Quick Answer

Start with the IRS online account because it is usually the fastest route when identity verification succeeds. If that path fails, use Form 4506-T for broader transcript requests, or use phone or mail when you only need a tax return or tax account transcript sent to your IRS address on file. For most lending or visa documentation, begin with a Tax Return Transcript and move to a Record of Account Transcript when both filed return data and account activity are needed.

Why an IRS Transcript is a Critical Asset for Your Global Business-of-One#

For most cross-border reviews, an IRS transcript is usually the best starting document because it gives you IRS-issued verification without requiring your full return packet. In many cases, that is enough. A transcript is not a full copy of your filed return. It is an IRS record, such as a Tax Return Transcript or Record of Account Transcript. A full return copy includes the complete filed return and attachments requested through Form 4506.

That distinction matters because your own return is still a self-provided copy, while a transcript is generated by the IRS for verification. It also masks some personal identifiers while keeping the financial entries visible, which is often a better fit when you need to prove income and filing history. Match the document to the decision the institution is actually making:

- Residency or immigration review: requirements vary by office. If they accept IRS documentation for income proof, start with a Tax Return Transcript. Use a Record of Account Transcript when they also want account-level history in one document.

- Mortgage or lending underwriting: IRS guidance says a Tax Return Transcript usually meets mortgage lender needs. Confirm the required tax years up front, since Tax Return Transcripts are generally available for the current tax year and 3 prior tax years.

- Compliance or due diligence checks: transcripts can be easier for reviewers to match and validate. If they provide a Customer File Number, include it to help matching.

Use a full return copy only when the requester explicitly needs the exact filed packet, including attachments such as W-2s and schedules, rather than verification of income or filing history.

| Document | Cost | Delivery speed | Authority signal | Typical acceptance context |

|---|---|---|---|---|

| Tax Return Transcript | $0 | Fastest online; by mail, allow 5 to 10 calendar days | IRS-issued transcript showing most original Form 1040 line items, forms, and schedules | Income verification, lending, housing, and benefits applications |

| Record of Account Transcript | $0 | Depends on request method | IRS-issued combined return and account transcript information | Cases where both return data and account history are requested |

| Copy of Tax Return (Form 4506) | $30 per return | May take up to 75 days | IRS-issued complete copy with attachments | Exact-return or attachment-specific requests |

As a safe default, start with a transcript when a counterparty needs credible proof of your income and filing history. Move to a full return copy only when they explicitly require the complete filed return with attachments.

Related: How to Get a PTIN from the IRS as a Tax Preparer.

Choosing Your Strategic Asset: Which IRS Transcript Do You Need?#

Choose the smallest IRS document that proves exactly what the reviewer needs. If they only need income as filed, start with a Tax Return Transcript. If they need post-filing activity, use a Tax Account Transcript or, when they want one combined file, a Record of Account Transcript.

Step 1. Decode the request before you order anything#

Start with the requester's exact wording, then map it to the validation goal. Most reviewers need one of five things: filed return line items, account activity after filing, both in one document, third-party wage and income data, or non-filing status. Before you request anything, confirm:

- Tax year(s)

- Exact requested document language

- Whether they need income-only proof, post-filing account changes, or both

If they ask for a "tax return," ask directly whether an IRS Tax Return Transcript is acceptable or whether they require a full filed return copy with attachments.

Step 2. Match the request to the minimum document that satisfies the check#

Use the minimum document that closes the review, then verify acceptance with the reviewer.

A Tax Return Transcript shows most original Form 1040-series line items as filed, without post-filing changes. A Tax Account Transcript shows basic return data plus payments and post-filing changes. A Record of Account Transcript combines return and account views in one document. A Wage and Income Transcript shows IRS-received forms such as W-2, 1098, 1099, and 5498. A Verification of Non-filing Letter confirms only that no processed 1040-series return is on record as of the request date.

