Quick Answer

Finance your first rental by choosing the loan that your cash flow can survive, not the largest amount a lender will approve. Build a lender-ready file, compare options by total cost, speed, reserve requirements, and downside if income or rent dips, and do not proceed unless cash after closing can cover your personal and property obligations for six months.

Finance your first rental without breaking your core cashflow#

Start by protecting your day-to-day cashflow, then treat loan approval as a constraint. If client payments are uneven, a payment that feels manageable in a strong month can create real pressure in a weak one.

You are not just choosing a mortgage. You are deciding how much fixed pressure to add when you take on a first rental property.

Keep two filters in view from the start:

- Risk capacity: how much loss or payment friction you can absorb financially without harming your lifestyle or core goals.

- Risk tolerance: how well you can handle volatility or potential loss psychologically.

Step 1. Anchor the decision on monthly survivability#

Start with monthly survivability, not the largest amount a lender may approve. Traditional mortgage underwriting often centers on personal income, not property performance. One common failure mode is personal DTI blocking a deal even when the property appears able to cover the mortgage.

You can also evaluate a DSCR loan, which looks at whether the property can cover the mortgage rather than relying mainly on paycheck-style qualification. Treat it as one path to evaluate, not an automatic answer, because DSCR financing has tradeoffs too.

Step 2. Build your lender file early#

Build your lender file early. A typical documentation checkpoint includes tax returns, W-2s, paystubs, and debt-to-income calculations. If you cannot explain your income profile and debt load clearly in one pass, tighten your file before you compare financing paths.

Step 3. Set a contingency mindset before you shop#

Set the contingency mindset before you shop. One beginner-oriented guide recommends building a contingency plan first. That can include saving for a year, starting a side business, or maintaining stable employment. The point is simple: avoid financing choices that strain your core cash buffer when income dips.

This guide gives you:

- a lender-ready document pack

- financing decision rules for approval friction, monthly payment pressure, and downside if revenue drops

- checkpoints to reduce financing surprises

If one rule carries through the whole process, use this: if a financing path weakens your core cash buffer too much, pause, even if a lender says yes. Approval helps. Liquidity protects the rest of your business.

For a step-by-step walkthrough, see How to Run Airbnb Rental Arbitrage as a Compliance-First Business.

Set your buy box and risk limits before lender outreach#

Set your constraints before you contact lenders. Otherwise, the process can drift toward approval size instead of deal fit.

Step 1. Choose one target property lane first#

Choose one target property lane first, then evaluate financing inside that lane. If you keep switching deal profiles too early, your comparisons get less reliable. Pricing, terms, and execution can vary across deals and lenders.

Use a short purchase brief to keep decisions stable: target type, target area, max price, and the cash you want to keep after closing. If those inputs keep changing, pause lender outreach until they are clear.

Step 2. Set your max price from your operating plan#

Set your max purchase price from your plan and underwriting, not lender capacity. Stress-test the assumptions so the deal does not depend on optimistic outcomes.

Before you discuss products, pick the priority for this purchase: cost, speed, or flexibility. That choice defines fit. A lower-cost option can still be the wrong choice if your deal needs a 10 to 21 day close. A full 30 to 60 day timeline may not fit the property or seller.

When you compare options, compare total cost of capital, not rate alone: rate, points, fees, required reserves, and prepayment-penalty risk.

Step 3. Put a cash-protection rule in place#

Put a cash-protection rule in place now. If your post-close cushion looks too thin for personal obligations and the first 90 days of operating surprises, pause the purchase, even if a lender approves it. Approval and fit are not the same.

A common failure mode is financing that does not match the operating plan. Slower, cheaper capital can miss competitive timing. Faster capital can increase downside through points, interest, and short timelines if execution slips.

For the full breakdown, read How to Screen Tenants for a Rental Property.

Build a lender-ready document pack before pre-approval#

Make the first review easy to verify. Submit a clean pack that shows identity, income, assets, debts, and liquidity in one place before you apply.

Step 1. Gather and label the core file set#

Start with the core preapproval documents lenders commonly request: tax returns, proof of income, and bank statements.

| Document | Timeframe | Article detail |

|---|---|---|

| Tax returns | Past two years | Listed as a core preapproval document |

| Proof of income, such as pay stubs | At least the past 30 days | When applicable |

| Bank statements | Past two to three months | Listed as a core preapproval document |

Lenders use these documents to confirm your identity, credit, and overall financial position. They also use them to decide how large a loan they may offer. Keep files organized and clearly named so the process can move more smoothly.

