Quick Answer

Start by splitting every USDC action into three records: payment receipt, same-owner wallet move, and later disposal. For tax on usdc to ledger, the transfer into a Ledger wallet is tracked for ownership continuity, while taxable checks usually happen at receipt and at any sell, swap, or spend. Keep one evidence trail with payer details, timestamp, transaction hash, and valuation at receipt, then reconcile those records to Form 1040/Form 1040-SR reporting questions before filing.

Start here with the one rule that prevents most USDC tax mistakes#

For tax on usdc to ledger, one rule prevents most mistakes: treat each action as a separate event before you record anything. Filing problems often start when a client payment, a self-transfer to your Ledger hardware wallet, and a later sale or spend all get blended into one crypto line item.

| Bucket | Definition | Article action |

|---|---|---|

| Receipt | You received USDC as payment for services or property | Record the receipt as potential income first |

| Wallet movement | You moved the same asset between accounts or wallets you control | Check whether the movement was only a wallet transfer |

| Disposal | You sold, exchanged, or otherwise disposed of the asset | Flag any sell, swap, or spend as a disposal event |

Classify USDC correctly from the start. For U.S. tax purposes, digital assets are treated as property, not currency, and stablecoins are included as digital assets. If a client pays you in USDC, record it with digital-asset discipline, not like a simple bank deposit.

This guide is for freelancers paid in USDC who then move funds to Ledger, with a practical compliance focus. If your facts span countries, keep the same record discipline and then review tax residency for that period.

Split every action into one of three buckets before bookkeeping or return prep:

- Receipt

You received USDC as payment for services or property.

- Wallet movement

You moved the same asset between accounts or wallets you control.

- Disposal

You sold, exchanged, or otherwise disposed of the asset.

Receipt and disposal track the IRS digital-asset framing on Form 1040 and Form 1040-SR. Those forms ask whether you received a digital asset, or sold, exchanged, or otherwise disposed of one during the year.

If one on-chain flow reflects multiple real-world actions, split it into separate records anyway. For example, "paid by client, then moved to cold storage" should be tracked as distinct entries.

Anchor your classification to current official guidance. IRS digital-asset guidance is a main baseline for filing posture. The IRS virtual-currency FAQ page says its FAQs generally apply to transactions completed before Jan. 1, 2025, so do not rely on that page alone for newer activity.

Use the same caution with stablecoin legal commentary. A Federal Register prototype page for a proposed rule dated 03/02/2026 is not an official legal edition or final law, and that page says legal research should be verified against an official edition.

Set up a small evidence file before your first payment. Keep it simple, but make every entry defensible. At minimum, track:

- what happened: receipt, wallet movement, or disposal

- when it happened: date and timestamp used in your records

- who paid you or which wallet sent it

- which address or account received it

- transaction hash or platform reference

- tax residency notes for the relevant period

Quick control: for each USDC entry, write one sentence explaining why it belongs in that bucket. If your export does not clearly show whether an entry was payment, self-transfer, or disposal, pause and reconstruct it before filing.

Use this header note in your folder: "Classify first. Document second. File third." Related: Vancouver, Canada: The Ultimate Digital Nomad Guide (2025).

Classify every USDC movement before you touch your records#

Classify first, then record. For each movement, work in the same order every time: received as compensation -> wallet transfer -> disposal (sell/swap/spend).

Record the receipt as potential income first#

If the event is "a client paid me in USDC," start in the income bucket. Crypto received as compensation is generally treated as taxable income at fair market value when received. That is your first tax check, even if you move it to your Ledger wallet right after.

Keep receipt and storage as separate facts. The payment arriving is one event. Moving the same USDC to self-custody is another.

Checkpoint before booking the receipt: capture payer, receiving address or account, timestamp, and transaction hash or platform reference.

Check whether the movement was only a wallet transfer#

Once receipt is isolated, ask whether the move was between wallets or accounts you control. "Transfer between wallets" is its own review category and should be reviewed separately from income and disposal.

Treat this as both a classification check and an evidence check. Confirm your records support that the asset stayed USDC, the destination is on your ownership map, and the amount and timing reconcile as a single move, allowing for fees. If any part is unclear, pause and resolve it before filing.

