Quick Answer

To get an ITIN as a non-resident, first confirm you are not eligible for an SSN, then complete Form W-7 and submit it with your federal return workflow, usually Form 1040 or Form 1040-NR. Apply by mail or in person based on document-handling confidence. Use a preflight check to prevent mismatches, and track status after submission so you can respond quickly to any IRS notice.

You Need an ITIN Without the Guesswork#

Approach an ITIN with an IRS-first sequence: verify your identifier path, prepare a complete Form W-7 package, then submit by mail or in person. If you run a business of one, treat it like an operations workflow. Make one clear identifier decision, build one clean package, and skip the guessing.

The point is to reduce rework, avoid compliance errors, and know exactly when to pause and escalate.

Before you start#

- Know the scope. An Individual Taxpayer Identification Number (ITIN) is a 9-digit number the IRS issues for federal tax purposes only.

- Check identifier eligibility first. If SSN eligibility is unclear, pause ITIN prep and confirm before you file.

- Set your return path. Plan around Form 1040 or Form 1040-NR from the start so your return workflow stays consistent.

- Plan per person. If family members apply, each applicant needs a separate Form W-7.

Run the decision framework#

Use this in order. Do not move forward until each line is clear.

| Decision point | If clear | If unclear |

|---|---|---|

| SSN vs ITIN path | Continue with ITIN prep | Pause and get confirmation before filing |

| Federal tax purpose | Build the ITIN application package | Do not submit yet |

| Form consistency | Align Form W-7 with Form 1040 or Form 1040-NR | Reconcile fields before filing |

| Document handling | Pick mail or in-person submission | Pause and confirm submission requirements in IRS guidance |

Step 1. Run the IRS ITIN eligibility interview. It helps you decide whether to file and takes about seven minutes. Step 2. Complete Form W-7 for each applicant. Treat names and filing details as controlled data, not draft text. Step 3. Prepare the return workflow. Leave SSN fields blank for each ITIN applicant listed on the return. Step 4. Choose your submission channel. The IRS accepts mail or in-person submission. Step 5. Apply the safe default. If a requirement feels ambiguous, pause and use Form W-7 instructions as the final check before you submit.

Example: a consultant filing in the U.S. with a spouse checks eligibility first, packages each person's Form W-7 cleanly, and submits once instead of falling into a correction loop.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Do You Need an ITIN or an SSN First?#

Start with one hard rule: if you have an SSN or can get one, do not start Form W-7.

This is the most important decision in the whole process. Get it wrong and everything downstream turns into wasted effort.

Run the binary gate first#

Step 1. Check current SSN status. Confirm whether you already have a Social Security number (SSN). Expected outcome: If yes, use that SSN on your U.S. federal income tax return and stop ITIN prep.

Step 2. Check SSN eligibility. If you do not have an SSN, confirm whether you can get one through SSA using Form SS-5. Expected outcome: If you are eligible, follow the SSN path and do not complete Form W-7.

Step 3. Check if an SSN application is pending. If you already applied for an SSN, wait for the result before filing Form W-7. Expected outcome: Keep Form W-7 paused until SSA gives a final determination.

| Decision point | Action now | Verification point |

|---|---|---|

| You already have an SSN | Use SSN and skip ITIN | Return uses SSN only |

| You are eligible for SSN | Use Form SS-5 pathway | SSN process started |

| SSN application pending | Pause Form W-7 | SSA decision received |

| SSA confirms SSN ineligibility | Start ITIN path | Form W-7 prep begins |

Confirm federal tax purpose before filing#

Step 4. Validate your federal tax purpose. Request an Individual Taxpayer Identification Number (ITIN) only when you need it for U.S. federal tax purposes. Expected outcome: You can clearly state the federal tax purpose for the request.

Step 5. Lock scope and apply a safe default. Treat the ITIN as a tax identifier only, not work authorization. If SSN eligibility is still unresolved after your checks, keep Form W-7 on hold until SSA determines whether you are ineligible for an SSN.

