Quick Answer

Handle a Roth conversion ladder by making planned annual conversions from pretax retirement accounts into a Roth IRA, tracking each conversion separately, and managing the tax cost in the conversion year. Estimate your baseline taxable income first, set a firm bracket ceiling, move tax cash to a reserve the same day, and follow Roth ordering and 5-year rules before any withdrawal.

The Roth Conversion Ladder: A Strategic Framework for the 'Business-of-One'#

If you plan to use retirement funds before age 59½, a Roth conversion ladder gives you a more controlled path than relying on early IRA distributions, which generally can trigger a 10% additional tax unless an exception applies. It is a multi-year process of moving pretax retirement money into a Roth IRA one conversion at a time.

You convert money from a traditional or other non-Roth retirement account into a Roth IRA, and the converted amount is taxed as ordinary income in that conversion year. The tradeoff is simple: pay tax now for more flexibility later.

Each conversion is its own rung, and each rung has its own 5-year holding period that starts on January 1 of the conversion year. Track every rung separately so your timeline and tax reporting stay clean. Use this quick screen so you do not confuse ladder planning with backdoor planning:

| Rung | Conversion tax year | 5-year clock starts | Access review window | Tracking fields |

|---|---|---|---|---|

| 1 | [YYYY] | January 1, [YYYY] | Review in [YYYY+5] | Amount [$], source account [], Form 8606 [Y/N] |

| 2 | [YYYY] | January 1, [YYYY] | Review in [YYYY+5] | Amount [$], source account [], Form 8606 [Y/N] |

| 3 | [YYYY] | January 1, [YYYY] | Review in [YYYY+5] | Amount [$], source account [], Form 8606 [Y/N] |

| Strategy | Use this when | Do not use this when |

|---|---|---|

| Roth conversion ladder | You want planned access to existing pretax retirement balances before 59½ and can manage the conversion-year tax cost. | Your main issue is only getting new money into a Roth IRA despite income limits. |

| Backdoor Roth IRA | Your income blocks direct Roth contributions, so you use the two-step contribute-then-convert path. | You are trying to build a multi-year access schedule for existing pretax balances. |

Two common mistakes are assuming one 5-year clock covers all conversions and converting without a plan for the tax bill. Before Phase 1, make sure you can check off the basics:

- list the pretax accounts you may convert from

- confirm the Roth IRA that will receive conversions

- create a tracker for conversion year, amount, source account, and Form 8606

- note which years give you room to recognize ordinary income without added pressure

If you want a deeper dive, read Japan Digital Nomad Visa: A Guide to the New 2025 Program.

Phase 1: Building Your Bulletproof Conversion Architecture#

Phase 1 is about making the first conversion hard to mess up. Before any money moves, set up records, a clean transfer path, separation between money types, and a tax reserve process you can repeat every time.

Build your conversion file before you place any transfer#

Your file should let you prove what happened, when it happened, and how it was reported. That matters because untaxed amounts in a traditional IRA become taxable when converted, and reporting still applies even when the transfer is trustee-to-trustee or handled at the same custodian. Keep it simple: one folder structure, one tracker, and one owner per item.

| Record item | Required fields | Document location | Owner |

|---|---|---|---|

| Conversion tracker row | Conversion date, tax year, amount converted, source account, receiving Roth IRA, cash or asset transfer, confirmation number | Master spreadsheet | You |

| Custodian confirmation | Submitted instruction (PDF/screenshot), completion notice, transaction ID | Retirement/Roth conversions/YYYY/Confirmations | You |

| Form 1099-R | Payer, gross distribution, taxable amount (if shown), tax year | Retirement/Tax forms/YYYY | You or tax preparer |

| Form 5498 | Roth conversion contribution amount, fair market value details as reported | Retirement/Tax forms/YYYY | You or tax preparer |

| Form 8606 | Filed status, tax year, preparer, copy saved | Taxes/YYYY/Filed return | You or tax preparer |

| Tax payment proof | Estimated payment date, amount, confirmation, bank transfer record | Taxes/YYYY/Estimated payments | You |

| Procedure note | Current custodian steps, cutoffs, whether in-kind is available, listed fees, support contact | Retirement/Procedures | You |

| Compliance check | Current form requirement pending official IRS verification | Retirement/Procedures | You |

Quick readiness check: if you cannot find each document in under five minutes, your Phase 1 records are not ready.

