Quick Answer

As a temporary resident in Mexico, the most reliable setup is three layers: private coverage first for major or time-sensitive care, voluntary IMSS as backup if you qualify, and cash or credit available for upfront costs. IMSS is not automatic day-one coverage, can involve pre-existing-condition barriers and waiting periods, and starts on the first day of the next month after enrollment.

The 3-Tier Risk Mitigation Framework: How to Build Your Health & Wealth Shield#

If you rely on one policy, you create a single point of failure. For a temporary resident in Mexico, the practical setup is three layers with separate jobs. Use private coverage for major or time-sensitive care, voluntary IMSS as a backup, and cash-pay capacity for the moments when billing does not work in real time.

Step 1 Use private cover as your first line for serious or time-sensitive care#

Use this tier for accidents, surgeries, hospital admissions, urgent specialist care, and other high-impact events where fast access matters.

Do not assume claims will run smoothly at the hospital. In Mexico, not all hospitals deal directly with insurers, so you may need to pay first and seek reimbursement later. Before you move, confirm which hospitals in your city are in network and whether your policy can pay the hospital directly.

Step 2 Add IMSS as a backup layer, not your universal default#

If you will stay in Mexico for more than 180 days and up to 4 years, IMSS can add redundancy if you qualify. The voluntary route is Seguro de Salud para la Familia, funded through prepaid annual fees. IMSS describes coverage that includes consultations, medicines, hospitalization, surgeries, emergency care, and specialties.

Use IMSS for backup access and routine public-system care when it fits your plan. Do not treat it as automatic day-one coverage or guaranteed acceptance. IMSS states there are pre-existing-condition barriers, waiting periods, and exclusions, and coverage starts on the first day of the month after enrollment.

| Tier | Trigger scenario | Where to seek care | Expected payment path | Common failure point |

|---|---|---|---|---|

| Private international or travel medical | Major accident, admission, urgent specialist care | Private hospital in your insurer network | Sometimes direct billing; sometimes reimbursement | Hospital requests deposit or declines direct billing |

| Voluntary IMSS | Backup care, routine treatment, public-network access | IMSS facilities | Prepaid annual fee | Coverage not active yet, exclusion, waiting period, or enrollment barrier |

| Cash-pay fallback | Urgent event when billing stalls or network is unclear | Nearest viable clinic or hospital | You pay upfront, then request reimbursement if eligible | Insufficient liquidity, card limits, missing claim documents |

Step 3 Keep a cash-pay fallback for gaps between policy wording and real care#

This layer matters when the nearest provider is out of network, the hospital will not bill your insurer directly, or treatment is needed before IMSS coverage starts. In Mexico, upfront payment may be required.

Set this up in advance: a dedicated emergency payment method, your policy details, ID copies, and claim instructions available offline. If you spend time in higher-risk or limited-care areas, add medical evacuation insurance.

Step 4 Set up the handoff before you need it#

A coverage stack works only if the handoff between layers is already clear. Use this sequence:

| Order | Action | Key check |

|---|---|---|

| 1 | Buy private cover first | Confirm network hospitals, direct-billing rules, exclusions, and emergency contact lines |

| 2 | Apply for IMSS second | Check eligibility, pre-existing-condition barriers, expected start date, and renewal inside the 30 days before annual expiration |

| 3 | Fund the cash layer third | Keep funds you can access the same day |

| 4 | Prepare your urgent-event pack | Store insurer hotline, IMSS details, ID copies, and a one-line triage rule: private first for major events, IMSS for backup, cash when billing delays care |

| 5 | Practice the emergency flow | Call 911 for an ambulance, then contact your insurer as soon as possible |

Related: Are You an Employee or a Contractor? A Self-Assessment Checklist.

Private vs. Public: A Strategic Analysis for the "Business-of-One"#

For expats comparing health coverage in Mexico, the useful question is not which system is better. It is which system should handle which event. If you are staying more than 180 days and less than 4 years, private cover and IMSS can solve different problems. The risk goes up when you treat them as interchangeable.

Step 1 Assign each option a clear role#

Give each system one clear job. Use private cover as your first line for high-stakes or time-sensitive care. Use Seguro de Salud para la Familia (IMSS) for public-network access and backup capacity.

