Quick Answer

Finance a sailboat by setting a hard monthly cashflow cap first, then comparing loans on APR, loan term, down payment, sales tax, and cash left after closing. The safest structure is the one that still works in weak revenue months, not the one with the lowest payment. Prepare a clean lender packet, stress-test scenarios, and avoid deals that depend on delayed receivables or card balances.

Finance a sailboat without breaking your business cashflow#

Treat the boat as a cashflow decision first. The right loan is the one your business can carry through slow client-payment periods, not the one with the fastest approval.

If you're figuring out how to finance a sailboat with uneven income, anchor every quote to three terms: APR (annual percentage rate), loan term, and down payment. APR is not the same as the interest rate because APR includes lender fees, and lenders must disclose APR before you are legally obligated. If a quote is unclear on APR, fees, or assumptions, treat it as incomplete.

Use this quick risk lens before you apply:

| Term | What it tells you | Cashflow risk to watch |

|---|---|---|

| APR | Total borrowing cost, including fees | A low payment can still be expensive once fees are included |

| Loan term | How long you repay | Longer terms can lower the monthly payment but extend interest exposure |

| Down payment | Cash paid upfront | A higher down payment reduces the financed balance but uses liquidity you may need after closing |

Keep affordability tied to operations, not just the monthly payment. A shorter term usually means a higher monthly payment and less of each payment going to interest. A longer term can ease monthly pressure but keep debt on your books longer.

For context, many boat loans run 4 to 20 years. Typical down payments are often 10% to 20%, and some offers may allow zero down. Those are structure options, not automatic wins. Zero down or a very long term can feel easier up front but leave you with less flexibility later.

Before you commit, run every quote through the same filter:

- Compare APR, not just the note rate.

- Confirm the term in months or years.

- Check the down payment and how much cash remains after closing.

- Include sales tax in your budget.

If the terms come back weak, pause and rework the deal instead of forcing the purchase. The rest of this guide walks through financing options, approval prep, decision checkpoints, and what to do when income is uneven or the terms are not workable.

For a related planning read, see How to Evaluate Multi-Currency Personal Finance Software for Tax Residency, FBAR, and Invoicing.

What to prepare before you talk to lenders#

Show up to lender conversations with one clean file and one realistic loan draft. That keeps the discussion on affordability and risk, not just the lowest monthly payment.

Step 1 Build a lender-ready prep file#

Before any Online Loan Application, pull together the numbers and context you want every lender to assess the same way: target boat price, planned down payment, and expected financing range.

| Prep item | What to include | Why it matters |

|---|---|---|

| Target boat price | The purchase price you want each lender to assess | Helps every lender assess the deal the same way |

| Planned down payment | An amount you can support without draining your buffer; source examples show offers as low as 10%, while many cases are closer to 20-30% | Keeps affordability tied to liquidity |

| Expected financing range | The financing range you want lenders to evaluate | Keeps the discussion focused on affordability and risk |

| Used-boat age and condition notes | Include if you are considering a used boat | Boat type and condition can affect terms |

| Marine-survey plan | Include a survey plan; one cited estimate places survey cost around $17-$20 per linear foot | Can surface issues early enough to renegotiate or walk away |

Use a down payment you can support without draining your buffer. Source examples show offers as low as 10%, while many cases are closer to 20-30%.

If you are considering a used boat, include age and condition notes and a marine-survey plan. Boat type and condition can affect terms, and a survey can surface issues early enough to renegotiate or walk away. One cited estimate places survey cost around $17-$20 per linear foot.

Step 2 Check your baseline risk position#

Have a simple baseline before the first call: your current credit profile, your total borrowing plan, and how much liquidity you will still have after the upfront payment. Stronger credit can improve pricing, while weaker credit may still be approved at a higher rate.

Also pressure-test ongoing ownership costs. Insurance, fuel, maintenance, and storage are often cited at about 10% of ownership cost, so avoid committing all available cash at closing.

Step 3 Build one realistic loan draft#

Build one simple loan draft before lender calls using real assumptions for down payment, term, and rate.

