Quick Answer

Create a freelance freedom fund by turning savings into a repeatable payment-event system. Define the fund as a dedicated business buffer, set clear targets, and allocate money from every paid invoice into tax reserve, freedom fund, and operating cash in the same order each time. Pair this with stronger terms at intake and a written exception workflow for late pay, holds, and disputes.

Stop "saving when you can": build a Freedom Fund that pays you back on every invoice#

Stop relying on discipline and switch to a percentage-based, per-payment system that saves automatically when you get paid. If you freelance, you're running a business-of-one. Your job is to install financial rules that keep working even when income is messy. A "save whatever is left" approach fails because your calendar and your cash flow rarely line up.

Freelancers deal with unpredictable income. As one 1099-focused retirement guide puts it: "You don't always know how much money you'll make month to month." So your savings plan has to flex with reality, not fight it.

Step 1: Define your "Freedom Fund" as a behavior, not a mood#

Treat your Freedom Fund as a dedicated savings bucket you fund every time money hits your account. You do not "save when you can." You save when you get paid.

This works because it scales up and down automatically: "Save a percentage of your income each time you get paid, rather than a fixed dollar amount." A practical starting range: aim for 10-20% of every check, depending on your savings goals and budget.

Use this decision table to choose the approach you can actually run:

| Approach | What you do | Works well when | Breaks when |

|---|---|---|---|

| Fixed dollar saving | Move the same amount monthly | Stable salary | Income fluctuates, payment timing shifts |

| Percentage per payment | Save a % every time you get paid | Freelance finance, variable months | You skip the transfer "just this once" |

Step 2: Install the "get paid, then allocate" routine#

Run this by default every time you get paid:

- Action: Pick your Freedom Fund percentage (start in the 10-20% range).

- Action: Set up small automatic transfers so the move happens without willpower, and start small if needed. Consistency matters.

- Verify: After the transfer, your checking balance still covers near-term obligations. The goal is to stay consistent without straining your cash flow.

- Record: Add a simple memo in your notes or ledger: date, payer, amount, Freedom Fund transfer.

Hypothetical scenario: a client pays earlier than expected. Instead of "celebrating" and spending it, you run the same split. Your system turns a good month into runway, not lifestyle creep.

Copy/paste checklist (run on every payment)

- Payment received (not just invoiced)

- Freedom Fund transfer runs automatically (or you trigger it same-day)

- Percentage matches your current savings goals

- Memo recorded for clean tracking

Define the Freedom Fund (operational definition, not vibes) + what it is NOT#

In this guide, a Freedom Fund is a dedicated bucket of business savings that you define clearly and protect with simple boundaries.

Use the term "Freedom Fund" as an operational label, not a mood. To keep it useful, decide what it's for, how money gets in, and what makes you leave it alone. Otherwise it turns into a fuzzy pile of money you raid for random wants, then regret when cash gets tight.

Step 1: Choose an operational definition you can enforce#

Pick a definition that matches your real life and helps you make consistent decisions.

Here's a simple working definition you can copy into your docs:

- Freedom Fund (working definition): "A separate savings bucket for my freelance business that I keep available for business continuity when my cash plan gets squeezed."

Hypothetical scenario: a client pushes back on an invoice right as you need to renew a critical subscription. Without a buffer, you might feel pressure to make rushed tradeoffs. With a defined fund, you have more room to respond calmly and stay consistent.

Step 2: Clarify what you mean by "Freedom Fund" (in writing)#

Avoid confusion by putting your boundaries somewhere you will actually see them. You're not buying a vibe. You're installing a system.

If you want this to stay operational, decide and write down answers to questions like:

- How it gets funded: Will you contribute on a schedule, per payment, or only when you have surplus?

- What it can be used for: What counts as "business continuity" for you, and what doesn't?

- What happens after you use it: Do you rebuild it on a timeline, or pause other spending until it's back where you want it?

Quick self-check: If you can't explain, in one sentence, why you moved money out of the Freedom Fund, your boundaries probably are not clear enough. Tighten them and keep going.

What to prepare before you start (10-minute setup + the minimum data you need)#

Prepare a basic cashflow snapshot and a simple plan so the Freedom Fund runs on reality, not optimism. You're aiming for visibility into what comes in, what goes out, and what's actually left to work with.

