Quick Answer

To fire your accountant or lawyer cleanly, protect continuity first, choose a successor before sending notice, and end the engagement in writing with a clear effective date, scope cutoff, and transfer instructions. Build a records inventory, track open work, confirm who owns each task until transfer, and save proof of notice, file delivery, access removal, and billing decisions in one paper trail.

Protect continuity before you send notice#

Ending an accountant relationship is mostly an execution problem. If you're working through this, the safest path is to protect continuity first, then close the engagement in writing with clear records.

Most avoidable damage starts when you terminate before mapping open work and record handoff. The cost usually shows up later, when open items and record requests were never clearly assigned. A better approach is a controlled sequence with checkpoints. Start with the engagement contract and termination clause, then track each handoff so the next professional can take over without gaps.

Treat the transition as a short project with one objective: no surprises after the effective date. You do not need complex templates. You need a current inventory and a written record of who is responsible for each open item until transfer is complete.

Before you start, gather:

- Signed engagement contract

- Current list of open obligations and active work in progress

- Records inventory for transfer

- Protect continuity first. Confirm what must stay on track, what is already in progress, and who owns each item until transfer.

- Document decisions as facts. Keep notices, acknowledgments, and scope decisions in one paper trail.

- Terminate in writing with boundaries. State the effective date, define what will be transferred, and clarify any in-progress work that will still be completed.

The sections below turn that sequence into practical decision rules so you can exit cleanly without creating new legal or transition risk.

Decide if this is a fixable issue or a replacement decision#

Make this call early. Try repair when risk is contained and trust is intact. Move to replacement when problems repeat or confidence in accuracy breaks down.

| Path | Use when | Key check |

|---|---|---|

| Replace | Missed deadlines keep repeating, risk grows, or non-responsiveness continues after explicit written feedback | Document what happened, when you reassessed, and why you exited |

| Repair first | The issue appears to be a one-off communication breakdown and there is no clear compliance risk | Set a reassessment date |

| Escalate quickly | Integrity concerns appear, including possible misrepresentation or conflicts of interest | Record dates, files, and business impact |

| Short performance window | You are unsure | At reassessment, check whether open items are closed, responses are timely, and ownership of work in progress is clear |

If you wait too long, you can end up half-repairing and half-transitioning at the same time. That is when deadlines get missed. Some communication failures are capacity-related rather than intentional neglect, but repeated breakdowns still raise risk. Choose a path, document it, and set a reassessment date if you are giving the relationship one more chance.

- Consider replacing when missed deadlines keep repeating, risk grows, or non-responsiveness continues after explicit written feedback.

- Repair first when the issue appears to be a one-off communication breakdown and there is no clear compliance risk.

- Escalate quickly when integrity concerns appear, including possible misrepresentation or conflicts of interest. Record dates, files, and business impact so the decision stays factual.

- If you are unsure, run a short written performance window with a reassessment date. On that date, check whether open items are closed, responses are timely, and ownership of work in progress is clear.

Use a simple evidence log during the decision period. For each issue, capture four fields: date, what happened, requested correction, and result. Keep entries factual and short. This helps you avoid vague language and gives your successor context without rewriting history.

A repair window needs a defined endpoint. Write the exact items that must improve, then check only those items at reassessment. If the same failure mode repeats, move to replacement and stop renegotiating expectations.

You do not need perfect certainty before you replace. You do need a factual record showing what happened, when you reassessed, and why you stayed or exited.

Build your transition packet before you notify anyone#

When possible, build the packet before any notice goes out. It makes the separation easier to run and document.

| Packet item | What to capture | Why it matters |

|---|---|---|

| Governing documents | Signed engagement contract, termination terms, communication instructions, transfer expectations, named service provider and recipient, and any timing or format details | So you do not have to re-read legal text each time |

| Records inventory | Filed returns, supporting tax records, current work in progress, owner, format, tax year, receipt status, delivery destination, and completeness check | Reduces rework |

| Notice and transfer drafts | Effective date, scope cutoff, in-progress work, and destination details | Keeps the final message controlled even if the call is tense |

| Paper-trail folder | Drafts, sent emails, confirmations, delivery proof, timestamps, a simple index, and the same final notice text across channels | Shows what was sent, to whom, and when |

-

Pull and mark the governing documents. Start with the signed engagement contract, if you have one. Note any termination terms, communication instructions, and transfer expectations in plain language so you do not have to re-read legal text each time. Capture who the contract names as the service provider and recipient, and copy any timing or format details into your transition notes so they do not get lost in email threads.

