Quick Answer

Yes - use a 1031 exchange investment property plan only when you can keep sale proceeds under Qualified Intermediary control, send signed property identification within 45 days, and receive the replacement by 180 days or your earlier return due date with extensions. Treat cash back, debt relief, or other non-like-kind value as boot that can create recognized gain. If delivery proof, ownership intent, or money flow is unclear, pause closing and get CPA or tax attorney review.

The CEO's Playbook for a Bulletproof 1031 Exchange: A 3-Phase Risk Mitigation Framework#

A 1031 exchange is a tax-deferral strategy, not a tax eraser. Use it when you are selling real property held for business or investment and plan to stay invested in other real property. If you need immediate cash, want a simpler close, or may not buy again on schedule, a standard sale is often the simpler, lower-risk path.

Before you decide, align on the four terms that drive outcomes:

- Like-kind property: real property used for business or held for investment exchanged for other business or investment real property of the same type.

- Qualified intermediary (QI): a third party that holds and uses sale proceeds to acquire replacement property.

- Constructive receipt: access to sale proceeds, even without physically holding them. This can break deferral.

- Boot: cash or other non-like-kind property you receive. Gain is recognized up to that amount.

Treat this as your fit test before listing. For 2018 and later years, Section 1031 applies only to real property, and real property held primarily for sale is excluded. This route fits if you can keep proceeds inside the exchange, follow stricter process rules, and execute on deadline.

| Decision point | Standard sale | 1031 exchange |

|---|---|---|

| Tax timing | Gain generally taxed at sale | Gain deferred if rules are met |

| Cash access | You receive proceeds at closing | You cannot take actual or constructive receipt |

| Administrative complexity | Lower | Higher, with timing and documentation rules |

| Failure consequence | Normal taxable sale | Failed deferral is treated as a sale in the exchange year |

Start from a compliance-first default. Proceeds should go to a QI (or qualified trust), not to you or to any account you control without restriction. The common failure points are familiar and avoidable. They include taking or controlling funds, unplanned boot, missing the 45-day identification deadline, or missing the 180-day receipt deadline or earlier return due date, including extensions.

The rest of this playbook breaks execution into three phases. Bring your CPA, attorney, and QI in early as a risk-control measure. Then confirm current procedural limits before you act, including Form 8824 reporting and timing rules.

You might also find this useful: Tax Implications for a UK Resident Owning a US LLC.

Phase 1: The Blueprint - Pre-Sale Strategy & Team Assembly#

Start a 1031 only if you can clear a real pre-sale go or no-go screen before listing. If eligibility, fund control, or replacement planning is weak, treat that as a no-go and use a standard sale path.

Decide whether this should be an exchange at all#

Your first job is to rule out bad candidates before you spend time and money on setup:

| Screen | What it checks | Article detail |

|---|---|---|

| Eligibility | Whether the property is real property held for business or investment | Property held primarily for sale does not qualify |

| Structure | Whether deferred-exchange rules are satisfied | A sale followed by a later purchase is not enough by itself |

| Timeline | Whether you can execute on exchange deadlines | Identify within 45 days and receive within 180 days or the earlier tax return due date, including extensions |

- Eligibility screen: Section 1031 applies to real property held for business or investment. Property held primarily for sale does not qualify.

- Structure screen: A sale followed by a later purchase is not enough by itself. The deferred-exchange rules still have to be satisfied.

- Timeline screen: You need a credible plan to identify replacement property within 45 days and receive it within 180 days or the earlier tax return due date, including extensions.

Before you engage vendors, write a short decision memo that answers four questions. What does the taxable-sale path look like? If you pursue an exchange, where could boot still be recognized? What changes if proceeds stay under QI control and replacement real property is acquired under exchange rules? Are there any geography limits that narrow your options from the start?

Keep that analysis grounded with this checklist:

- Model the taxable-sale path. Estimate recognized gain without an exchange.

- Model the deferral path. Compare outcomes if proceeds stay under QI control and replacement real property is acquired under exchange rules, including potential boot.