Example: a consultant gets conflicting advice online and pauses. They confirm SSN ineligibility, then move ahead with Form W-7 only after the identifier path is settled.

What Should You Prepare Before You Start?#

Prepare the full ITIN application package upfront, with Form W-7 aligned to Form 1040 or Form 1040-NR (unless an IRS exception applies), so you file once instead of fixing preventable mismatches later.

Once you clear the SSN versus ITIN gate, the next job is building the package. A clean package prevents avoidable stalls.

Build the package before you fill anything#

Step 1. Choose your return workflow first. Pick Form 1040 or Form 1040-NR when required for your filing path. Expected outcome: You can state which U.S. federal income tax return you will attach, if applicable.

Step 2. Create one Form W-7 per applicant. Each person applying for an Individual Taxpayer Identification Number needs a separate Form W-7. Expected outcome: You have one clearly labeled W-7 for each applicant.

Step 3. Stage supporting records early. Prepare proof of identity and foreign status, plus U.S. residency proof for dependents when required. Expected outcome: You can map every supporting record to the correct applicant before assembly.

| Prep item | Action | Verification point |

|---|---|---|

| Return form | Lock Form 1040 or Form 1040-NR when required | One return path only |

| Applicant forms | Draft Form W-7 for each person | No missing applicant |

| Family filing | Attach each spouse or dependent W-7 to front of return | Attachment order confirmed |

| SSN fields | Leave SSN areas blank for ITIN applicants | No placeholder SSNs |

Run a preflight consistency pass#

Step 4. Reconcile fields across forms and records. Match names, addresses, and applicant details across your package, then fix missing information before assembly. Expected outcome: No conflicting or incomplete entries remain.

Step 5. Check common rejection triggers before submission. Run a final pass for misspelled names, incorrect addresses, and missing information. Expected outcome: You have removed obvious data-entry issues that can cause rejections.

Step 6. Use Form W-7 instructions as your final authority. When details conflict, follow that instruction set before you submit to the IRS. Expected outcome: Your package stays consistent from prep through submission.

Example: a consultant preparing an ITIN package for a spouse catches a name mismatch during preflight. They fix it before filing and avoid a rejection cycle. If your residency position still feels unclear, settle it first with 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

How to Submit the ITIN Application Package Step by Step#

Submit your ITIN package in one controlled sequence: align Form W-7 to your return, assemble in filing order, then file only after every consistency check passes.

Prep gets you most of the way there. Submission is where last-minute errors creep in, so run it like a checklist.

Run the submission sequence#

Step 1. Complete Form W-7 and align core fields. Match names, dates, and applicant details to your U.S. federal income tax return before you move forward. Expected outcome: Your ITIN form and return read as one coherent record.

Step 2. Assemble in filing order. Attach Form W-7 to the front of the return and include all required items tied to allowable tax benefits. If you qualify for an exception to attaching a return, include the substitute documentation required for that exception. Expected outcome: Your package follows the filing path for your case, without partial assumptions.

Step 3. Run a preflight against IRS instructions. Recheck identity details, return attachment, and SSN handling on every page. Leave SSN fields blank for each ITIN applicant listed on the return. Expected outcome: You remove internal conflicts before submission.

| Preflight check | Pass rule |

|---|---|

| Name and applicant data | Exact match across Form W-7 and return |

| Return attachment rule | Form W-7 attached to the front of the return when required |

| SSN handling | Blank SSN area for each ITIN applicant |

| Exception path | Required substitute documents included |

Use a safe default when details get fuzzy#

Step 4. Pause when document authentication rules are unclear. Do not guess. Taxpayer Assistance Centers can authenticate most documents in person, but dependent school or medical records still require mailing with the package. Expected outcome: You choose the right submission path for each document type.

| Item | What the article says | Channel or timing |

|---|---|---|

| Most documents | Taxpayer Assistance Centers can authenticate most documents in person | In person |

| Dependent school or medical records | Still require mailing with the package | |

| Status notice | Around 7 weeks | Timing |

| Status notice in tax season or overseas cases | 9-11 weeks | Timing |

| Mailed supporting documents | Returned within 60 days | Timing |

Step 5. Keep a full copy and a tracking log. Keep a copy of your application for your records. Then log the send date, method, and key follow-up dates for status checks. Expect status notice timing around 7 weeks, or 9-11 weeks in tax season or overseas cases; if you mailed supporting documents, IRS says they are returned within 60 days. Expected outcome: You can respond quickly if you receive an assigned ITIN notice, a correction request, or a rejection notice.

Example: a freelancer pauses when a dependent document rule looks unclear. They choose the correct handling path and avoid a preventable resubmission cycle.

Should You Apply by Mail or In Person?#

Choose mail when your ITIN application package is complete and stable, and choose in person when you want stronger document-handling confidence before submission.

At this point, the question is not preference. It is operational risk. Where are your unknowns, and which channel reduces them?

Use this channel decision rubric#

| Decision factor | Mail fits best when | In person fits best when |

|---|---|---|

| Documentation certainty | You already validated every item in the package | You want a second procedural check before filing |

| Handling originals | You accept mailing the package | You want most supporting documents authenticated and returned immediately |

| Follow-up tolerance | You can handle follow-up without live help | You want direct help if issues come up |

| Filing urgency | You can move now with a ready package | You can secure an appointment in time |

| Support needs | You can execute Form W-7 without live help | You want help from a Certifying Acceptance Agent on review and IRS issue handling |

Use one rule to break ties. Pick the path with fewer unknowns today. Do not optimize for speed if your package still has ambiguity.

Follow the channel playbook#

Step 1. Confirm package readiness. Verify Form W-7 and the rest of your ITIN application package are complete and consistent. Expected outcome: You can submit without changing core fields.

Step 2. Select your channel with the rubric. Score certainty, urgency, and rework risk before you act. Expected outcome: You can explain your choice in one sentence.

Step 3. Execute mail submission when ready. Send the full ITIN application package only after final checks pass. Expected outcome: You keep your process organized.

Step 4. Execute in-person submission when confidence is the priority. Book ahead for an IRS Taxpayer Assistance Center with ITIN services and confirm scope before you go. The IRS notes appointments may take several weeks. Expected outcome: You avoid surprises at the appointment.

Step 5. Confirm support model if using a CAA. Ask how they will review Form W-7, what fees apply, and how they will coordinate with the IRS if issues appear. Expected outcome: You know who owns each next action.

Example: one freelancer mails a fully preflighted package. Another chooses an in-person path because document-handling confidence is the bottleneck.

What Happens After Submission and How Do You Recover Fast?#

Track your case in three lanes, act on the exact IRS notice you receive, and trigger a recovery checklist the moment anything breaks.

Submission is not the finish line. Your post-submit process is what keeps a small issue from turning into a multi-week detour.

Track your status lane and act fast#

Step 1. Start a status clock on submission day. Use a baseline of seven weeks for an IRS status notice, and plan for nine to eleven weeks during tax season or if you applied from overseas. Expected outcome: You follow a realistic follow-up window instead of reacting too early.

Step 2. Classify your notice into one lane. Use the first notice to route your next move.

| Lane | Signal | Next action |

|---|---|---|

| Pending assignment | No notice yet within normal window | Keep tracking and hold package copy ready |

| Assigned | CP565 notice | Use your Individual Taxpayer Identification Number on future federal filings |

| Correction needed | CP566 or CP567 notice | Provide requested information or resubmit, based on what the notice requires |

Step 3. Watch your document return timing. If you mailed supporting documents, track the 60 day return window and update your archive when they arrive. Expected outcome: You keep a complete record for ITIN renewal and future filings.