-

Create the records inventory before requesting files. List filed returns, supporting tax records, and current work in progress you need to transition. Track owner, format, tax year, and receipt status. Keep filed returns indefinitely, and keep supporting records through the general three-year IRS assessment window, noting that some situations can extend that period. Add two operational fields that reduce rework: where each item should be delivered and how completeness will be confirmed.

-

Draft notice and transfer language in advance. Prepare a written termination notice and a separate records transfer request before the conversation. Include effective date, scope cutoff, in-progress work, and destination details. Draft it now so your final message stays controlled even if the call is tense. Keep the notice focused on execution and dates, not debate about past performance.

-

Set up one paper-trail folder. Store drafts, sent emails, confirmations, and delivery proof with timestamps. Keep a simple index so you can show what was sent, to whom, and when. If you use multiple communication channels, store the exact same final notice text in the folder so there is no confusion about version control.

A prepared packet lowers friction because each request is specific. It also helps the current accountant execute transfer steps faster, and helps the successor start review with fewer clarification loops.

Before you send anything, do one dry run: read your notice, transfer request, and inventory in sequence. If a third party could identify the effective date, scope boundary, and file destination without asking follow-up questions, the packet is ready.

Select the successor before you terminate#

Pick the replacement before you send notice. That keeps continuity and transfer control with you instead of leaving them to timing luck.

-

Define scope before interviews. Share a one-page brief with entity type, recent returns, open items, and any foreign account or asset exposure. Ask whether the candidate can review historical returns and handle current filing obligations, including cross-border reporting if relevant. This is not a sales call. You need a clear yes or no on current obligations and intake timing.

-

Confirm cross-border reporting competence. For cross-border profiles, ask when Form 8938 may apply, how thresholds can shift by filing status or residency, and how they separate Form 8938 from FBAR. They should distinguish FBAR filing on FinCEN Form 114 when aggregate foreign account value exceeds $10,000 at any point in the year, and explain that Form 8938 does not replace FBAR when both apply. Ask them to explain this distinction in plain language, since clarity now reduces filing confusion later.

-

Test handoff execution. Share a redacted records inventory and request a first-week intake plan plus draft receiving instructions for your transfer request. Look for clear ownership, required formats, and a basic completeness check. A strong candidate should tell you exactly what they will review first, what they need to start, and how they will confirm that transfer files are usable.

-

Prioritize continuity if deadlines are close. When time is tight, choose the candidate who can start quickly, communicate clearly, and run a controlled handoff, even if the fee is higher. Red flags include vague answers, no written commitments, or confusion about FBAR timing, including the April 15 due date and automatic extension to October 15.

A practical screen is to ask each candidate for the same three deliverables: intake start date, first review priorities, and missing-file escalation method. Compare responses side by side. The candidate who gives you concrete next actions is usually safer than the one with broader claims and fewer details.

Before notifying the current CPA, confirm three items: named successor, confirmed start plan, and ready transfer instructions.

Review contract and jurisdiction limits before you act#

Let the contract drive the plan. Keep jurisdiction-specific points open until you verify them.

Re-read the termination clause and capture exact requirements#

Pull the exact notice form, timing requirements, wind-down limits, and any terms tied to records or working papers, if the contract specifies them. Save the clause text with your planned effective date so you and your successor can review the handoff plan quickly. If language is ambiguous, mark the ambiguity directly in your notes and route it for legal review before sending notice.

Choose notice delivery based on risk, not assumptions#

Use the contract as your baseline for notice delivery rather than assuming one method is always sufficient. If receipt or timing could be disputed, send the same notice through an additional trackable channel. Keep wording identical across channels so there is one effective date and one scope cutoff. Consistency matters more than format variety. Conflicting phrasing can create avoidable disputes later.

Separate confirmed obligations from open jurisdiction questions#

Document what the contract clearly requires, then list what still needs local confirmation. Process details can vary by jurisdiction and engagement type, so avoid importing rules from unrelated contexts. Professional-rule headings, such as co-operation with successor accountant or retention of documentation and working papers, do not replace contract-specific and local requirements. Mark open items as pending instead of guessing. A short pending list is safer than an incorrect assumption presented as fact.