Step 2. Add a short freelancer stability note#

If your income varies month to month, explain the pattern up front. Self-employed borrowers usually need more documentation, often including two years of business tax returns, a year-to-date profit and loss statement, and 60 days of business bank statements.

Keep this note brief and tie every point to documents in your application. Explain how you earn, where variability comes from, and which period best reflects consistency. The goal is to help the lender review your file with less back-and-forth.

Step 3. Pre-answer liquidity questions with a summary#

Add a one-page liquidity summary so the lender can quickly trace available funds. List each account, ownership type, current balance, and the statement that supports it.

Separate personal and business funds clearly, and label which accounts are intended for down payment and closing. Before submission, make sure summary balances match the statements in your pack exactly. A traceable summary can help preapproval move more smoothly than extra narrative about future income.

Compare financing options by cashflow risk, speed, and flexibility#

Choose the loan structure that still works if rent or income dips, not the one that only looks cheapest on paper.

Step 1. Pick the decision lens before you compare rates#

Set one primary objective first: lowest total cost, fastest close, or most flexible underwriting. Deals often underperform because financing and execution plans are mismatched.

Compare cost of capital, not rate alone. Look at rate, points, fees, reserve expectations, and prepayment risk. As of February 2026, one broad benchmark cited a 30-year fixed average of 6.01%. Rental pricing was often about 0.50% to 1.50% above owner-occupied loans.

Step 2. Compare options on friction, speed, payment pressure, and downside#

| Option | Approval friction | Time to close | Monthly payment pressure | Downside if revenue dips | Walk away when |

|---|---|---|---|---|---|

| Conventional loan | Can be documentation-heavy, and pricing can shift with LLPA-style risk adjustments. | Can run more like a 30 to 60 day process than a sprint. | Usually lower than short-term debt, but rental pricing is typically above owner-occupied. | Vacancy plus income volatility can tighten cash quickly if reserves are thin. | Your approval depends on optimistic income assumptions, or the property condition is likely to create underwriting delays. |

| FHA loan | Fit depends on owner-occupancy in one unit of a 2, 3, or 4 unit property. | Typically a full mortgage timeline, not a speed option. | Payment fit still depends on the live-in rental plan being real. | Misaligned if you want a non-owner-occupied rental from day one. | You do not plan to live in one unit. |

| VA-related multifamily path (if available) | Availability and terms are lender- and borrower-specific, so confirm details early in writing. | Varies by lender and file. | Varies by terms and structure. | Main risk is losing time on assumptions that never clear lender review. | Availability, eligibility, or occupancy expectations are still unclear. |

| Portfolio lender | Rules are lender-specific, so confirm how your file will be underwritten. | Timeline is lender-specific; get a written estimate. | Total cost can differ from agency-style execution. | Carrying cost can reduce margin for error if flexibility comes with higher pricing. | The extra cost leaves post-close reserves too thin. |

| Hard money loan | Often used as a speed option, but terms can be punishing if execution slips. | Can land on the faster end in some deals, closer to 10 to 21 days. | High pressure from points, interest, and short timelines. | Delays in rehab, lease-up, or refinance can create fast cash strain. | Your plan needs stable long-term cashflow immediately. |

| Private money loan | Specialized option with terms that vary widely. | Varies by lender or investor. | Cost profile can shift meaningfully based on fees and repayment terms. | Risk includes both payment pressure and unclear exit timing. | Terms are not fully written, or repayment path is vague. |

Step 3. Make explicit rule calls before you commit#

If you are weighing a portfolio lender against an agency-style path tied to Fannie Mae or Freddie Mac, treat it as a flexibility-versus-cost tradeoff and confirm timeline, reserves, and total cost in writing.

If you are considering hard or private money for speed, pressure-test the exit plan first. Fast closings help only when refinance timing, rent assumptions, and rehab scope are realistic.

Before you choose, get four items in writing from each lender:

- expected timeline

- reserve requirement

- whether qualification leans on personal income or a DSCR-style property test

- full cost of capital

In one market-specific example, lenders often looked for 3-6 months of PITI reserves and viewed 1.0-1.2+ DSCR as a stronger signal. Treat those as context, not universal thresholds.

Final checkpoint: confirm the property is financeable in current condition, including working mechanics, intact roof, functioning windows and doors, and no major safety hazards. If that screen fails, timeline risk rises and a "cheap" loan can become expensive.