IMSS is voluntary for people without another public social-security scheme. It is paid through cuotas anuales anticipadas, and coverage starts on the first day of the next month after enrollment. Care begins through your assigned UMF (Unidad de Medicina Familiar), which affects where you can first be seen. Checkpoint: if you cannot state in one sentence when you use private first versus IMSS first, your setup is still too vague.

Step 2 Compare how each system works in real life#

The biggest difference is not the brochure language, but how access, payment, and timing work when you actually need care.

| Decision point | Private cover | IMSS family plan | What to do |

|---|---|---|---|

| Access path | May offer direct private-hospital access, but not all hospitals deal directly with insurers | Starts in assigned UMF and may involve waiting periods for some services | Use private first when timing is critical |

| Provider path | Depends on insurer network and hospital participation | Public-network pathway tied to IMSS assignment | Verify your usable facilities before you buy |

| Payment flow | May be direct billing or reimbursement; upfront payment can still be required | Annual fee paid in advance; service delivered through IMSS system | Keep cash or credit available even if insured |

| Language support | Variable by city and provider | English support is not universal | Plan for Spanish support where needed |

| Best use | Urgent specialist care, admissions, surgery planning, major events | Backup access and routine public care within IMSS rules | Build triage rules around this split |

With private cover, the main risk is payment flow. A hospital may require upfront payment even when treatment is covered, and you then seek reimbursement. Before you travel, ask insurers which hospitals in your city are in network and which usually attempt direct billing.

With IMSS, the main risk is eligibility and timing. Pre-existing conditions can block enrollment, and some services have waiting periods, including examples of six months, ten months, and two years for listed conditions or procedures. Treat IMSS as a structured backup, not a day-one answer for known care needs.

Step 3 Price private cover around your real use pattern#

Price this around your geography and cash flow, not brand names. If you mostly stay in Mexico and nearby regions, compare narrower geographic coverage with broader worldwide coverage. Any fixed savings claim should be held until fresh insurer pricing is verified.

Then stress-test the cost sharing:

- Can you fund your deductible quickly?

- Can you handle an urgent hospital deposit if direct billing fails?

- Do you know the reimbursement document set your insurer requires?

If you live outside major urban areas, be stricter about network checks because medical and emergency availability can be more limited.

Step 4 Use IMSS intentionally and close common gaps#

IMSS is most useful when you value it for what it actually provides, not what you hope it will cover. Think in two buckets. First, the administrative value: annual enrollment plus prepaid participation. Second, the care-delivery value: access to IMSS medical, surgical, pharmaceutical, hospital, and maternity services, subject to IMSS rules, exclusions, and waiting periods.

Before you budget, verify the live IMSS fee table. Current IMSS pages show different effective years, 2025 vs 2026. One published table shows $9,300 for ages 0 to 19 and $22,150 for ages 80+, but confirm the current version before enrollment.

Use these triage rules:

- Use IMSS for: backup public care and routine visits that can follow the UMF route.

- Use private for: accidents, admissions, urgent specialist needs, surgery planning, and cases where delay is costly.

Do not leave dental and mental-health assumptions untested. IMSS shows oral-health service capacity, but inclusion depends on the specific service path and rules. For both IMSS and private cover, run this checklist:

- Confirm exclusions and waiting periods in writing.

- Check whether dental and mental-health benefits are standard, limited, or add-on only.

- Set a dedicated out-of-pocket buffer for these categories. Current threshold pending insurer or provider verification.

Done well, this turns private cover and IMSS from competing ideas into a plan you can actually use. For a step-by-step walkthrough, see A Guide to Health Insurance for Freelancers in Germany.

Navigating the Gauntlet: A Strategic Plan for IMSS Enrollment#

Treat IMSS enrollment as a document-and-timing exercise, not a one-time errand. For Seguro de Salud para la Familia, use procedure IMSS-02-014 and validate your identity data, NSS, and medical questionnaire before you submit.

Before you start#

Confirm eligibility first. This voluntary IMSS option is for people who do not have coverage through another public social security institution. You can file initial enrollment through IMSS Digital or at your corresponding subdelegation. The digital route applies only to initial enrollment. In-person hours are published as Monday to Friday, 08:00 to 15:30.