Confirm the contracting party before sending notice#

If the accountant works at a firm, verify whether the agreement is with the individual, the firm entity, or both. Address notice to the contracting party and copy day-to-day contacts to reduce avoidable delays. When the wrong party receives notice, even a clear letter can still delay the handoff.

This review step protects timing. Once contract requirements, delivery path, and jurisdiction questions are separated and visible, you can move quickly.

Choose your timing and handoff mode#

Your timing should match risk and continuity needs. Treat this as practical process guidance, not a legal timing rule. If trust or record accuracy is in doubt, consider an immediate scope cutoff. If an abrupt change is more likely to drop active work, use a staged handoff.

Before you start#

Before sending notice, confirm three basics: a successor start plan, a written notice draft with a proposed effective date, and a live list of open items that could break if ownership changes midstream. Focus on pending filings and any records with known coding, duplicate, or balance issues.

- Classify risk first.

If accuracy concerns or repeated response delays exist, shorten the timeline and consider immediate cutoff. If continuity risk is higher because in-flight work could be dropped, use a staged transition. Record one sentence explaining the choice.

- Set one date and narrow scope in writing.

If filings are pending, set one effective date and limit work to already-scoped items. Keep wording consistent across notice and follow-ups so ownership is clear.

- Stage the handoff where tasks are already in motion.

For active workstreams, assign each open task to one owner through cutoff, then transfer control in a fixed order. Have the successor confirm file receipt and readability early in the takeover.

- Move to immediate cutoff if unresolved errors touch filing accuracy.

If unresolved errors affect filings, consider stopping scope immediately and shifting cleanup ownership to the successor. One reported engagement described mistakes, fines, and delayed responses in the same relationship; treat that as a warning signal, not a universal pattern.

Use this comparison to pick mode without overthinking:

| Situation | Better mode | Why |

|---|---|---|

| Accuracy concerns are unresolved | Immediate cutoff | Can limit additional exposure and clarify ownership quickly |

| Open tasks are complex but trust remains | Staged handoff | Can reduce drop risk for in-flight work |

| Deadline pressure is high and successor is ready | Immediate or short staged overlap | Keeps decisions tied to continuity needs |

| Scope is unclear across active tasks | Short staged handoff with item owners | Forces explicit ownership before cutoff |

This step is about execution discipline: one mode choice, one owner per task, one timeline.

Send a termination notice that closes scope clearly#

Your notice is the control document for ending services. It should define timing, scope boundary, and transfer instructions in one place.

Before you start#

Open the engagement contract, records inventory, and successor contact details. Draft one written notice that matches handoff mode and contract terms, including recipient and delivery method.

- Draft the notice as a disengagement letter.

State that the relationship is ending and give the effective date in plain language. Include any outstanding work, final responsibilities, fees due, and transfer or retention instructions.

- Set a clear scope boundary.

Add one explicit line clarifying what ends on the effective date and what, if anything, remains as outstanding work.

- Use a formal written delivery method.

Send the notice in writing and keep delivery details with your file. If dispute risk is higher, consider using an additional written channel to reduce ambiguity.

- Preserve proof and close the handoff loop.

Save final notice text, send timestamp, delivery records, and replies in one folder. Repeat transfer instructions clearly, including successor details, so next ownership is explicit.

Good notices are short, specific, and hard to misread. Vague timing language or unclear boundaries around new work can create scope disputes. You can reduce that risk by keeping one date, one scope cutoff, and one transfer path.

Before sending, do a clarity check: can someone outside the dispute answer four questions from the notice alone? What ends, when it ends, what still must be completed, and where files go next. If any answer is unclear, edit the notice before delivery.

Clear notice language helps reduce avoidable scope disputes.

Run records transfer with acceptance checks#

Treat transfer like controlled delivery with proof, not an open-ended request thread. The goal is simple: what arrived, what is missing, and what is usable.

Before you start#

Prepare transfer request language, inventory, and successor contact details. Keep a signed release permission ready to attach, since some accountants may ask for written authorization before releasing records.

- Send one formal request with a clear route.

Ask for direct transfer to the successor when possible, and include a fallback route if direct transfer is declined.

- Prioritize critical file groups in the first request.

List the highest-priority returns and related workpapers first so review can start on the most important records.

- Confirm delivery and run acceptance checks.

