Quick Answer

Treat s-corp shareholder distributions as separate owner payouts only after payroll is completed and posted. Classify each transfer clearly, update stock basis before calling any non-dividend amount tax-free, and keep approval, bank proof, and ledger coding together. Schedule K-1 reports distribution amounts, but taxable treatment depends on your basis records.

Step 1: Set a Defensible Salary - Your Compliance Foundation#

Start with one rule: classify each owner transfer clearly, then keep enough records to test distribution taxability against stock basis later. In an S corporation, income, loss, deductions, and credits flow through to shareholders and are taxed on shareholders' personal returns. Whether a non-dividend distribution is taxable depends on stock basis, not debt basis. Schedule K-1 reports the non-dividend distribution amount, but it does not tell you the taxable amount.

Apply three checks before you lock the pay decision#

What you do need is a documented method you can explain and records that hold up under review.

- Classification check

Pass: owner transfers are consistently labeled in your books, with matching support. Fail: transfers are mixed in one catch-all owner account.

- Basis-visibility check

Pass: you can show current stock-basis tracking and distribution totals, and you track debt basis separately. Fail: you cannot show how distributions map to stock basis, or you rely on debt basis for distribution taxability.

- Year-end reporting check

Pass: your records tie to Schedule K-1 inputs, and loss items are reviewed with the four ordered limitation checks before claiming. Fail: you assume a K-1 loss is automatically claimable or cannot reconcile distribution totals cleanly.

| Check area | Strong evidence | Weak evidence | What to retain | Cleanup risk if missing |

|---|---|---|---|---|

| Classification | Consistent labels per transfer and matching support | Mixed transfer types in one owner bucket | Ledger detail plus transfer support | Reclassification work at year end |

| Basis visibility | Stock-basis tracking tied to distributions, with debt basis tracked separately | No basis tie-out or debt basis used for distribution taxability | Basis workpapers and period tie-outs | Taxability analysis can fail late |

| K-1 readiness | Records tie to K-1 inputs and loss limits are reviewed in order | Reliance on K-1 alone for taxability or loss claims | Reconciliation notes and limitation review file | Filing delays or correction cycles |

Build the file in sequence#

Keep the setup simple and deliberate. Start with a short memo that explains your compensation rationale and classification policy. Then add a dated internal decision record so the amount, timing, and classification approach are explicit. Next, align your accounting setup to that decision and verify the first period posts correctly. If anything is still unresolved, mark it as pending verification instead of guessing.

It also helps to keep support in chronological order. That makes later review faster because you can see whether the books actually followed the documented approach.

Clear the gate before Step 2#

Move to Step 2 only when all of these are true. If classification is mixed, basis support is incomplete, or K-1 readiness depends on guesswork, stop and fix Step 1 first.

- compensation rationale and transfer classification are documented

- owner transfers are separated cleanly in the books

- stock-basis tracking is current enough to evaluate distribution taxability

- K-1 preparation inputs are traceable from your records

- unresolved items are flagged, not assumed

Related: How to Structure an S-Corp for a Husband and Wife Partnership.

Step 2: Master the Pay-Then-Distribute Sequence - Your Operational Cadence#

Once pay and classification are set, the next job is consistency. Use one conservative operating rule each cycle for s-corp shareholder distributions: check cash, complete and post payroll, then authorize and record any distribution as a separate event. Treat this as an internal control habit, not as a verified IRS-mandated payment order for every fact pattern.

Run the same sequence every period#

- Cash is available

Use cleared business cash, not projected receipts. Before any owner transfer decision, review open bills, the next payroll cycle, payroll tax pulls, and other near-term debits.

- Payroll is complete

For this cadence, treat payroll as complete when the run is processed, payroll-liability entries are posted, and the payroll register aligns with provider confirmation or bank movement.

- Distribution is a separate event

Record the distribution with its own authorization note, its own bank transfer, and its own ledger line to a dedicated distribution or equity account.

If you follow that order every month or every quarter, your records are usually easier to review. If you skip the order, that exception can create cleanup work later because the owner transfer purpose may be less clear.

| Sequence behavior | What happens in practice | Reconciliation impact | Documentation risk |

|---|---|---|---|

| Cash in -> payroll complete -> separate distribution | Payroll records, bank movement, and distribution ledger entry align | Typically cleaner period close and fewer year-end cleanup passes | Stronger support trail |

| Owner transfer before payroll is fully complete | Cash moves to owner while payroll is still unresolved | Harder to show what cash was available after wage obligations | More reclassification questions |

| One mixed transfer labeled later | One payment is treated as multiple purposes after the fact | Manual cleanup and weaker traceability | Weakest support trail |

Pre-distribution control gate#

Before you release a distribution, confirm all five items:

| Control | What to confirm |

|---|---|

| Payroll reconciliation | Register, provider or bank confirmation, and ledger postings agree |

| Near-term obligations | Open bills, next payroll, payroll tax pulls, and scheduled drafts are covered |

| Retained buffer | Cash remains for routine operations and known obligations |

| Ledger coding | Distribution or equity account is ready, not payroll or miscellaneous expense |

| Basis note | Verify basis treatment before release is present where relevant |

If one item fails, do not force the payout through and promise yourself you will fix the records later. Pause the transfer, note what is missing, and clear that item first. A short delay is usually easier to manage than a later reclass with incomplete support.

Keep special mechanics separate#

Default to plain cash distributions. If you are considering a DRIP or another reinvestment-style approach, treat it as a separate governance event with heavier documentation. Do not treat it as a simple reroute of a normal payout.

A DRIP can function as internal equity financing and, in closely held settings, can credit distributions against new equity subscriptions under a board-approved plan. If you use that structure, include a formal dividend declaration, an automatic reinvestment election, and explicit plan terms, including pricing and eligibility. A DRIP is generally a poorer fit where many shareholders need current cash income. Assess minority-holder dilution or illiquidity risk before proceeding.

If you want a deeper dive, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

Step 3: Build an Audit-Proof Record - Your Risk Mitigation Layer#

If Step 2 gives you a clean cadence, Step 3 is what makes it hold up later. At this point, the main risk is record quality: can you show who approved each payout, what it was, and how the cash and books match?