Term structures vary. Source examples include 2 to 15 years, with some loans extending up to 20 years. One market snapshot cited roughly 8%-16%, and many products use variable-rate APR, so repayments can move when base rates move.

If the deal only works at the longest term or the most optimistic rate, lower the target price or pause. A practical next checkpoint is an in-principle approval before boat hunting, which can improve your chances when an offer is on the table.

Set your cashflow ceiling before boat shopping#

Set one hard monthly ceiling before you shop, and treat any deal that depends on perfect cash timing as out of bounds. If the payment only works when invoices clear on schedule or you need to float gaps on cards, lower your target price or wait.

Step 1 Calculate one all-in monthly cap#

Build your cap from one total monthly number, not a pile of separate estimates. Include the loan payment, maintenance, storage, and other ownership costs, plus any sales tax effect on financing or cash due at closing.

Use the same inputs lenders use in boat-loan math: purchase price, down payment, loan term, APR, and sales tax, if applicable. Also account for the fact that lenders may include presumed operating and maintenance costs when they assess monthly debt.

Step 2 Reject plans that rely on unstable cash#

Use a strict screen: if the plan needs a strong revenue month, a hoped-for client payment, or ongoing credit-card balances, it is not resilient enough.

Minimum card payments can make a tight month look manageable, but that does not make the debt affordable. Paying more than the minimum lowers what you pay over time, so carrying minimum payments month after month is a warning sign, not a strategy.

Step 3 Compare two structures before choosing a price band#

Before you settle on a price range, pressure-test two structures on the same boat price:

- Higher down payment with shorter loan term

- Lower down payment with longer term

Shorter terms usually raise monthly payments but reduce total interest, while a larger down payment reduces monthly payments on the same terms. Use realistic down-payment ranges, commonly 10% to 20%, with some market guidance at 10% to 30%, and choose the structure that still works in a weaker revenue month.

Step 4 Set a post-closing reserve and test it#

Decide on a post-closing reserve in dollars before you sign so the purchase does not crowd out needed living or operating funds. Do not drain needed living or operating funds just to improve the financed amount.

Run one final check after including the down payment, sales tax due, and immediate ownership costs. If the reserve left is too thin to use confidently, the boat loan is too large.

Compare financing paths for your situation#

Once you know your ceiling, choose the financing path that protects it in normal months and weak ones. For most independent purchases, start with a dedicated boat loan quote, use personal loans as a comparison point, treat credit cards as short-term bridging only, and look at SailTime financing only if the boat will enter the SailTime fleet.

Step 1 Separate open-market options from program-only financing#

A boat loan is a specialty product for buying a boat, and lenders price both your profile and the collateral. BoatUS says dedicated boat loans can offer more competitive rates and better terms than personal loans or credit cards, but Boat Trader also notes that rates and terms vary by credit history, collateral type and age, and loan amount.

SailTime sits in a different lane. Its financing is only for boats purchased and placed into the SailTime program, so it is not interchangeable with general marine-lender quotes.

| Path | Approval friction and flexibility | Collateral risk | Prepayment and refinancing |

|---|---|---|---|

| Boat loan | Specialty product for boat purchases. BoatUS says review can include a credit inquiry and follow-up documents such as tax returns or bank statements. BoatUS says many applicants get decisions in 2-4 business days, and some online partner channels through YachtWorld cite 24-48 hours. Terms commonly run seven to twenty years. | The boat is collateral, so default can put the vessel at risk. | Prepayment terms depend on the contract. Refinancing can be used to lower payment, reduce rate, or shorten duration. |

| Personal loan | Typically unsecured and based on your promise to repay, not pledged boat collateral. | No boat pledged as collateral. | Check the contract for any prepayment-penalty conditions. Refinance options can differ from secured marine loans. |

| Credit card financing | Card financing works differently from installment lending. | Not structured around boat collateral the way secured marine loans are. | APR may be fixed or adjustable. FRED listed commercial-bank credit-card plans at 20.97 in Nov 2025, so carrying a large balance is often expensive. |

| SailTime fleet program financing | Conditional and tied to fleet placement, not a general market offer. | Eligibility depends on program participation, so this is not a direct substitute for open-market lending. | SailTime advertises no prepayment penalties after the first 12 months. Verify first-year terms and any refinance limits in writing. |

Step 2 Check the contract terms that create risk later#

Start with collateral and prepayment language. A secured marine loan can come with a longer structure, but missed payments can put the boat at risk. An unsecured loan avoids pledging the boat, but it can still strain cashflow if the payment or cost is higher.