Related reading: A Guide to Schedule E (Supplemental Income and Loss) for Foreign Rental Property.

Calculate true cash to close and survive the first six months#

If post-close cash is too thin, do not proceed. The real decision is not just whether you can close, but whether you can carry the property and your core obligations for the first six months if income timing goes wrong.

Step 1. Separate cash into four non-interchangeable buckets#

| Bucket | What it covers | Practical rule |

|---|---|---|

| Down payment | Equity you bring to close, with many rental loans often planned at 15-25% down | Treat this as purchase capital only. |

| Closing costs | Transaction costs due at closing | Use updated lender estimates, not guesses. |

| Reserves | Backup cash after closing, with 6 months of payments used as a target in the cited rental-loan guidance | This must still be intact after close. |

| Early repairs | Immediate make-ready and first-month fixes | Fund this up front, not from hoped-for rent. |

Do not blur these buckets. Using reserves to patch a closing gap can make early vacancy or delayed income much harder to absorb.

Step 2. Run two funding paths before you choose#

Model the same deal in two versions:

| Item | Standard financing path | HELOC/home equity path |

|---|---|---|

| Cash used at close | Down payment + closing costs + early repairs | Lower cash at close if part is borrowed against home equity |

| Post-close reserve test | Keep your reserve target available after close | Keep your reserve target available after close, including any added home-equity payment |

| Payment pressure | Rental-loan payment only | Rental-loan payment plus home-equity debt payment |

This comparison is about survivability, not just getting to closing day.

Step 3. Stress-test the numbers like a freelancer#

Run at least three monthly scenarios before you commit: a normal month, a delayed-invoice month, and a vacancy month. For conservative math, do not assume full rent immediately. In the cited guidance, lenders may count only 75% of expected rent in underwriting, and your own pressure test should be at least that strict.

If your plan only works when rent starts on time and client payments land on schedule, the deal is too tight.

Step 4. Use one hard go/no-go rule#

Proceed only if, after closing, accessible cash still covers your core personal obligations and property obligations for six months. If that threshold fails, pause the purchase and rework the structure before you commit.

Related: The Ultimate Guide to Getting a Mortgage as a Freelancer.

Before you lock your reserve threshold, tighten the cash-in side with a repeatable invoicing workflow using Gruv's Free Invoice Generator.

Run pre-approval as a negotiation process, not a yes/no event#

Treat pre-approval as a way to improve terms and reduce offer-stage risk, not as a one-time yes/no checkpoint. Get competing written options before you shop seriously so you can compare assumptions, not just headline rates.

Step 1. Define the approval you actually want#

Pick your priority before lender calls: lowest cost, fastest close, or more flexibility. Then ask for true pre-approval, not pre-qualification, and keep the letter aligned to your real monthly budget and target price range. If your letter shows a much higher amount than you plan to offer, that can weaken your negotiating position.

Step 2. Compare written assumptions, not just payment quotes#

Collect written quotes across lender options. Ask each lender to spell out the assumptions behind the approval in plain language, then compare the same scenario side by side.

| Written item | What to compare |

|---|---|

| Loan or product path | Compare the same scenario side by side |

| Down payment and reserve expectations | Check how much cash each lender expects |

| Quoted rate and whether rental pricing includes a premium | Note whether rental pricing includes a premium, often cited around 0.50% to 1.50% versus owner-occupied loans |

| How your financial profile is treated in the approval assumptions | Compare the assumptions in plain language |

| Conditions still outstanding before final approval is realistic | See what still must clear before final approval is realistic |

At minimum, get those items in writing from each lender.

Step 3. Re-trade weak terms before active offer writing#

Negotiate before you hand a letter to your agent and start writing offers. If pricing is strong but conditions are heavy, ask what specific documents would clear them. If one lender is more flexible but more expensive, use that comparison to push other lenders on structure and pricing.

Step 4. Track conditions and timing as live risks#

Pre-approval helps, but it does not guarantee final underwriting or closing. Track each lender's letter amount, issue timing, any listed validity window, outstanding conditions, and missing documents. Review those weekly while you search. Some lenders can respond quickly, sometimes same day, but do not build your offer strategy on emergency turnaround.

You might also find this useful: How to Invest in Real Estate as a Digital Nomad.

Underwrite each deal with financing attached before you offer#

Treat financing as part of the deal, not a separate step after the offer. Before you bid, tie each property to the loan path you expect to use, the cash needed at close, and the reserves you will still have after closing and early repairs.