| Document | You use it to prove | Best when | May be rejected when | Common use context | Acceptance nuance |

|---|---|---|---|---|---|

| Tax Return Transcript | What you filed originally | They need filed income; year is within current year + 3 prior years | They need post-filing changes, payment history, or a full filed return copy | Income-as-filed verification | Confirm current acceptance with the reviewer before you submit |

| Tax Account Transcript | Post-filing account activity | They need payments, adjustments, or account status; online can cover current year + 9 prior years | They need return line items and account data in one file | Account-change and payment verification | Confirm current acceptance with the reviewer before you submit |

| Record of Account Transcript | Filed return data plus account history | You want one document that answers both "what was filed?" and "what changed after filing?" | They explicitly require the full filed return packet with attachments | Combined return-plus-account verification | Confirm current acceptance with the reviewer before you submit |

| Wage and Income Transcript | Third-party information returns IRS received | They need payer-reported data such as W-2, 1099, 1098, or 5498; current processing-year data is generally available in first week in February | They need proof of what you filed; online generation is limited to approximately 85 income documents | Third-party payer-data checks | Confirm current acceptance with the reviewer before you submit |

| Verification of Non-filing Letter | No processed 1040-series return on file as of request date | They specifically request non-filing status for a year; current tax year is not available before June 15 | They want proof you had no filing requirement, which this letter does not prove | Formal non-filing status requests | Confirm current acceptance with the reviewer before you submit |

Treat this table as a selection tool, not acceptance proof. Acceptance is institution-specific and jurisdiction-specific, so verify with the actual reviewer before you submit.

Step 3. Use a clear escalation rule#

Start with a Tax Return Transcript when income-as-filed is enough. The IRS says this usually meets many mortgage lender needs.

Move to a Tax Account Transcript when post-filing payments or changes may matter. Use a Record of Account Transcript when you want one file that covers both filed income and account history.

Step 4. Hand off edge cases early#

Some requests are not really transcript-selection questions. If they explicitly require a photocopy or full filed return, schedules, or attachments, you're in Form 4506 territory, with a fee of $30 per return.

Also escalate before submission if they require non-English documents. IRS transcripts are English-only, and transcript availability can be limited in some conditions.

For a step-by-step walkthrough, see How to Get a Certificate of Residence (Form 6166) from the IRS.

The Expat's Decision Matrix: Selecting Your Optimal Retrieval Method#

Pick your retrieval path by failure risk first, then speed. For most expats, the practical order is Individual Online Account first, Form 4506-T if online access fails or the request type or volume needs it, and automated phone only as a constrained backup.

