Quick Answer

Yes. For health insurance dubai freelancer planning, you need a DHA-compliant policy aligned to your visa route before filing and again at renewal. The minimum floor may satisfy compliance, but it may not fit your day-to-day care or travel pattern. Verify insurer licensing, coverage-period dates, network fit, and direct billing in writing, then keep the policy active without gaps. That supports visa progress and reduces avoidable disruption to your work.

Why This Isn't Just Paperwork - It's Your License to Operate#

If you are using Dubai's virtual work route, health insurance is part of your visa file from the application stage. Proof of cover is checked at application and again at renewal, so policy dates that do not line up with your filing timeline can create rework.

Before you start: The UAE's official virtual work route lists a copy of health insurance as a requirement, and GDRFA Dubai marks it as compulsory for issuance and mandatory for renewal. If you are applying through a different freelance or residence route, verify that route's current document list before you buy.

Match your policy to your visa channel#

For virtual work residence, health insurance proof is reviewed through ICP or GDRFA Dubai. Your practical job is simple: confirm where insurance is checked in your process so you are not fixing it after submission.

Validate the proof document, not just payment#

Use the Health Insurance Card, or equivalent insurer proof, that shows enrollment for the stated Coverage Period, including start and expiry. Also confirm that the insurer is licensed in Dubai by the Dubai Health Insurance Corporation. A quote or payment receipt alone may not show enrollment for the required period.

| Proof item | What it shows | If missing or wrong |

|---|---|---|

| Health Insurance Card or equivalent insurer proof | Confirms enrollment | Missing proof can lead to extra document checks, resubmission, or processing delays |

| Coverage Period | Shows start and expiry | Wrong dates can create rework or processing delays |

| Insurer licensing | Insurer is licensed in Dubai by the Dubai Health Insurance Corporation | An unlicensed insurer can lead to extra document checks, resubmission, or processing delays |

| Quote or payment receipt | May show payment | Alone it may not show enrollment for the required period |

Keep coverage continuous across your residence cycle#

A lapse is not just an admin problem. Dubai's legal framework allows fines from AED 500 to AED 150,000. Enforcement guidance says fines may be backdated to the breach date, and retained circulars include enforcement through visa applications. Repeating the same violation within 1 year can double the fine, capped at AED 500,000. If you see a route-specific lapse charge in practice, verify it against current guidance.

| Risk type | What triggers it | What it looks like for you |

|---|---|---|

| Legal risk | No valid cover or a lapse during the residence cycle | Fines, possible backdating, and enforcement exposure |

| Administrative delay risk | Missing proof, wrong dates, or an unlicensed insurer | Extra document checks, resubmission, or processing delays |

| Business continuity risk | Coverage gap while you are resident and working | Unplanned admin work and urgent policy replacement |

What to do now

- Confirm your insurer is licensed in Dubai.

- Confirm the policy validity window matches your application and renewal dates.

- Align coverage start and expiry with visa milestones, not quote timing.

That gets you into a valid filing position. Next, make sure the plan also works when you actually need care.

If you want a deeper dive, read The Crypto Cautionary Tale: Why Freelancers Should Be Wary of Crypto Payments.

Moving Beyond 'Cheap': A Framework for Assessing Your True Risk Profile#

Price should be your last filter, not your first. Use a risk-based approach: define your highest-impact exposures first, then compare plans against that risk map.

Build your practical coverage map before you compare plans#

Map where you may need care: your home base, your frequent travel corridors, and any place where routine care matters. For each area, decide whether you need emergency-only support or ongoing care, such as GP visits, prescriptions, follow-ups, and specialist access.

Then verify those needs against the policy wording and schedule of benefits, and mark each area as included, excluded, or unclear. If something appears in sales material but not in policy documents, treat it as unverified.

If your setup includes an ADGM regulatory application, add a separate checkpoint before submission: contact the FSRA Authorisation Function at [email protected], and confirm defined terms in the GLO Rulebook.

Check provider-network fit, not just network size#

Network size matters only if it matches how you expect to access care. Before you compare price, confirm these points in writing:

| Network check | What to confirm | Documentation |

|---|---|---|

| Preferred hospitals or clinics | Whether they are in-network | Use branch-level verification where possible |

| Direct billing | Whether it is available where you expect to use care | Keep confirmations in writing |

| Specialist care | Whether referral or pre-authorization is required, and how that process works | Confirm in writing |

| Out-of-network claims | How claims are handled, including required documents and timing | Confirm in writing |

Verify pre-existing and chronic-condition rules in writing#

If you have ongoing conditions, recurring medication, or likely specialist follow-up, get the coverage rules in writing before you buy. Use these prompts with the insurer:

- What is treated as pre-existing under this policy?

- How are chronic conditions handled: covered, limited, or approval-based?

- Is there a waiting period?

- Are medications, monitoring, and follow-up consultations included?

- What disclosures or medical records are required at application and claim stage?

Keep your proposal form, disclosures, and written responses together so there is one clear record if questions come up later.

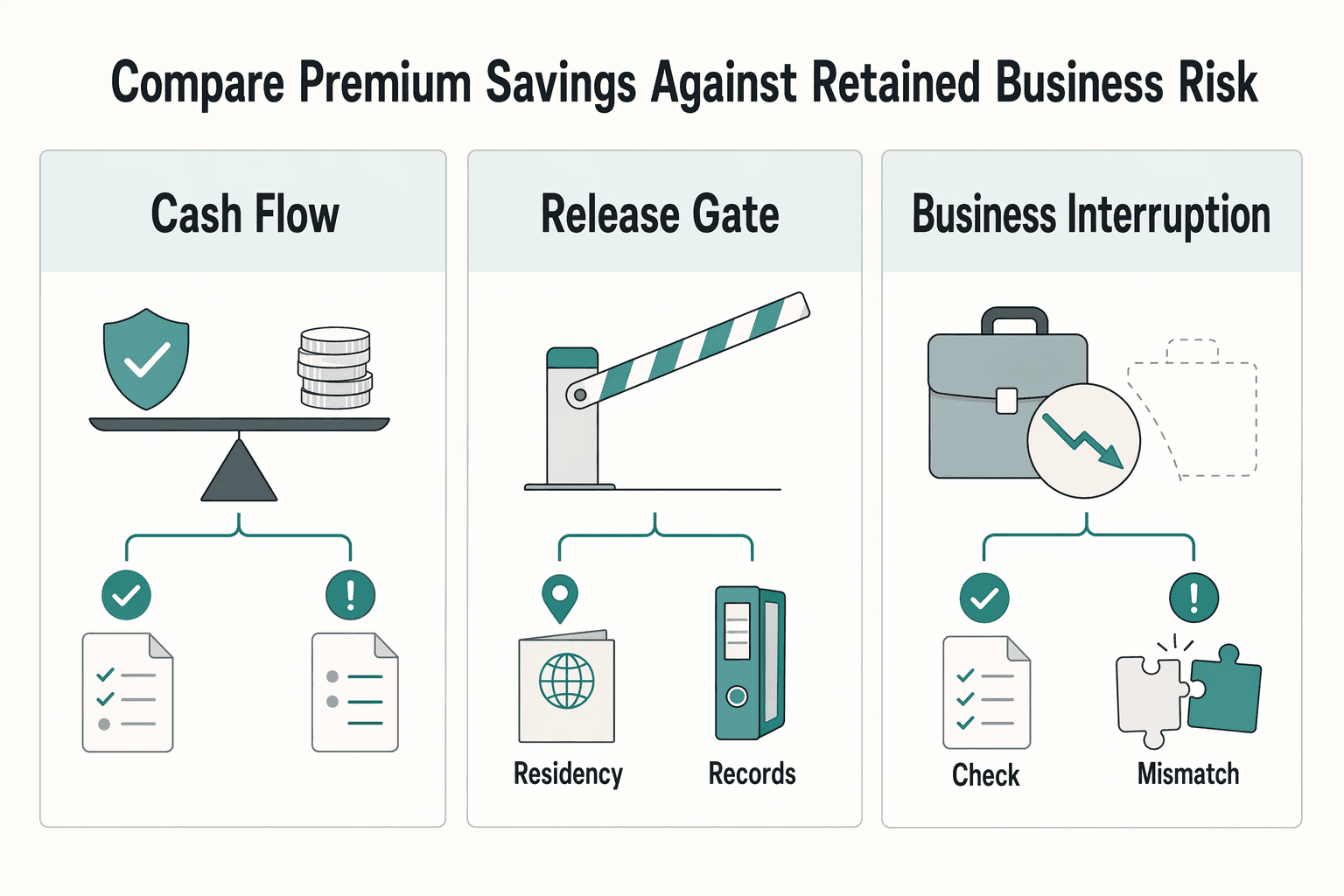

Compare premium savings against retained business risk#

The real comparison is not cheap versus expensive. It is which risks stay with you and which the plan absorbs.

| Decision area | Lower-premium option: what to verify | Broader option: what to verify |

|---|---|---|

| Cash flow | Whether you may need to pay upfront and rely on reimbursement | Whether direct billing meaningfully reduces upfront cash pressure |

| Treatment access | Whether network limits or approval steps could slow non-urgent care | Whether access rules are clearer and operationally easier for your use pattern |

| Business interruption | Whether claims and admin steps could extend downtime | Whether the process is likely to reduce disruption during core work periods |

Treat guidance as informative, not exhaustive, and confirm final terms in binding policy documents before deciding.

You might also find this useful: A Deep Dive into the UAE's Golden Visa Program for Freelancers.

How to Deconstruct Policy Fine Print Like a CEO#

Treat the policy wording and benefits schedule as the real product. The policy wording is the binding document, so if a clause is unclear there, treat it as unconfirmed, no matter how clean the brochure looks.

Before you start#

Collect these five documents in one folder:

- policy wording

- benefits schedule

- current network list, time-stamped

- pre-approval rules

- claims guide or stated claims turnaround

If you are reviewing a Dubai minimum-standard plan, also confirm which ISAHD appendix is currently in force. A 2024 circular states an updated EBP table effective 1 Jan 2025.

Check network access and direct billing#

Start with the practical question: can you use your actual providers without fronting large cash payments?

Pass/fail checks:

Pass:Your exact provider and branch are in-network on a current list, for your plan tier.Pass:direct billing is confirmed for those providers.Fail:You only get generic language like "available at most in-network hospitals and clinics," without plan-level confirmation.

Why this matters to cash flow and downtime:

- direct billing means the provider bills the insurer directly and you usually pay only your cost-share. That reduces upfront cash pressure.

Check international coverage, medical evacuation, and medical repatriation#

Pressure-test the overseas language against how and where you actually travel.

Pass/fail checks:

Pass:The policy clearly defines overseas scope, such as emergency-only versus broader care, along with geography and approval conditions.Pass:medical evacuation and medical repatriation are explicitly stated where relevant.Fail:"Worldwide cover" appears without clear trigger conditions or process detail.

Why this matters to cash flow and downtime:

- medical evacuation can cover transfer to the nearest appropriate medical center when local treatment is unavailable.

- medical repatriation can cover travel costs tied to moving for treatment when local treatment is unavailable.

Check cost-sharing mechanics, not just premium#

This is often where low-price plans become expensive in practice. You need to know what you still pay when care is needed.

Pass/fail checks:

Pass:You can identify each deductible, co-insurance, and sub-limit in the benefits schedule.Pass:You can estimate your out-of-pocket impact for a GP visit, specialist visit, scan, and hospital admission.Fail:The annual limit looks strong, but key services are constrained by narrow sub-limits or unclear cost-share wording.

Why this matters to cash flow and downtime:

- deductible: fixed amount you pay regardless of total treatment cost.

- co-insurance: percentage of covered care you pay.

- sub-limit: cap on a specific service or procedure inside the overall limit.

| Fine-print area | Acceptable clause language | Red-flag clause language | Action to take |

|---|---|---|---|

| Network | Named network, plan-specific, current list date shown | "Extensive network" with no dated attachment | Request current plan network list; verify provider by branch |

| Overseas cover | Scope and transport terms clearly defined | "Worldwide" with no conditions or benefit wording | Request exact overseas benefits page and approval triggers |

| Cost share | Deductible, co-insurance, sub-limit shown in schedule | "As per policy" with no schedule detail | Request benefits schedule; test one realistic treatment scenario |

| Authorizations and claims | Prior-approval services and filing requirements clearly stated | No clear pre-approval or document rules | Request pre-approval guide and claims document checklist |

Check claims process and turnaround#

Before you buy, make sure you can file correctly and understand the timing risk.

| Claims item | What to confirm | Article note |

|---|---|---|

| Filing deadline | Deadline for claim submission | Reimbursement usually depends on timely filing |

| Required documents | Documents needed for submission | Reimbursement usually depends on correct documents |

| Submission method | Whether filing is digital or manual | Make sure you can file correctly |

| Pre-approval rules | What needs pre-approval | Process gaps can delay repayment |

| Reimbursement turnaround | Turnaround confirmed in writing; some insurers publish 15 to 30 days | This is plan-specific |

Pass/fail checks:

Pass:You have the filing deadline, required documents, submission method, including whether filing is digital or manual, and pre-approval rules in writing.Pass:You confirmed the policy's reimbursement turnaround in writing. Some insurers publish ranges such as 15 to 30 days, but this is plan-specific.Fail:You get vague guidance like "just submit receipts."

Why this matters to cash flow and downtime:

- Reimbursement usually depends on correct documents and timely filing. Process gaps can delay repayment.

Before you commit, confirm you have:

- policy wording

- benefits schedule

- current network list

- pre-approval rules

- claims SLA or claims guide

Once you can read the fine print clearly, the market gets easier to sort. The next section gives you a faster way to narrow options without losing the important detail.

For related context, see How to Get Health Insurance in Spain as a Digital Nomad. Before you submit anything, use this visa planning checklist to map your insurance paperwork alongside the rest of your relocation steps: Visa Cheatsheet for Digital Nomads.

Navigating the Market: Three Tiers of Freelancer Health Insurance#

Use a three-tier filter to narrow options faster. Match the policy first to your stay length, then compare policy complexity and budget pressure before you decide. For 2026 planning, a practical first split is still short-stay travel medical insurance versus long-term international health insurance.

Pick your starting tier by how you actually work#

Tier 1: Short stay or strict budget control. This fits if you are testing Dubai, setting up temporarily, or minimizing fixed costs while income stabilizes. Compare current written quotes and full policy wording when you assess options. Risk rises when your expected care needs are not clearly covered or reimbursement timing could strain cash flow.

Tier 2: Long-term Dubai base with steady operations. This fits if Dubai is your main base and you want coverage aligned with longer-term living abroad. Risk rises if key terms stay unclear, including coverage scope, exclusions, and cost sharing.

Tier 3: Continuity-first, cross-border working style. This fits if you move between countries often and want one plan structure you can carry across locations. Risk rises when added portability features cost more than you realistically use.

Compare friction, not brochure language#

Policies vary across coverage, premiums, and exclusions, so treat this like any other fixed business cost. Compare what happens when you actually need care.

| Tier | Who this is for | Network strength | International portability | Pre-approval friction | Claims speed | Out-of-pocket exposure | Best fit by freelancer profile |

|---|---|---|---|---|---|---|---|

| Tier 1 | Short stay, temporary setup, or highest budget pressure | Verify current provider list in writing | Confirm exactly where coverage applies | Request written approval rules | Request written claims steps and contacts | Check deductibles, co-pays, and exclusions in wording | Trial phase, low expected care use, high price sensitivity |

| Tier 2 | Long-term local base with stable work rhythm | Verify local network depth for routine care | Confirm overseas terms and limits in writing | Ask how approvals work for planned and urgent care | Ask for written claims process details | Model cost sharing against your monthly budget | Full-time freelancer with regular local care expectations |

| Tier 3 | Frequent travel or high continuity needs | Verify local and overseas networks separately | Confirm cross-border terms in writing | Check approval rules for high-cost care across locations | Ask for service and escalation channels in writing | Stress-test total yearly cost against uneven income months | Cross-border operator with higher continuity needs |

Pressure-test bundled visa insurance before accepting it#

Bundled cover is not automatically bad, but it only deserves a yes after document review. Request these four items first. If any are missing, treat the bundle as unverified and pause the decision.

- Full policy wording

- Insurer name

- Current network list

- Upgrade options and switch process

Choose your tier in practice#

Use the same risk inputs from earlier sections:

- Stay duration: Short stays generally point first to travel medical insurance; longer-term living abroad generally points first to international health insurance.

- Policy complexity: Compare coverage, premiums, and exclusions in writing before you commit.

- Budget pressure: Budget insurance alongside fixed and variable expenses, then check sustainability against fluctuating income months.

- Planning discipline: Keep health insurance in your core remote-work logistics plan, not as a last-minute add-on.

Final budgeting check: freelancers often deal with month-to-month income swings, while insurance stays a fixed cost. Choose the highest tier you can sustain consistently, not just in a strong month.

Related: How to Manage Your Time Effectively as a Freelancer.

Your Health Insurance Is Your Ultimate Business Asset#

The practical goal is twofold: visa approval and business protection. If you optimize only for the application step, you can still miss the protection side when health issues disrupt delivery.

| Mindset | Primary goal | Short-term benefit | Operational risk | Best fit |

|---|---|---|---|---|

| Compliance-first | Put an acceptable policy in place for submission | Quicker submission progress | Day-to-day usability may be too narrow for how you actually work | You need an admin-ready starting point now |

| Risk-mitigation | Protect your ability to keep working during illness or injury | Better alignment between coverage and income continuity | More time spent validating details up front | Your income depends on consistent delivery and mobility |

Define your exposure#

Start with the interruption you cannot absorb. If even a short health disruption could delay client delivery or threaten renewals, this decision is not only about paperwork.

Before you compare plans, note three basics: how quickly you may need care, how sensitive your client work is to downtime, and how much unplanned spend you can absorb.

Match coverage depth to that exposure#

A leaner plan may fit if your immediate priority is submission readiness. If continuity matters more, put practical access and usability ahead of headline simplicity. The useful test is simple: if you are unwell for a week, does this plan help you recover and keep work moving, or does it add friction?

Confirm the plan is current and route-fit#

Validate details in writing, not just in a sales summary. Keep dated proof of what you are buying, and recheck recency before submission. One freelancer-insurance guide, for example, shows an update timestamp of February 19, 2026. That is exactly why last-mile checks matter.

- Verify current acceptance requirements for your specific visa route.

- Review plan details in writing, including what is and is not covered.

- Confirm whether your coverage needs to match where you live and work.

- Recheck current submission requirements before filing.

For a step-by-step walkthrough, see How to Get Health Insurance in Portugal as a Digital Nomad.

Once your Dubai insurance and visa setup are stable, you can simplify how you invoice clients and receive cross-border payments as a solo professional: Gruv for Freelancers.

Frequently Asked Questions

Do I need insurance before visa issuance or visa renewal?

Get a DHA-compliant plan before submitting on any route that requires health-insurance proof. For example, the UAE virtual work residence route lists a health-insurance copy as part of the requirements.

What is the minimum plan I can use?

Use a DHA-compliant plan if your immediate goal is minimum compliance. The Essential Benefits Plan (EBP) is the minimum-benefits floor referenced in Dubai materials, but minimum compliance does not guarantee broad access. Before you buy, confirm the current network works for where you live and work.

How much should I budget?