Step 1. Build one deal sheet and use it on every property#

Use one standardized sheet so you can see whether the deal still works after real financing costs and reserve impact are included.

Track, at minimum:

- purchase price and estimated cash to close

- rent assumption and your backup comp notes

- loan type, quoted rate, lender fees, points, and expected time to close

- monthly principal, interest, taxes, insurance, and known association dues

- repair or turn-cost estimate

- post-close reserves left in your accounts

Your checkpoint is simple: after filling out the sheet, you should know both the projected payment and the reserve cash left.

Step 2. Run the same sheet for a single-family rental and a multi-family property#

If you are comparing property types, keep the method identical so you avoid apples-to-oranges decisions. Use the same rent-source approach, closing-cost treatment, reserve logic, and financing assumptions unless the lender has already confirmed property-specific differences.

Standardization makes the right comparison clearer: total cash in, monthly obligation, and remaining cushion after close.

Step 3. Reject deals that only work in the best case#

Set a go/no-go rule before you get attached: if the deal only works at best-case rent, zero repairs, and a frictionless closing, pass.

Financing mismatch is a common failure mode. A lower-cost option can still be the wrong fit if the timeline is too slow for the deal. Faster financing can close in about 10 to 21 days, but it can also increase downside through points, fees, and short timelines versus a 30 to 60 day process.

Stress-test with a defendable rent assumption, a real repair line, and realistic reserves. If the numbers break, move on.

Step 4. Reconfirm the loan after the property is identified#

Pre-approval is not final underwriting. Once you have a target property, send the listing plus your deal sheet to the lender and confirm what changes after property-specific review.

Get written confirmation on pricing, fees, reserve expectations, time to close, and whether loan-level price adjustments apply based on file risk factors. If your debt-to-income ratio is already tight, even small changes can make the deal fragile.

Do not assume original terms hold because a pre-approval letter exists. Treat vague lender answers as live risk before you offer.

Use home equity or private money only in narrow scenarios#

Use home equity, private money, or hard money only when they solve a specific timing problem and your exit path is clear. If financing and the operating plan are not aligned, the deal can fail even when the property looks good on paper.

Step 1. Pick the real reason you need faster money#

Before using nontraditional funding, choose the one outcome that matters most for this purchase: lowest long-term cost, fastest close, or maximum flexibility. The same property can carry different costs across borrowers once pricing adjustments, fees, reserves, and close speed are factored in.

If the deal is not truly speed-constrained, treat that as a stop sign. A slower conventional loan can still be the better fit when speed is not the binding constraint, even at 30 to 60 days instead of 10 to 21 days. Your checkpoint is simple: state in one sentence why speed is worth the cost-of-capital tradeoff for this property.

Step 2. Use home equity only if your household can absorb the downside#

If you consider a home equity loan or HELOC, use it only when the deal still works after full cost of capital, not just the headline rate.

Underwrite points, fees, reserve impact, and prepayment-penalty risk in the full structure. Then verify post-close liquidity: after purchase, early repairs, and at least one delay scenario, you can still carry costs without relying on a perfect lease-up.

Step 3. Put private money terms in writing before you proceed#

A private money loan is workable only when terms are clear and the repayment path is realistic. Keep relationship boundaries explicit from day one.

At minimum, document:

- amount funded and funding timing

- payment structure and payoff triggers

- what happens if refinance is delayed

- any extension path, if applicable

Use the same deal sheet with the private lender that you use for your own underwriting. If the plan is too weak to show clearly, do not use this route.

Step 4. Treat hard money as short-horizon capital#

A hard money loan can solve speed, but it raises execution pressure through points, fees, and short timelines. Risk increases quickly if rehab or lease-up takes longer than planned.

It is most defensible when a near-term payoff or replacement path is already defined. Stress-test takeout assumptions: as of February 2026, the benchmark 30-year fixed was 6.01%, and rental loans may add 0.50% to 1.50%, which can change exit economics. If payoff depends on perfect timing or refinancing certainty, do not proceed.

This pairs well with our guide on How to Calculate Depreciation on a Foreign Rental Property.

Fix common underwriting breakdowns before they kill your timeline#

Once you choose a funding path, timeline risk can come from file friction, not just rate. Treat shifting conditions or conflicting documents as an execution problem and resolve it early.