Recover quickly and keep filings consistent#

Step 4. Use the lost ITIN safe default. If you lose your ITIN, do not apply for a new number. Expected outcome: You avoid duplicate identifier problems.

| Situation | Action | Detail |

|---|---|---|

| Lost ITIN | Do not apply for a new number | Avoid duplicate identifier problems |

| Expired ITIN | Renew in person, by mail, or by submitting Form W-7 with your tax return | Restore a valid identifier before it blocks filing |

| Federal return entry | Enter the ITIN in the same space where your federal tax return asks for an SSN | Keep return processing aligned |

| Form 8938 and FBAR | Evaluate them as separate tracks | File FBAR with FinCEN, not with the IRS |

Step 5. Run an ITIN renewal path for expired numbers. Renew in person, by mail, or by submitting Form W-7 with your tax return. Expected outcome: You restore a valid identifier before it blocks filing.

Step 6. Keep return workflow consistent. Enter the ITIN in the same space where your federal tax return asks for an SSN. Expected outcome: Your federal return processing stays aligned.

Step 7. Route adjacent reporting separately. Evaluate Form 8938 and FBAR obligations as separate tracks, and file FBAR with FinCEN, not with the IRS. Expected outcome: You avoid mixing forms that follow different filing systems.

Example: a consultant receives a correction notice and fixes what the IRS asked for that same week. They log every change and keep the next filing cycle on schedule.

Common ITIN Mistakes and the Recovery Playbook#

Prevent ITIN delays by enforcing five gates: confirm SSN ineligibility, reconcile every field, limit ITIN scope to federal tax purpose, map downstream filings, and escalate early on ambiguity.

These are the repeat offenders that turn a straightforward filing into a correction cycle. Use this as a reset sequence whenever something breaks.

Run the five step recovery sequence#

| Gate | Recovery action | Expected outcome |

|---|---|---|

| SSN eligibility | Stop Form W-7 work until you clear SSN eligibility | You avoid filing on the wrong track |

| Form consistency | Reconcile Form W-7 against your return field by field; leave SSN fields blank on the return for each ITIN applicant; attach a separate Form W-7 | Your submission reads as one consistent package |

| ITIN scope | Treat the ITIN as an IRS tax processing identifier only, not work authorization and not a general legal ID | You prevent scope drift that creates downstream filing mistakes |

| Downstream filings | Check whether Schedule SE applies to your self-employment workflow, then test FBAR and Form 8938 separately; file FBAR with FinCEN, not with the IRS | You manage recurring obligations as distinct tracks instead of one blended guess |

| Escalation | Escalate to an acceptance agent when application issues need IRS coordination, or involve a qualified tax professional when rules conflict, facts stay ambiguous, or a correction cycle repeats | You stop compounding risk with DIY assumptions |

- Step 1. Stop Form W-7 work until you clear SSN eligibility. If SSN eligibility stays unclear, pause and validate your identifier path first. Restart Form W-7 only after you confirm you need an Individual Taxpayer Identification Number for a federal tax purpose.

Expected outcome: You avoid filing on the wrong track.

- Step 2. Reconcile Form W-7 against your return field by field. Match applicant details and entries exactly. For each ITIN applicant, leave SSN fields blank on the return and attach a separate Form W-7.

Expected outcome: Your submission reads as one consistent package.

- Step 3. Reset ITIN scope before you share it. Treat the ITIN as an IRS tax processing identifier only, not work authorization and not a general legal ID.

Expected outcome: You prevent scope drift that creates downstream filing mistakes.

- Step 4. Map downstream filings after issuance. Check whether Schedule SE applies to your self-employment workflow, then test FBAR and Form 8938 separately because one does not replace the other. File FBAR with FinCEN, not with the IRS.

Expected outcome: You manage recurring obligations as distinct tracks instead of one blended guess.

- Step 5. Set escalation triggers now. Escalate to an acceptance agent when application issues need IRS coordination, or involve a qualified tax professional when rules conflict, facts stay ambiguous, or a correction cycle repeats.

Expected outcome: You stop compounding risk with DIY assumptions.

Example: a consultant finds a name mismatch between Form W-7 and the return. They pause submission, reconcile every applicant line, and escalate one unresolved tax residency question before filing.

Related: The Best Bank Accounts for Freelancers in the UK.

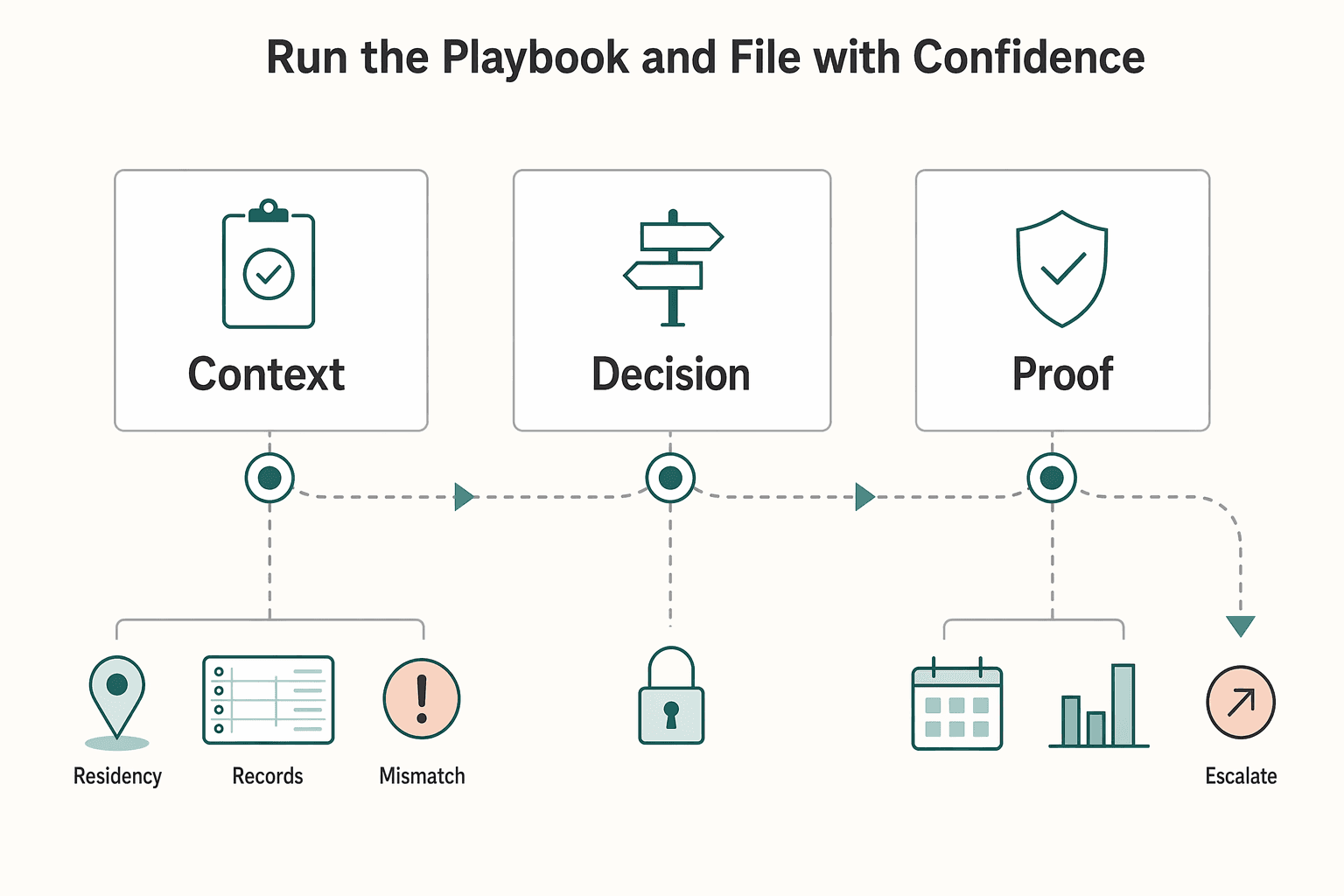

Run the Playbook and File With Confidence#

Run this in order: clear SSN eligibility, confirm federal tax purpose, submit a clean ITIN application package, then monitor status and renewal triggers.