Set your budget by coverage path, then compare written quotes using the same deductible, region, and outpatient setup. If you compare only headline price, you can miss major differences in network quality and exclusions. Use current annual quotes for planning, then benchmark other options on the same assumptions.

Can I choose my own policy, or should I accept a bundled visa package?

Use the same checklist either way. Get the full policy wording, the current network list, written exclusions, waiting rules, sub-limits, and confirmation that the plan is accepted for your exact visa-processing route. If any item is missing, pause and treat the plan as unverified.

How should I judge portability if I work across countries?

Match portability to your real travel pattern, not marketing labels like “worldwide.” If you skip the policy wording, you may find too late that overseas care is limited, reimbursement-only, or emergency-only. Add home-country coverage only if you expect meaningful time there or need continuity with named providers.

What about pre-existing conditions?

Declare pre-existing conditions before you buy and ask for the handling terms in writing. Some Dubai materials indicate that pre-existing conditions should not automatically block cover, but treatment timing and scope can still vary by policy. If continuity matters for your work, confirm the exact rules before payment.

Can I use any cheap UAE basic package?

Check the scheme scope before buying a low-cost UAE policy. If you skip this check, you can pay for a plan that does not fit your Dubai residency path. One clear warning sign: WHI states its plans are not applicable for Dubai and Abu Dhabi visa holders.

What happens if I let my cover lapse?

Keep coverage continuous and check the current fines schedule before taking any gap risk. If your policy lapses, you can face penalties under Dubai’s health-insurance fines framework and create route-specific processing issues where insurance proof is required. Do not rely on older summaries when current compliance details are available.

What should I recheck right before applying?

Recheck live requirements at submission time, not only when you start researching. If you skip this final check, you can rely on outdated benefits, fees, or document rules. At minimum, recheck your visa route requirements, insurer acceptance status, latest policy wording, and current network list.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- dha.gov.ae/uploads/032022/AR2022322813.pdftrusted

- dlp.dubai.gov.ae/Legislation%20Reference/2013/Law%20No.%20%28...trusted

- gdrfad.gov.ae/en/services/f52024e3-b812-11ed-5210-4cd98f76...trusted

- gdrfad.gov.ae/en/services/f52024d1-b812-11ed-5210-4cd98f76...trusted

- madonna.edu/pdf/catalog-ug-2024-2025.pdftrusted

- mohre.gov.ae/en/guidance-and-awareness-portal-new/the-bas...trusted

- nyuad.nyu.edu/content/dam/nyuad/campus-life/volunteering-a...trusted

- state.gov/reports/2023-investment-climate-statements/uaetrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Freelance Crypto Payments That Protect Cashflow and Reduce Disputes

Crypto payments make sense only when they improve how reliably you get paid after you plan conversion, compliance, and recordkeeping up front. They can reduce friction in some international setups where traditional platforms add fees, restrictions, or extra steps. They also move risk onto conversion timing, exchange-fee exposure, and documentation quality, so use a simple acceptance test before you agree:

How to Manage Your Time Effectively as a Freelancer

Most freelancers struggle not because they work too few hours, but because they misallocate the hours they have—treating time as an infinite resource rather than a finite business asset with a real cost per unit. The solution is a three-layer operating system: a Time Budget Framework that commits hours to four categories before any client work is booked, a Weekly Operating Template that assigns those categories to specific calendar windows, and a monthly Admin Audit Checklist that reconciles invoicing, bookkeeping, and compliance records. Multi-client orchestration requires a WIP limit, dedicated client windows, and a capacity decision rule run before accepting new engagements. Together, these systems replace reactive decision-making with a repeatable structure that keeps delivery quality consistent, records audit-ready, and the freelance practice operationally durable.

UAE Golden Visa for Freelancers and the Green Visa Decision Guide

Choose the route your documents can support now, not the visa label with the most search volume. If you searched for `uae golden visa for freelancers`, use that as a starting query, then choose between Golden Residency and the Green route based on the evidence you can actually file.