Then check payoff terms line by line before comparing APRs. Prepayment penalties depend on the agreement, so ask each lender for the exact payoff language, not a verbal summary.

Refinancing should also be part of your first decision. Boat Trader presents refinancing as a practical way to improve payment, rate, or term on an existing boat loan, and options can differ with personal loans or card financing.

Step 3 Choose your first quote by fit, not familiarity#

If you are buying outside a fleet program, get marine loan quotes first and prepare follow-up documentation early.

If avoiding collateral is your top priority, compare a personal loan only after you have a marine-loan baseline for payment, term, and prepayment terms.

If the plan depends on carrying card debt beyond a short gap, resize the purchase.

If the boat is entering the SailTime fleet, treat SailTime as a separate decision tree and confirm eligibility, first-year prepayment terms, and contract constraints before closing.

You might also find this useful: The Best Personal Finance Apps for Freelancers.

Build your underwriting packet before pre-approval#

Treat pre-approval as a real underwriting submission, not a casual rate check. BoatUS describes the flow as calculator first, then an Online Loan Application for underwriting review, followed by lender evaluation to set next steps. A clear packet helps you avoid preventable back-and-forth.

Step 1 Build a one-page borrower summary#

Start with one page that makes your file easy to evaluate: target purchase price, planned down payment, and any trade-in value. If your income pattern needs context, add a short note in plain language.

BoatUS says loan amount is purchase price minus down payment and trade-in value, and notes most lenders require a down payment, typically 10% to 20%. If those inputs are not clear before pre-approval, the review gets harder than it needs to be.

Verification point: you should be able to answer, on one page, what you are buying, how much cash you are putting in, and whether a trade-in is part of the deal.

Step 2 Explain uneven income before it is interpreted as risk#

If your income is seasonal, project-based, or concentrated in a few clients, include a short memo up front. Explain strong and weak months, contract timing, and concentration in plain language.

The goal is context, not spin. If income is uneven, explain the timing so the pattern is easier to evaluate.

Verification point: a lender should be able to tell whether the variability reflects seasonality, timing, or a real decline.

Step 3 Confirm the underwriting path if an LLC is involved#

If you are buying through an LLC, confirm the lender's review path before you apply. Ask what they want evaluated for your file and how the borrower should be structured in the application and closing process.

Get that answer lender by lender, in writing. That helps you avoid rebuilding the file late under a different structure.

Step 4 Turn lender signals into your own pass/fail checklist#

Use lender-facing guidance to build your own pre-submit checks. BoatUS highlights the core variables in loan math: down payment, trade-in value, interest-rate variation by lender and credit profile, market conditions, and the payment-versus-total-interest tradeoff across term length. MarineMax also notes that quoted monthly payments are estimates and finalized at purchase.

Run this checklist before every application:

- I know the exact purchase price, down payment target, and any trade-in value.

- I can explain the income number on the application, especially if it is uneven.

- I understand rate and payment assumptions can vary by lender, credit profile, and market conditions.

- I chose a term with a clear monthly-payment versus total-interest tradeoff.

- I am treating pre-qualification results and quoted monthly payments as non-final until closing.

If key items are still unclear, clean up the packet before you submit.

We covered this in detail in How to Finance Your First Rental Property.

Run scenario math that goes beyond monthly payment#

Do not decide from a single monthly quote. When you run the numbers, keep the boat and ownership assumptions constant, then test whether the structure still works when cashflow timing gets worse.

