Quick Answer

Act now: identify the notice type (such as CP3219N or CP3219A), record the date on the letter, and calendar the petition deadline from that date, not the day you opened it. Build a narrow packet with the notice, filed return, and documents tied to each disputed item. If you agree, check whether Form 5564 is included and appropriate. If FEIE day counts, tax home, or income classification are disputed, move quickly to a CPA, Enrolled Agent, or tax attorney.

Stage 1: Triage & Containment - Your First 72-Hour Action Plan#

Contain first, solve second. Your immediate job is to lock the deadline, identify the exact issue, and assemble a clean packet.

Quick triage checklist from page one of the notice:

- Record when you received it.

- Record the response or petition deadline shown on the notice.

- Confirm the tax year or years listed.

- Isolate the stated adjustment reason in plain English.

- Note the notice number (CP or LTR) in the top right corner.

This is a statutory notice of deficiency, meaning a legal notice proposing a tax change. It is not a final bill or a completed audit result. It also starts the Tax Court petition window, so date control comes first.

Step 1: Confirm notice type and response path#

Start with the notice number, because that tells you which instructions apply. Not all deficiency notices follow the same workflow. A CP3219N is a Notice of Deficiency, and CP3219A is another deficiency workflow you may see. If Form 5564 is enclosed, it is the waiver form used when you agree with the proposed changes.

Verification check: you should be able to state, without rereading, the year, the proposed change, the deadline, and the notice number.

Step 2: Lock deadline risk before doing deeper analysis#

Treat the printed date and deadline on the notice as controlling until verified otherwise. For many notices, the petition window is 90 days from the date shown on the notice, or 150 days for persons outside the country. It is not measured from when you opened the envelope. If a petition is late, Tax Court cannot consider it.

Keep one rule in mind during triage: sending additional information does not extend the Tax Court petition deadline.

Step 3: Build a first-pass document packet#

Keep this first packet narrow. You need enough to evaluate the issue quickly, not your full tax archive.

Collect:

- The full notice package, all pages

- The filed return for the listed tax year or years

- The exact documents tied to the IRS adjustment, such as cited income forms or deduction support

- Envelope or certified mail details, if available

Hold off on unrelated receipts, long narrative emails, and every supporting file you have ever saved. Create one folder named with the tax year plus notice number, then subfolders: Notice, Filed Return, IRS-listed Documents, Draft Response. If you dispute later, prepare to send a signed statement with photocopies, not originals.

| Do now | Do after initial review | Do not do yet |

|---|---|---|

| Calendar the deadline shown on the notice | Draft a short issue summary for your preparer or attorney | Send original documents |

| Compare IRS proposed changes to your filed return | Decide whether you agree, partially agree, or dispute | Assume extra submissions extend the petition deadline |

| Save notice pages, return, and cited support in one folder | If you agree, review whether Form 5564 is included and appropriate | Sign a waiver before confirming the adjustment |

Step 4: Verify address and cross-border timing#

If you are abroad, verify the mailing address on the notice against the IRS address on file. Statutory notices are sent to the last known address by certified or registered mail, and Form 8822 is used for IRS address changes.

Use the 150-day outside-the-country rule as a verification step, not an assumption. Confirm your facts and the notice instructions before you rely on the longer window.

By the end of Stage 1, you should have a hard deadline on your calendar, a clean packet, and a one-sentence description of the dispute.

You might also find this useful: How to Handle an IRS CP2000 Notice (Underreported Income).

Stage 2: Root Cause Analysis - From Triage to Strategy#

Once the deadline is under control, move to diagnosis. Your strategy is only as good as the mismatch you are actually dealing with: reporting mismatch, eligibility test failure, or income-classification mismatch.

A deficiency notice becomes manageable when you can trace one clean chain: what the notice claims, where that item sits on your return, what third-party record relates to it, and what your records support.