Request confirmation by file group, then have the successor mark each as received, missing, or unreadable.

- Close gaps quickly and keep timestamps.

If items are missing or unreadable, send a targeted follow-up with the exact list. Keep original request, confirmations, acceptance notes, and follow-ups in one thread.

One practical rule: do not mark transfer complete based only on a download notification. Treat transfer as complete after the successor verifies files open, match requested periods, and are usable for current work. This helps catch corrupted files or incomplete exports earlier.

If older files are unavailable, ask whether they may have been destroyed after a period of time and record that response. Keep the response in the same thread so future questions about missing history can be answered quickly.

Lock down systems and access on the same day#

Once records transfer is moving, lock access the same day when practical. Waiting leaves unnecessary exposure after handoff.

Accounting tools often hold concentrated financial and personal data. Access cleanup is not admin polish; it is a control step.

Before you start#

Use one checklist for accounting software, payroll records, billing accounts, and tax portals. Track current owner, replacement owner, and confirmation that prior access was removed.

- Rotate credentials and remove old permissions.

Update high-risk credentials and remove access no longer needed across accounting, payroll, and billing tools.

- Verify portal access and contact routing.

Where portals are used, review who still has access and route account contacts to the successor or current internal owner.

- Confirm revocation in writing with evidence.

Save proof for critical accounts, such as a screenshot, log entry, or admin confirmation, then send a short summary of what changed and when.

- Keep all proof in one paper trail.

Store checklist, confirmations, and evidence with the rest of the offboarding record.

Sequence matters here. Remove unnecessary access first, then verify successor access, then confirm account notifications and contact details. That order helps limit the chance that old access or outdated contacts remain in place longer than intended.

Because these systems hold highly sensitive client information, and one breach can expose many clients at once, close access windows as quickly as practical.

Close billing cleanly and resolve disputes fast#

Billing questions can slow cooperation during a transition. Close billing with clear documentation, and separate numbers and reporting questions from rights and risk questions.

- Request an itemized bill and map each charge to the engagement contract.

Ask for each task and fee line in writing. Mark each line as completed, unclear, or out of scope based on contract terms.

- Document prepaid work versus completed work and request written reconciliation.

List what was prepaid, what was completed, and the amount under review. If you think an adjustment may be needed, ask for clarification based on contract scope rather than assuming an automatic refund.

- Separate undisputed and disputed lines in writing.

Identify which line items you agree with and which you dispute, with brief reasons tied to contract terms. This keeps the discussion focused and easier to resolve.

- Escalate to the right professional when needed.

Use an accountant for numbers and reporting questions, and legal counsel for rights, obligations, and legal risk. Many issues have both money and risk dimensions, so you may need both in the right order.

When drafting dispute messages, keep the tone neutral and the requests precise. Ask for clarification by line item, not broad statements about overall fairness, and keep a dated written record of invoices, payments, and communications.

This is general information, not legal or tax advice.

