assumptions. Get specialist review and document what is known versus unknown.

Escalate mixed or incomplete fact patterns early#

If your facts are mixed, incomplete, or internally inconsistent, move to specialist advice early instead of treating these as cleanup items later.

One final guardrail: use the Foreign Insurance Audit Techniques Guide for context, but do not treat it as binding authority on its own.

If key facts or filing details are still unclear, keep a dated timeline in the Tax Residency Tracker to make advisor review faster and cleaner.

Copy and use this quarterly checklist#

Use this as a quarterly control: confirm the facts, rerun the key analyses, and keep one evidence file you can defend without rebuilding it later.

Confirm what changed before touching forms#

Compare this quarter against your last fact sheet, including taxpayer status, policy details, values, payer and owner records, and supporting documents. If you cannot prove a fact is unchanged, treat it as changed and reopen the analysis.

Re-run your core tax workpapers#

Re-run your prior core tax workpapers using current-quarter records. Keep each conclusion with its support in the same place, including contract language, statements, remittance records, and correspondence. If support is thin, mark it unresolved instead of forcing a clean answer.

Test Form 8938 independently from your other form workflows#

Test Form 8938 independently from your other form workflows. Use current IRS materials and document what you relied on: the Form 8938 PDF, the linked instructions with the 11/2021 revision marker, and the IRS overview page date of 23-Jan-2026. The trigger is condition-based: file when the total value of specified foreign financial assets in which you have an interest is more than the appropriate reporting threshold.

Reconcile shared facts across Form 8938 and related filings#

Reconcile shared facts across Form 8938 and related draft or prior filings. Core identifiers and ownership or value facts should not conflict across forms. Use a one-page reconciliation sheet and resolve fact conflicts before finalizing anything.

Log unknowns early#

Log unknowns early. Track each open item with an owner, required evidence, and decision deadline, then escalate anything that could change whether or how you file. Unknown threshold inputs for Form 8938 are an escalation item because the filing decision depends on the appropriate reporting threshold.

Store each quarter in one audit-ready folder#

Store each quarter in one audit-ready folder. Include filed returns, workpapers, payment proof, statements, valuation inputs, exchange-rate support, decision memos, open-items log, and key correspondence. This reduces audit friction and makes next quarter an update rather than a rebuild.

Frequently Asked Questions

Is there tax on foreign life insurance premiums for U.S. taxpayers?

Possibly. The article says Section 4371 can apply when three elements are present: a policy of insurance, insurance of a U.S. risk, and issuance by a foreign insurer or reinsurer. For life, sickness, accident, and annuity contracts, the stated rate is 1 cent on each dollar of premium paid.

Who usually has to remit and file when premiums are paid to a foreign insurer?

The practical starting point is the person who actually pays the premium. If Section 4371 applies, that payer should be matched to quarterly Form 720 based on the payment records. Do not assume an insurer or broker removes your filing responsibility without proof.

Does meeting IRC Section 7702 automatically remove excise-tax exposure?

No. Section 7702 is an income-tax classification rule, while Section 4371 is a separate excise-tax analysis. The article says those determinations should be kept separate in your file.

What happens if my policy likely does not qualify under U.S. life-insurance rules?

Treat it as an income-tax issue, not just a form issue. The article says IRS guidance treats contract income as ordinary income if the contract does not meet Section 7702, and it also says to check PFIC and Form 8621 exposure separately.

Do I need both Form 720 and Form 8938 for the same policy year?

Sometimes, yes. Form 720 is a quarterly excise-tax return, while Form 8938 applies when specified foreign financial asset thresholds are met. The article says to test each filing regime independently for the same policy year.

How do FBAR and FinCEN reporting relate to foreign life insurance accounts?

FBAR is FinCEN Form 114 and is separate from your income tax return. If the policy is treated as a foreign financial account and your aggregate foreign financial accounts exceed $10,000 at any time during the year, you may need to file. Filing Form 8938 does not replace FBAR.

When should I stop DIY filing and hire an international tax professional?

There is no fixed universal cutoff in the rules described here. The article says to get professional help when key facts are uncertain, including U.S.-risk analysis under Section 4371, Section 7702 status, PFIC or Form 8621 exposure, or treaty-based Section 4371 exemption procedures.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

PFIC Rules for US Expats Investing Abroad

Start with compliance, not optimization. Screen PFIC risk before you buy, rebalance, or add cash. A common costly mistake is buying a familiar local fund first and checking PFIC classification later.