You have the system. Now run it once, end to end, without side quests.

- Step 1. Confirm SSN eligibility status first. If you have or can obtain a Social Security number, stop the ITIN path. Use an Individual Taxpayer Identification Number only when you are not eligible for an SSN.

Expected outcome: You avoid filing the wrong identifier request.

- Step 2. Confirm your federal tax purpose. Tie your filing to a clear U.S. federal tax requirement before touching Form W-7. Keep scope tight, because an ITIN supports federal tax administration only.

Expected outcome: You file for the right reason and avoid scope drift.

- Step 3. Complete Form W-7 with per-person discipline. Prepare one Form W-7 for each applicant if a spouse or dependents also need an ITIN. Do not treat one form as a family shortcut.

Expected outcome: Your package matches IRS processing logic.

- Step 4. Prepare Form 1040 or Form 1040-NR to match the ITIN flow. Keep return data consistent with Form W-7 and leave SSN fields blank for ITIN applicants listed on the return.

Expected outcome: You reduce mismatch notices and correction cycles.

- Step 5. Choose your submission path based on document risk. Apply by mail if your package is complete and you accept asynchronous handling. Choose an IRS Taxpayer Assistance Center or Certifying Acceptance Agent if you want in-person document support and prefer not to mail original documents.

Expected outcome: You align process speed with document-handling confidence.

- Step 6. Track post-submission milestones. Use seven weeks as a baseline status window, and expect nine to eleven weeks during peak season or for overseas applications. If you mailed original documents and they do not return within 60 days, contact the IRS.

Expected outcome: You catch delays early and recover fast.

- Step 7. Set renewal and escalation guardrails. If an ITIN goes unused on a federal return for three consecutive tax years, it expires on December 31 after the third year. Escalate through an IRS ITIN service channel or an acceptance agent when eligibility or cross-border facts remain unclear.

Expected outcome: You keep non-resident tax compliance stable over time.

Example: a freelancer pauses before submission and confirms there is no SSN path. They fix one mismatched field between Form W-7 and Form 1040-NR, choose a TAC appointment, and reduce resubmission risk.

Frequently Asked Questions

Do I need an ITIN if I am a non-resident freelancer?

Not always. You need an ITIN when you have a federal tax purpose (such as filing a U.S. federal income tax return) and you are not eligible for an SSN. If you are eligible for an SSN, use that path first.

Should I apply for an ITIN or an SSN first?

Start with SSN eligibility. If you qualify for a Social Security number, do not start Form W-7. If you do not qualify and still need to file, request an individual taxpayer identification number.

What exactly must be included with Form W-7?

Build one ITIN application package that aligns Form W-7 with your Form 1040 or Form 1040-NR workflow. Include supporting identity and foreign-status documents, and include U.S. residency proof for dependents when required.

Can I apply for an ITIN without filing a tax return?

In many cases, you file Form W-7 with a federal return. In limited exception cases, you can apply without attaching a standard return. If you think an exception applies, verify it before submission so you do not trigger a preventable rejection.

Is mail or in-person submission better for first-time applicants?

Mail works when your package is complete and you can tolerate waiting. In person can reduce document-handling uncertainty because most supporting documents can be authenticated and returned immediately.

What should I do if my ITIN is lost or expired?

If your ITIN is expired and you will include it on a federal return, renew it before filing. ITINs expire on December 31 after three consecutive tax years of non-use. If you do not know your number, use the no or do not know option on Form W-7 instead of guessing.

When should I stop DIY and talk to a tax professional?

Escalate when SSN eligibility is unclear, your facts span multiple countries, or your ITIN application has issues you cannot resolve cleanly. If timelines matter, remember status updates often take about seven weeks and can stretch to nine to eleven weeks between January 15 and April 30 or for overseas applications. If you want a broader non-resident tax framework after this how to get an itin guide, read 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

The Best Bank Accounts for Freelancers in the UK

Confirm with each provider directly, as UK bank product details and eligibility requirements can change. Always verify the current terms on official provider pages before applying.