Choose the transfer path that reduces avoidable errors#

The cleanest path is usually the one that keeps money moving directly between IRA accounts. If both IRAs are at one institution, use its internal trustee instruction process instead of taking funds personally.

| Check | What to confirm |

|---|---|

| Custodian workflow | The custodian supports traditional IRA to Roth IRA trustee-directed conversion |

| Conversion format | The conversion must be cash-only or can be done in-kind |

| Fees and transaction details | The fee disclosures and transaction details are acceptable |

| Review and confirmations | The request flow gives you review screens and written confirmations |

Before you submit, verify every item above. The last one matters more than it looks: review screens and written confirmations help prevent accidental distribution errors.

Do not rely on "fix it later." Conversions for tax years after December 31, 2017 cannot be recharacterized back to a traditional IRA.

Segregate converted money from other Roth dollars#

This is one of the easiest controls to skip and one of the most useful later. Keep converted amounts separately tracked from regular Roth contributions so future withdrawal analysis and reporting stay cleaner.

One option is to use one Roth IRA for conversion amounts and another for regular contributions. If you keep everything in one account, the minimum workable approach is a ledger that tags each entry as regular contribution, conversion amount, or earnings, with tax year, amount, and linked documents.

Fund the tax reserve the same day you convert#

Conversion day should also be tax-reserve day. The tax system is pay-as-you-go, and underpayment can create penalties. Use this mini-playbook:

| Playbook item | Article details |

|---|---|

| Trigger event | Conversion settles |

| Estimate method | Project added federal tax from the conversion, then compare your running payments to safe-harbor checks (90% of current-year tax, or 100% of prior-year tax, or 110% of prior-year tax if prior-year AGI was above $150,000) |

| Transfer rule | Move the estimated amount immediately into a dedicated tax savings account |

| Reconciliation cadence | Review monthly and check payment timing before April 15, June 15, Sept. 15, and Jan. 15 (following year) |

| State estimated-tax check | Current state estimated-tax requirement pending official state tax verification |

Run that playbook every time rather than leaving the tax reserve decision for later.

Confirm Phase 1 is actually done#

Do not move to Phase 2 until the setup is real, not assumed. Continue only if all of these are true:

- I have the source IRA, receiving Roth IRA, and documented custodian procedure.

- I confirmed trustee-directed conversion workflow and whether in-kind is available.

- My records system is live, including confirmations and Forms 1099-R, 5498, and 8606.

- Converted amounts and regular contributions are separately tracked.

- My tax sinking fund process is active, with estimate method and review dates defined.

You might also find this useful: A Guide to Backdoor Roth IRAs for High-Earners.

Phase 2: The Variable Income Execution Engine#

Once the setup is solid, the annual job is straightforward: estimate your taxable-income range, choose a bracket ceiling, and convert only up to that limit.

Estimate baseline taxable income before any conversion#

Start with projected taxable income without a conversion, using a low/base/high range if your income is variable. Your conversion amount sits on top of that range, so the baseline needs to be explicit.

For 2026, the standard deduction is $16,100 (single or married filing separately) and $32,200 (married filing jointly) if you use the standard deduction. Use current-year IRS figures when you plan, because thresholds are updated annually.

Keep the tax effect straight. Converted amounts are included in income, except for any basis portion. Save your planning worksheet or tax-planning screenshot with your conversion records so you can show how you set the range.

Set a hard "do not exceed" bracket target#

Pick the highest marginal bracket you are willing to accept, then convert only up to that ceiling. This is the control that keeps a flexible plan from turning into an expensive one.