- Map liquidity impact. If you need cash from closing for personal use or other obligations, reassess. Cash or other non-like-kind value can create boot.

- Check geography constraints now. For globally mobile plans, use the safe default: U.S. real property is not like-kind to foreign real property.

- Tax treatment checks: Have your tax team verify current capital-gains, NIIT, depreciation recapture, and state treatment assumptions.

At minimum, create a one-page comparison of taxable-sale versus exchange assumptions, expected cash available at closing in each path, and boot-risk notes.

Assign accountability before the property goes live#

A 1031 gets messy when responsibility is implied instead of assigned. Name one owner for each risk-critical lane before listing, then get the handoffs in writing.

| Accountability lane | Owner |

|---|---|

| Tax modeling and scenario assumptions | CPA |

| Contract language and closing document review | Attorney |

| Fund custody and exchange mechanics under written exchange agreement | Qualified Intermediary (QI) |

| Timeline control (45-day/180-day milestones and handoffs) | Broker or transaction lead |

| Final go/no-go decisions | You |

| Final reporting review (Form 8824) | CPA (with your sign-off) |

This split is an operating control, not a legal mandate. Get written confirmation of who owns what, along with document dependencies and handoff timing.

Vet the qualified intermediary on evidence, not reputation#

Choose a QI on documented controls, not marketing language. Ask basic questions. How are funds held? Who can move them? What coverage exists? Who will actually handle your file? Who has authority when something changes late?

| Candidate | Fund safeguards | Insurance coverage | Segregated accounts | Exchange experience | Service model | Fees | Escalation path |

|---|---|---|---|---|---|---|---|

| QI A | Confirm how funds are held and who can move them | Request proof of E&O and any fidelity bond | Confirm segregated vs pooled handling | Confirm deferred-exchange experience | Named operator vs pooled support | Written fee schedule | Named decision-maker for urgent issues |

| QI B | Same checks | Same checks | Same checks | Same checks | Same checks | Same checks | Same checks |

| QI C | Same checks | Same checks | Same checks | Same checks | Same checks | Same checks | Same checks |

State requirements can provide practical benchmarks, but they are not universal federal minimums. Example benchmarks: Virginia includes qualified escrow or trust handling and a $250,000 E&O minimum. Washington includes a $1,000,000 fidelity-bond minimum.

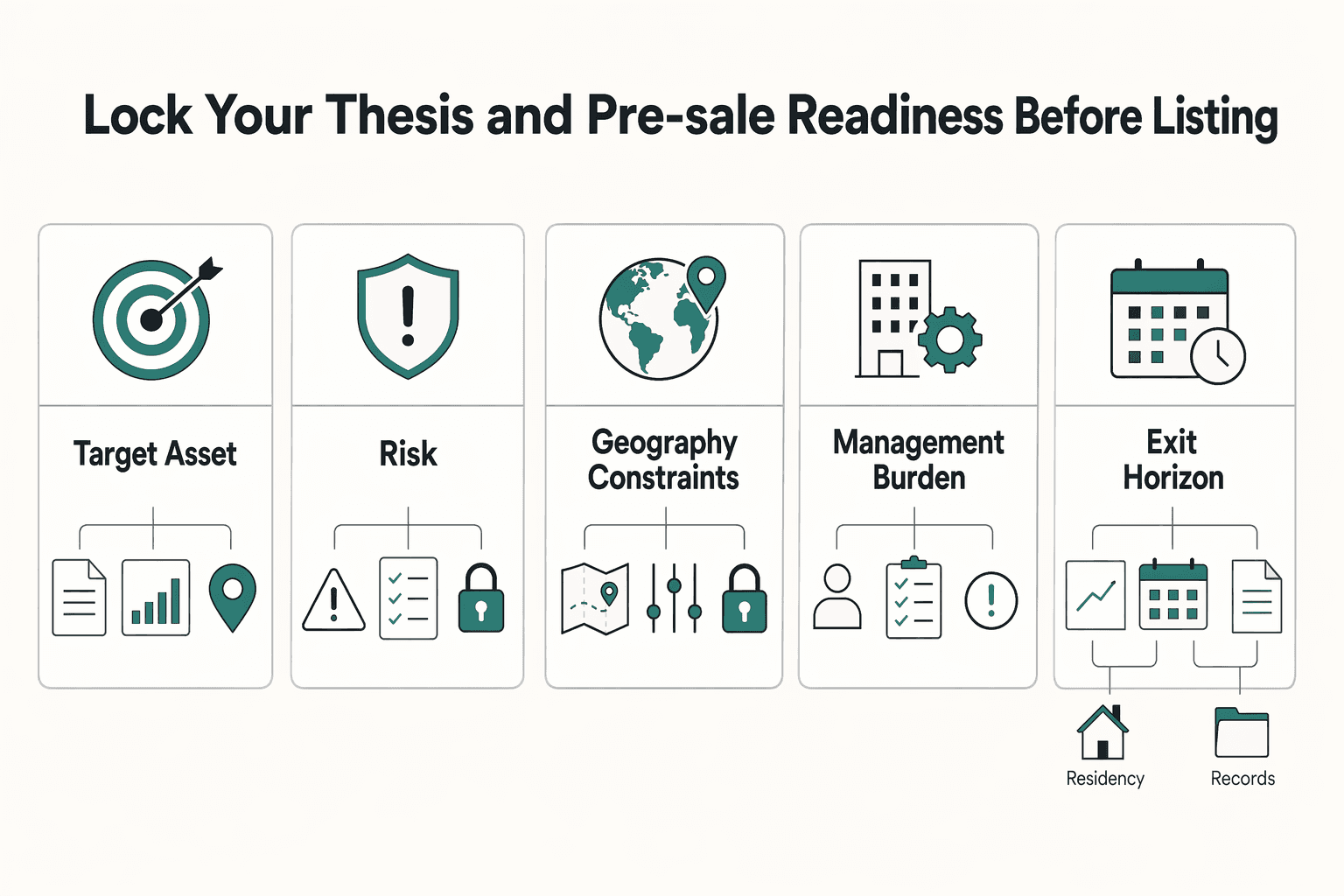

Lock your thesis and pre-sale readiness before listing#

Do not wait until after the sale to decide what you are trying to buy. Write your acquisition thesis before you list, then test whether your process can actually support it.

Frame the decision around:

- Target asset profile: single vs multiple replacements, passive vs operational intensity

- Risk tolerance: stable income orientation vs value-add risk

- Geography constraints: market and lender limits, plus U.S.-only constraints where relevant

- Management burden: self-management vs third-party operations

- Exit horizon: hold period aligned to your broader deferral strategy

Then run this pre-sale readiness checklist:

- Team accountability is documented.

- QI is selected and the exchange-agreement path is ready.

- Exchange intent and file documentation are organized.

- A backup replacement-property pipeline exists before listing.

- The identification process is prebuilt: written, signed, and delivered to a person involved in the exchange.

If you cannot show backup properties, assigned owners, and a vetted QI before listing, delay the exchange decision.

Related: How to Invest in Real Estate as a Digital Nomad.

Before you lock your exchange plan, align your travel and residency facts with your CPA and QI, and use the Tax Residency Tracker if helpful.

Phase 2: The Project Plan - The 180-Day Execution Sprint#

Once your sale closes, the strategy work is over and execution takes over. Your job now is to preserve exchange structure, deliver a valid identification, and close only on a replacement that still makes sense on its own merits.

Lock structure and timeline on day one#

Day one is where many avoidable failures start. Confirm this is still a deferred exchange in substance, not just a sale followed by a later purchase. Work from the written exchange agreement and, if you are using one, confirm that funds are handled under the QI arrangement.

| Item | When | Article detail |

|---|---|---|

| Exchange agreement | Before you move on | Signed exchange agreement |

| Closing statement | Before you move on | Relinquished-property closing statement |

| Funds-control confirmation | Before you move on | Written confirmation of how exchange funds are held or controlled |

| Identification | Within 45 days of transferring the relinquished property | Identify replacement property |

| Receipt | By 180 days or your return due date (including extensions), whichever is earlier | Receive replacement property |

Before you move on, verify and file these core documents:

- Signed exchange agreement

- Relinquished-property closing statement

- Written confirmation of how exchange funds are held or controlled

Then set your timeline immediately: identify replacement property within 45 days of transferring the relinquished property, and receive replacement property by 180 days or your return due date (including extensions), whichever is earlier. Use one shared tracker so you, your QI, and your advisors are working from the same dates.

Send a valid identification and preserve delivery proof#

Identification is not a casual email or a rough property list. It must be a signed written document from you that unambiguously describes the replacement property. It also must be sent before the identification deadline through an allowed method to the transferor of replacement property or another non-disqualified person involved in the exchange.

Keep a complete proof file:

- Signed identification notice

- Timestamped transmission record, whether by email, fax, courier, or hand delivery proof

- Written receipt acknowledgment with recipient identity

If identification or delivery requirements are not satisfied, the replacement property can be treated as not like-kind for exchange purposes.

| Option | When to use | Main risk | Fallback fit |

|---|---|---|---|

| 3-property rule | One primary target plus one or two backups | Thin backup depth if diligence is weak | Strong default for simpler deals |

| 200-percent rule | You want broader optionality across multiple targets | Aggregate FMV cap risk if values are off | Good flexibility without using the most demanding path |

| 95-percent rule | Complex cases with attorney + QI oversight | High execution risk if the regulatory test is missed | Weak casual fallback |

Pressure-test boot before replacement closing#

Late-stage pricing, credits, and financing changes are where many exchanges drift into recognized gain. Boot is non-like-kind value received in the exchange year, and you want to measure it before you sign final papers, not after.

- Cash boot: cash proceeds not reinvested into like-kind real property

- Debt-related boot: relief from debt in the exchange can create taxable gain

Run this check before closing:

- Reconcile sale price, net proceeds, and debt payoff against replacement price and required closing funds.

- Confirm whether any cash returns to you at or after closing.

- Compare relinquished debt payoff with new financing plus cash contributed.

- Have your CPA and QI review draft settlement statements if price, credits, or financing changed.

If numbers move late, get a revised boot estimate before authorizing closing.

Run contingencies early and escalate fast#

Backups only help if they are real options. Pre-vet at least one backup so you can pivot without restarting diligence under deadline pressure.

Escalate the same day to your CPA, attorney, and QI if any of these happen:

- Property description may be ambiguous

- Buyer entity or title plan changes

- Financing comes in lower than expected

- Draft closing statement shows cash back to you

- Primary replacement fails after identification is locked

Use a live execution tracker to keep the handoffs visible:

| Milestone | Owner | Required document | Status | Failure impact |

|---|---|---|---|---|

| Relinquished sale closed under exchange structure | QI (if used) + closing agent | Exchange agreement + closing statement | Open / Done | Structure breakdown or missing audit trail |

| Identification sent | You | Signed written identification | Open / Done | Invalid or late identification |

| Identification receipt confirmed | Valid recipient (often QI) | Acknowledgment or delivery proof | Open / Done | Delivery dispute risk |

| Replacement contract review complete | Attorney + you | Draft purchase contract | Open / Done | Title/entity/assignment errors |

| Boot and financing check complete | CPA + lender + you | Loan terms + draft settlement statement | Open / Done | Unexpected recognized gain |

| Replacement received | Closing team | Final closing statement + deed package | Open / Done | Exchange failure if not timely received |

| Reporting file delivered | You + CPA | Complete Form 8824 support file | Open / Done | Weaker reporting support |

Safe default: if the only remaining replacement is a deal you would reject on its own merits, pause instead of forcing a weak acquisition.

For a step-by-step walkthrough, see How to Rebalance Your Investment Portfolio Without Cashflow Stress.

Phase 3: The Debrief - Post-Acquisition Integration & Long-Term Strategy#

Closing is not the end of the job. Post-close work is where you turn a completed transaction into a supportable file, a clean operating handoff, and a usable record for the next decision.

The available source material for this section is not 1031-specific, so treat the steps below as an internal process checklist, not tax or legal guidance.

Build the post-close handoff file#

Do this immediately, while details are still fresh. Set up one indexed, digital-first folder with a simple table of contents so any reviewer can trace documents, decisions, and opening balances without digging through email.

As a practical checklist, not a legal minimum, include your executed purchase contract and amendments, final closing statement, deed or title evidence, lender package, insurance binder, rent roll, security-deposit records, service contracts, utility transfer confirmations, and property-manager handoff notes. Keep intermediary or exchange-related communications in a separate subfolder.

Before you archive anything, cross-check four fields across core documents: legal owner name, property address, closing date, and money amounts tied to your opening ledger. If names or amounts conflict across title, insurance, management, or banking records, resolve that mismatch before moving on.

Create a verified basis memo#

Do not treat basis as something you can reconstruct from memory later. Treat it as a documented calculation that your advisors verify from current, relevant authority.

| Memo item | Verification status |

|---|---|

| Adjusted basis | Current definition and figures pending tax-advisor or source-record verification. |

| Deferred gain | Current definition and figures pending tax-advisor or source-record verification. |

| Depreciation carryover treatment | Current definition and figures pending tax-advisor or source-record verification. |

| Land, building, and other allocation entries | Current figures pending tax-advisor or source-record verification. |

| Opening depreciation schedule start point | Current figures pending tax-advisor or source-record verification. |

Because basis treatment depends on current authority and your facts, have your advisors verify each memo item before use. Ask your CPA to produce a short memo covering adjusted basis, deferred gain, and depreciation carryover against source records. Your role is to provide clean source documents and flag any open assumptions.

Keep these unresolved fields visible in the memo:

- Adjusted basis definition and amount: Current definition and figures pending tax-advisor or source-record verification.

- Deferred gain definition and amount: Current definition and figures pending tax-advisor or source-record verification.

- Depreciation carryover treatment: Current definition and figures pending tax-advisor or source-record verification.

- Land, building, and other allocation entries: Current figures pending tax-advisor or source-record verification.

- Opening depreciation schedule start point: Current figures pending tax-advisor or source-record verification.

Checkpoint: every amount should tie to a named document or a clearly labeled written assumption.

Assign owners and review checkpoints#

Once the file is built and the basis work is scoped, assign the post-close handoff the same way you handled the transaction itself. Use this as an internal workflow example, not a legal allocation of responsibility.

| Task | Owner | Required document | Review checkpoint |

|---|---|---|---|

| Archive close file | You | Indexed digital folder | Core documents are named, dated, and searchable |

| Transfer operations | You + property manager | Rent roll, deposit ledger, vendor list, service contracts | Opening tenant balances match closing records |

| Confirm title and entity alignment | Attorney + you | Deed, title evidence, entity records, insurance | Ownership details match across title, insurance, management, and banking |

| Prepare basis memo | CPA | Closing package, prior tax workpapers, depreciation records | Each figure ties to a document or labeled assumption |

| Set annual review note | You + CPA + attorney | One-page strategy memo | Open items are labeled as pending advisor verification |

Set guardrails before any next exchange or exit#

Do not assume the next exchange, exit, or transfer will follow the same path just because this one closed. Revalidate the strategy only after current tax and legal review confirms your assumptions for your facts.

Consider pausing and escalating for review when the ownership entity, intended use, financing structure, residency, co-owner structure, or family transfer plans change. These changes are not automatically disqualifying, but they can change your planning path.

Keep estate-planning notes in the file as conditional items, not promises. For any inheritance or basis assumption, mark the current rule as pending advisor verification and refresh it whenever holdings, family structure, or jurisdiction changes.

If you want a deeper dive, read Digital Nomad Tax Survival Guide for 2025.

Conclusion: Executing with CEO-Level Confidence#

A 1031 exchange is a compliance process first and a tax-deferral tool second. It works best when your Section 1031 execution and records are complete, consistent, and defensible.

Lock pre-sale readiness#

Before you sell, make sure eligibility is clear and ownership of the process is clear. Your investment-property position should be documented, and you should have engaged an independent qualified intermediary. Set up one exchange file now so your core records are organized before the transaction starts.

Maintain in-process control#

During the exchange, your goal is a clean written trail of what happened and who handled each required step. Keep transaction records together as events occur. If facts change mid-process, pause and get written clarification instead of relying on verbal assumptions.

Finish post-close integration#

After closing, your goal is a complete handoff file that supports consistent tax reporting and future review. A 1031 exchange delays taxes rather than eliminating them, so post-close documentation is part of risk control, not administrative cleanup.

Decision checkpoint#

Proceed now if your facts and records are clear and complete. Pause and fix documentation if anything is missing or inconsistent. Escalate to an experienced real estate or tax attorney when material facts are unclear.

| Before you call it complete | What to confirm |

|---|---|

| Pre-sale readiness | Investment-property position is documented and the independent QI is engaged |

| In-process control | Exchange actions were recorded in writing and records are consolidated |

| Post-close integration | Your reporting handoff pack is complete and internally consistent |

For related context, see How to Calculate Depreciation on a Foreign Rental Property.

If this exchange is part of a broader cross-border tax workflow, explore Gruv's tools hub.

Frequently Asked Questions

What are the most common 1031 exchange mistakes?

Common failure points include missing the 45-day identification deadline, missing the 180-day completion deadline (or the earlier return due date, taking extensions into account), taking actual or constructive receipt of proceeds, or using identification that does not meet the 3-property, 200%, or 95% rule frameworks. Any of these can cause deferral to fail, and the transaction may be treated as a taxable sale. Receiving cash, debt relief, or other non-like-kind value can also trigger recognized gain. Verify identification timing and delivery proof now. If money flow or debt changes are unclear, talk to a CPA or tax attorney now.

How do you choose a qualified intermediary for a 1031 exchange?

A QI is the safe-harbor party that holds and applies sale proceeds so you do not have actual or constructive receipt. The main risk is straightforward: if you can access proceeds outside the QI structure, the transaction can be treated as a sale instead of a deferred exchange. Before closing, confirm exactly where proceeds will be held and retain the signed QI agreement, wire instructions, and wire confirmations.

What happens if a 1031 exchange fails?

If Section 1031 requirements are not met, the IRS can treat the transaction as a sale rather than a deferred exchange. That means deferral is lost, and gain and basis reporting can change, especially if non-like-kind value was received. Have your CPA recalculate gain and basis from final documents and file consistently, including Form 8824 for each reportable exchange.

Can you 1031 exchange into multiple properties?

Yes, if your written identification fits an allowed framework: the 3-property rule, 200% rule, or 95% rule. The risk is not the number of properties by itself. The real problems are late identification, unclear property descriptions, or falling outside the rule you chose. Send a formal dated written identification within 45 days and keep delivery proof. Escalate to a tax attorney now if facts changed after day 45 or descriptions are ambiguous.

Can I use a 1031 exchange on my primary residence?

No. Section 1031 does not apply to property used solely as a personal residence, and expected appreciation alone does not establish investment intent. Mixed personal and rental use can weaken investment-intent support if records are incomplete. If use is mixed, compile leases, rent records, and personal-use logs, then talk to a CPA or tax attorney before assuming eligibility.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

How to Invest in Real Estate as a Digital Nomad

**Run anything with money and moving parts like an operations system (cash, docs, delegation, and controls), not a "passive income" vibe.** Real life stress-tests weak spots. You change time zones, a client pays late, and something breaks at the worst moment. As the CEO of a business-of-one, your job is to build a setup that keeps working when you are not available on demand.

Tax Implications for a UK Resident Owning a US LLC

When people search **uk resident owning us llc tax**, they often start with the wrong question. You do not win by chasing a clever position. You win by running a compliant system that can handle the way the US and UK classify LLC income differently, with records you can defend.