Step 1: Build a four-part issue chain#

For each disputed item, map these four points:

| Issue-chain part | What it covers |

|---|---|

| Notice claim | The exact income item or exclusion the IRS says is wrong |

| Return entry | Where you reported it on the filed return, or where it was omitted |

| Third-party record | The related payor, platform, payroll, or payment record tied to that item |

| Your records | The documents that explain what actually happened, such as invoices, contracts, travel logs, account records, or receipts |

If you cannot point to one return entry and one supporting record for the item, keep investigating.

Step 2: Run the three most common diagnostics#

| Diagnostic | Key checks | What it usually means |

|---|---|---|

| Income reporting mismatch | Match disputed amounts to the year the work was earned; confirm income was still reported on your U.S. return when FEIE was claimed; reconcile invoices, payment dates, and account receipts for year-end work | If the numbers reconcile after timing corrections, it is likely a reporting or timing issue, not a qualification issue |

| Eligibility-test failure (FEIE) | Confirm foreign-earned compensation for personal services; confirm your tax home was in a foreign country; rebuild travel days from primary records and count only full 24-hour days; do not assume other factors override a missed minimum-day requirement; use the IRS Interactive Tax Assistant as a cross-check | Verify eligibility inputs before debating totals; verify the current FEIE amount limit rather than relying on memory |

| Income-classification mismatch | Confirm each disputed amount is compensation for personal services; separate employer-provided meals and lodging; check how each disputed item was classified on the return before recomputing amounts | If classification corrections resolve the mismatch, fix classification first, then recalculate |

Income reporting mismatch

Start here if the adjustment looks like underreported income or a number mismatch.

Check these points:

- Match disputed amounts to the year the work was earned, not only when paid.

- Confirm income was still reported on your U.S. return when FEIE was claimed.

- Reconcile invoices, payment dates, and account receipts for year-end work.

If the numbers reconcile after timing corrections, you likely have a reporting or timing issue, not a qualification issue.

Eligibility-test failure (FEIE)

If FEIE is at issue, verify eligibility inputs before debating totals.

Check these points:

- Confirm the income is foreign-earned compensation for personal services.

- Confirm your tax home was in a foreign country.

- Rebuild travel days from primary records and count only full days, meaning 24-hour periods from midnight to midnight, when using the physical presence test.

- Do not assume residence type, intent, illness, family issues, vacation, or employer instructions override a missed minimum-day requirement.

- If relevant, confirm days counted were not in a foreign country in violation of U.S. law.

- Use the IRS Interactive Tax Assistant as a cross-check.

For FEIE amount limits, verify the current limit rather than relying on memory.

Income-classification mismatch

If the dispute turns on income type, validate classification before changing totals.

Check these points:

- Confirm each disputed amount is compensation for personal services.

- Separate employer-provided meals and lodging, which may be handled under other rules and are not foreign earned income.

- Check how each disputed item was classified on the return before recomputing amounts.

If classification corrections resolve the mismatch, fix classification first, then recalculate.

Step 3: Choose DIY vs delegate without overconfidence#

Use the issue type, not your stress level, to decide whether to handle it yourself or hand it off.

| Situation | Decision signals | Risk if wrong | Best next action |

|---|---|---|---|

| Clear reporting or timing error | Numbers reconcile and you agree after document review | You concede before fully checking earned-year treatment | Prepare a concise correction summary based on reconciled records |

| FEIE eligibility dispute | Tax home, day counting, or income classification is contested | A small eligibility error can change the outcome | Pause DIY, organize travel and income proof, and get issue-specific review |

| Income-classification mismatch | Payment type is disputed | You treat non-qualifying amounts as foreign earned income or miss a valid correction | Split items by type, correct classification, and get review where classification is unclear |

Step 4: Screen an advisor with a short rubric#

If you delegate, screen for fit with four questions:

- Have you handled deficiency matters with this exact issue type, especially FEIE day-count or tax-home disputes?

- How do you validate physical-presence counts (330 full days in a 12-month period) from primary records?

- How do you test earned-year timing when work year and payment year differ?

- How do you classify disputed amounts, including compensation for personal services versus amounts that are not foreign earned income?

Step 5: Produce the Stage 2 handoff#

Before you respond or escalate, package the file so someone else can understand it without reconstructing the whole case.

By the end of this stage, your packet should include:

- A one-sentence issue statement

- An evidence packet organized by disputed item

- Your selected path: agree, partially agree, or dispute

- Open questions for advisor review, especially FEIE day count, income timing, and income classification

Related: The Best Digital Nomad Cities for Entrepreneurs and Startups.

Stage 3: The 'Never Again' System - Building a Resilient Operation#

Keep the prevention side simple. After a Notice of Deficiency, the goal is one source of truth, one pre-filing reconciliation, and clear escalation rules when something does not tie out.

Step 1: Build one source of truth for income, expenses, and documents#

Your setup can be lightweight, but it has to reflect gross income and expenses clearly. Use one bookkeeping ledger, one document folder structure, and one recurring capture session. The IRS says daily recording is best practice. A weekly session is a practical operating habit, not a legal rule.

Track at least these fields for each transaction:

- Date

- Counterparty or payee

- Amount

- Currency

- Income source or expense category

- Payment method or account

- Invoice or receipt reference

- Client or project link (internal tag)

- Short purpose note when context is not obvious

Log each payout, invoice, refund, fee, and expense once, then link it to supporting files. Your weekly check is simple: each deposit ties back to an invoice or payout report, and each expense line ties to support.

Step 2: Reconcile books vs payer reports before filing#

Do this before filing, not after a mismatch shows up. Wait until income documents arrive, then compare your books with payer-filed forms and bank activity.

| Source | Recorded in your books | Reported to tax authorities | Action required |

|---|---|---|---|

| Card and third-party network payments | Gross sales with fees, refunds, and discounts tracked separately | Form 1099-K Box 1a may report gross payment amount, not reduced for fees, credits, refunds, shipping, cash equivalents, or discounts | Reconcile book gross receipts to 1099-K totals and document each difference |

| Direct client ACH, wire, or similar receipts | Invoice date, customer, amount, currency, bank receipt | You may receive an information return, or no form | Match each receipt to an invoice and report income even if no form arrives |

| Wage or other information returns | Matching income entries in your records | W-2, 1099-series, 1098, or similar forms | Do not file until each form is matched or investigated |

For any platform filing-threshold note, verify the current threshold. Threshold rules can change, and your income-reporting responsibility does not depend on receiving a 1099-K.

Step 3: Apply one evidence standard to every deduction#

A common failure mode is treating some expenses as if they need less proof than others. Use the same evidence standard every time: receipt or invoice, business purpose, client or project link as an internal tag, and storage location. A card statement alone may not be enough.

| Period | When it applies |

|---|---|

| 3 years | Generally for records that support income, deductions, and credits until the period of limitations runs out |

| 6 years | In certain omitted-income situations, including specific foreign-asset cases |

| At least 4 years | For employment tax records |

Supporting records should identify payee, amount, proof of payment, and date incurred. If one document does not cover all elements, keep a combined file set, such as a receipt, a statement excerpt, and a short note.

Keep records until the applicable period of limitations runs out: generally 3 years, 6 years in certain omitted-income situations, including specific foreign-asset cases, and at least 4 years for employment tax records.

Step 4: Run a lightweight compliance cycle with hard escalation rules#

Keep the cycle small and repeatable:

- Monthly close: categorize transactions, clear uncategorized items, match deposits, and attach missing support.

- Pre-filing check: reconcile books to all W-2, 1099, and 1098 documents received, confirm major differences, and resolve gross-vs-net mismatches.

- Advisor handoff: send books, reconciliation notes, open questions, and support files as one clean packet.

Escalate to a CPA, Enrolled Agent, or attorney when you need rebuilt books, multi-platform reconciliation, amended returns, or representation in IRS correspondence. CPAs, EAs, and attorneys have unlimited representation rights before the IRS. Use Form 2848 if you want someone to represent, advocate, or negotiate for you. The return third-party designee checkbox is not enough for audit or compliance representation.

Escalate to a tax attorney, or another person admitted before the U.S. Tax Court, when the matter is moving toward Tax Court or you are considering a petition. Keep one non-negotiable rule: if a notice includes a Tax Court filing window, calendar it immediately. IRS discussions do not extend that filing window, and late petitions are not considered. You remain accountable for what is reported on your return, even when an advisor helps.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Turn your prevention checklist into a live record before your next filing cycle with the Tax Residency Tracker.

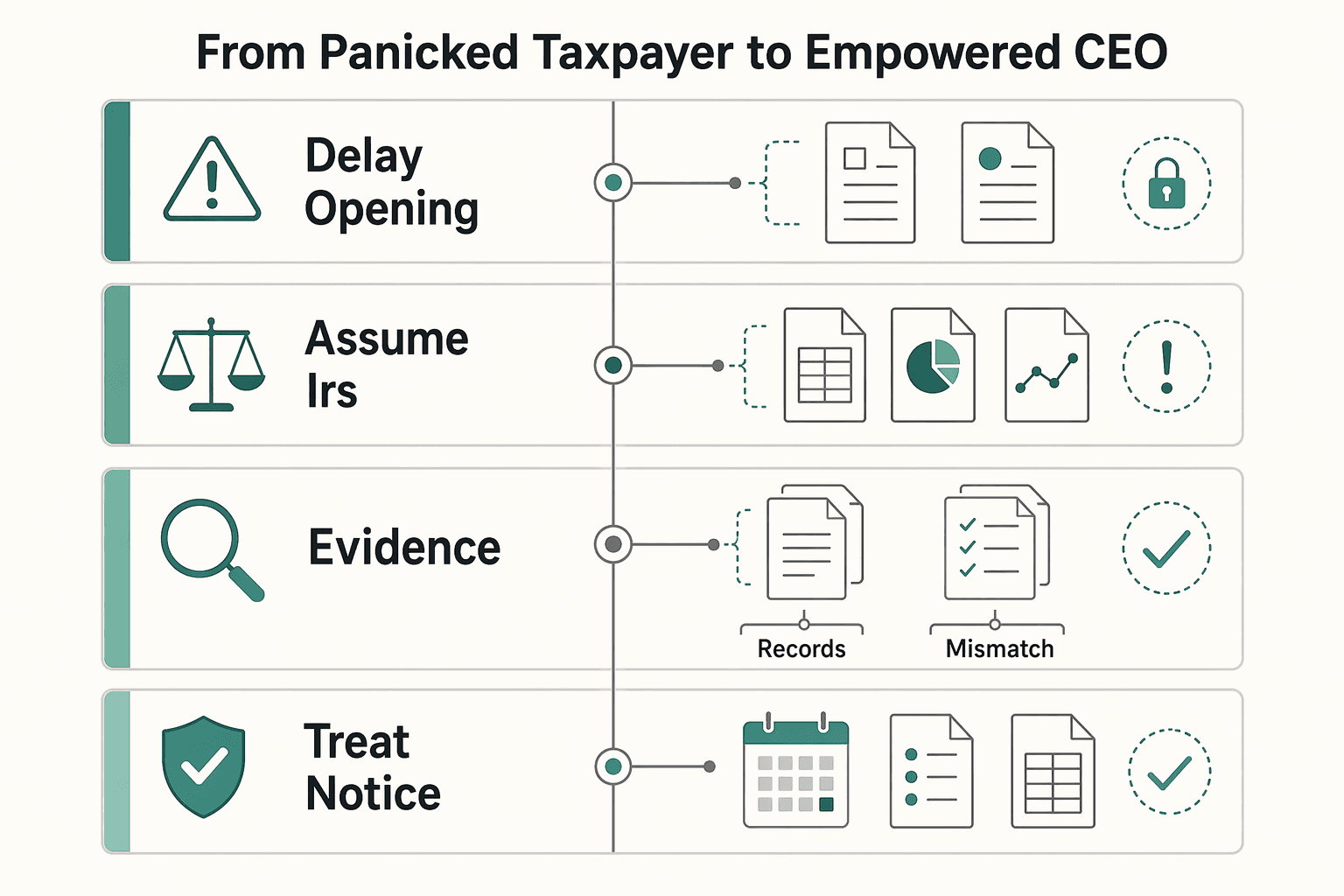

From Panicked Taxpayer to Empowered CEO#

Treat this as an operating issue, not a verdict. A notice of deficiency is a proposed tax change, not a final bill or audit determination. Your job is to verify what changed, protect your court rights on time, and fix the control gap that let the mismatch happen.