Step 1 Build three cashflow scenarios first#

| Scenario | Cash condition | Pass test |

|---|---|---|

| Base case | Normal client receipts and usual expenses | Loan payment and core obligations clear without strain |

| Weak quarter | Lower revenue or slower bookings for one quarter | Payments still clear from current cashflow |

| Bad quarter with delayed receivables | Expected invoices arrive late | Payments clear from settled cash and reserves, not hoped-for collections |

If a structure only works when receivables arrive on time, it is too tight.

Step 2 Stress the core loan variables in order#

Run the same scenarios through your Boat Loan Calculator and adjust three core inputs: APR, loan term, and down payment.

| Variable | How to test it | Grounded note |

|---|---|---|

| APR | Hold purchase price constant and test APR assumptions | One market snapshot cited roughly 8%-16%, and many products use variable-rate APR |

| Loan term | Hold APR constant and compare term options | Source examples include 2 to 15 years, with some loans extending up to 20 years |

| Down payment | Hold purchase price and APR constant, then shift down payment levels | Include the lender-typical 10% to 20% range and test a higher down payment only if liquidity stays healthy |

Work through them in this order:

- Hold purchase price constant and test APR assumptions.

- Hold APR constant and compare term options.

- Hold both constant and shift down payment levels.

Include the lender-typical down-payment range of 10% to 20%, then test a higher down payment only if liquidity stays healthy. Use an amortization schedule so you compare total borrowing cost, not just payment size.

Step 3 Add timing-sensitive costs that quick quotes miss#

Include sales tax (if applicable), lender fees reflected in APR, and both upfront and annual ownership costs in the months they are likely to hit. A deal can look fine on an annual view and still create a cash squeeze when upfront items stack into a weak receivables period.

Also account for closing requirements that can affect timing, such as a marine survey and an executed sales contract. If the timeline shifts, your cash plan should still hold.

Step 4 Apply a break-even stop rule#

Add annual debt service to annual ownership costs, then compare that total to your stable cashflow band after essential living costs and core business needs. If total ownership plus debt exceeds that band, pause or resize the purchase.

Use this as a conservative decision rule:

- If it fails in the base case, stop.

- If it passes the base case but fails the weak quarter, lower the budget.

- If it fails the bad quarter unless you rely on revolving debt, walk away.

Choose a go-or-wait decision with explicit rules#

Make the decision explicit. Use credit score, debt-to-income ratio, and post-close liquidity to choose one path before you apply.

Step 1 Build a simple matrix#

This matrix is a screening tool, not a promise of approval. Use all three signals together.

| Decision | What your file looks like | What to do next |

|---|---|---|

| Apply now | Credit is solid, DTI is in or near a lender-friendly range, and you still have meaningful cash reserves after closing | Move to pre-approval, then compare lender terms |

| Wait and recheck | One metric is weak but improving | Improve that metric first, then recheck on a set date |

| Lower budget or pause | The deal requires thin reserves or a high post-close DTI to work | Reduce the purchase target, or pause until the file is stronger |

As reference points, one marine-finance source uses 700+ as a useful credit target, and another says many lenders prefer DTI around 35% to 45% or lower. Treat those as guides, not universal cutoffs, because lender and product limits vary.

Step 2 Verify all three inputs with current numbers#

Do not decide from memory. Pull your current credit score, calculate DTI as monthly debt payments divided by gross monthly income, and estimate cash reserves after the down payment, tax, fees, and immediate catch-up costs.

Use the same numbers in your calculator and in your application prep. Pre-close cash is not a reserve if it disappears at closing.

Step 3 Fix the weakest metric first#

If one metric is weak but improving, focus on that single fix before submitting new applications.

If credit is the issue, work on credit first. If DTI is the issue, reducing recurring debt can help improve that ratio. If DTI is borderline and reserves are thin, rebuild liquidity before applying.

Avoid scattered applications while you are in that improvement window.

Step 4 Set a personal rejection trigger#

Use a stricter stop rule than technically approved. If the offered terms only work when future cashflow arrives exactly as planned, do not proceed.