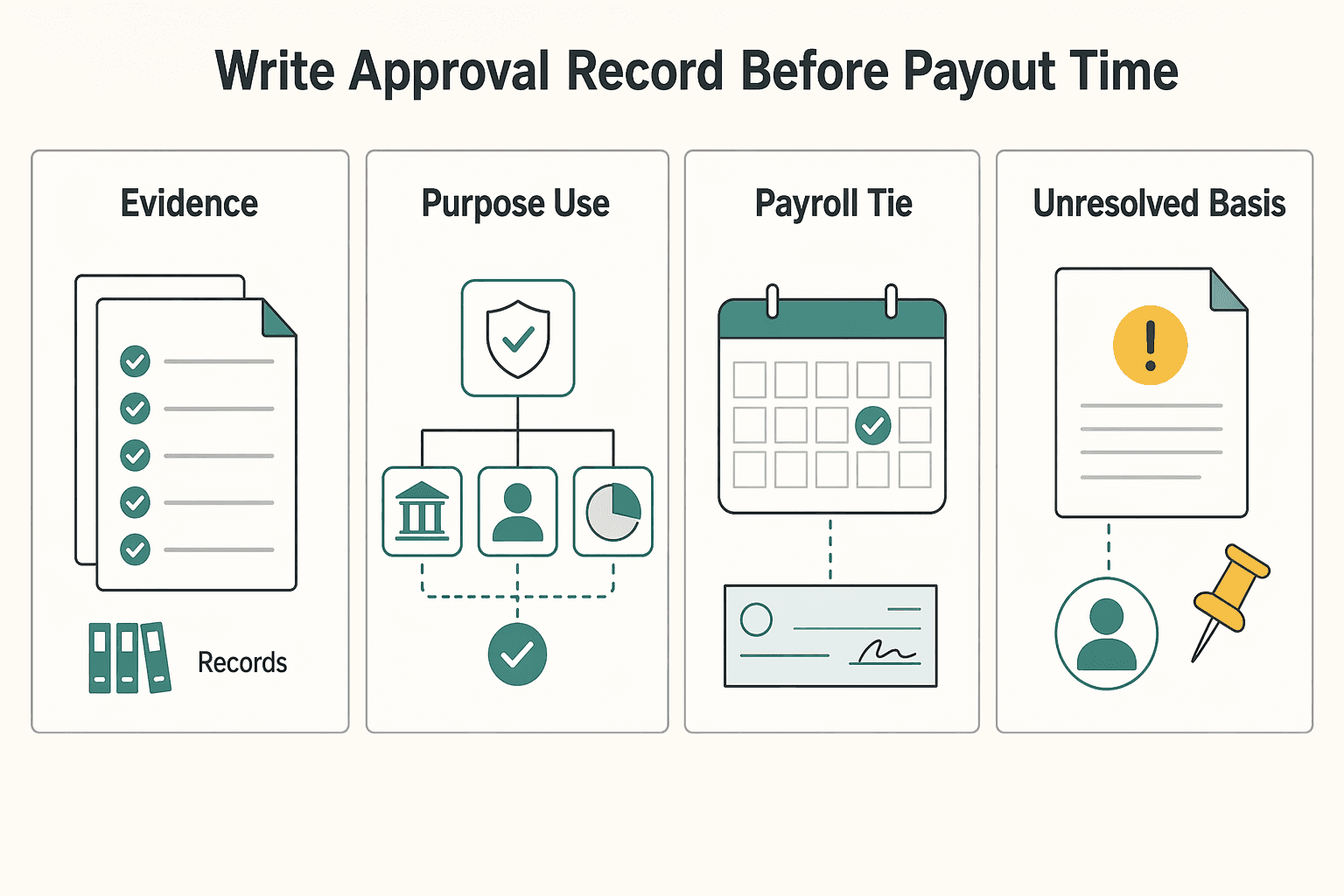

3.1 Write the approval record before or at payout time#

Use primary authority, not summary text, when you set your standards. The IRS says IRB synopses are reader aids and "may not be relied upon as authoritative interpretations," and non-binding operational guidance can also change without notice.

| Approval item | What to record |

|---|---|

| Date | Record the date for each payout |

| Amount | Record the payout amount |

| Recipient | Record the recipient |

| Purpose | Use a plain-language purpose |

| Approver | Record the approver |

| Payroll tie | If it is tied to a completed payroll cycle, say so |

| Unresolved basis item | Mark the item as pending advisor review instead of guessing |

Treat the approval record as an internal control record, and have your advisor confirm legal form under your governing documents. For each payout, record at least the date, amount, recipient, plain-language purpose, and approver. If it is tied to a completed payroll cycle, say so. If a basis item is unresolved, mark it as pending advisor review instead of guessing.

If you use a short dated memo for a one-owner S-corp, treat it as an internal control record and confirm acceptability with your advisor. The control goal is contemporaneous evidence, not ceremony. The key is that someone reviewing the file later can tell what you intended at the time of payment without having to infer it from a bank statement alone.

3.2 Keep ledger coding and cash evidence aligned#

Good documentation breaks down fast when the ledger and the bank trail do not match. Use a consistent, clearly named ledger account and memo convention for payouts, and keep transfer proof with the same record. If an entry lands in the wrong account, correct it in period while the activity is still easy to trace.

| Record element | Clean approach | Risky approach |

|---|---|---|

| Ledger label | Consistent, clearly named ledger account with a clear memo | Expense, wages, loan, or uncategorized label with no review |

| Transfer path | Single clearly traceable business-to-owner transfer path when practical | Multiple mixed transfers bundled after the fact |

| Approval proof | Dated minutes, written consent, or signed memo saved with payout file | Approval recreated later or missing |

| Source-document linkage | Bank confirmation or check image linked to the ledger entry | Ledger line with no transfer evidence |

Where rules require a method, they usually say so directly. For example, 26 CFR 1.482-9 explicitly requires using one listed method for arm's-length pricing in controlled services transactions. You do not have that same explicit method list here for distribution approval fields, so keep your internal record standard clear and defensible.

3.3 Prefer one payout path when practical#

This habit helps prevent cleanup work later: keep each payout traceable through one identifiable business-to-owner transfer when practical. Keep personal and business spending separate, and avoid patterns that force reconstruction after the fact.

If classification is unclear, fix it immediately with a same-period correction, reclass, or reversal and note why. Keep one evidence pack per payout: approval record, transfer proof, ledger entry, and a short tie-out note for anything unusual, including unresolved basis items or other open questions. If you split the money flow across several transfers, make sure the file explains the sequence clearly enough that another person could trace it without asking you what happened.

3.4 Hand off a year-end package your accountant can use fast#

By year end, your accountant should not need oral history to understand what happened. Send a reconciled package, not just a total, so each payout can be traced from approval to transfer to ledger. Include the following:

- full-year distribution ledger export with clear labels and miscoding corrected

- transfer support for each payout, or a reconciled statement map to ledger lines

- any internal allocation support used during multi-owner periods

- notes for unusual items: reversals, reclasses, returned transfers, and unresolved basis items pending review

A short cover note that ties the annual distribution total in the ledger to the support you are sending can save a round of questions. The goal is a handoff that lets return prep start from organized records instead of reconstruction.