Flag any sell, swap, or spend as a disposal event#

If it is not income and not a same-owner transfer, treat it as a disposal check. Selling, trading, or spending crypto can trigger gain or loss analysis, including for USDC.

USDC being designed around a 1:1 U.S. dollar ratio does not remove disposal analysis. Keep a separate disposal line with date, amount, what you received, and basis support.

| Action type | Likely tax treatment | Evidence you should keep | Filing impact in the United States | Outside the United States |

|---|---|---|---|---|

| Client paid you in USDC | Generally analyzed as income at fair market value when received | Invoice or contract, payer identity, timestamp, receiving address or account, transaction hash or platform reference | Potential income tax analysis at receipt | Jurisdiction-specific review needed |

| You moved USDC between wallets you control | Transfer review category; verify whether it was only a same-owner wallet move | Source and destination wallet records, ownership map, timestamps, transfer reference, amount reconciliation | Classification and recordkeeping review before deciding whether any taxable entry is required | Jurisdiction-specific review needed |

| You sold, swapped, or spent USDC | Disposal that can create gain or loss analysis using cost basis | Disposal timestamp, amount disposed, what you received, linked acquisition record, basis support | Potential capital gains tax analysis | Jurisdiction-specific review needed |

Split blended activity into separate line items#

One on-chain flow can still represent multiple tax facts. If you were paid in USDC and later moved it to your Ledger, book two lines: one receipt and one transfer.

Apply the same rule when a later spend, sale, or swap happens. Each action gets its own line item. A practical rule is one verb per line: received, transferred, or disposed. If a row needs "and then," split it.

Prepare your evidence pack before the first client payment lands#

Build the file before funds move so each payment can be traced from receipt through later movements.

| Evidence pack item | Key details | Control or note |

|---|---|---|

| Receipt bundle | Invoice or contract, payer identity, timestamp, receiving address or account, transaction hash or platform reference, and the fiat value recorded at receipt | One payment maps to one payer, one destination, one timestamp, and one transfer reference |

| Ownership map | Account or wallet name, owner, business use, and active receiving addresses | Add new receiving addresses before using them for client payments |

| Cost-basis log template | Date, asset, amount, source wallet, destination wallet, fees, linked receipt record, and resulting cost basis | Each transfer row should link back to an acquisition record |

| Guidance scope | IRS FAQ framing generally applies to digital-asset transactions completed before Jan. 1, 2025 and, unless otherwise noted, to taxpayers holding virtual currency as a capital asset | Revisit the template as guidance evolves |

Capture the receipt record at payment time#

For each USDC client payment, keep one complete receipt bundle: invoice or contract, payer identity, timestamp, receiving address or account, transaction hash or platform reference, and the fiat value recorded at receipt.

That checklist is an operational standard, not an IRS-mandated format in the excerpts provided. The practical point is simple: if virtual currency is treated as property, your value and acquisition record should be defensible later.

Use a simple reconciliation rule: one payment maps to one payer, one destination, one timestamp, and one transfer reference. If that mapping is unclear, fix the record quickly.

Also avoid label-based assumptions. IRS guidance says assets with virtual-currency characteristics are treated as virtual currency regardless of label, so keep the file as a digital-asset receipt record.

Map ownership before self-custody transfers#

Document wallet ownership before you move funds between accounts you control. If you use Coinbase, a Ledger wallet, and a backup wallet such as Trezor, record that ownership continuity in one place.

Keep it to plain fields: account or wallet name, owner, business use, and active receiving addresses. Add new receiving addresses before using them for client payments. If continuity is missing, treat new transfer patterns as higher risk and repair the documentation first.

Build a cost-basis log template now#

Set up the log before your next transaction. A practical template can include: date, asset, amount, source wallet, destination wallet, fees, linked receipt record, and resulting cost basis.

This exact template is not prescribed in the excerpts, but it gives you a durable chain from receipt to later movement and, if needed, disposal. Apply one control: each transfer row should link back to an acquisition record. If it does not, flag it immediately.