Higher DTI can lead to tighter terms, more down-payment pressure, or denial. Even with approval, walk away if the plan depends on uncertain cashflow or fallback credit card financing.

Step 5 Write down the decision#

Record the date, your three inputs, your scenario result from the prior section, and your action: apply now, wait and recheck, or lower budget.

Keep it short and factual so the next review is based on updated numbers, not listing pressure.

Related: A Guide to Sailing Around the World as a Digital Nomad.

Submit applications and negotiate terms without hurting approval odds#

Keep applications tight, comparable, and time-boxed so you can negotiate from clean offers instead of noisy credit activity.

Step 1 Tighten your lender list and timing#

Apply to a short list of lenders that specialize in marine financing, then submit within one shopping window. CFPB guidance says same-type loan inquiries are generally treated as a single inquiry when they happen within 14 to 45 days, and one boat-finance source suggests a practical target of a couple weeks to a month.

Treat every Online Loan Application as a real application event. If a site routes you to an online application for partner underwriting, log it with the submission date and keep it inside the same window.

Step 2 Negotiate the terms that matter after the rate#

Headline rate is only part of the deal. Negotiate the terms that affect payoff flexibility and closing risk. Ask each lender the same questions and get the answers in writing.

| Item to compare | What to ask |

|---|---|

| Rate lock | Is the rate locked, and until what date? If it is not locked, when can it change? |

| Prepayment penalties | Is there a fee for paying off early or making large principal payments? Can you quote a similar loan without that feature? |

| Refinance path | Do you or an affiliate handle boat-loan refinance, and what timing rules apply? |

| Early-pay flexibility | Can you make extra principal payments without fees or restrictions? |

If lock status, penalty terms, or payoff flexibility are unclear, treat that as risk and press for a clearer offer.

Step 3 Ask about refinancing before you sign#

Ask refinance-path questions while lenders are still competing for your business. Confirm whether they, or an affiliate, handle boat-loan refinance and whether they require a minimum age on the existing loan.

There is no universal refinance timeline. One lender discloses a 260-day minimum, while another says there is no clear-cut rule, so get each lender's rule in writing.