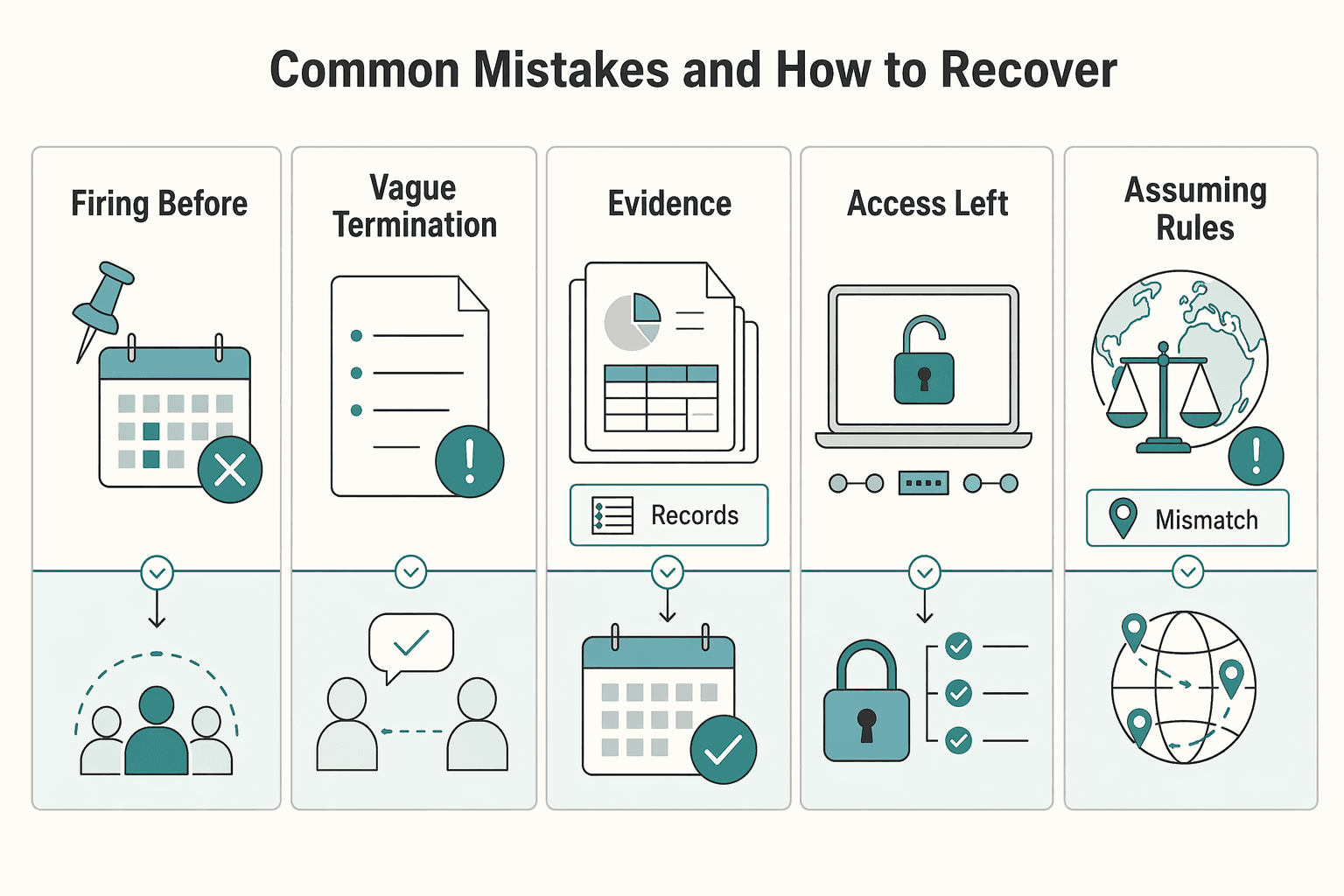

Common mistakes and how to recover#

When offboarding goes sideways, use a fast sequence: continuity, documentation, transfer completeness, access control, then jurisdiction checks.

| Mistake | Recovery | Verification checkpoint |

|---|---|---|

| Firing before hiring | Name the successor first, confirm intake capacity, re-issue transition dates, and send an updated transfer request with the new recipient | Successor confirms intake date, priority deadlines, and first review scope |

| Vague termination notice | Send a clear written notice with one effective date, explicit scope cutoff, and no-new-work language tied to the agreed engagement scope | Acknowledgment repeats the same date and scope |

| Incomplete records transfer | Send a second request that lists missing items by file, period, and preferred format, and require item-level confirmation and readability checks | Successor marks each item as received, missing, or unreadable |

| Access left open | Rotate credentials, remove permissions, reassign account ownership, and update notifications across accounting, payroll, and billing tools | Each critical account has dated evidence of access removal and owner reassignment |

| Assuming rules are identical everywhere | Confirm local tax and legal requirements before sign-off, and route reporting versus legal-risk questions to the right professional | Maintain a dated list of deadlines, open risks, and clear owners |

- Mistake: firing before hiring.

Recover by naming your successor first, confirming intake capacity, and re-issuing transition dates. Send an updated transfer request with the new recipient. Verification checkpoint: successor confirms intake date, priority deadlines, and first review scope.

- Mistake: vague termination notice.

Recover by sending a clear written notice with one effective date, explicit scope cutoff, and no-new-work language tied to the agreed engagement scope. A termination email may work in some cases, but do not assume it will resolve every case. Verification checkpoint: acknowledgment repeats the same date and scope.

- Mistake: incomplete records transfer.

Recover with a second request that lists missing items by file, period, and preferred format. Require item-level confirmation and readability checks. Verification checkpoint: successor marks each item as received, missing, or unreadable.