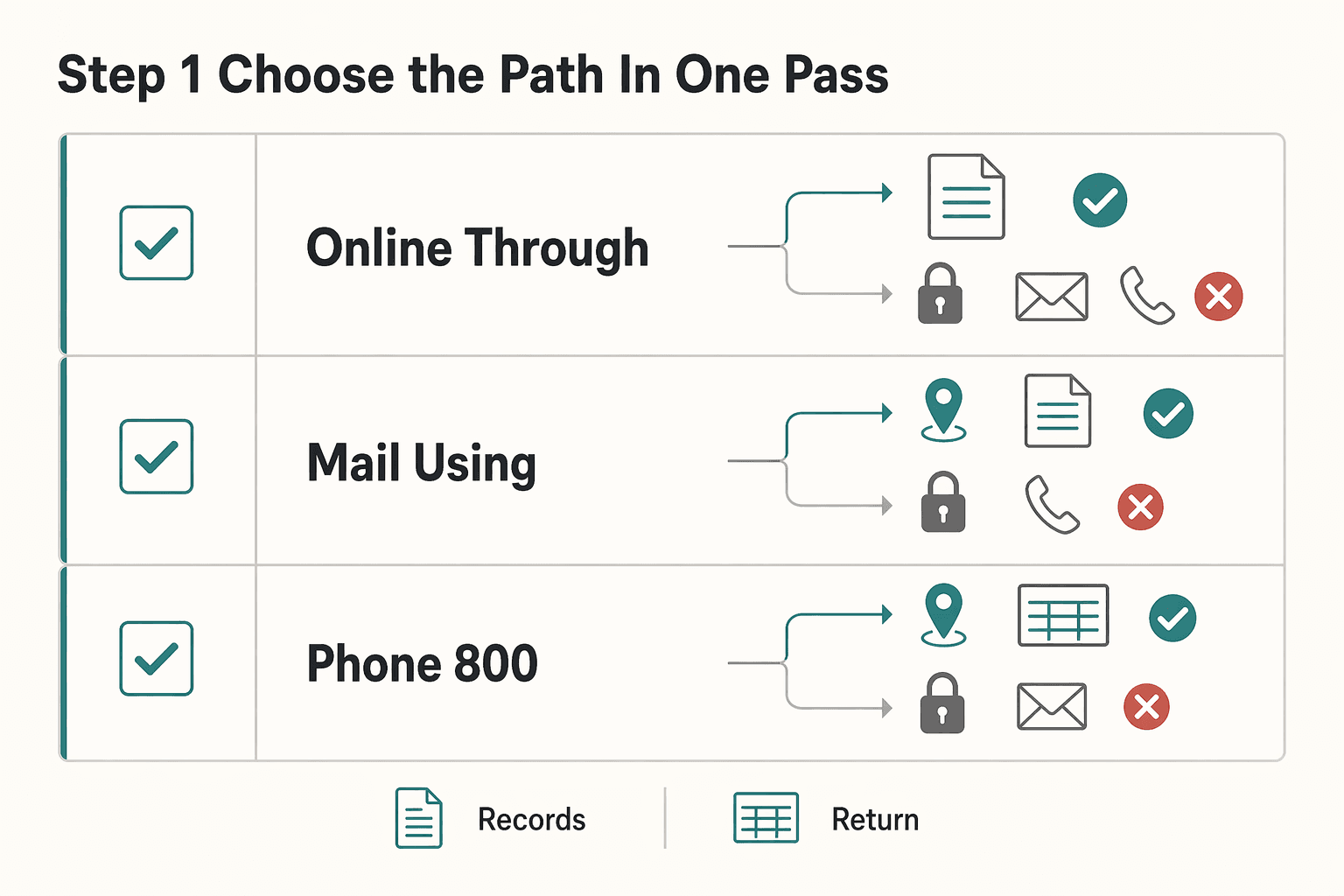

Step 1. Choose the path in one pass#

| Path | Choose this when | Timing signal (use as planning guidance) | Scope limit | Failure risk |

|---|---|---|---|---|

| Online through Individual Online Account | You need the transcript urgently and can complete ID.me verification | High confidence: fastest route if verification succeeds | Broadest online transcript access | Medium: ID verification can fail or stall |

| Mail using Form 4506-T | Online verification is blocked, or you need a transcript type outside mail or phone ordering | Medium confidence: processing plus mailing path | Can request tax return, tax account, wage and income, and record of account transcripts | Medium-High: incomplete or illegible forms, wrong routing, or address issues can reject or delay |

| Phone at 800-908-9946 | You only need a tax return or tax account transcript, and your IRS address of record is current and reachable | Medium confidence: mailed delivery path | Limited to tax return and tax account transcripts | High: same address constraints as mail, plus limited transcript scope |

If your IRS address of record is uncertain, treat mail and phone as blocked until you fix it.

Step 2. Run Path 1 first, with fallback ready#

Use online first because the IRS positions it as the fastest method. The main gating step is ID.me registration, so go in with a fallback plan instead of assuming the first pass will clear. Pre-check before you start:

| Checkpoint | Article detail |

|---|---|

| ID.me registration | You have what you need to complete ID.me registration. |

| Identity verification documents | Documents are ready for identity verification if automated selfie checks fail. |

| Video verification IDs | For video verification, two primary IDs, or one primary + one secondary. |

| Selfie fallback | If repeated selfie attempts fail, ID.me can route you to a short video call. |

| Transcript review | After sign-in, verify the transcript type and tax year before you download anything. |

| Wage and income volume | If you need a wage and income transcript and expect more than approximately 85 income documents, move to Form 4506-T instead of retrying online generation. |

Before you begin, make sure you can complete ID.me registration and have backup identity documents ready. For video verification, that means two primary IDs, or one primary + one secondary.