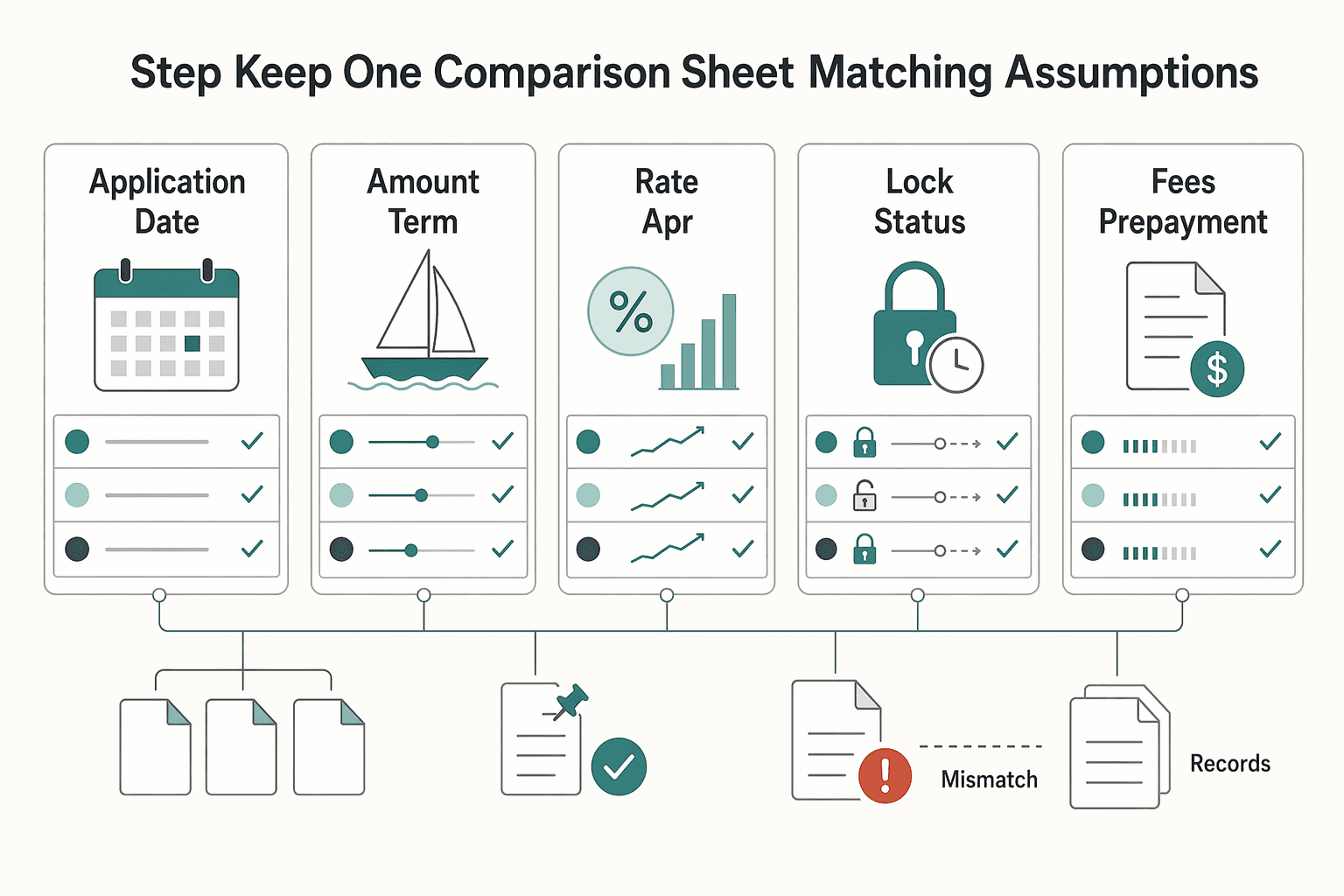

Step 4 Keep one comparison sheet with matching assumptions#

Do not compare mismatched quotes. Request the same loan type, purchase price, down payment, term, and expected close timing from each lender.

| Quote field | What to track | Grounded note |

|---|---|---|

| Application date | Record the submission date for each lender | Keep applications inside the same shopping window |

| Amount and term | Use the same loan type, purchase price, down payment, term, and expected close timing | Do not compare mismatched quotes |

| Rate or APR | Track the quoted rate or APR | Save each quote with its date because advertised rates are time-sensitive |

| Lock status and expiry | Note whether the rate is locked and until what date | If lock status is unclear, treat that as risk |

| Fees and prepayment terms | Track fees and any payoff or extra-principal limits | If penalty terms or payoff flexibility are unclear, press for a clearer offer |

| Refinance notes and required documents | Track refinance-path notes and requested documents | Get timing rules and document needs in writing |

Track lender name, application date, amount, term, rate or APR, lock status and expiry, fees, prepayment terms, refinance notes, and required documents. Save each quote with its date, since advertised rates are time-sensitive.

Related reading: How to Clear In and Out of Countries on a Sailboat.

Protect repayment cashflow with a stronger get-paid system#

Approval is only the start. The loan stays manageable when each monthly payment is funded early with settled cash, kept separate from day-to-day spending, and checked before the due date.

Step 1 Separate repayment money from day-to-day cash#

If your setup allows it, keep repayment cash in a dedicated reserve separate from your operating pool. The goal is simple: move repayment cash out of everyday spending visibility once it is settled.

Keep three balances easy to see: operating cash, next-payment reserve, and true excess. Before each due date, confirm the full payment is already visible in the reserve and funded by settled receipts, not pending transfers or expected invoices.

Step 2 Shorten receivables so payments come from settled cash#

Repayment is safer when invoices turn into cash faster than the loan comes due. Tighten invoicing and follow-up so debt service is funded by settled receipts, not timing luck.

If you regularly need credit cards to bridge normal payment cycles, treat that as a structural mismatch between repayment obligations and cash conversion. Adjust billing structure, reserve levels, or purchase sizing before that gap becomes routine.

Step 3 Match repayment planning to tax-document reality#

For globally mobile owners, keep repayment planning aligned with tax-document discipline so you do not overstate available cash. If cross-border reporting is part of your process, keep those records organized alongside reserve planning.

When it applies, Form 8938 is the key document to track. The IRS says it is attached to your annual income tax return, and filing depends on both being a specified person and having an interest in reportable specified foreign financial assets, which can include an account at a foreign financial institution. The IRS cites aggregate value exceeding $50,000 for certain U.S. taxpayers and also states higher thresholds apply for joint filers and taxpayers residing abroad. If you do not have to file an income tax return for the year, you do not need to file Form 8938 for that year.

Step 4 Review monthly before each due date#

Run one non-negotiable monthly checkpoint before the payment is due. Review invoice aging, confirm the reserve balance, and verify the next payment is already covered by settled cash.

If that payment is not yet visible, treat it as an active issue, not a healthy month. This cadence gives you warning before client delays or competing cash claims turn into missed payments.

This pairs well with our guide on How to Have a Healthy Money Conversation with Your Partner.

Before your first loan payment hits, you can standardize billing with this free invoice generator.

Common financing mistakes and how to recover#

Financing mistakes usually become obvious when you review written terms and actual cashflow regularly. Recovery starts by checking documents and liquidity before you shop again.

Step 1 Reset affordability before you keep shopping#

If you chose the boat before setting your limit, pause and rebuild around APR (annual percentage rate), payment fit, and reserves. The core test is whether the payment still works in a weaker period and leaves enough liquidity after closing costs to cover the next due date from cash already in hand.

Use calculators and summaries as a starting point, then confirm your go or no-go decision against the actual loan documents and your reserve math. If the payment only works with expected invoices, reduce the purchase size, adjust the structure, or wait.

Step 2 Audit the first approval instead of accepting it#

An approval is a starting point, not a final answer. Compare offers side by side using the same fields every time: APR, term length, payment, required cash at closing, and cash left after closing.

Rely on the primary loan paperwork, not verbal summaries. If any term is unclear, get it in writing and re-check before signing.

Step 3 Stop using short-term borrowing to paper over a bad structure#

Recurring short-term borrowing to make routine payments can signal a structural problem. Recover by reducing that dependence and rebuilding liquidity until the next payment can be covered by settled cash, not future receivables.

If you still need a bridge to make routine payments, revisit the purchase size or financing structure before the gap becomes permanent.

If you want a deeper dive, read How to Invest in Real Estate as a Digital Nomad.

Final checklist before you sign#

A clean approval is not the finish line. If you want a practical way to finance the boat without stressing your business, sign only when the deal still works in a bad quarter, not just a normal month.

Step 1: Re-run the payment against real cashflow#

Run the final offer through your actual numbers, not memory. Use a boat loan calculator with the offered rate, loan term, and down payment, then compare the payment against both your base month and your weaker months.

Do not evaluate the loan payment in isolation. Include total ownership costs such as insurance, maintenance, storage, registration, fuel, and upgrades. After the down payment and closing cash leave your account, you should still be able to cover near-term payments from reliable cashflow.

As a final pressure check, review DTI. One source suggests that keeping DTI ideally below 40% can improve approval odds, but at this stage it is also a sanity check on affordability.

Step 2: Audit the final offer and closing documents#

Confirm the written terms line by line before signing. Verify the interest rate, loan term, down payment, fees, and any stated prepayment terms in writing.

Review the sale documents with the same care. The Sales and Purchase Agreement should clearly set the deal terms, including when a deposit is returned or forfeited after checks or inspections. The Bill of Sale should list the vessel registration number, model, make, and year, and state whether finance is still outstanding on the vessel.

Expect some timing friction at closing. Missing proof of insurance, unclear deposit language, or mismatched vessel identifiers can delay completion, and marine financing can take longer than car loans.