Step 1. Reconcile your core documents before underwriting asks twice#

If your loan path uses income documentation, align your tax returns, bank statements, and proof of income before submission. Names, account activity, deposits, and income explanations should tell the same story, because inconsistency can be treated as risk in income verification.

Use one checkpoint: the file should read cleanly without obvious contradictions. If income is variable, add a short explanation so major deposits or swings are not read as inconsistencies.

Step 2. Pin down the blocker when conditions keep shifting#

When conditions keep changing, ask your mortgage lender for an updated list of open conditions and the single blocking item in writing. This helps separate a documentation issue from a loan-product mismatch.

If the blocker is valuation support, tighten your comps before the next review. Use at least two strong comparable sales from the past 6 to 12 months instead of relying on one older comp.

Step 3. Open a second lender track before the file is officially dead#

If the file is stalling, consider opening a backup lender track before a formal denial. A second path can protect your timeline if the original file cannot move.

One fallback to evaluate is a DSCR program, where approval can be based on property cash flow rather than personal income documents. If you pivot, confirm the required file early, typically appraisal, lease, and rent schedule, and order the appraisal immediately when it is the pacing item.

Manage the offer-to-close sequence to avoid cashflow shocks#

Cashflow risk during closing is often execution risk: who is doing what, by when, and what can still move your cash to close. As soon as an offer is accepted, run one dated checklist shared by your real estate agent and mortgage lender. Treat every money-moving item as live until funding is done.

Step 1. Build one dated checklist with clear owners#

Keep contract and loan tracking in one place, not in separate threads. Use a simple format: item, owner, current status, next update date, and impact if delayed.

California escrow guidance supports this operating style: communicate regularly with your lender and treat documents as time-sensitive. Use that discipline in your own process, even though closing mechanics can vary by state.

Step 2. Verify milestones that can still change cash to close#

Do not rely on "you're basically done." Use checkpoints you can confirm:

- request an estimated closing statement early, then update it as numbers firm up

- review the preliminary title report before closing

This keeps late surprises visible while you still have room to respond.

Step 3. Match financing structure to the real timeline#

If your timeline is closer to a 10 to 21 day sprint, confirm your financing can actually close that fast. If it is more like a 30 to 60 day process, align expectations early instead of forcing a sprint late.

Choosing financing that does not fit the deal plan is a common way solid deals underperform. Fast-close debt can solve timing, but it can also raise cost-of-capital risk through points, interest, and tighter execution pressure if the close slips.

Step 4. Ring-fence close funds from operating cash#

Consider keeping closing money separate from day-to-day business cash once you have a working estimate. This is a practical guardrail, not a legal requirement.

A simple check: if client payments arrive late this week, your close funds should still be intact. If not, your purchase timeline may be tied to receivables volatility instead of the transaction plan.

Keep your client payment system stable while you add rental debt#

If your incoming cash is hard to forecast, consider waiting before you add fixed property payments. Keep business cash predictable first, because an investment property mortgage is still due even when client payments slip.

Step 1. Separate operating cash from property cash#

Run business operations and property obligations from clearly separated cash buckets. This can reduce the risk of covering mortgage payments from guesswork and keep records easier to review if you later refinance or add debt.

Use a simple monthly check: cash-in records, cash-out records, and a clear log of mortgage, repair, and reserve transfers should be easy to reconcile.

Step 2. Make collections predictable before payments start#

Set invoice terms, follow-up timing, and payout tracking so expected cash has dates, not assumptions. The same operating logic shows up in rental management: deliberate collection systems and late-payment protocols can be a practical control for income stability.

Review this weekly: invoices due, cash received, payouts scheduled, and property payments due in the next 30 days. If that view stays fuzzy across multiple cycles, pause expansion.

Step 3. Stress-test refinance assumptions before relying on them#

If your plan depends on refinancing, treat timing and proceeds as uncertain until validated. One guide notes 6-12 month seasoning before refinance and typical investment-property leverage around 75-80% LTV, which can limit how quickly cash comes back out.

Build the plan so it still works if costs rise or timing slips. Repair surprises, refinance friction, market shifts, and reported renovation overruns around 15-20% can all tighten cashflow. If you want a deeper dive, read Should Your Freelance Business Accept Credit Cards?.

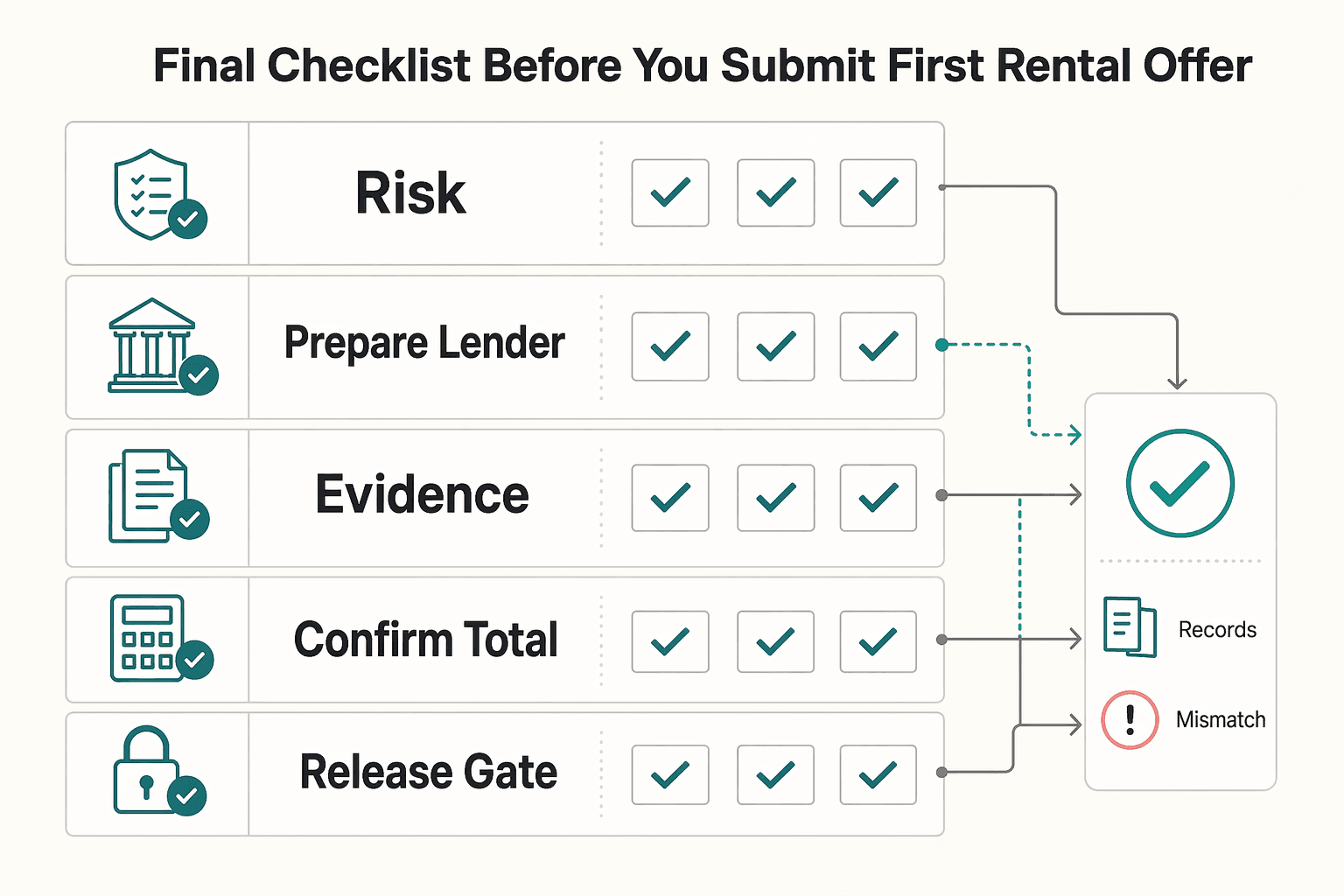

Final checklist before you submit your first rental offer#

Use this as your go/no-go gate. Submit only when every line is a clear yes.

- Define your buy box and max risk limit.

Choose one lane for this offer cycle and write down your max purchase price plus the minimum cash you will keep after closing. Keep your down-payment assumptions realistic: one lender source cites 15% to 20% for many first-time investors, while a multi-family purchase where you live in one unit may be possible at 3.5%.

- Prepare your lender file and reconcile gaps early.

Organize the documents your lender asks for before you are under contract. Then check for inconsistencies or missing items while you still have time to fix them. Overlooking a critical detail can create real downside, including financial loss or closing delays.

- Compare financing paths and document fit.