Use this rule to decide whether to hire help:

- DIY if your Spanish is functional, you can attend weekday office hours, your paperwork is straightforward, and you can track each requirement yourself.

- Use a helper or legal representative if language, schedule, or family-document complexity makes repeat visits likely, or if you want one point person for the handoffs.

If you hire help, define the scope up front: document prep only, or full support through subdelegation filing, payment tracking, and UMF registration.

Step 1. Verify your file before filing#

Start with document control, then forms.

| Item to verify | What to check |

|---|---|

| Identity | Accepted official ID, consistent across records |

| Residency status | Current immigration evidence; do not assume temporary resident status guarantees IMSS acceptance |

| CURP | Present and matched exactly to your legal name |

| NSS | NSS for each family member in the enrollment set |

| Proof of address | Current comprobante de domicilio aligned with the subdelegation for your address |

| Civil-status documents | Birth certificate and, if applicable, marriage certificate; confirm current requirements before filing |

| Form set | General-data application and medical questionnaire, completed consistently |

Checkpoint: names, dates of birth, CURP, and NSS should match across all documents.

Step 2. Follow the handoff timeline#

Most enrollment delays come from assumptions about what counts as approval, what counts as activation, and which office handles the file. Follow the sequence closely.

| Stage | Outcome | Common delay |

|---|---|---|

| Intake | Your file enters review | Wrong office, missing NSS, or incomplete family-member records |

| Review and medical questionnaire validation | IMSS evaluates data and eligibility | Inconsistent answers, unclear pre-existing-condition history, or document-format questions |

| Annual-fee payment | Enrollment is credited only after payment | Treating approval as activation or missing payment proof |

| Confirmation and UMF registration | You appear at your assigned Unidad de Medicina Familiar with a copy of the medical questionnaire and request registration as a derechohabiente | Not confirming UMF assignment or missing questionnaire copy |

| Activation date | Coverage starts on the first day of the next month after contracting | Assuming same-day access before activation |

Do not blur these into one step. Approval is not activation, payment is not UMF registration, and UMF registration is not same-day access.

Step 3. Control eligibility and waiting-period risk#

This is the main risk-control area. IMSS distinguishes enrollment-blocking pre-existing conditions from conditions with waiting periods, so verify the current condition list and waiting-period details from official IMSS records before relying on the checklist.

Also track two post-enrollment controls. All enrolled family members must attend medical review within the first six months. IMSS states that if a listed condition is diagnosed as pre-existing during the first year, that member's coverage is canceled with no refund of the paid quota. Keep copies of everything submitted, and keep private coverage active through activation and the early review period.

You might also find this useful: Tax Residency in Mexico: Beyond the Temporary Resident Visa. Before you submit documents, turn your move steps into a single checklist with the Visa Cheatsheet for Digital Nomads.

The CFO's Playbook: Advanced Health & Wealth Protection Strategies#

Once your IMSS enrollment is moving, make the coverage stack usable under pressure. At this stage, the work is practical: document your tax file correctly, choose the right claim path, and set clear IMSS-versus-private triage rules.

Before you start#

Create one claim-ready folder you can access from your phone and laptop. Include your policy summary, insurer emergency contacts, member ID cards, passport or resident ID copies, IMSS enrollment records, and a short medical snapshot with blood type, medications, and allergies. Checkpoint: you or someone with you should be able to open this file in under two minutes during an emergency.

Step 1. Run the tax deduction as a compliance checklist#

If you are self-employed and file in the U.S., treat this as a compliance checklist, not a generic tax tip.

- Use Form 7206 to calculate the self-employed health insurance deduction.

- Report the result on Schedule 1 (Form 1040), line 17.

- Confirm eligibility first: IRS instructions require that at least one listed status condition is true.

- Confirm one core condition where relevant: self-employment with net profit on Schedule C or Schedule F.

- Confirm the plan is established (or considered established) under your business.

- Do not treat this deduction as a reduction to self-employment tax. It does not reduce net earnings for that calculation.

- Keep records: policy schedule, premium payment proof, covered-person details, and your or your family coverage records.

- Current amount limit pending official IRS verification.

Work with a qualified preparer who has, at minimum, an IRS PTIN and experience with self-employed cross-border returns. The test is simple: they should be able to explain why your plan does or does not qualify as established under the business, and how your Form 7206 result flows to Schedule 1 line 17.

Step 2. Build your claim-ready file now#

Most claim problems start long before the claim. Build the file before any incident, and store the documents you will actually need:

| File item | What to store |

|---|---|

| Policy | Policy summary and benefit terms |

| Contacts | Insurer emergency line and claims contacts |

| ID | Member card and ID documents |

| Payment proof | Recent premium payment proof |

| Forms or portal details | Pre-authorisation and claim forms, or portal or app process details |

| Medical records | Medical records and diagnosis notes |

| Invoices | Facturas electrónicas (CFDI) and proof of payment |

At minimum, keep the policy, contacts, ID, premium proof, forms or portal details, medical records, and Facturas electrónicas (CFDI) together.

Do not assume translation is always required, but be ready to add translations if your insurer requests clarification. In reimbursement cases, missing diagnosis details or valid invoices can delay processing.

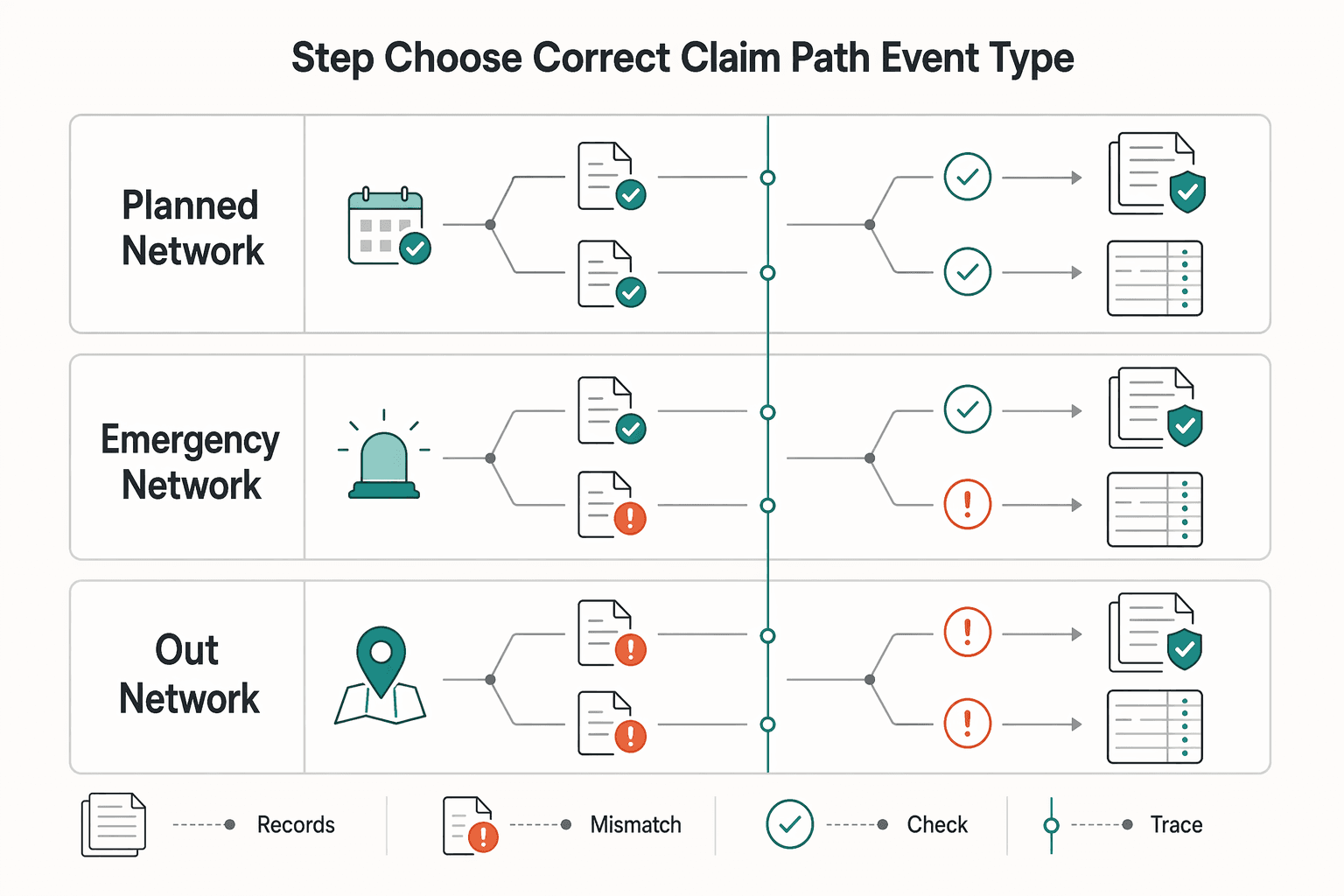

Step 3. Choose the correct claim path by event type#

Claim friction usually comes down to two things: pre-authorisation and network status. Those two factors also drive your cash-flow risk.

| Event type | Pre-authorisation | Who pays first | Records to collect | Timeline expectation | Escalation path |

|---|---|---|---|---|---|

| Planned in-network care | Often required for inpatient or high-cost treatment; may enable direct settlement | Plan terms vary; with pre-authorisation, approved in-network care may be settled directly | Approval record, diagnosis, estimate, final invoice | Some plans apply a treatment-use window after approval (for example, 31 days in one plan) | Insurer case team, then formal complaint route if needed |

| Emergency in-network admission | Notify insurer quickly even if you could not pre-clear before arrival (example window: 48 hours) | Payment handling depends on plan and network terms; keep receipts for anything you pay | Admission note, diagnosis, treating physician details, invoices you paid | Depends on plan terms and document completeness | Insurer emergency line first, then complaints channel if authorization stalls |

| Out-of-network care | Direct billing is less common; reimbursement path is common | You may need to pay upfront and claim later | Diagnosis, eligible invoice copies, supporting documents, payment proof, discharge records | Varies by insurer; one example target is 5 working days after complete paperwork | Insurer complaints team, then CONDUSEF Portal de Queja Electrónica or user-attention channels |

Keep originals after reimbursement. Some insurers may request originals for audit for up to 12 months after settlement.

Step 4. Apply clear IMSS/private triage and handoff rules#

This is where your setup becomes usable. Give each system the cases it handles best:

- Use IMSS, including your UMF route, for routine, stable, non-urgent care when timing is acceptable.

- Consider private care first for urgent, specialist-led, diagnostic-heavy, or hospital-based events.

- If IMSS referral timing does not match clinical urgency, switch to private care immediately and preserve all records.

- Do not drop private coverage only because IMSS enrollment is active. IMSS materials still reference pre-existing-condition exclusions and waiting periods.

If you want a deeper dive, read The Crypto Cautionary Tale: Why Freelancers Should Be Wary of Crypto Payments.

From Anxiety to Autonomy: Owning Your Health Strategy#

A workable strategy is not complicated. It works when three things are true: your compliance paperwork is in order, your major-event coverage is active, and your emergency care path is already decided.

Step 1#

Start with the items that can fail quietly. If you are on temporary resident status, that status is for stays longer than 180 days and shorter than 4 years. After entering Mexico on that visa, you should complete the INM resident ID step. Re-verify visa and filing requirements before you act, since consular requirements can change without notice.

If you are using IMSS Seguro de Salud para la Familia, treat activation timing as a hard checkpoint. Coverage starts on the first day of the next month after contracting, and enrollment requires identification, birth certificate, CURP, and proof of address. Verification: you can show an active start date and produce your residency and insurance documents in under five minutes.

Step 2#

Do not wait until a crisis to test your private-hospital path. Ask your insurer and one hospital you would actually use whether your exact policy supports direct billing there. Some facilities can settle eligible inpatient or day-case treatment cashlessly, but not every provider or location will.

Plan for pay-and-claim as a live fallback. Keep your insurance ID card and claim paperwork accessible on your phone and in print. Verification: you have one named hospital, one insurer contact number, and one confirmed direct-billing answer.

Step 3#

Set your cash-pay fallback now, not at admission. Hospitals in Mexico often require upfront payment and may place a card hold, and some overseas care is reimbursed later rather than paid directly. Do not rely on U.S. government payment support for overseas medical bills. If evacuation is part of your risk profile, U.S. mission guidance notes costs can be $10,000 and up.

Also set one emergency notification rule with your insurer. Some plans ask you or a companion to notify them within 48 hours after treatment is sought. Verification: you know which card, limit, reserve, and person will be used if direct billing fails.

Step 4#

Review this setup on a cycle, not just once. The point is to catch quiet failures before they become expensive ones.

| Decision area | What to confirm | What to fix next |

|---|---|---|

| Residency and document control | Resident ID step completed or scheduled; insurance ID, visa, CURP, and claim forms accessible | Re-verify current filing requirements and rebuild your document folder |

| Major-event protection | Policy active; start date confirmed; hospital network and direct billing checked with a real provider | Replace assumptions with fresh insurer and hospital confirmation |

| Emergency care path | Upfront payment method available; insurer emergency number saved; 48-hour notice rule checked | Set cash reserve or card capacity and brief your emergency contact |

Next review cycle, do this sequence before finalizing decisions:

- Re-verify current visa requirements through the relevant consulate or INM source records.

- Re-verify direct-billing and emergency-notice workflow directly with the insurer.

- Reconfirm one hospital billing path and refresh your document pack with current cards, forms, and contact numbers.

We covered this in detail in The Best Private Health Insurance Providers for Expats in Germany.

As you finalize your Mexico setup, track residency timing and tax steps in one place with the Tax Residency Tracker.

Frequently Asked Questions

Is IMSS insurance good enough for expats in Mexico?

Usually not if you also want private-hospital options. Use IMSS Seguro de Salud para la Familia as a public-coverage layer, not as your only plan. It starts on the first day of the next month after you contract and can include pre-existing-condition barriers, waiting periods, and exclusions.

How much does private health insurance cost for an American in Mexico?

Do not rely on old price ranges. Request fresh quotes for Mexican Seguro de Gastos Médicos Mayores and for emergency-focused travel health or medical evacuation cover. Pricing varies by policy terms, so also verify exclusions, waiting periods, network hospitals, and whether payment is direct or reimbursement.

What is the best health insurance for US expats in Mexico?

There is no single best option for everyone. IMSS is a voluntary public plan with defined benefits and eligibility limits, while Mexican private major medical is built for major accident or illness expenses. Travel or evacuation cover is usually narrower and focused on emergency events, not routine care by default.

Can I use my US health insurance in Mexico?

Assume nothing until you confirm your policy terms. Medicare and Medicaid do not pay for care outside the United States, and hospitals in Mexico usually require upfront payment and may place a credit-card hold at admission. Some U.S. private plans reimburse later, which still means you may need to pay first.

Do I need a temporary resident visa to get health insurance in Mexico?

Confirm product requirements before you apply. A temporary resident visa is for stays longer than 180 days and shorter than 4 years, and after entry you must process your residence card within 30 calendar days. For IMSS, check family-plan eligibility first, and for other products confirm enrollment requirements directly with the insurer.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cdc.gov/yellow-book/hcp/health-care-abroad/travel-in...trusted

- consulmex.sre.gob.mx/omaha/images/2025/visasingles/visatemp.pdftrusted

- consulmex.sre.gob.mx/leamington/index.php/non-mexicans/visas/115-...trusted

- imss.gob.mx/derechoH/segurosalud-familiatrusted

- imss.gob.mx/faq/seguro-familiatrusted

- irs.gov/forms-pubs/about-form-7206trusted

- irs.gov/instructions/i7206trusted

- mx.usembassy.gov/medical-practitionerstrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Freelance Crypto Payments That Protect Cashflow and Reduce Disputes

Crypto payments make sense only when they improve how reliably you get paid after you plan conversion, compliance, and recordkeeping up front. They can reduce friction in some international setups where traditional platforms add fees, restrictions, or extra steps. They also move risk onto conversion timing, exchange-fee exposure, and documentation quality, so use a simple acceptance test before you agree:

Are You an Employee or a Contractor? A Self-Assessment Checklist

Forget the label. Classification turns on the relationship you actually run, not the title you typed into the contract. It is also much easier to fix before you sign.

Tax Residency in Mexico for Nomads Beyond the Temporary Resident Visa

Start with one conservative call: are you likely becoming a Mexican tax resident this year, and what evidence supports that call today? That decision shapes the rest of your year. If you skip it, every later task turns reactive, from local tax planning to U.S. filing choices.