- Mistake: access left open.

Recover immediately by rotating credentials, removing permissions, reassigning account ownership, and updating notifications across accounting, payroll, and billing tools. Verification checkpoint: each critical account has dated evidence of access removal and owner reassignment.

- Mistake: assuming rules are identical everywhere.

Recover by confirming local tax and legal requirements before sign-off, and route reporting versus legal-risk questions to the right professional. Even serious disputes can fail if deadlines are missed. Verification checkpoint: maintain a dated list of deadlines, open risks, and clear owners.

When recovery starts late, prioritize by exposure. One practical order is to secure active deadlines and account access first, then close missing records and billing disputes, then finalize local requirement checks.

A common preventable miss is failing to assign a single internal owner for the transition. Even in a small company, one point person can own updates, follow-ups, and final sign-off so proof does not stay scattered.

Conclusion and copy paste checklist#

Clean closure is not one message. It is a tracked closeout with documented decisions, completed steps, and a clear paper trail.

If your accountant transition overlaps with business closure, the most expensive miss is closure drift. If a business is not legally closed with the state, annual taxes and fees may continue. Confirm local closure requirements early and keep those actions in the same paper trail.

If that applies, use this copy paste checklist to keep execution tight:

- Get qualified legal and accounting advice before finalizing dissolution decisions.

- Print and use the state closure checklist (for Rhode Island, the "Close Your Rhode Island Business" checklist) to track progress.

- Follow your governing documents when approving closure actions.

- Document all decisions including meeting minutes and how remaining assets will be distributed.

- If you are terminating a Rhode Island employer account, submit TX-13 to initiate the process.

- After initiation, submit all outstanding employer tax forms required for Rhode Island employer-account termination.

- In Rhode Island, file the final Quarterly Tax & Wage Report within 10 days of ceasing operations.

- In Rhode Island, ensure final paychecks are issued within 24 hours of an employee's last day.

- If WARN applies, provide 60 days advance notice for qualifying plant closings or mass layoffs.

- Archive the full paper trail with corporate records including decisions, filings, and closure notes.

If this transition overlaps with Rhode Island business closure, include those state steps in final sign-off and retain the records with corporate records.

Final reminder: once the checklist is complete, run one short internal review to confirm no open deadlines remain.

Frequently Asked Questions

Should I hire a new accountant before firing the current one?

If possible, yes. Hiring the successor first protects continuity, lets records transfer directly, and gives open items an owner immediately after cutoff. If the problem looks one-off, a short repair attempt can still be reasonable before you switch.

Do I need to give a reason in a written termination notice?

Not necessarily. One reported case accepted a termination-of-services email without rebuttal, but that is not a universal rule. Keep the notice short, factual, and well documented.

Should I use email only or send a certified letter?

Email can be enough in some lower-friction cases, but it is not universal. If receipt or dispute risk is higher, use email plus a trackable delivery channel. Keep the wording identical across channels.

What records should I request before ending the relationship?

Request the work products tied to the engagement, plus the status of what is already on file and what is still pending transfer. Use item-level confirmation so missing files surface early. Keep one consistent inventory to make follow-up faster.

What should I do with accounting software access and passwords?

Document what access exists and who will own it after the transition. Do not treat the handoff as complete until old access is removed and new ownership is verified. Keep proof with the rest of the offboarding record.

Do I still owe fees after termination, and when can I request a prorated refund?

Whether fees or refunds apply depends on the contract terms. If prepaid work was not delivered, you can request a prorated refund in writing, but it is not guaranteed. Keep billing disputes separate from tax obligations so filing responsibilities stay on track.

How is offboarding a lawyer different from offboarding a CPA in practice?

Do not assume offboarding a lawyer follows the same process as offboarding a CPA. This guide does not establish one definitive legal framework for both. If both are involved, split responsibilities early so reporting questions and legal-risk questions go to the right professional.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- csrc.nist.gov/CSRC/media/Projects/risk-management/800-53%2...trusted

- federalregister.gov/documents/2024/07/09/2024-14609/termination-...trusted

- irs.gov/forms-pubs/about-form-2848trusted

- irs.gov/instructions/i2848trusted

- uscourts.gov/forms-rules/forms/substitution-attorneytrusted

- aicpa-cima.com/resources/download/client-termination-practi...external

- americanbar.org/groups/professional_responsibility/publicati...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: