Quick Answer

Start with your net profit from Schedule C line 31, because that is the input Schedule SE uses. Apply the form’s 92.35% adjustment before computing Social Security and Medicare, then check mixed-income handling if you also have W-2 wages in boxes 3 and 7. Finish by carrying the self-employment tax and deductible half through the Form 1040 package and confirming current-year instructions before submission.

For an independent professional, self-employment tax is not just another line on the return. It is one of the biggest places where sloppy defaults turn into avoidable cost. The standard advice to "set aside 30%" is a rough rule for a rough situation. It does not reflect the control you can have over how this tax is calculated, planned for, and managed when your business is run deliberately.

The goal is not to become a tax expert. It is to stop treating tax compliance like a yearly fire drill and treat it like an operating discipline. This guide walks through that shift in three parts. First, get the baseline right. Second, use the few planning decisions that actually change the result. Third, set up a process that keeps tax cash and tax math under control all year.

Comply with Confidence: Mastering the Non-Negotiable Baseline#

Get the baseline right before you try to lower your tax bill. Many errors here are mechanical: starting from gross revenue instead of profit, carrying the wrong Schedule C number, or ignoring W-2 Social Security wages in a mixed-income year. Keep these terms straight before you do any math:

- Net earnings from self-employment: your business gross income minus ordinary and necessary business expenses.

- Self-employment tax: Social Security and Medicare tax for people who work for themselves.

- Social Security portion: the Social Security part of self-employment tax (12.4%).

- Medicare portion: the Medicare part of self-employment tax (2.9%).

- Adjustment to income (SE tax): the deductible employer-equivalent half of your self-employment tax, used when figuring AGI.

Start with your completed Schedule C, any Forms W-2, and the current-year Schedule SE instructions. Do not reuse last year's wage-cap number.

Step 1. Confirm you need Schedule SE#

Check the current-year filing trigger in the IRS instructions before you file. You usually owe self-employment tax if your net earnings are $400 or more.

Also follow the form's stop rule. If the computed earnings amount on Schedule SE is under $400, you stop and do not owe self-employment tax.

Step 2. Run the calculation in the IRS order#

The form does not apply the full rate to 100% of Schedule C profit. If the relevant line is positive, Schedule SE first applies 92.35% (0.9235), then calculates the Social Security and Medicare portions. If you skip the 92.35% step, you likely overstate the tax.

Step 3. Reconcile the form flow (Schedule C to Schedule SE to Form 1040 package)#

| What you enter | Where it comes from | Where it goes next |

|---|---|---|

| Net profit or loss | Schedule C line 31, business income minus ordinary and necessary expenses | Used on Schedule SE; also reported through Schedule 1 in the Form 1040 package |

| Net earnings subject to SE tax | Schedule C line 31, then adjusted on Schedule SE, including the 92.35% step when required | Schedule SE computes self-employment tax |

| SE tax and one-half deduction | Completed Schedule SE | SE tax is attached through Schedule 2 in the Form 1040 package; one-half is deducted as an adjustment to income |

Checkpoint: the Schedule C line 31 amount should match the starting profit figure you carry into Schedule SE. If it does not, fix that before filing. If you need a refresher on the starting form, use A Guide to Schedule C (Profit or Loss from Business) for Freelancers.

Step 4. Apply the mixed-income guardrail before filing#

This is a common error point. If you have both self-employment income and wages, you need to check how the Social Security portion is applied across both.

If you have self-employment income only, verify the current-year Social Security maximum in that year's Schedule SE instructions, and follow Schedule SE rules for the Medicare portion.

If you have self-employment income plus W-2 wages, review your W-2 Social Security wages and tips, boxes 3 and 7, before filing. Schedule SE uses that information to apply the combined-wages guardrail so you do not overpay the Social Security portion once combined wages and self-employment earnings reach the annual maximum.

If these four items reconcile, your baseline is solid: Schedule C line 31, the 92.35% adjustment, W-2 Social Security wages if any, and the one-half deduction.

For related cross-border context, read Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Optimize Like a CFO: The High-Earner's Strategic Edge#

Once the baseline math is right, only a few planning decisions deserve serious attention. The big ones are retirement-plan structure, cross-border Social Security treatment, and how the half-SE-tax adjustment carries through the return. If your facts involve two countries, W-2 wages, or a new retirement plan, verify current-year rules before filing.

Before you start: keep your completed Schedule C, any Forms W-2, current-year Schedule SE instructions, and any foreign social insurance records in front of you.

Step 1. Choose a retirement plan by contribution role and cash-flow reality#

Start with how the contribution works. That determines how the plan behaves in practice:

- A one-participant 401(k) has two roles: employee and employer.

- A SEP uses employer contributions only.

- A SIMPLE IRA allows both employee and employer contributions.

Do not assume a contribution automatically lowers self-employment tax. The guidance in the draft places self-employed retirement-plan deductions on Form 1040 Schedule 1. Unless you have verified the current-year treatment, treat this first as an income-tax and long-term savings decision.

| Plan | Setup complexity | Contribution flexibility | Cash-flow fit | Usually the safer default when |

|---|---|---|---|---|

| SEP-IRA | IRS describes it as easy to set up and operate | Employer contributions only; annual contributions can vary | Strong fit for uneven income | You want low friction and variable annual funding |

| One-participant 401(k) | Same rules and requirements as other 401(k) plans | Employee and employer contribution roles | Better if you can handle more administration | You want both contribution buckets and can manage compliance |

| SIMPLE IRA | Allows employee and employer contributions; confirm current eligibility and rules | Employee and employer contributions | Depends on your contribution cadence and current-year plan rules | You want both roles without using a one-participant 401(k) |

Contribution limits change by filing year, so verify them before you act. For reference, the draft notes that IRS Publication 560 lists elective deferrals at $23,500 (2025) and $24,500 (2026). It also lists the defined-contribution plan limit at $70,000 (2025) and $72,000 (2026), excluding catch-up contributions.

Step 2. Run FEIE vs. Totalization as a two-question decision path#

If you live abroad, keep income tax separate from Social Security and Medicare treatment. That distinction matters because people often apply an income-tax concept to a payroll-tax issue and get the wrong answer.

| Question or claim | Focus | What to verify |

|---|---|---|

| FEIE | Income tax | Can affect income tax, but does not eliminate U.S. self-employment tax on net profit |

| Totalization Agreement | Social Security and Medicare tax | Check whether an agreement applies because it must be considered when determining whether an individual is subject to U.S. Social Security and Medicare tax |

| Agreement-based exemption | Documentation | A Certificate of Coverage is required from the foreign social security agency, and a copy of that foreign certificate must be attached to the U.S. return each year |

- FEIE question: FEIE can affect income tax, but it does not eliminate U.S. self-employment tax on net profit.

- Totalization question: check whether a Totalization Agreement applies, because IRS guidance says these agreements must be considered when determining whether an individual is subject to U.S. Social Security and Medicare tax.

If you claim an agreement-based exemption, documentation is not optional. IRS guidance requires a Certificate of Coverage from the foreign social security agency, and SSA guidance says a copy of that foreign certificate must be attached to the U.S. return each year. Verify the current documentation requirement before filing.

Step 3. Carry the half-SE-tax deduction through the correct forms#

This adjustment is easy to miss because it feels minor, but it touches more than one part of the return. The half-SE-tax deduction is calculated on Schedule SE and carried through Schedule 1 in the Form 1040 package. Do not rely on an old Schedule 1 line number without checking the current-year form.

That carry matters because the retirement-plan calculation guidance references the deductible part of SE tax from Schedule 1. Before you file, confirm:

- The deduction came from the completed current-year Schedule SE.

- It is reported on current-year Schedule 1 as an adjustment to income.

- You escalate to a tax professional if you have mixed-country coverage, a potential Totalization claim, mixed W-2 and self-employment income, or retirement-plan calculations that depend on the deductible SE-tax amount.

If your business structure is still an open question, see How to Choose the Right Business Structure for Your Freelance Business.

Automate for the Future: Building Your "No Surprises" System#

Once the return mechanics and planning choices are clear, the next job is operational. A good tax process does two things consistently: it calculates from current numbers, and it keeps payment cash separate before each due date. That is what keeps estimated payments tied to real performance instead of vague memory.

Step 1. Build a repeatable estimated-tax process#

Estimated tax is pay-as-you-go and can include both income tax and self-employment tax. If you are self-employed, you generally file annually and pay estimated taxes quarterly. Four equal installments are the default, and the annualized installment method may help when income is uneven. Use this sequence every time you refresh your estimate:

| Checkpoint | Figure | Note |

|---|---|---|

| Balance due after withholding and refundable credits | At least $1,000 | Estimated payments are usually in play |

| Current-year tax comparison | 90% of current-year tax | A common anti-penalty comparison |

| Prior-year tax comparison | 100% of prior-year tax | A common anti-penalty comparison |

| Higher prior-year comparison | 110% of prior-year tax | Applies when prior-year AGI was above $150,000 or $75,000 if married filing separately |

- Project annual net profit from Schedule C, line 31:

Projected net profit = ____ - Estimate net earnings subject to SE tax:

Projected net profit x 0.9235 = ____ - Estimate self-employment tax:

Result x 15.3% = ____

If you also have W-2 wages, review current Schedule SE instructions before finalizing the Social Security portion.

- Estimate federal income tax: start with expected AGI, then taxable income, then expected tax after deductions, credits, and withholding.

Estimated federal income tax = ____ - Compute annual amount still to cover:

SE tax + federal income tax + other expected tax - withholding - refundable credits = ____

- Set installment target:

Annual amount still to cover / 4 = ____

If income is lumpy, rerun quarter by quarter instead of forcing equal payments.

Checkpoint: if you expect to owe at least $1,000 after withholding and refundable credits, estimated payments are usually in play. A common anti-penalty comparison is 90% of current-year tax or 100% of prior-year tax. That increases to 110% when prior-year AGI was above $150,000 or $75,000 if married filing separately. Verify the current payment schedule and safe-harbor rules before you rely on them.

Step 2. Fund a dedicated tax account from actual exposure#

A fixed reserve percentage is easy, but it may not match your actual exposure. A better approach is to fund a dedicated tax account from your actual exposure: projected self-employment tax, projected federal income tax after deductions and credits, and any state or local exposure. Verify your current reserve target before you use it.

The key is not just the percentage. It is discipline around the account itself. Keep boundaries strict so records stay clean and payment cash does not get spent by accident. Use this operating checklist:

- Transfer trigger: when client money clears into business checking, move the tax reserve.

- Transfer timing: set a consistent timing rule you can follow (for example, same day or next business day).

- Separation rule: do not use the tax account for operating expenses or personal spending.

- Regular true-up (for example, monthly): compare reserved cash to your updated annual estimate and next due amount; if short, top it up before additional spending.

For execution, IRS Direct Pay allows bank-account payments and lets you change or cancel a scheduled payment within 2 days. If you use EFTPS, schedule by 8 p.m. ET at least one calendar day before the due date.

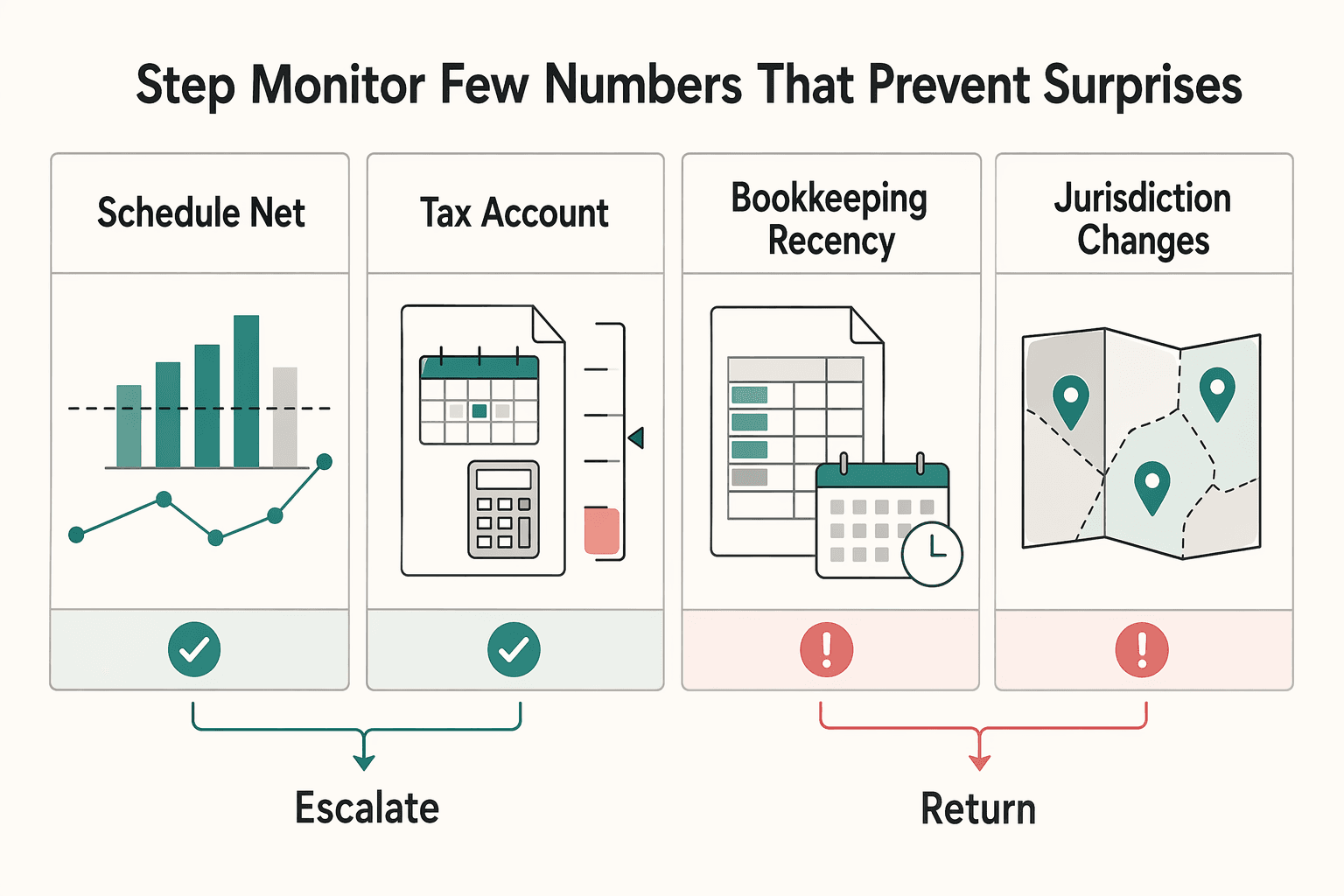

Step 3. Monitor the few numbers that prevent surprises#

You do not need a complex dashboard here. You need a short list of control numbers and a habit of acting quickly when one drifts.

| Metric | Why it matters | Action if off-track |

|---|---|---|

| Schedule C net profit year to date | This feeds your SE estimate and estimated-tax math | Reforecast immediately if actual profit is materially above or below plan |

| Tax account balance vs next payment | Confirms cash readiness, not just spreadsheet intent | Transfer any shortfall now and pause owner draws until caught up |

| Bookkeeping recency | Stale books weaken every estimate | Close books before calculating the next payment |

| Jurisdiction changes | New state or cross-border facts can change obligations | Escalate before the next deadline if your filing footprint changed |

Escalate early if income swings quarter to quarter, bookkeeping lags long enough to make estimates guesswork, or your facts span multiple jurisdictions.

For a step-by-step walkthrough, see How to Fill Out FBAR (FinCEN Form 114) Step by Step.

If you have both employee and self-employment income, pressure-test your classification before you finalize Schedule SE with the W-2 vs 1099 calculator.

From Form-Filler to Financial CEO: Your Next Move#

The practical shift is simple: handle Schedule SE like an operating routine, not a once-a-year scramble. Start with clean inputs, apply only the rules that change the outcome, and build a process that keeps both the math and the cash current. When the facts stop being simple, escalate early.

Step 1. Reconcile the inputs before you calculate#

Comply: reconcile the inputs before you calculate anything. Pull Schedule C, confirm line 31, net profit or loss, and trace it into Schedule SE. Confirm the 92.35% adjustment step, then check whether line 4c is at least $400. If it is under $400, Schedule SE says you stop for SE tax. If you had church employee income, verify the separate $108.28 trigger.

| Trigger | Amount | What the article says |

|---|---|---|

| Net earnings from self-employment | $400 or more | You usually owe self-employment tax |

| Computed earnings amount on Schedule SE | Under $400 | Stop and do not owe self-employment tax |

| Church employee income | $108.28 | Verify the separate trigger |

Signal to monitor: your books, Schedule C, and Schedule SE all tie out, with support for income and expenses. Failure mode to avoid: using gross revenue instead of net earnings, income minus ordinary and necessary business expenses, which can overstate SE tax. If your records are not clean yet, fix that first with your P&L, invoices, and expense records. Then use this Schedule C guide.

Step 2. Apply only the rules that change your result#

Optimize: apply only the rules that materially change your result. Confirm the deductible half of self-employment tax is handled correctly because it affects AGI. If you live abroad, do not treat FEIE as an SE-tax exemption. If you may rely on a totalization agreement, treat the Certificate of Coverage as required proof, not paperwork to chase later.

Signal to monitor: identify any mixed-income or cross-border complexity early. That includes W-2 plus self-employment income, foreign social insurance facts, or exposure near Additional Medicare Tax thresholds of $250,000 / $125,000 / $200,000 by filing status. Failure mode to avoid: taking a position before you have documentation to support it.

Step 3. Separate tax cash and review on a fixed cadence#

Automate: separate tax cash and run a fixed review loop. Here, a "tax savings account" simply means a separate bank account used only to hold estimated-tax money, not an IRS-defined term. Set a transfer approach from your year-to-date results, then pay estimated tax as income is earned. General due dates are April 15, June 15, September 15, and January 15 of the following year, but confirm current-year calendar shifts before paying.

Signal to monitor: stay on track against estimated-tax underpayment checkpoints, including the $1,000 balance-due test and the 90% / 100% payment framework. Failure mode to avoid: paying yourself first and discovering the tax shortfall later. Operational definitions: here, "owner pay rhythm" means your planned timing for moving money to personal spending after reserving tax cash. "Review cadence" means your recurring check before each estimated-tax deadline to compare profit, transfers, and taxes paid.

Step 4. Escalate when the facts stop being plain#

You may be able to handle it internally when you have one straightforward Schedule C, current books, no totalization exemption claim, and no meaningful wage and self-employment interaction.

Consider bringing in a tax professional when you live abroad, use FEIE, may claim totalization treatment, need Certificate of Coverage support, have both W-2 and self-employment income, or are near Additional Medicare thresholds. That is where small classification errors can become expensive.

You might also find this useful: How to Fill Out Form 1116 (Foreign Tax Credit).

If your Schedule SE workflow still feels unclear after the checklist, map the safest next step for your cross-border setup by talking with Gruv.

Frequently Asked Questions

Do you pay self-employment tax on foreign income?

Do not assume the Foreign Earned Income Exclusion (FEIE) settles this by itself. FEIE is an income-tax exclusion for qualifying individuals, and you still file a U.S. return reporting the income. To claim FEIE-related benefits, you need foreign earned income and a foreign tax home, and if you qualify for only part of the year, your maximum exclusion is adjusted by qualifying days. Use the IRS Interactive Tax Assistant, keep a clear day-count log if you are using the 330 full days test, and verify any Schedule SE impact separately in current-year instructions or with a professional.

How do Solo 401(k) or SEP-IRA contributions affect this tax?

Do not assume all contribution types are treated the same. Confirm current-year IRS instructions before reducing estimates, and talk to a professional if you are combining plan types.

What is the fastest way to estimate what you may owe?

There is no one-line, grounded formula in this section for Schedule SE. Estimate from current books using current-year IRS guidance, then rerun the numbers whenever income shifts.

Can you deduct all of your self-employment tax?

Do not assume the full amount is deductible. Verify the deductible portion in current-year instructions, especially if you are amending a return or overriding software results.

Do you need a long form or short form for Schedule SE?

Use the current year’s Schedule SE and instructions instead of relying on older "long vs short" wording. If your return is not straightforward, confirm the correct path before filing.

What if you have both W-2 income and self-employment income?

Report both income streams on your U.S. return and treat mixed-income Schedule SE handling as a verify-now item in current-year instructions. Reconcile your records first, and get professional help for complex cross-border facts.

Do you owe self-employment tax if your business had a loss?

Do not assume a loss ends your filing obligations. Close your books, keep invoice and expense support, and verify current filing requirements before you assume no filing obligation applies.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How to Choose the Right Business Structure for Your Freelance Business

Most freelancers end up in a business structure by default rather than by design, but that accidental choice shapes taxes, personal liability, and payment operations in ways that compound over time. This guide walks independent professionals through four entity types — Sole Proprietorship, Single-Member LLC, S-Corp election, and Corporation — covering the tax treatment, liability exposure, and operational overhead of each. Rather than prescribing a single best answer, it provides a trigger-based framework: start with the structure that fits today, then upgrade when specific signals — indemnification clauses, enterprise KYB requirements, a first hire, or material net profit — make the switch worthwhile. The result is a deliberate, revisable foundation that keeps records clean, reduces onboarding friction, and avoids the expensive mismatches that come from letting structure lag behind business growth.

How Freelancers Can File Schedule C With Defensible Records

Use Schedule C as the operating report for your solo business. It reports business income, expenses, and your net profit or loss. If you are a sole proprietor, this is usually the form that determines it. If you are a [single-member LLC](https://www.irs.gov/businesses/small-businesses-self-employed/single-member-limited-liability-companies) that has not elected corporate tax treatment, it is generally treated as a disregarded entity for income tax, and Schedule C is often used to report that business income and expenses.