If repeated selfie attempts fail, ID.me can route you to a short video call. Treat that as a normal fallback, not an exception. After you sign in, verify the transcript type and tax year before you download anything.

If you need a wage and income transcript and expect more than approximately 85 income documents, move to Form 4506-T instead of retrying online generation.

Step 3. Use Path 2 when control and completeness matter more than speed#

Form 4506-T is usually the better path when online access will not clear or when you need transcript coverage that mail and phone do not provide. It is slower, but it can cover transcript types those channels do not.

| Step | Article detail |

|---|---|

| Confirm address strategy | The IRS mails transcript requests only to your address of record. Old-address forwarding is not available. |

| Stabilize delivery access | Make sure that address is monitored and reachable for you. |

| If the address is outdated | File Form 8822 first, then wait for address processing before submitting Form 4506-T. |

| Submit Form 4506-T | Submit Form 4506-T legibly and completely, and route it to the correct IRS mail or fax destination for where the return was filed, including the routing used for foreign-country filers. |

| Track and secure handling | Log submission details and securely handle received documents. |

If you use this path, lock down the address first, then submit a complete and legible Form 4506-T to the correct IRS mail or fax destination for where the return was filed, including the routing used for foreign-country filers. Log the submission details so you can track what was sent and when, and handle the received documents securely.

Use this path when online verification remains blocked and you need transcript coverage beyond mail or phone limits.

Step 4. Keep Path 3 as a last resort, with hard stop criteria#

Keep the automated phone service at 800-908-9946 as a backup. Use it only when both of these are true:

- You need only a tax return or tax account transcript

- Your address of record is current and accessible

Escalate instead of resubmitting if you hit identity mismatches, outdated address records, repeated non-delivery, or repeated ID.me failures. Contact IRS or ID.me support for transcript issues, and involve a tax professional when address history, identity mismatches, or recurring delivery failures keep blocking progress.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025. Before you send your transcript, align your residency timeline and supporting records in one place with the Tax Residency Tracker.

The Expat's "Failure Point" Playbook: Overcoming Common Hurdles#

When a transcript request stalls, fix the first broken control point instead of resubmitting the same request. In practice, the usual failure points are address matching, online registration friction, and weak delivery routing.

Step 1. Fix address matching before transcript requests#

If your address of record is uncertain, stop there first. IRS transcript mailing depends on that address, so a mismatch can block a successful mailed transcript request. Use this pre-request checklist:

| Check | Article detail |

|---|---|

| Latest filed return | Confirm the mailing address from your latest filed return. |

| Monitored and reliable | Decide whether that address is still monitored and reliable. |

| Form 8822 | If not, file Form 8822 to report your home mailing address change. |

| Match IRS records | Make sure your request details match IRS records before requesting the transcript. |

| Before signing Form 4506-T | Confirm all applicable lines are complete and legible, including current and prior address fields where required. |

| If the details do not align | Correct them before you submit. |

Check the mailing address from your latest filed return, decide whether it is still monitored and reliable, and file Form 8822 first if it is not. Before you sign Form 4506-T, make sure all applicable lines are complete and legible, including current and prior address fields where required, and confirm the details match IRS records cleanly.

Step 2. Switch to the fallback path if online registration keeps failing#

If online registration keeps failing, stop repeating the same attempt. Before you try again, make sure your entries match your latest filed return, especially your mailing address.

If online registration remains blocked, use the IRS mail alternative for a tax return or tax account transcript, then continue from there.

Step 3. Use Form 4506-T delegation when delivery reliability is the main risk#

If your delivery chain is weak, deadlines are tight, or IRS records repeatedly conflict with your entries, delegation through Form 4506-T can be a practical choice. Before naming a recipient, verify:

- You are using the active Form 4506-T revision.

- Recipient name and address are exact.

- Handling expectations are clear, including storage, forwarding, and transmission process.

Use delegation deliberately. Once a transcript is disclosed to a listed third party, IRS control over downstream handling is limited. Escalate to a tax professional when mismatches keep recurring, deadlines are urgent, or IRS record conflicts persist.

