Quick Answer

To dissolve a US LLC without loose ends, complete both state legal closure in every state where it is registered and federal tax closure for the closing year. Before filing, confirm approval authority, map every registration, log open obligations, and keep proof of state acceptance, final returns, and any IRS business-account closeout steps.

Start Here So You Don't Leave Liability Behind#

Before you file anything, run one checkpoint. If you cannot list every state where your LLC is registered and your federal tax classification, you are not ready to close. Treat the LLC as closed only when both tracks below are complete and documented.

State legal closure means formally dissolving the LLC in each state where it is registered, not just stopping operations. That usually means a state dissolution filing such as Articles of Dissolution. Federal tax closure means finishing the IRS side for the closing year, including the final return and IRS business-account closeout steps. The filing path depends on how the LLC is classified for federal tax purposes.

| Track | Purpose | Owner | Completion evidence to keep | Common failure mode |

|---|---|---|---|---|

| State legal closure | End legal status in each registered state | You | State filing records and acceptance or approval notices | Operations stop, but state dissolution is never completed, so state taxes and filings continue |

| Federal tax closure | Close federal tax obligations for the final year | You | Final return filing records and IRS tax closeout records | State paperwork is filed, but final federal closeout is incomplete |

| Both together | Support a real "closed" decision | You | One organized record set covering both tracks | Items are "done" informally, but records are missing |

Set one rule now: do not mark the LLC closed based on a date or a submitted form alone. Mark it closed only when both tracks have completion evidence.

Build your minimum documentation checklist now, then collect each item as you file: approval record, filing submission record, acceptance or approval record, and federal tax closeout record. For any state-specific requirement not yet confirmed, mark it as pending official verification. State rules vary, so check each state directly. For example, New York sets a 90-day filing window after dissolution and commencement of winding up, with a $60 filing fee.

Need the full breakdown? Read How to Contribute a Personal Asset Like a Car to an LLC.

Gather Your Dissolution File Before You Touch State Forms#

Start by building one dissolution file that lets someone else verify authority, state scope, and unresolved obligations without chasing you for missing context. If the file cannot do that, you are not ready to submit state forms. Use one working file with five sections:

- Governing documents

- Approval evidence

- Entity details

- State registration map

- Open-obligation log

Set up one pre-filing intake file#

Work from current records, not old drafts. Confirm the exact legal entity name and state-issued identifiers exactly as recorded. For example, California filings require the exact name on record and the exact 12-digit Entity (File) Number.

Confirm authority before drafting filings#

Pull authority documents first. Start with the limited liability company agreement, then the organizing documents, and document the close decision in writing. Use the decision rule that matches your setup:

| LLC setup | What to confirm before filing |

|---|---|

| Single-member LLC | The sole owner's authority under your documents, plus signed written consent or a resolution |

| Multi-member, member-managed LLC | The voting threshold and consent method in the agreement; do not assume a simple majority |

| Multi-member, manager-managed LLC | Whether manager approval, member approval, or both are required |

If your documents are silent, apply the state default rule and record exactly what rule controlled. Defaults vary. Delaware uses members owning more than 2/3 unless the agreement says otherwise. California dissolution can be approved by 50 percent or more of voting interests unless governing documents require more.

Map every registered state#

List every state where the LLC is registered, not just the formation state. Include foreign registrations that may require withdrawal or other closure filings.

For each state, your map should show the status, filing office, exact entity name on record, entity number if used, and planned filing. If missing submissions do not stand out immediately, the map is not complete enough.

Log open obligations and separate prep from blockers#

Dissolution starts winding up. It does not mean the LLC is instantly finished. Track taxes, employees, contractor-reporting tasks, known debts, and creditor-facing items before treating owner distributions as complete.

| Lane | What belongs here | Proceed rule |

|---|---|---|

| Required before filing | Governing documents, written approval evidence, exact entity details, complete state registration map | Do not file until complete and consistent |

| Can run in parallel | State form drafting, federal closeout planning, final-return prep based on federal tax classification | You can prepare these now, but do not submit state filings before authority is documented |

| Blocking issues | Unclear approval authority, missing state registrations, identity mismatches, material liabilities with no owner or next action | Pause and fix before filing |

Do not leave items like "taxes later" or "contractors later" without a named owner and next step. You must file a final federal return for the year you close, and the return and forms depend on how the business is classified for federal tax purposes.

Run an independent-review checkpoint#

Before filing, ask someone outside the decision to review the file and answer one question: can they verify authority and filing readiness from the file alone, without follow-up? If not, hold filing until the record is complete.

This is not a legal requirement. It is a practical control to reduce filing-first mistakes, such as discovering missing authority, missing jurisdictions, or unresolved obligations afterward.