Confirm the guidance scope you are using#

If you rely on IRS FAQ framing, verify scope first. The FAQ page says it generally applies to digital-asset transactions completed before Jan. 1, 2025, and, unless otherwise noted, to taxpayers holding virtual currency as a capital asset.

That does not make your evidence pack unusable after that date. It means you should revisit your template as guidance evolves instead of assuming the same setup will stay sufficient indefinitely.

Record receipt as income first and price it once#

For bookkeeping, record each USDC client receipt when you receive it, assign one value once, and keep later wallet activity separate.

Book the receipt at the moment of control#

In this workflow, book the USDC service payment at receipt, then handle later moves, sales, or spending as separate events.

For U.S. tax context, IRS virtual-currency guidance treats virtual currency as property, and those FAQs generally apply to transactions completed before Jan. 1, 2025. Within that scope, the value you record at receipt is your anchor record.

Use one valuation timestamp policy all year and apply it consistently. The IRS materials here do not require one exact timestamp method, so the standard is consistency and defensibility. One payment should have one recorded value, not repeated repricing after market moves.

Flag self-employment review without forcing the conclusion#

If you operate solo, tag the receipt for Schedule SE review when you book it. That tag is a checkpoint, not proof that every USDC receipt is automatically subject to self-employment tax.

IRS describes Schedule SE (Form 1040) as the form used to compute tax due on net self-employment earnings. IRS also notes self-employment tax covers Social Security and Medicare taxes only, and that the page is not all-inclusive.

Keep these guardrails in mind. You usually must pay self-employment tax at $400 or more of net self-employment earnings. The stated rate is 15.3%. Generally 92.35% of net self-employment earnings is subject to that tax.

At filing time, confirm treatment using current Schedule SE instructions. IRS posted a correction to the 2025 Schedule SE instructions on 20-FEB-2026, so do not rely on stale copies.

Keep income records separate from later gain or loss records#

Keep two connected records with different jobs:

- Income ledger: what you earned, when, and from whom

- Asset or wallet ledger: what happened to those units after receipt

This separation helps prevent double counting. A later sale, spend, or transfer should not be booked as a second service receipt.

Reconcile before month-end close#

Before month-end close, verify that your income ledger and wallet ledger match for each receipt on units, timestamp, and payer reference. This is an operational control, not an IRS-prescribed field list.

If a record does not match, fix it before adding later transfer or disposal entries. Early repair helps prevent downstream reporting errors from compounding.

Move to self-custody without losing cost basis continuity#

Treat a self-custody move as a continuity task. IRS guidance treats virtual currency as property, and taxable crypto transactions are generally tied to sale or exchange, while crypto received for services is income-tax relevant. Duplicate entries can create reporting noise.

Mark the move as a wallet transfer, not a new acquisition#

If you move USDC from Coinbase to a Ledger wallet you control, record it as a transfer linked to the existing lot unless the facts indicate a sale, exchange, or payment-for-services event. The provided excerpts do not give a transfer-specific rule for self-custody moves, so do not create a new income entry just because the assets arrived in a different wallet.

Reconcile the source and destination entries to the same lot, with any fee difference clearly separated. Keep the transaction hash, timestamp, source account, destination address, and your ownership map together. If ownership evidence is incomplete, pause and resolve that record first.

Carry forward the original cost basis and acquisition metadata#

Keep the original basis history attached to the lot as it moves. Carry forward the original receipt value, timestamp, payer reference, and lot ID into the transfer entry, rather than assigning a new pricing date on arrival in self-custody.

A common failure mode is an inbound self-custody transfer being auto-labeled as a buy in exports or imports. That can break basis continuity and create errors later when you sell, swap, or spend. If an inbound amount cannot be linked to an existing lot, mark it unresolved instead of guessing.

Track transfer fees in their own field#

Record transfer or network fees separately from the transferred USDC amount. The material here does not support one universal fee treatment, so your immediate goal is complete records and consistent handling at filing time.

Use a dedicated fee field with the fee asset, amount, and transaction hash. That keeps review straightforward later if fee treatment needs to be evaluated against your facts.

Preserve the ownership chain when you rotate devices#

If you later move the same lot from a Ledger wallet to a Trezor, keep the same lot ID and continuity trail in your records. The device changed, but your ownership chain in the books should still be clear.