Do not default to the first path that looks available. For each option, write one line on monthly payment pressure, total cash used, and post-close liquidity. Keep one tradeoff visible: all-cash can reduce mortgage interest and PMI, but it can also leave you with less liquidity if a problem appears.

- Confirm total cash-to-close plus reserves under stress.

Model full cash required, not just down payment. One lender's reference range is $37,500 to $60,000 including down payment, closing costs, and reserves. Treat that as a checkpoint, not a universal rule. Run a stress case with an income dip, rent delay, or early repair and make sure the plan still holds.

- Validate pre-approval assumptions and timing with your mortgage lender.

Pre-approval can speed execution, but it does not guarantee final approval, final pricing, or an on-time close. Ask the lender to confirm the assumptions behind the letter, including property type, occupancy plan, and price range. If you are using 620 as a reference point, verify your lender's actual threshold.

- Run the deal sheet and apply your written go/no-go rule.

Plug in the real property numbers: price, financing terms, expected rent, taxes, insurance, maintenance, and vacancy allowance. Then apply one rule you will follow without exceptions. If the deal only works under best-case assumptions, do not submit the offer.

We covered this in detail in How to Calculate Cap Rate for a Rental Property.

For a separate freelancer payments workflow, explore Merchant of Record for Freelancers.

Frequently Asked Questions

How much down payment should I expect for a first rental property?

A practical starting range is 15% to 20% down for many first-time rental buyers. A multi-family purchase where you live in one unit may be possible at 3.5% down. Budget beyond the down payment alone because total cash also includes closing costs and reserves.

What do lenders actually review first for first-time rental financing?

This material does not support a single fixed review order. It highlights proof of income from steady employment and also points to upfront cash needs such as down payment, closing costs, and reserves. One lender source also uses 620 as a minimum credit-score reference point.

Which loan type is usually best for a beginner investor with variable income?

This material does not name one universally best loan type. Choose the option that still works when cash flow tightens, not just in a strong month. Check whether projected rent can cover the mortgage, vacancies, insurance, property taxes, and maintenance while keeping the result closer to positive cash flow than negative cash flow.

Can I use a HELOC or home equity loan to buy my first rental?

Yes, a HELOC can be used for some or all of a purchase, subject to your available credit limit and other lender factors. The main check is whether the line is large enough for the deal and whether your household can absorb the added payment pressure. This material does not provide comparable detail for home equity loan terms, so treat those as lender-specific.

Should I choose a single-family rental or multi-family property for financing ease?

Do not assume one is always easier to finance. This material does not support a universal winner between single-family and multi-family. It does note that residential properties, including both, are generally more beginner-friendly than commercial property, and living in one unit of a multi-family can materially change your down payment math.

What should I finish before I start touring properties seriously?

Finish your qualification basics first. That means clear proof of income, a realistic cash-to-close plus reserves plan, and a preliminary cash-flow screen that includes mortgage, vacancies, insurance, property taxes, and maintenance. If those numbers do not hold up, pause and tighten the plan before touring heavily.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- clame.nyu.edu/Resources/E0A4E7/312653/The%20On%20Rental%20...trusted

- clemson.edu/business/academics/finance/documents/resume-...trusted

- cs.princeton.edu/courses/archive/spring18/cos226/assignments/...trusted

- dhcd.maryland.gov/HousingDevelopment/Documents/rhf/2023MRFP-Gu...trusted

- dhcd.maryland.gov/HousingDevelopment/Documents/QAP_MRFP/2026-M...trusted

- dre.ca.gov/files/pdf/escrow_info_consumers.pdftrusted

- files.consumerfinance.gov/f/documents/201411_cfpb_expert-report-crawsh...trusted

- home.treasury.gov/system/files/136/2024-National-Money-Launder...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Should Your Freelance Business Accept Credit Cards?

Offer card payments, but stay in control of how money reaches you. The goal is not a smoother checkout screen. It is predictable cash you can use to run the business.

Getting a Mortgage as a Freelancer Without Guesswork

Start by reconciling your income file before you compare rates. For a **mortgage for freelancers**, the first gate is simple: can an underwriter read your documents cold and see one consistent income story?

How to Invest in Real Estate as a Digital Nomad

**Run anything with money and moving parts like an operations system (cash, docs, delegation, and controls), not a "passive income" vibe.** Real life stress-tests weak spots. You change time zones, a client pays late, and something breaks at the worst moment. As the CEO of a business-of-one, your job is to build a setup that keeps working when you are not available on demand.