Start by reading the notice against your filed return and isolating each disputed item. Before you decide anything, be able to state the tax year, the deadline shown on the notice, and the specific mismatch the IRS identified. Not every disputed item can be challenged in Tax Court, so confirm which items are eligible before you escalate.

Then protect the court window. You generally have 90 days from the date on the notice, or 150 days if it was addressed to you outside the United States, to file a petition with the U.S. Tax Court, not the IRS, and sending additional information to the IRS does not extend that deadline.

| Panic reaction | CEO action | Likely outcome |

|---|---|---|

| Delay opening or reviewing the notice | Review it immediately and compare IRS changes to your return | You can identify exactly what is disputed |

| Assume IRS correspondence extends all timelines | Calendar the Tax Court deadline from the notice date | You preserve your right to petition |

| Send documents without a structured response | Send a signed statement with supporting copies and keep your court timeline separate | You respond on substance without losing procedural rights |

| Treat the notice as personal failure | Document the process failure and add preventive controls | You reduce repeat mismatch risk |

Then choose your lane. If you agree, follow the notice instructions, and the package may include Form 5564. If you disagree, respond immediately with a signed statement and supporting copies, and escalate to a qualified tax professional when the issue is technical, disputed, or not fully documented.

Before you close the case, lock in prevention: keep tax forms and source documents together, review them before filing, and define an escalation trigger for items you cannot substantiate quickly. That is how you turn one notice into a repeatable compliance process.

For a step-by-step walkthrough, see How to Respond to an IRS Mail Audit Notice.

After you resolve this notice, explore Gruv Tools.

Frequently Asked Questions

What is the first thing you should do if you get an IRS Notice of Deficiency?

Takeaway: Read the IRS Notice of Deficiency immediately and calendar the deadline shown on that specific notice. Next, keep a copy for your records and organize the notice, related forms, and the documents that support your position.

Does this mean you are being audited?

Takeaway: No. A statutory notice is a proposed tax change, not a final bill, and not an audit. Next, treat it as a focused dispute and identify exactly what item the IRS says does not match.

Can you handle it yourself?

Takeaway: It depends on the complexity of your case and how clear your records are. Next, if the facts are disputed or unclear, consider getting help from a CPA, Enrolled Agent, or tax attorney and share your notice and supporting documents.

What happens if you agree with the proposed change?

Takeaway: If you agree, you can usually sign and return the waiver form included with your notice. Next, verify the exact waiver form on your letter because notices do not all use the same one. For Letter 3219B, the waiver form is Form 4089, and returning it without payment leads to a later bill with interest and applicable penalties.

What happens if you ignore it or miss the filing window?

Takeaway: This is the hard failure mode, because a late Tax Court petition will not be considered. Next, use the date on your notice to confirm your filing window; for CP3219N, it is generally 90 days from the notice date (150 days for persons outside the country).

How do you dispute it and avoid another one later?

Takeaway: If you disagree, reply quickly and preserve your right to file a Tax Court petition by the date on your notice. Next, sending additional information does not extend that petition deadline; if you petition, the Tax Court encourages eFiling, and you will need to register for a DAWSON account.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

The Best Digital Nomad Cities for Entrepreneurs and Startups

Choosing a nomad base for your company is an execution decision first. Lifestyle matters, but it belongs in the second round. The costly mistakes usually show up after the city-ranking stage, when a place that looks great online turns into a slow or expensive setup once you start invoicing, signing contracts, and working against real deadlines.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.