Maximum conversion amount = verified bracket cap - projected baseline taxable income

Use a verified entry in your tracker so you do not freeze stale numbers: Do not exceed bracket target: current bracket target pending official IRS verification

For 2026 planning context, the IRS lists 22% over $50,400 (single) / $100,800 (MFJ), and 37% over $640,600 (single) / $768,700 (MFJ). The 2026 inflation-adjustment release was issued Oct. 9, 2025 and covered more than 60 tax provisions, so annual verification is important.

Because conversions made on or after January 1, 2018 generally cannot be recharacterized back to a traditional IRA, treat your ceiling as final when you execute.

| Income scenario | Recommended action | Primary risk | When to pause conversions |

|---|---|---|---|

| Lower-income year | Use most or all room under your bracket cap | Late-year income changes or basis handling errors | Pause until current-year thresholds and year-end range are rechecked |

| Typical year | Convert part of remaining room and recheck before year-end | Small income surprises push you over target | Pause if your range now overlaps your cap |

| Higher-income year | Do a small conversion or skip | Paying a higher marginal rate to stay on schedule | Pause if baseline income is already at/above your target bracket |

Use market downturns only with clean in-kind execution controls#

A down market can be a useful time to evaluate a conversion, but only if you already want those assets inside the Roth and can document the transfer cleanly. For property conversions, the amount is generally the asset's fair market value on the distribution date, so valuation timing affects reported income.

Before you submit an in-kind conversion, check these items:

- select assets you intend to hold long term in the Roth

- confirm the custodian supports in-kind conversion and how it determines fair market value

- record ticker, share count, conversion date, and value used at transfer

- store the custodian confirmation with your tracker so Form 1099-R and Form 8606 reporting can be tied back to the transaction

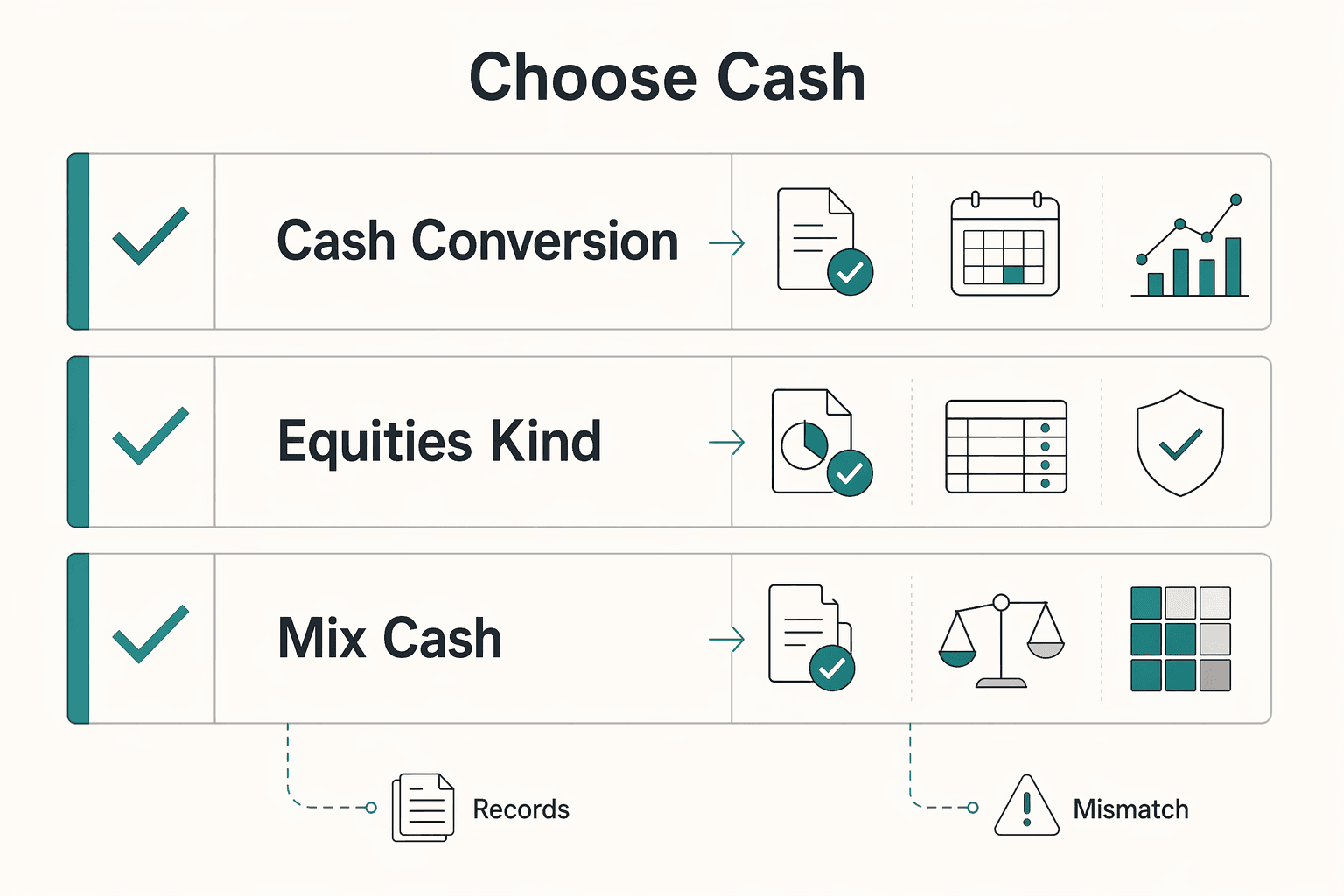

Choose cash, equities, or a mix with a practical risk matrix#

The right transfer method depends on your constraints, not your preferences. The question is not what sounds smart in theory, but what you can execute and document cleanly.

| Transfer choice | Best fit | Main tradeoff | Avoid when |

|---|---|---|---|

| Cash conversion | You need precise dollar control or near-term liquidity | Simpler amount control, but less equity exposure in Roth | You have long horizon and want to move specific growth assets now |

| Equities in-kind conversion | You have long horizon and higher volatility tolerance | More valuation sensitivity and tighter documentation burden | You cannot tolerate short-term swings or weak recordkeeping |

| Mix (cash + equities) | You want bracket precision plus selective upside | More moving parts to manage | You cannot maintain clean execution records |

Before you move to Phase 3, confirm the annual plan is fully documented:

- verify the current-year IRS threshold you are using

- lock low/base/high taxable-income estimates

- set and document your do-not-exceed bracket target

- decide full, partial, or pause for this year

- if converting securities, confirm in-kind rules and capture valuation evidence

- confirm records will reconcile to Form 1099-R and Form 8606

That gives you a controlled annual conversion amount. Next comes the withdrawal side. Related: The FIRE Movement for Freelancers: A Path to Financial Independence. Before you finalize this year's conversion amount, pressure-test your expat income assumptions with the FEIE calculator.

Phase 3: The Withdrawal Protocol & The Expat 'Red Alert'#

The ladder is only useful if the withdrawal side is disciplined too. Before every Roth distribution, run the same sequence: identify the source bucket, confirm seasoning and qualification status, and write down the reasoning.

Identify the source bucket before you request a distribution#

Start with the ordering rule in 26 CFR 1.408A-10. Roth IRA distributions are deemed to come out in this order: regular contributions, then conversion contributions, then earnings. That means the first control is classification from your records, not assumptions about what you meant to withdraw.