Fragmented tagging creates avoidable risk. One hop gets marked as transfer, another as buy, and then exchange records, wallet exports, and Form 8949 workpapers diverge. Visible mismatches in reporting can draw scrutiny. Use one operating rule in your records: when ownership appears to stay the same, keep the same history and evidence pack for each hop.

Treat selling swapping and spending as separate taxable decisions#

Treat each later USDC exit as its own disposal decision. Once your receipt and wallet-transfer records are clean, classify every sell, swap, or spend separately before you calculate potential tax results.

Confirm the capital-asset scope first#

The IRS FAQ positions used here apply to taxpayers who hold virtual currency as a capital asset. Confirm that scope before applying capital-gain or loss disposal logic across the board.

Also check guidance timing. The IRS FAQ page says it generally applies to transactions completed before Jan. 1, 2025, and references Notice 2014-21 (2014) for the property-treatment baseline. If your disposals are later, review current guidance before filing.

Classify the disposal type before recording fields#

Do not collapse all outbound USDC into one generic sale file. Record each category on its own terms:

- Sell to fiat

Record disposed units, date and time, fiat proceeds, fees, source wallet, destination account, and transaction hash or exchange confirmation.

- Crypto-to-crypto trade

Treat the USDC leg as disposed property and record the valuation used, received asset, fees, and transaction IDs or records for the trade.

- Spend on goods or services

Because virtual currency is treated as property for U.S. federal tax purposes, track these payments as potential disposal events in your books and keep payee or merchant record, invoice or receipt, valuation used, wallet record, and transaction hash.

| Disposal scenario | Original lot timing field to carry | Federal tax posture to review | Minimum evidence required |

|---|---|---|---|

| Sell USDC for fiat | Original acquisition date and disposal date | Review whether the sale results in a capital gain or loss under your facts and current guidance | Exchange confirmation, proceeds, fees, transaction ID, linked original lot record |

| Swap USDC for another crypto asset | Original acquisition date of the disposed USDC lot and trade timestamp | Review whether the exchange results in a capital gain or loss under your facts and current guidance | Trade record for both sides, valuation used, fees, transaction IDs, linked lot history |

| Spend USDC on goods or services | Original acquisition date and payment timestamp | Review whether disposal treatment applies under your facts and current guidance | Merchant receipt or invoice, valuation used, wallet record, transaction hash, linked lot record |

Compute from the original lot trail#

For U.S. federal framing, sale or exchange transactions generally result in capital gain or loss. For each disposal, use the original lot record carried forward from the income record and compare it to the value realized at disposal.

Your reconciliation check should tie the original service-payment record, transfer history, and final disposal record together. If that chain does not reconcile, fix the records before filing summaries.

Reconstruct conservatively if lot tracing is weak#

If you cannot trace lots confidently, do a conservative reconstruction and document assumptions before filing. Use available wallet exports, exchange confirmations, transaction hashes, and original payment records. Clearly label what is confirmed versus inferred.

Do not let software-created replacement acquisitions become your default basis without review. If that happened, correct lot history first, then rerun disposal classification and calculations. Also remember federal framing is not the full picture. Some states may tax cryptocurrency transactions too.

Add cross-border reporting guardrails before filing season#

For globally mobile freelancers, cross-border reporting starts with your tax residency facts. Those facts can determine whether you need to evaluate Form 8938, FinCEN Form 114 (FBAR), or both.

Confirm whether U.S. filing status is in play#

Start with residency, not the token. Form 8938 applies to specified individuals, which includes a U.S. citizen and a resident alien of the United States for any part of the tax year. If you moved mid-year or split time across countries, keep your crypto records aligned with your residency file.

Use one consistency check before anything else: your day-count log, move or immigration timeline, and tax return position should tell the same U.S.-status story. If they do not, resolve that first.

Test Form 8938 and FBAR separately#

If U.S. filing may apply, run two separate checks instead of one blended crypto review.

Form 8938: used to report specified foreign financial assets when total value exceeds the applicable threshold. A baseline$50,000threshold is cited for certain U.S. taxpayers, and higher thresholds can apply for some filers, including some joint filers and taxpayers residing abroad.FBAR (FinCEN Form 114): remains a separate requirement when it applies. Filing Form 8938 does not replace it.

Keep one more guardrail in mind: do not assume a Ledger device, a self-custody address, or USDC holdings are automatically reportable on Form 8938 or FBAR.

Keep one evidence folder for residency, ownership, and values#

Build one tax-year folder that combines residency-day logs, account ownership records, and crypto records. At minimum, keep:

- a dated residency timeline

- foreign institution or platform account records

- proof of account ownership

- account value records needed to support maximum-value reporting fields when required

If no U.S. income tax return is required for the year, Form 8938 is not required even if foreign assets exceed thresholds. If a U.S. return is required, keep your residency and crypto files synchronized so your reporting position stays consistent.

If your filing footprint spans more than one country, use the Tax Residency Tracker to keep day counts and supporting records organized before filing.

Escalate early when facts move beyond straightforward filing#

If your residency facts changed, your basis trail is incomplete, or your draft return conflicts with your records, escalate before filing.

Decide whether your facts are still DIY#

Changed tax residency is a clear trigger. In California, residency is a facts-and-circumstances determination, and part-year treatment can change what is taxed: worldwide income while resident, and California-source income during nonresident periods. If you physically performed services in California while nonresident, check whether Form 540NR is required.

For federal income tax, virtual currency is treated as property. So if your cost basis records are incomplete across exchanges or wallets, treat that as a filing risk and get help before finalizing income, gain, or loss figures.

Check for contradictions before you file#

Run one consistency pass: your residency timeline, workday log, wallet records, and draft return should align. If they do not, escalate instead of forcing a clean narrative.

Also check scope. The IRS virtual-currency FAQ states it generally applies to digital-asset transactions completed before Jan. 1, 2025 and, unless noted otherwise, to taxpayers holding virtual currency as a capital asset. If your position falls outside that frame, treat it as a professional-review trigger.

| Trigger | Risk if ignored | Documents to bring | Likely specialist type |

|---|---|---|---|

| Changed residency or part-year California facts | Wrong sourcing, missed California filing, weak residency position | Day-count log, move timeline, travel or lease records, workday calendar, draft return | State residency CPA or EA |

| Multiple exchanges or wallets with incomplete basis records | Potentially misstated income, gain, or loss | Exchange exports, wallet ownership map, transaction history, fee records, basis log | Crypto-focused tax preparer |

| Draft return conflicts with platform records | Filing inconsistencies that are hard to defend later | Draft return, annual statements or forms received, reconciliation notes | CPA or EA who can reconcile return support |

| Position depends on post-Jan. 1, 2025 activity or non-capital-asset treatment | Overreliance on FAQ guidance outside its stated scope | Transaction summary, treatment assumptions, supporting notes | Tax professional with digital-asset technical depth |

Bring the evidence pack, not just questions#

Bring a reconciled file, not a verbal summary. At minimum: draft return, basis log, wallet ownership records, residency-day records, and any California workday calculation if California is relevant. This lets an adviser quickly isolate whether your issue is documentation, sourcing, or tax treatment.

For a step-by-step walkthrough, see A guide to the 'exit tax' when leaving Canada as a self-employed professional.

Fix the mistakes that cause most USDC filing stress#

Filing stress usually comes from mixed or unsupported records, not from one missing formula. Clean the record trail first, separate event types clearly, and escalate material uncertainty before you file.

-

When you treat every movement as the same kind of event: Separate likely wallet transfer lines from receipt and disposal records in your ledger. Keep prior lot and cost basis notes attached for review instead of rebuilding them from scratch.

-

When you combine receipt and disposal into one entry: Split the timeline into distinct events: initial receipt records first, then later disposal records. Keep each entry tied to its own transaction evidence so a reviewer can follow the sequence without guesswork.

-

When ownership continuity is weak across platforms: Rebuild an ownership file for Coinbase and your Ledger hardware wallet with available account exports and transaction-level records so control history is clear.

-

When you file with unresolved gaps and unsupported authority: If basis links, ownership continuity, or timestamps are still uncertain, document assumptions and get professional review before filing when the uncertainty is material. Do not rely on bulletin synopses or proposal-stage items as final authority. The July 29, 2024 IRB synopsis says synopses are not authoritative, and the cited IRB excerpt is about W-2 and W-3 printing, not crypto treatment.

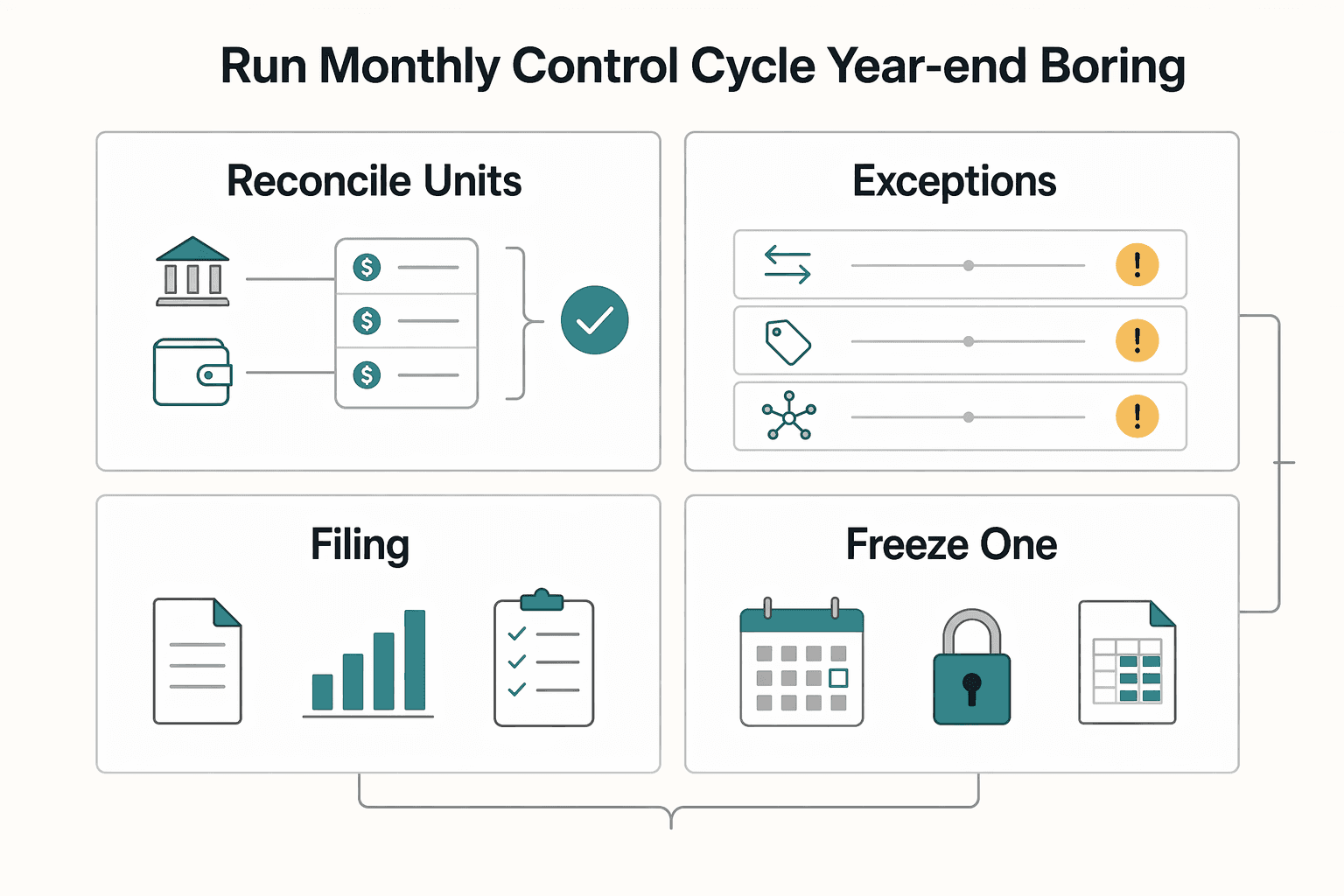

Run a monthly control cycle so year-end is boring#

A monthly control cycle is a practical way to keep your records filing-ready instead of rebuilding everything at year-end. Use one repeatable process that reconciles balances, logs exceptions, and flags records that may matter for U.S. filing review.