We covered this in detail in How to Amend a 941 Payroll Tax Return.

Conclusion: From Anxiety to Agency#

This process is manageable if you make three decisions in order: choose the right transcript, choose the request path you can actually complete, and confirm delivery before you submit.

Step 1. Choose the transcript that matches the request#

Use the institution's wording, not assumptions. A tax return transcript shows most line items from your original Form 1040-series return and usually meets mortgage documentation needs. If they need combined return and account data, request a record of account transcript. If they need proof that no return was processed, request a verification of non-filing letter. Current tax year verification of non-filing letters are not available until June 15.

Checkpoint: confirm whether they accept a transcript or require a full return copy. If they require a full copy of your return, use Form 4506. Return copies cost $30 per copy.

Step 2. Choose the fastest request path you can finish#

Start online when possible, since the IRS says that is the fastest method. If online access does not work, phone or mail can request tax return and tax account transcripts. Mailed transcripts are sent to the IRS address on file, typically within 5 to 10 calendar days. If you need another transcript type, use Form 4506-T. The form states that most requests are processed within 10 business days.

Failure mode to avoid: repeating requests with mismatched data. Verify all entered information first. If your address changed, file Form 8822 before Form 4506-T and allow four to six weeks for processing.

Step 3. Plan delivery before you request#

Set the delivery path up front. If the receiving institution needs file matching, include the Customer File Number when available. If they use an IRS IVES workflow, follow that authorization process instead of sending documents through a channel they do not accept.

Next-step checklist#

Before you submit, confirm you have:

- the exact transcript type the institution requested

- matching IRS record details and any required forms, such as Form 4506-T or Form 8822

- a chosen access path: online, phone, mail, or form request

- the recipient, file reference, and submission channel the institution will accept

If your case includes mismatched records, urgent deadlines, or institution-specific documentation rules, pause and work with a qualified tax professional. Related: Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?. If a bank or visa team asks for documentation beyond the transcript, contact Gruv to confirm the right compliance-first workflow for your market and program.

Frequently Asked Questions

How can you request an IRS transcript from abroad?

Start with IRS online access if speed matters, because that is the fastest path when you can complete identity verification. Use phone (800-908-9946) or transcript-by-mail when you only need a tax return transcript or tax account transcript sent to your address of record, and plan for about 5 to 10 calendar days for delivery. Use Form 4506-T if you need another transcript type, and verify the current IRS form instructions before you submit.

What is the fastest way to get IRS tax return transcript if you live abroad?

Try the online route first when time is tight. If identity verification keeps failing, switch to phone or mail for the transcript types those channels support. If you need a different transcript type, use Form 4506-T.

Can the IRS mail a transcript to a foreign address?

IRS materials describe transcript requests as mailed only to your address of record and warn that old-address forwarding will not work. If your IRS address is wrong, file Form 8822 first and allow about four to six weeks for processing before submitting Form 4506-T. If you need an exact return copy sent to a third party, use Form 4506.

How can you get a transcript without a US phone number or credit card?

Use the online method if you can complete its identity checks, but keep a fallback path ready. If online verification does not clear, request supported transcript types by phone or mail, or use Form 4506-T for other transcript types. If your IRS address is outdated or mismatched, file Form 8822 first and allow processing time before submitting Form 4506-T.

Which transcript is best for a foreign mortgage or visa application?

Match the document to what the institution specifically asks for. For income proof, a tax return transcript is often accepted and is generally available for the current and three prior tax years. For payment history, ask whether they want a tax account transcript or a record of account transcript. Use a wage and income transcript for W-2, 1099, 1098, or 5498 data, and use a verification of non-filing letter if they need proof that no return was processed. Current-year letters are not available until June 15.

Is a transcript the same as a copy of your tax return?

No. A transcript is a free IRS summary of key return or account data, while a return copy is an exact replica of your filed return and attachments requested on Form 4506. Request a transcript first unless the requester explicitly requires a full return copy. A return copy costs $30 per return and is generally available for 7 years.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.