If you have multiple conversion years, direct contributions, or rollovers, build a one-page ledger first. At minimum, reconcile cumulative regular contributions, each conversion year and amount, and the remaining balance that can only be earnings.

| Roth bucket | Tax treatment | Penalty risk | Required checks |

|---|---|---|---|

| Regular contributions | Current withdrawal tax treatment pending official IRS verification | Current penalty treatment pending official IRS verification | Confirm cumulative lifetime regular contributions from your records before classifying dollars here |

| Conversion contributions | Conversion amount was treated as a distribution from the traditional IRA and a rollover contribution to the Roth when executed; current withdrawal treatment needs rule verification | Current conversion-withdrawal penalty treatment pending official IRS verification | Match planned withdrawal to each conversion year and amount, not just total Roth balance |

| Earnings | Not includible in gross income only if the distribution is qualified under 26 CFR 1.408A-6 | Current earnings-withdrawal penalty treatment pending official IRS verification | Verify the applicable 5-taxable-year test and any other qualifying condition against official IRS rules before using earnings for the bridge |

Confirm seasoning status and document why this withdrawal works#

Once the bucket is identified, test qualified-distribution status under 26 CFR 1.408A-6. The rule includes a 5-taxable-year requirement, and that period starts on the first day of the relevant taxable year or, if earlier, the first day of the taxable year of the first conversion contribution. Age 59½ is one listed qualifying condition, so do not treat earnings as automatically qualified based only on account age.

Write down three points for every withdrawal and keep that note with statements and conversion confirmations:

- which bucket is being distributed

- whether the 5-taxable-year requirement is met

- why you are treating the distribution as qualified or non-qualified

Separate FEIE from conversion income if you live abroad#

If you live abroad, keep FEIE and conversion treatment separate from the start. FEIE applies to earned income for personal services such as wages, salaries, professional fees, and similar compensation. Under 26 CFR 1.408A-4, a conversion is treated as a distribution from a traditional IRA and a rollover contribution to a Roth IRA.

In practice, do not assume conversion income is excluded under FEIE. U.S. persons abroad are taxed on worldwide income, and FEIE is not a blanket exclusion for all income types. Misclassification can distort taxable-income reporting and create avoidable cashflow stress at filing time.

Use FTC as a decision framework, not an assumption#

FTC may help, but only if the facts support it. This is not a place for shortcuts. Use this framework before relying on FTC:

May help when: foreign income tax was actually paid, the tax can qualify under IRS creditability tests, and you have usable foreign-source income in the relevant category.May not help when: taxes relate to income excluded under FEIE/foreign housing exclusion, treaty-rate reductions limit creditable tax, or category limits reduce usable credit.Required inputs: foreign tax payment records, income sourcing by category, current-year Form 1116 category setup, prior carryback/carryforward detail.Where treaty/sourcing can change outcomes: treaty re-sourcing may change source treatment and can require a separate FTC limitation computation.

Pre-withdrawal checklist for expats#

Before any distribution, confirm you have:

| Checklist item | What to have |

|---|---|

| Records by year | Contribution and conversion records by year, plus a bucket-classification note for this withdrawal |

| Qualified-status check | A written qualified-status check, including the 5-taxable-year requirement and relevant condition checks |

| Foreign tax records | Current-year foreign tax records and prior Form 1116 workpapers, including any carryback/carryforward history (1-year carryback, 10-year carryforward) |

| Local-country treatment | A note on local-country treatment of Roth conversions/withdrawals where U.S. and local rules may differ |

| Specialist review | A specialist-review trigger if you have multiple conversion lots, prior FEIE elections, treaty positions, or multiple Form 1116 categories |

If any one of those is missing, stop and clean up the file before you request the distribution.

That protocol keeps the withdrawal process controlled and auditable. The FAQ covers the edge cases that usually trip people up first.

Your Ladder, Your Enterprise: Taking Control#

Treat the ladder like an annual operating discipline. Proceed only when your income, expected tax impact, and bridge funding are ready for that year's conversion.

Define your terms#

Use a few terms consistently so your notes and decisions stay readable:

- A Roth conversion ladder is a multi-year strategy of moving money from tax-deferred retirement accounts into a Roth IRA through planned annual conversions.