You might also find this useful: How to Revoke an S-Corp Election. If you want your payout workflow to mirror this same audit-ready discipline, review how Gruv Payouts handles policy gates, status tracking, and traceable records where supported.

Conclusion: You Are Now the CFO of Your Business-of-One#

Keep the core rule simple: keep your distribution records clean, track stock basis consistently, and do not treat a non-dividend distribution as tax-free until your basis records support that conclusion.

Schedule K-1 shows the amount of non-dividend distribution you receive, but it does not state the taxable amount. Shareholder distribution (non-dividend) is tax-free only up to stock basis. Stock basis is your shareholder-level running amount that changes with S-corp activity and is used to determine distribution taxability.

Run this every-cycle close checklist#

Use this checklist at each close:

| Step | Checklist |

|---|---|

| 1. Confirm period records are complete | Go if owner transfers and related entries for the period are processed and supported in your records. Stop if cash moved without support or period records are incomplete. |

| 2. Reconcile and classify the period | Go if bank movement and equity postings tie to the same period. Stop if owner transfers are miscoded or unsupported. |

| 3. Update basis before calling any payout tax-free | Go if stock basis tracking is current. Remember that Schedule K-1 shows the non-dividend distribution amount, not the taxable amount, and debt basis is not used to determine whether a distribution is taxable. Stop if basis is unresolved and mark the treatment as pending review instead of estimating. |

| 4. Release distribution and save the payout file | Keep approval, transfer proof, and the equity entry together so year-end treatment is traceable, including cases where one distribution creates multiple tax consequences. |

| Area | Doing it right now | Cleanup later |

|---|---|---|

| Compliance risk | Clear basis tracking and distribution classification | Higher chance of incorrect distribution tax treatment |

| Bookkeeping effort | One clean close cycle | Backtracking through mixed entries |

| Tax filing friction | K-1 and return prep starts from organized records | Harder to determine distribution taxability |

If your facts cross entities or jurisdictions, add one control point before changes: confirm the rule that applies to your exact case. If you need the mechanics, start with How to Run Payroll for an S-Corp with a Single Employee (Yourself).

For a step-by-step walkthrough, see The Best Way to Manage Shared Finances in a Business Partnership. If your owner-pay process is cross-border or spans multiple entities, use Contact to confirm market coverage and compliance gating before you change operations.

Frequently Asked Questions

How do you set a reasonable salary?

Set pay based on the services you actually perform, not a fixed split. If you are a corporate officer, perform more than minor services, and receive or are entitled to compensation, those payments are treated as wages for federal employment tax purposes. Document how you chose the number and why it fits your role. Choosing a low wage first and defending it later is a known risk. In a 2012 dispute, $24,000 annual wages alongside large distributions did not make intent to keep wages low a controlling factor.

What order should you pay yourself?

The key point is classification, not a fixed sequence. If a payment is remuneration for your services, treat it as wages through payroll. Keep separate owner profit transfers distinct from wage compensation.

What is the difference between salary, a distribution, and a dividend?

Use wages for pay tied to services. Use distribution or dividend labels only for amounts that are not remuneration for services, because labels alone do not control tax treatment. | Payment type | When to use | How to record | Key risk if miscoded | | --- | --- | --- | --- | | Wages | You perform more than minor services and are paid or entitled to compensation | Treat as wage compensation through payroll | Employment tax exposure if labeled as something else | | Shareholder distribution | The payment is not remuneration for services | Keep separate from wage compensation | Recharacterization as wages if it is actually pay for services | | Dividend | The payment is labeled as a dividend, not service pay | Keep separate from wage compensation | Label alone does not prevent wage recharacterization |

How should you document a distribution?

Document each payment so it is clear whether it was compensation for services or a non-wage owner payment. Keep wage and non-wage classifications separate in your books. If something is miscoded, correct it promptly so the record stays clear.

What if there are multiple owners?

Apply the same test owner by owner: what services were performed, and was the payment remuneration for those services? Being both an officer and a shareholder does not remove wage-treatment requirements. Keep each owner’s payments clearly classified and review edge cases with your tax adviser.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.