If you want a deeper dive, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

Confirm Authority and Choose Voluntary Closure#

Once your file is built, confirm that you are on the right closure path before you file. Do not submit anything until authority, approval method, and the final decision record all match your governing documents.

Step 1. Confirm which path you are on. Use voluntary closure only when the owners, through the proper governing person, are initiating and approving the shutdown. Administrative dissolution is different. The state can impose it for compliance failures, such as missed annual-report obligations in some states. If your status is already administrative, pause the owner-driven closeout process and follow that state's cure or reinstatement process instead.

Step 2. Confirm who can approve and which rule controls your case. Start with the operating agreement. If it defines the trigger or approval mechanics, follow it. If it is silent, document the state default rule you are relying on.

- Single-member LLC: confirm the sole owner's authority and document that approval in your decision record.

- Multi-member, member-managed LLC: confirm the actual threshold and consent method. Do not assume one universal rule.

- Multi-member, manager-managed LLC: confirm whether managers have decision authority under your operating agreement and the applicable state default rule.

- If management structure is unclear: document which rule controls. For example, some statutes default to member-managed unless the agreement says manager-managed.

| Requirement | Where to verify it | Evidence to save |

|---|---|---|

| Who has authority to approve dissolution | Operating agreement first, state default rule if silent | Copy of controlling provision or statute note |

| Required vote or consent method | Operating agreement, relevant state filing or form instructions | Signed consents, minutes, written resolution, vote record |

| What event triggers dissolution | Operating agreement, applicable statute | Short decision memo tying the trigger to your facts |

Step 3. Run a pre-filing consistency check. Before you submit anything, confirm three points: the approver identity and capacity, the exact entity details in the filing draft, and the final approval artifact. If any of those conflict, stop and fix it. Save the final approval artifact and the filing receipt or confirmation together in your proof pack.

Split the Work Between State and Federal From Day One#

As soon as authority is confirmed, split the shutdown into two tracks and run them in parallel. If you treat the state filing as the whole job, you can still leave federal returns, employment tax filings if you had employees, or EIN handling open.

Define both tracks before any filing#

Use exact labels in your closure file:

- State closeout: legal dissolution or cancellation filings, plus related state obligations, in every state where your LLC is registered.

- Federal closeout: IRS-side shutdown work, including your final return, related federal forms, required employment tax returns if you had employees, and EIN business-account handling. The IRS does not cancel an EIN. It can deactivate it after required returns and taxes are handled.

| Track | Primary owner | Trigger to start | Completion evidence | Common handoff failure |

|---|---|---|---|---|

| State closeout | State filing lead | Signed approval record | State acceptance artifact when available, not only a submission receipt | Filing is submitted, but accepted or stamped proof is never saved |

| Federal closeout | Tax lead | Signed approval record and confirmed federal tax classification | Final return package filed, plus EIN closeout record when applicable | Team assumes state dissolution also closes IRS obligations |

| Cross-track control | Proof-pack owner | Any status change in either lane | Cross-updated log with linked proof in both lanes | One lane is marked complete while the other is still open |

Sync both tracks at every status change#

Use one operating rule for your team: treat a task as complete only when proof is saved, and where practical, track acceptance separately from submission. Cross-update both tracks whenever an item is:

- submitted

- accepted

- corrected and refiled

- marked not applicable, with a short reason

If Form 966 is relevant to your federal classification, track it as a separate deadline item. Form 966 applies to corporations, not every LLC, and is due within 30 days after the dissolution or liquidation resolution is adopted.

Keep one note per jurisdiction#

For each state, keep a short note in this format: form, filing office, prerequisite check, submission artifact, acceptance artifact. If any point is still unverified, enter: Current state-specific requirement pending official verification.

| State | Filing | Noted requirement or evidence |

|---|---|---|

| New York | Articles of Dissolution with the Department of State | Within-90-days timing rule; $60 fee |

| Texas | Certificate of Termination after winding up | Comptroller tax certificate required; $40 filing fee |

| Delaware | Certificate of Cancellation | Taxes paid before filing; stamped "Filed" copy returned as acceptance evidence |

This keeps state-specific details from drifting. The examples above show the level of detail you want in each note.

For a step-by-step walkthrough, see What is the 'Corporate Veil' and How Does an LLC Protect It?.

File the State Dissolution Documents in the Right Order#

Order matters here. In some states, sequence is mandatory. For example, in California, Form LLC-3 must be filed before or with LLC-4/7 when the unanimous-vote box is not checked. File out of sequence and you can end up with a rejection, an LLC that still appears active, or a foreign registration left open after the home-state shutdown.

Use this routing rule: your home state handles dissolution of the LLC itself, and each foreign registration state handles surrender or withdrawal of that state authority. Those are separate filings with separate prerequisites, and foreign withdrawal or surrender is not the same as dissolving the LLC in its home state.

| Sequence | What you confirm first | Home-state (domestic) row | Foreign-state (withdrawal/surrender) row | Do not proceed without |

|---|---|---|---|---|

| 1. Route | Correct form and office | Current dissolution form name, filing office, fee, and processing options pending official verification | Current withdrawal or surrender form name, filing office, fee, and processing options pending official verification | Verified form and office for that state |

| 2. Prerequisites | Blocking conditions cleared | Current state-specific winding-up, tax, and approval prerequisites pending official verification | Current state-specific tax or withdrawal prerequisites pending official verification | Logged proof that blockers are cleared |

| 3. Submit | Method, signer, and payment | Current filing method, signer, payment method, and submission artifact pending official verification | Current filing method, signer, payment method, and submission artifact pending official verification | Submission copy and payment proof |

| 4. Accept + verify status | Acceptance artifact and public record check | Current acceptance artifact and status-check method pending official verification | Current acceptance artifact and status-check method pending official verification | Acceptance evidence and updated status capture |

Treat each state as its own queue. One accepted filing does not validate the next state's form, fee, timing, or prerequisite rules.

Processing-speed decision (after prerequisites are cleared)#

| Option | Use it when | What to watch |

|---|---|---|

| Standard | No hard dependency on acceptance date | Lowest cost, but you still need full proof capture |

| Expedited | You need accepted status by a specific date tied to a real obligation or closing dependency | Extra fees apply and vary by state. For example, New York offers optional expedited handling including $25 for 24-hour processing, and Delaware lists same-day ranges and one-hour service fees |

Expedited handling changes speed, not correctness. It will not fix a wrong form or a missing prerequisite.

Archive immediately for each state#

- submitted filing copy

- payment proof

- acceptance evidence, such as an acknowledgment or receipt PDF

- updated public-status capture for that state record

If any one of these is missing, do not mark that state as closed. Related: The 'Profit First' Method Part 2: Setting Up Your Bank Accounts.

Wind Up Operations Before You Distribute Anything#

Treat owner payouts as the last step, not the next step. During the wind-up period, your LLC continues only to complete closure work. An open obligation is any debt, duty, or liability not yet paid, settled, or adequately provided for. A distribution hold means no owner payout until those items are resolved or properly reserved.

State dissolution filings start the process, but separate closeout work may still remain for contracts, tax duties, customer commitments, and recurring charges. Winding up is active work: close obligations first, then distribute what is truly left.

Stop new work and record the wind-up start#

A practical first move is to stop creating new obligations while the entity remains active for wind-up tasks:

- Stop accepting new client work, orders, deposits, and commitments.

- Stop signing new contracts, renewals, or purchase obligations.

- Keep required compliance tasks active until closure steps are complete.

- Record the wind-up start date and save timeline evidence.

Keep proof of that start point in your closure file: internal approval, dated notes, paused-intake evidence, and any notices sent to clients, staff, or vendors. If timing is questioned later, this record helps you.

Build an obligations log that controls payouts#

Use one log as a decision tool, not a loose checklist. If any item is unresolved, owner distributions stay on hold.

| Log field | What it should show |

|---|---|

| Open obligation | The exact debt, promise, claim, filing, refund, or cancellation task |

| Status | Open, in progress, closed, or reserved |

| Owner | The person accountable for closing it |

| Dependency | What must happen first, such as final invoice, signoff, or acceptance |

| Proof link | Where the supporting evidence lives |

Tax closeout belongs in this same log. A final return for the closing year and any outstanding tax items must be completed before EIN deactivation, so unresolved tax work remains a payout blocker.

Close commitments in a practical sequence#

Use a practical sequence to reduce risk, then verify state-specific requirements and timing. The exact order can vary by state law and your operating agreement.

- Close revenue and customer commitments.

- Close recurring vendor commitments.

- Close related registrations, permits, licenses, and business names.

This helps you avoid two common failures: canceling too early and breaking needed closeout tasks, or canceling too late and continuing charges and filing exposure.

Run a release gate before any distribution#

Do not distribute because the balance looks clean. Distribute only when every gate is a documented "Yes."

| Release gate | Ready to Distribute: Yes | Ready to Distribute: No |

|---|---|---|

| No open liabilities | Debts are paid or adequately provided for | Any debt, claim, tax item, or reserve question is still open |

| No unresolved customer obligations | Deliverables, refunds, and access commitments are complete | Any customer promise is pending, disputed, or undocumented |

| No active recurring commitments | Recurring services are terminated or scheduled with proof | Auto-renewals, recurring bills, or active service contracts remain |

| All closure proof in one audit-ready folder | Log, notices, confirmations, receipts, and cancellations are centralized | Evidence is missing or scattered |

If any row is "No," keep the distribution hold in place.

Related reading: How to Create an Accountable Plan for a Single-Member LLC.

Close Taxes Based on How Your LLC Is Taxed#

Tax closeout starts with one control point: your tax classification in the closing year. That classification determines the final federal filing path, so this stays a distribution blocker until it is complete and documented. Do not start with forms. Confirm classification first, document it, and then build the filing list from that decision.

Document classification before building the tax list#

Create a short classification memo in your closure file so everyone is working from the same tax treatment. This is an internal control, not an IRS form. Include:

- Closing year

- Federal tax classification used for that year

- Who confirmed it

- Supporting records

- Proof location in the closure file

Use default treatment unless you have an election record showing otherwise. Your standard is simple: a second reviewer should be able to confirm the tax path, the confirmer, and the proof location in under a minute.

Use one tax closeout table for federal and state work#

Keep federal and state tasks in one table so handoffs stay clean and dependencies stay visible.

| Task | Decision or applies when | Owner | Status | Dependency | Proof location |

|---|---|---|---|---|---|

| Final federal income tax return | Required. Use the path tied to the closing-year classification and mark as final where applicable. | Classification memo complete | |||

| Partnership final return check | Required if taxed as a partnership, check the final return box. | Final books closed | |||

| Corporate final return check | Required if taxed as a corporation, check the final return box. | Final books closed | |||

| Schedule SE review | Review if closeout runs through the owner return, include if net earnings are $400 or more. | Final owner-level numbers ready | |||

| Final employment tax tasks | Required if you had employees: final wages, deposits, and employment-tax reporting. | Final payroll processed | |||

| Contractor reporting review | Review if you paid contractors in the closing year, verify current-year 1099-NEC instructions before close. | Vendor totals finalized | |||

| Form 966 applicability gate | Mark Required or Not applicable with rationale. Required when taxed as a corporation and a dissolution or liquidation plan was adopted, not an LLC-wide default. Do not use for deemed liquidation. Current filing deadline pending official verification. | Classification memo and dissolution resolution reviewed | |||

| State income, franchise, or sales tax closeout | Review each state where you were registered or filing, state tax closeout is separate from dissolution acceptance. | State nexus list confirmed | |||

| State payroll closeout | Required where payroll existed, verify each state rule and due date before closing the row. | Final payroll date confirmed |

If a row is complete, the proof column should link to real evidence: filed return, confirmation, receipt, payment record, or portal export.

File first, archive proof second, remove access last#

Do not remove payroll or tax-portal access before required filings are done and the evidence is archived. Use this order:

| Order | Action | Key note |

|---|---|---|

| 1 | File required federal and state tax items | Returns and taxes must be complete first |

| 2 | Archive filing and payment evidence in the closure file | This sequence supports EIN account deactivation later |

| 3 | Export final-period and year-end reports from payroll and tax portals | Do not remove payroll or tax-portal access before this is done |

| 4 | Verify outstanding returns and balances are cleared | Check this before removing or reducing access |

| 5 | Remove or reduce access | Do this only after the earlier steps are complete |

Follow that order. This sequence also supports EIN account deactivation later. Returns and taxes must be complete first.

Run a final verification check before marking tax closeout complete#

Before you mark this track done, verify that the memo, table, and proof file all line up. Check:

- Classification memo matches the filing path used.

- Required final returns are filed or clearly marked not applicable.

- Form 966 is marked Required or Not applicable with rationale and a verified deadline note.

- Employment-tax and contractor-reporting reviews are closed where applicable.

- State tax rows are closed for each state with filing duties.

- Proof is archived before access is removed.

Tax closeout is complete only when an independent reviewer can verify the full record without reconstructing it.

For related cross-border context, see How Canadians Can Set Up a US LLC Without Tax Surprises and the FBAR calculator.

Shut Down Payroll, Benefits, Banking, and EIN Cleanly#

After the tax path is set, handle shutdown as four separate tracks: payroll closeout, benefits decisions, banking and card closure, and EIN-related IRS closure. They connect, but none of them proves the others are done.

Build one auditable shutdown tracker#

Use one tracker across all four tracks, with separate row groups so blockers stay visible. The goal is to prove each track is complete with dated evidence, not assumptions.

| Task | Owner | Status | Dependency | Proof location |

|---|---|---|---|---|

| Final compensation obligations processed | Final work dates confirmed | |||

| Final federal, state, and local tax returns filed (marked final where applicable) | Final tax return path confirmed | |||

| Any required state tax clearance confirmed before dissolution filing | State requirements verified | |||

| Financial account closure readiness reviewed (checks cleared, automatic payments handled) | Final account activity reconciled | |||

| Employee records and payroll reports exported before access removal | Final filings submitted | |||

| Contractor reporting review completed | Vendor totals finalized; current reporting threshold pending official verification | |||

| EIN-related IRS closure step reviewed and actioned | Final tax return path completed; current IRS closure requirements pending official verification |

Completion standard: a second reviewer can open one proof item per completed row and confirm what was done, when, and by whom.

Decide benefits termination vs transfer or continuation before revoking access#

Treat benefits as a separate decision block, not a payroll footnote. For each plan, decide terminate versus transfer or continuation first. If notices or final remittance steps apply, handle them before shutting off access. Capture for each plan:

- Plan name and vendor

- Decision: terminate or transfer or continue

- Required notices pending official verification of current requirements

- Final remittance or contribution status

- Coverage end date or transfer effective date

- Proof location for notices, remittance confirmation, and vendor acknowledgment

Keep payroll, broker, and provider access until required notices, if any, are sent, final amounts are handled, and records are saved.

Close banking and cards only after settlement risk is cleared#

Close financial accounts only after checks are cleared and automatic payments are handled, and after you review any pending deposits, returns, disputes, or auto-debits. Closing too early creates avoidable cleanup risk and weaker proof. Log the decision criteria in the file before closure:

- Last expected inflow

- Last expected debit

- Open disputes

- Linked subscriptions or auto-payments

- Refund or charge activity still in motion

Then archive the closure confirmation, closure date, final statement, and zero-balance evidence in the proof pack.

Keep contractor reporting and EIN closure as explicit final gates#

Close contractor reporting only after totals, filing duty, and proof are documented. Do not hardcode a threshold until verified. Current reporting threshold pending official verification.

Keep EIN-related IRS closure as its own gate, separate from state dissolution. Mark it complete only after you verify current IRS closure requirements and archive submission or confirmation evidence.

Handle Cross-Border Loose Ends Before You Walk Away#

Do not close this file until cross-border reporting is resolved. This section is complete only when you have filing proof or a written non-applicable conclusion for each item. Form 8938 and FBAR are separate tests with separate outcomes. Run both analyses, document both conclusions, and archive both.

Build a foreign-asset review table before final archive#

Start with a full inventory of foreign accounts and other specified foreign financial assets tied to the closing year. Then map each item to an owner, jurisdiction, reporting track, and proof location.

Tie this review to the LLC's federal tax treatment, since the closeout path depends on whether the LLC is treated as a partnership, corporation, or disregarded entity.

| Asset | Owner | Jurisdiction | Reporting track | Evidence location |

|---|---|---|---|---|

| Foreign bank account | LLC or owner | Form 8938 / FBAR / not applicable | ||

| Foreign brokerage or investment account | LLC or owner | Form 8938 / FBAR / not applicable | ||

| Other specified foreign financial asset | LLC or owner | Form 8938 / not applicable | ||

| Signature-authority-only account | LLC representative or owner | FBAR / not applicable |

Completion check: each known item has a row, owner, jurisdiction, reporting track, and evidence path. Do not exclude an account just because it produced no taxable income.

Test Form 8938 on its own path#

Form 8938 stands on its own and follows filer-profile rules. Confirm whose return is being closed, whether the filer is a specified person, and which profile-specific threshold applies. Do not hardcode one universal threshold. Use this note structure and leave unresolved fields marked pending official verification:

- Filer profile used: individual / specified domestic entity / other, pending official verification

- Filing status and residency profile pending official verification

- Threshold logic: current threshold pending official verification

- Income tax return required for the year: yes / no

- Conclusion: Form 8938 required / not required

- Proof: return workpapers, valuation support, draft or filed form

If no income tax return is required for the year, record that and mark Form 8938 not required with dated support.

Test FBAR separately and keep a separate conclusion#

FBAR is a different filing path from Form 8938, so document it separately. Use two explicit criteria:

- Did you have financial interest in, or signature or other authority over, at least one foreign financial account?

- Did aggregate foreign-account value exceed

$10,000at any point in the calendar year?

If both are yes, treat FBAR as required. Keep this result separate from your Form 8938 conclusion.

Also track timing and proof in the file. FBAR is due April 15 after the reported calendar year, with an automatic extension to October 15. Save value support, aggregation workpapers, and filing confirmation when required.

Apply an archive gate before you mark cross-border closed#

Close cross-border only after each reviewed item has a final filing result or a written non-applicable rationale, plus retained records. Before final archive, confirm:

- Every identified foreign item appears in the review table.

- Form 8938 has a completed, profile-based written conclusion.

- FBAR has a completed written conclusion using authority or interest plus the

$10,000aggregate test. - Required filings are completed and proof is stored.

- Non-applicable outcomes have dated rationale and retained workpapers.

If any row still depends on threshold verification, ownership clarification, or missing statements, keep this section open.

Avoid the Mistakes That Reopen a Closed Business#

Do not treat the stop-work date as the close date. Use three labels in your file so status stays clear. Use state acceptance for your documented state acceptance checkpoint. Use administrative dissolution only when discussing that separate Georgia category, not as your internal closeout label. Use closure complete for your internal sign-off only after state acceptance is documented and remaining legal and tax items are finished or recorded as not applicable.

| Mistake | Trigger | Risk if missed | Recovery action | Required evidence |

|---|---|---|---|---|

| Stop operating and assume closure | Activity slows and the team moves on before filing review finishes | You sign off without acceptance proof | Track the filing through acceptance before changing status | Filing receipt, acceptance confirmation, dated status update |

| Pause compliance too early | Annual registration window arrives while the LLC still exists on state record | Required state work remains open in your file | Continue state compliance through the acceptance date, close or document any leftover items | Filed annual registration, if due, or dated non-applicable memo |

| Treat closure as one event | State acceptance is treated as the end of all work | Non-state legal or tax tasks are left unresolved | Keep legal and tax tracks separate until each has a finished result | Open-items log, filed proofs, dated non-applicable conclusions |

Mistake 1. Why it happens. What you do now. Proof required. State processing is not instant, and timing varies with workload. In Georgia, online filings are typically reviewed in 7 to 10 business days and paper filings in 15 business days. Slower periods are noted in late December through January and around late March, late June, and late September. Treat "submitted" as in progress, not complete. Keep the receipt and acceptance artifacts together, plus a dated note showing when you updated status.

Mistake 2. Why it happens. What you do now. Proof required. People often assume filing paperwork cancels routine obligations immediately. In Georgia, annual registration is required by law and confirms the entity still exists. For Georgia LLCs, annual registration is filed between January 1 and April 1 of the year after the initial filing, then in that same window each year thereafter. If the entity is still on record during that window, keep this item active until your acceptance checkpoint is documented. Save the filing proof or a dated memo explaining why it was not applicable.

Mistake 3. Why it happens. What you do now. Proof required. Teams often treat state acceptance as the finish line for everything. Instead, keep one open-items page and force each remaining legal or tax task to end in either completion proof or a dated non-applicable conclusion. Do not archive early. Keep the final checklist, supporting workpapers, and completion notes in the same closure file.

Before final archive, confirm all are true:

- State acceptance is documented in the file.

- Any state obligations due before acceptance are completed or documented.

- Legal and tax items are completed or marked not applicable with dated support.

- Any late cleanup has a note, proof location, and completion date.

This pairs well with our guide on How LLC Owners Separate Business and Personal Finances.

Build a Proof Pack That Survives Audits and Disputes#

Build one closure packet as your complete evidence set for legal closure, tax closeout, and account shutdown. If a notice or dispute appears later, this packet should let you prove status quickly.

Federal and state closeout run in parallel, so completion in one lane does not complete the other.

Use this completion standard. State records are complete only with acceptance evidence. Tax records are complete only with both filing and payment proof. EIN closeout is complete only with your outbound request plus any IRS response.

| Artifact category | What it proves | Completion signal (filed vs accepted) | Where it is stored |

|---|---|---|---|

| State dissolution or cancellation records | The state recorded the entity closeout | Complete only with a state acknowledgment, filing receipt, or filed-stamped copy, not just a draft or submission screenshot | Closure packet > State > home state / foreign registrations |

| Federal tax closeout records | You filed the correct final return for the LLC's tax classification and handled related tax obligations | Complete only when filing proof and payment proof are both present | Closure packet > Tax > Federal |

| EIN deactivation records | You requested IRS business account deactivation after required filings and payments | Complete only when the outbound letter is saved and any IRS reply is attached if received | Closure packet > IRS > EIN |

| Operational account shutdown records | Operational accounts were closed | Complete when provider confirmation or final statement is saved | Closure packet > Operations |

Keep one closure log and require a retrievable proof link for every line#

Treat the log as your index. For each line item, record artifact name, status, date, owner, and a retrievable file path or link. If a line does not map to a saved PDF, notice, statement, or email, mark it incomplete. Also separate filed from accepted. Evidence format varies by state, so store the exact acceptance artifact your filing office issues.

Match tax proof to tax classification and payment status#

Your tax packet must match how the LLC was taxed, because the final return type depends on business type. Keep the final return, filing confirmation, payment proof, and any classification-specific forms together.

Only include Form 966 when the entity is treated as a corporation for federal tax purposes and a dissolution or liquidation plan was adopted. If so, track its 30-day filing deadline from plan adoption. For contractor reporting, do not hardcode thresholds in evergreen text. Note that you verified the current filing-year instructions, then record the requirement you applied.

Track EIN deactivation separately, then set retention by document purpose#

Do not treat EIN closeout as EIN cancellation. Keep the outbound IRS letter, including EIN, legal name, address, reason, and EIN assignment notice if available, and attach any IRS response received.

Assign retention by what each record proves, and add a short reason retained note to each category. Use purpose-based periods in your log, for example:

| Record category | Retention baseline | Reason retained (example) |

|---|---|---|

| Employment tax records | At least 4 years | Supports employment tax filings and payments |

| Payroll records | At least 3 years | Supports payroll history and wage compliance |

| Wage computation support | 2 years | Supports how wages were calculated |

| Personnel or employment records | 1 year | Supports employment recordkeeping obligations |

Your packet is complete only when every status line maps to retrievable proof and each retained record shows why it is still kept.

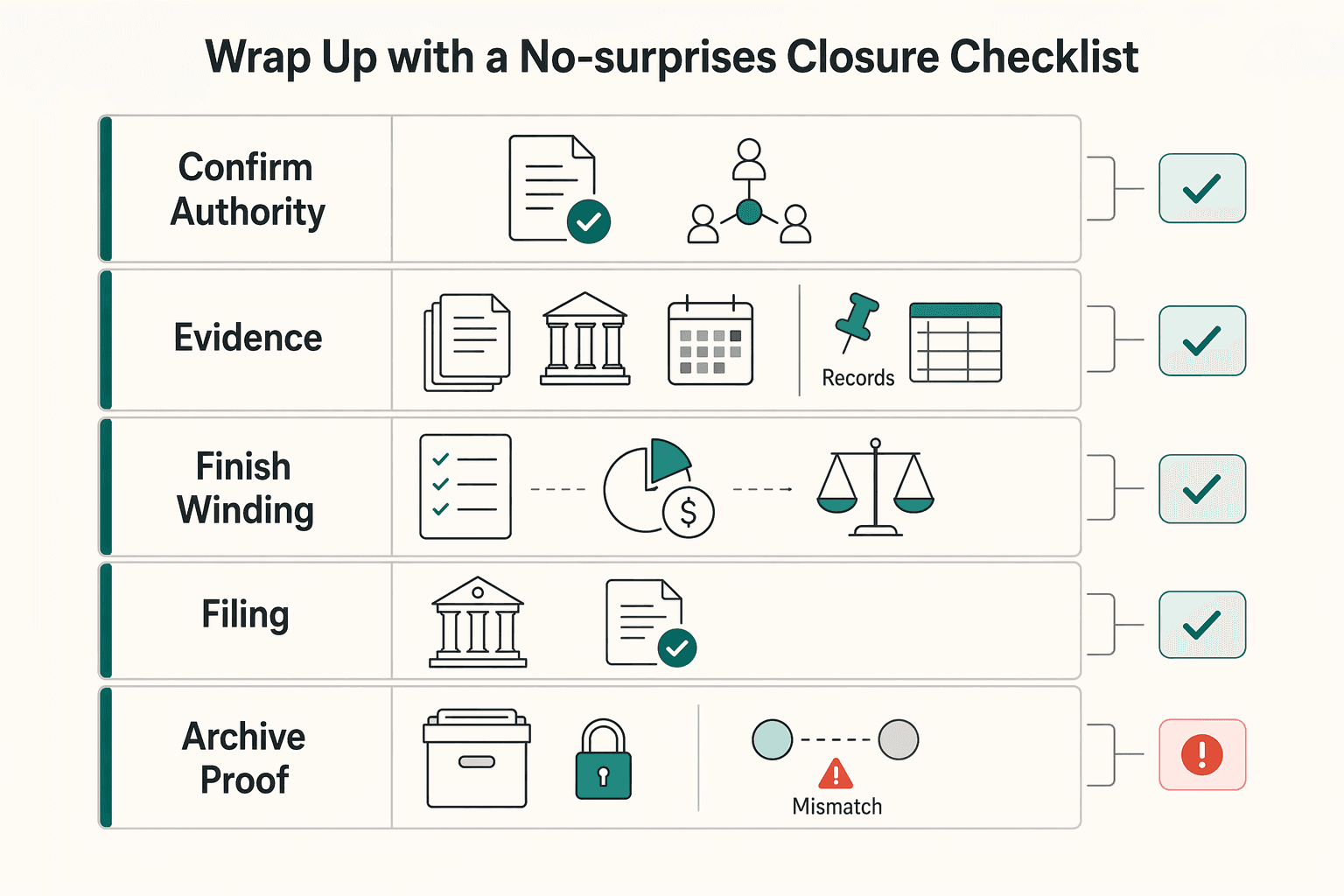

Wrap Up With a No-Surprises Closure Checklist#

Use this as your final go/no-go gate: if you cannot produce the proof artifact, the LLC is not closed for your purposes. "Complete" means evidence-backed completion, not a task marked done.

Because an LLC can continue indefinitely unless it is formally terminated, and because process details follow your operating agreement and formation-state LLC law, treat this checklist as an execution control, not admin cleanup. Run each checkpoint and close it only when the required evidence is in your file.

| checkpoint | required evidence | owner | status |

|---|---|---|---|

| 1. Confirm authority | Operating agreement clause, plus documented member approval (for example, signed consent, minutes, or resolution). If the agreement is silent, record the formation state statutory default rule used | ___ | Closed only when the approval basis and approval record are both in file |

| 2. File state dissolution documents | Accepted filed copy of the jurisdiction-required dissolution form (for example, Articles or Certificate of Dissolution), plus filing receipt and acceptance or status confirmation. Current state dissolution requirement pending official verification | ___ | Closed only when filing is accepted, not just submitted or paid |

| 3. Finish winding up | Evidence of winding up affairs, including creditor or obligation handling and liquidation or distribution records where applicable | ___ | Closed only when wind-up evidence shows no unresolved business obligations |

| 4. Close tax filings | Evidence that final tax returns were filed, plus filing proof. Current tax clearance requirement pending official verification for classification-specific items | ___ | Closed only when final return proof is saved |

| 5. Document IRS notification | Evidence of IRS notification action where applicable, plus submission, mailing, or response proof | ___ | Closed only when the action taken is documented, not just planned |

| 6. Archive the proof pack | Indexed closure folder containing approval, filing, tax, and wind-up records in one retrievable location | ___ | Closed only when another person can retrieve the full file without extra explanation |

If authority is unclear, records conflict, or a jurisdiction requirement is uncertain, escalate before moving forward. Keep one operating rule for this checklist: if any artifact is missing, contradictory, or unresolved, closure stays open until it is resolved.

When you are ready to standardize your next compliance workflow, browse Gruv tools.

Frequently Asked Questions

What is the first legal step to dissolve a US LLC?

The first legal step is to confirm who has authority to approve dissolution under your operating agreement and state LLC law. Save written approval evidence before filing. If authority is unclear or owners disagree, pause and escalate.

Do I need to file with the state, the IRS, or both?

Usually both. State closure and federal tax closeout are separate tracks, and state acceptance does not finish IRS obligations or deactivate the IRS business account. Run both tracks in parallel and verify each state separately if the LLC was registered in more than one state.

What is the difference between dissolution and winding up?

Dissolution starts the legal closure process. Winding up is the follow-through work of settling obligations, filing final returns, closing accounts, and only then distributing what remains. Stopping operations is not the same as ending the entity, and some states separate notice from final termination.

Do single-member and multi-member LLCs follow different approval steps?

Sometimes. The controlling rules come from your operating agreement and state law, so confirm the correct approver, approval date, and authority basis in your file. If ownership changed, a member is inactive, or your documents conflict, do not guess.

Do I need to file Form 966 for an LLC?

Usually not. Form 966 applies when the LLC is taxed as a corporation and a dissolution or liquidation plan was adopted, not to every LLC. Verify federal tax classification first, then decide whether it applies.

Can I just stop operating and skip filing dissolution paperwork?

No. Stopping operations does not end the LLC's legal status or filing obligations by itself. You still need accepted state closeout filings and federal closeout steps, and foreign registrations may require separate surrender or withdrawal filings.

What final tax filings and payroll forms are usually required?

You must file a final federal return for the year you close, and the exact return package depends on the LLC's federal tax classification. If you had employees, complete final payroll tax filings, and if cross-border reporting may apply, review Form 8938 and FBAR separately. Keep proof of the filings, and mark Form 941 as final when applicable.

Try a related tool

Sarah focuses on making content systems work: consistent structure, human tone, and practical checklists that keep quality high at scale.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

The 'Profit First' Method Part 2: Setting Up Your Bank Accounts

Most freelancers who try Profit First open a few extra bank accounts and call it done. That's the wrong move.

How to Choose Airline and Hotel Loyalty Programs for a Relocation

For a move, loyalty should reduce friction, not become a side project. You are not choosing airline and hotel programs for bragging rights or theoretical value. You are choosing them because relocation exposes weak coverage, weak flexibility, and outdated assumptions faster than almost any normal trip.