| Step | Action | Article note |

|---|---|---|

| Reconcile units first, then tie them to books | Total USDC across exchange accounts and self-custody wallets, match that total to your bookkeeping balance, and clear in-transit transfers and booked fees before you add tax labels | Clear breaks before you add tax labels |

| Keep a one-page exception log and clear it monthly | Track missing transaction records, missing valuation support, missing ownership evidence, and any account closure to review | Keeps the year-end balance from looking clean while the underlying support is incomplete; account closures may matter for Form 8938 |

| Pre-tag records that may affect filing forms | Mark foreign account or custodial records for Form 8938 or FBAR review during the year | Form 8938 is attached to the annual return, and filing Form 8938 does not replace a separate FBAR filing when FBAR is otherwise required |

| Freeze one monthly export bundle | Keep a read-only package with exchange exports, wallet history, valuation support, your ownership map, and the exception log, plus month-end value snapshots where foreign-asset reporting could become relevant | Form 8938 is tax-year specific and captures maximum account values |

Step 1. Reconcile units first, then tie them to books. At month-end, total your USDC across exchange accounts and self-custody wallets, then match that total to your bookkeeping balance. Clear breaks, including in-transit transfers and booked fees, before you add tax labels.

Step 2. Keep a one-page exception log and clear it monthly. Track only issues that create filing friction later: missing transaction records, missing valuation support, missing ownership evidence, and any account closure to review.

This keeps your year-end balance from looking clean when the underlying support is still incomplete. If foreign deposit or custodial accounts are in scope, this matters because Form 8938 asks whether any such accounts were closed during the tax year.

Step 3. Pre-tag records that may affect filing forms. Tag records during the year, not during return week. Mark foreign account or custodial records for Form 8938 or FBAR review.

Form 8938 is attached to your annual return and due with that return, including extensions. Filing Form 8938 does not replace a separate FBAR filing when FBAR is otherwise required. Also remember thresholds are not one-size-fits-all, and some joint filers and taxpayers living abroad have higher thresholds.

Step 4. Freeze one monthly export bundle. Keep one read-only package per month with exchange exports, wallet history, valuation support, your ownership map, and the exception log. Preserve month-end value snapshots where foreign-asset reporting could become relevant, since Form 8938 is tax-year specific and captures maximum account values. This bundle is an internal control, not a standalone government form requirement, but it makes preparer handoff and review much faster.

Use this copy-paste checklist before you file#

Run this checklist as your final pre-filing control. Avoidable errors here often involve misclassification, broken basis continuity, and skipped U.S.-linked reporting review.

Classify each line item as income, wallet transfer, or disposal event.

Label transactions by what happened, not by platform. Keep client payment receipt, own-wallet movement, and any later sale, swap, or spend as separate entries when they occur in sequence. If you cannot explain an outflow in one sentence, treat it as unresolved before filing.

Confirm cost basis continuity from receipt through self-custody and any later sale/swap/spend.

Carry the same lot history forward when funds move to self-custody. A wallet move may not be a new acquisition by itself, so confirm treatment for your facts before filing. Keep one continuous record trail from receipt to final use so later gain or loss treatment is traceable instead of reconstructed.

Reconcile exchange and wallet records, then tie totals to your tax return workpapers.

Match records across systems, then confirm your filing workpapers agree with those reconciled totals. Your records should tell one consistent story for holdings, income entries, and disposal entries without double counting.

Review residency-linked obligations (United States, FBAR/FinCEN, FATCA/Form 8938) where applicable.

If you may have a U.S. filing footprint, run this review separately from income or disposal classification. Form 8938 is used by specified persons (specified individuals or specified domestic entities) to report specified foreign financial assets, including financial accounts maintained by a foreign financial institution, when total value is above the applicable threshold. Attach Form 8938 to your annual return and file by that return's due date, including extensions. Thresholds vary by filer profile, with higher thresholds for some groups, including joint filers and taxpayers residing abroad, and one published context starts at an aggregate value exceeding $50,000. Form 8938 also asks whether foreign assets were acquired or sold during the tax year. Filing Form 8938 does not remove a separate FBAR (FinCEN Form 114) duty when FBAR is otherwise required, and if you are not required to file an income tax return for the year, Form 8938 is not required.