Step 3: Check post-close liquidity and near-term obligations#

Before you wire funds, calculate what cash remains after the down payment, deposit, lender charges, and immediate ownership costs. Base that number on cash in the bank, not expected receivables.

Also confirm any registration and other closing-related payments you may need to handle around closing. The goal is simple: avoid draining working capital right after close because you focused only on the lender's cash-to-close figure.

Step 4: Write your fallback plan before you sign#

Write a one-page fallback plan before committing. If revenue dips, decide in advance what you will cut, what you will defer, and whether refinancing could be realistic later.

That keeps the decision disciplined. Sign when the boat improves your life without putting your business at risk.

If you want to operationalize this checklist across collections, balances, and payouts, contact Gruv.

Frequently Asked Questions

How do I finance a sailboat step by step if my income is variable?

Set your payment limit using weaker income months, not your best month. Prepare a clean packet with the target price, planned down payment, income explanation, and any documents the lender may request, such as tax returns and bank statements. Then compare written APR, term, cash to close, and any prepayment penalties before signing.

How much down payment is typical, and how should I decide my own amount?

There is no single universal down-payment rule. The article cites 10% to 20% in one source, 10% to 30% in another, and some programs may offer $0 down for eligible borrowers. Choose an amount that still leaves strong post-closing liquidity.

What do lenders check besides credit score when reviewing a sailboat loan?

Yes, lenders usually review more than credit score. The article notes debt-to-income ratio, liquidity, and broader stability signals such as employment and homeownership context. A 700+ score is one reference point, but approval still depends on the full file.

Is a marine boat loan usually better than a personal loan for freelancers?

Often, yes, but not automatically. Boat-specific loans can offer more competitive rates and terms than personal loans or credit cards, and may offer lower down payments or longer terms depending on the deal. Compare the written offer, especially APR, term, prepayment terms, and cash to close.

Can I qualify if my debt-to-income ratio is borderline but my liquidity is strong?

Possibly. Lenders weigh credit, liquidity, and debt-to-income ratio together, so strong liquidity may help when one metric is weaker. It still does not guarantee approval, so present clear financial documents up front.

When does SailTime fleet program financing make sense over independent marine lenders?

It makes sense only if the boat will enter the SailTime fleet. SailTime positions it as program-specific financing, not a general substitute for open-market marine lending. For qualified borrowers, it highlights LLC-friendly treatment, no processing fees, and no prepayment penalties after the first 12 months.

How much liquidity should I keep after closing if lender minimums are unclear?

There is no universal post-closing reserve target. Keep enough cash after closing to cover early payments and near-term obligations from cash already in the bank. If the reserve is too thin to use confidently, lower the purchase size or wait.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- consumer.ftc.gov/credit-scorestrusted

- consumerfinance.gov/ask-cfpb/what-is-the-difference-between-a-lo...trusted

- consumerfinance.gov/language/cfpb-in-english/auto-loans-key-termstrusted

- fdic.gov/consumer-resource-center/loanstrusted

- federalregister.gov/documents/2017/11/17/2017-21808/payday-vehic...trusted

- gao.gov/assets/a202440.htmltrusted

- irs.gov/businesses/corporations/do-i-need-to-file-fo...trusted

- irs.gov/irm/part5/irm_05-015-001trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Should Your Freelance Business Accept Credit Cards?

Offer card payments, but stay in control of how money reaches you. The goal is not a smoother checkout screen. It is predictable cash you can use to run the business.

How to Invest in Real Estate as a Digital Nomad

**Run anything with money and moving parts like an operations system (cash, docs, delegation, and controls), not a "passive income" vibe.** Real life stress-tests weak spots. You change time zones, a client pays late, and something breaks at the worst moment. As the CEO of a business-of-one, your job is to build a setup that keeps working when you are not available on demand.

Sailing Around the World as a Digital Nomad Without Breaking Your Workflow

A floating HQ may make sense only if you treat it as an operating change, not a reward for wanting more freedom. You are not just changing where you work. You are taking on more of the continuity burden yourself, with more autonomy on one side and more logistics and disruption exposure on the other.