- A Roth conversion is a one-time move of funds into a Roth IRA.

- A risk control is a rule you follow to reduce avoidable errors, especially over-converting in one year or losing track of separate 5-year waiting periods.

Keep a short operating checklist#

The checklist should be short enough to use every year and specific enough to catch real mistakes:

| Control | Purpose | What must be true |

|---|---|---|

| Separate accounts | Keep spending cash, tax cash, and retirement assets from getting mixed | You can clearly identify each bucket before you convert |

| Tax cash plan | Avoid a conversion tax bill you cannot fund | You have cash available for the expected tax impact before execution |

| Conversion records | Track each conversion across years | Your annual conversion records align with account confirmations |

Use clear proceed/pause criteria#

Proceed when your year is relatively low income, the conversion amount still fits the tax bracket room you planned to use, and your bridge funding can cover spending during the initial 5-year wait before converted funds are available. Lower portfolio values can be an opportunity to start a ladder, but they are not a reason to ignore sizing discipline.

Pause when the planned conversion would push you into a higher bracket than intended, you are not prepared for the year-of-conversion tax impact, or your bridge funding is not in place. There is no stated cap on how many conversions you can do or how much you can convert, so conversion sizing is your main control against an unnecessary tax spike.

Run ongoing governance (plan, execute, review, adjust)#

Keep the cadence simple and repeatable:

- Plan: Set a total conversion target and split it into yearly amounts.

- Execute: Submit the annual conversion and store the confirmation in your record set.

- Review: Recheck income, expected tax impact, bridge funding, and each lot's 5-year status.

- Adjust: Increase, reduce, or skip the next conversion, and add any verified current-rule updates to your process notes.

For a step-by-step walkthrough, see How to Get Health Insurance as an Early Retiree (Before Medicare).

If you want to run this plan with clearer operational checklists, use Gruv's planning and workflow tools.

Frequently Asked Questions

What mistakes cause the most trouble?

The biggest problems are usually incomplete records, unclear assumptions, and acting before you verify the current rules that apply to your situation. If the expected tax impact is unclear or difficult to fund from outside cash, pause and get specialist tax review before you proceed.

How should you track multiple conversions?

Track each conversion as a separate entry with the actual date, amount moved, whether the confirmation was saved, and what still needs verification. A simple tracker is enough if it lets you reconcile dates, amounts, and confirmations easily.

Can you use this strategy as a U.S. expat?

Yes, but do not treat FEIE as a blanket shield. FEIE applies to foreign-earned income such as wages, salaries, professional fees, or other pay for personal services, while U.S. citizens or resident aliens abroad are still taxed on worldwide income. If you use the physical presence test, it requires 330 full days in any 12-consecutive-month period, so close counts or complex travel should get specialist review.

How much should you convert in a variable-income year?

Start by estimating current-year income, the likely tax impact, and the outside cash available to fund that tax, then write a brief decision note. If income is unusually high or your cash reserve is thin, reduce the amount or wait. After you execute, document what you assumed so you can defend the decision later.

How do you start without making the paperwork messy?

Start in order and do not skip the basics. Confirm account details with your custodian, request the conversion, save the transaction confirmation the same day, then log the date and amount in your permanent ledger. Move projected tax cash into a separate reserve account and add a brief control note that shows what still needs verification and where documents are stored.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

The FIRE Movement for Freelancers Who Need Reliable Cashflow

For freelancers, FIRE is more durable when your cash handling is predictable enough to support regular saving and investing through uneven client cycles. The practical order is simple: steady incoming cash where you can, decide in advance where each dollar goes, and automate only after the basics stop wobbling.

Backdoor Roth IRA SOP for High Earners

A **backdoor Roth IRA** is a strategy, not a separate account. You make a non-deductible contribution to a traditional IRA, then convert that amount to a Roth IRA. This usually matters when your modified AGI limits or blocks a direct Roth IRA contribution, even though Roth conversions are not income-limited.