Escalate unresolved basis, residency, or reporting conflicts to a qualified tax professional before filing.

Escalate before you file if basis continuity breaks, residency facts are unclear, or you cannot determine whether Form 8938 or FBAR analysis applies. Bring a clean evidence pack so a reviewer can verify your position without rebuilding your full transaction history.

Related reading: How to Handle the 'Kiddie Tax' for Your Child's Investment Income.

Before you submit, run a final threshold check with the FBAR Calculator so you can confirm whether a deeper review is needed.

Frequently Asked Questions

Is sending USDC from Coinbase to a Ledger wallet taxable?

Usually not, if it is only a transfer between wallets you own. In the framing used here, own-wallet stablecoin transfers are generally treated as non-taxable events. Keep records that connect the outgoing transfer and the receiving wallet so the movement is clearly traceable.

If a client pays me in USDC, is that income?

In many cases, yes. Payment in stablecoins for goods or services is generally treated as ordinary income, using fair market value in U.S. dollars to determine tax impact. Save your invoice or contract, receipt details, and USD value at receipt in one record set.

Do I pay tax again when I sell USDC later?

Potentially. A later disposal is analyzed separately from the original income event and can trigger capital gains tax analysis. The key is to keep the income entry and later disposal entry distinct in your records to reduce reporting errors.

Is spending USDC taxable?

It can be. Using stablecoins to make a purchase can be a disposal event subject to capital gains tax analysis. So spending USDC is different from a pure transfer between your own wallets.

Do I have to report wallet transfers on my tax return?

Pure own-wallet transfers are often tracked as records rather than treated as taxable disposals. You should still log them clearly, because incomplete transfer records can make later reporting harder.

What proves cost basis after moving to cold storage?

Use a continuous record chain from receipt to later disposal. Keep receipt records, USD value at receipt, transfer metadata, and later disposal records linked together. In this framing, moving USDC to self-custody is generally treated as a transfer between your own wallets, not a separate disposal.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- federalregister.gov/documents/2026/03/02/2026-04089/implementing...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- ftb.ca.gov/file/personal/residency-status/part-year-and...trusted

- ftb.ca.gov/forms/2023/2023-1031-publication.pdftrusted

- irs.gov/individuals/international-taxpayers/frequent...trusted

- irs.gov/filing/digital-assetstrusted

- occ.gov/news-issuances/news-releases/2026/nr-occ-202...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC10648726trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Using a Data Processing Agreement with Subcontractors

Put your data processing agreement in place before a processor or sub-processor gets access to personal data. If you use a processor, UK GDPR guidance requires a [written contract or other legal act](https://ico.org.uk/for-organisations/uk-gdpr-guidance-and-resources/accountability-and-governance/contracts-and-liabilities-between-controllers-and-processors-multi/when-is-a-contract-needed-and-why-is-it-important). Set that contract boundary before support logins, shared folders, or troubleshooting access turn into live processing.

Vancouver Digital Nomad Guide 2026 for Long-Stay Remote Work

If you are planning a longer stay in Vancouver, make the go or no-go call before you commit to non-refundable flights, deposits, or a long lease. This guide is about remote work planning in Canada, not short-trip sightseeing. The goal is to help you validate route, documents, and budget in the right order so one weak assumption does not force a rushed decision later.

How to Get Paid in Crypto as a Freelancer (and Manage the Risks)

Freelancers use crypto payments for a practical reason: slow payouts and high transfer costs can squeeze monthly cash flow. Traditional rails are still slow in many cases, and [crypto-freelance payment guides](https://www.request.finance/crypto-freelance/how-to-get-paid-in-crypto-a-freelancers-guide-2024) report regional fee pressure that can land around 5% to 10%. When a client wants to pay this way, the goal is not novelty. It is predictable settlement, clean records, and fewer avoidable disputes.