Now that you've defined the fund and written governance rules, you need a minimum set of inputs to operate it cleanly. This prep keeps your savings goals grounded in what actually happens when payments arrive later than you expect.

Before you start (quick prerequisites)#

| Preparation | Examples | Used for |

|---|---|---|

| Recent income records | Invoices, bank deposits, or a spreadsheet | See what you earned, when you got paid, and what tends to be predictable vs. lumpy |

| Recurring expenses | A list of recurring expenses you must pay each month | Identify fixed, non-negotiable costs your cash has to cover |

| One page plan | Doc, notes app, or spreadsheet | Name must-pay expenses and your Freedom Fund contribution rule |

Step 1: Build a quick cashflow snapshot (observed, not guessed)#

Pull together a recent slice of your income so you can see:

- What you earned

- When you got paid

- What tends to be predictable vs. lumpy

Keep it simple. The goal is to stop relying on vibes and start relying on records.

Step 2: List "keep-the-lights-on" costs#

Write down your fixed, non-negotiable costs, especially anything that would cause problems fast if you missed it. This is the baseline your cash has to cover before you decide what's safe to set aside.

Anchor this in basic planning hygiene. Fidelity puts it plainly: "A personal budget provides a detailed picture of your income, expenses and leftover cash." Use that same discipline for freelance finance so your long-term planning stays clean.

Step 3: Write a one-page plan for how money gets allocated#

Create a single page that names:

- Your must-pay expenses

- Your Freedom Fund contribution rule: how you decide what gets set aside, and when

If you want a simple starting point, you can choose a fixed dollar amount to contribute, even $50 biweekly, and adjust later.

Want a quick next step? Try the free invoice generator.

How much should your freelance Freedom Fund be? (targets, thresholds, and a safe default)#

Set your Freedom Fund with two targets: coverage for timing gaps, plus a separate reserve for payment issues.

Now that you've mapped your buckets and pulled real invoice timing, you can stop guessing and set targets you can actually operate with. This section turns your collection reality into simple decision rules.

Step 1: Build a two-number target (coverage + payment issues)#

Start by separating "late or slow pay" from "money that might not land the way you expected."

| Target | What it protects | When it matters most | How to size it (based on your data) |

|---|---|---|---|

| Coverage target | Ordinary delays (approvals, payout timing, and other timing gaps) | You still need to pay fixed costs while you wait for an invoice to clear | Add up your non-negotiable operating commitments for a typical period, then choose a coverage window that matches your real payment lag (from "sent vs. paid") |

| Payment-issues reserve | Disputes, reversals, deductions, and other payment breaks | Any setup where payments can get disputed, delayed, or reduced | Look at which clients, terms, or payment methods tend to create issues. Size a reserve you can use without touching taxes or core operating cash |

You'll feel tempted to pick a single round number. Don't. Two targets keep your system clean because they reflect two different failure modes.

Step 2: Translate your invoice mix into a risk posture. Different clients, terms, and payment methods can come with different timing uncertainty and different chances of payment issues. Treat anything that increases ambiguity about when you'll get paid, or what exactly counts as "done," as a reason to be more conservative with your targets. If fees materially hit margin, fix that upstream.

Step 3: Stress-test client concentration (without a magic percentage). If one client drives a meaningful share of your monthly cashflow, treat a delayed invoice from them as a real operational stress test. Ask: "If they pay late, do my current targets keep me calm and solvent?" If not, consider whether you want a larger cushion, tighter terms, or both.

Step 2: Set two action lines (below-target vs comfortably above)#

Run the Freedom Fund with two simple triggers tied to your actual invoice cadence:

- Below-target line: when the fund drops under this point, pause discretionary spend, delay optional purchases, and tighten new project intake terms (deposit, milestones, shorter net).

- Comfortable-above line: when the fund sits clearly above your targets, you can choose higher-leverage moves: pay yourself extra, prepay a necessary expense, or route excess into an investment fund that still fits your liquidity needs.

Hypothetical scenario: a repeat client suddenly pushes payment to "after internal acceptance." You check where you are versus your action lines. If you're close to the below-target line, you require a deposit or milestone before you start. If you're comfortably above, you can negotiate firmly without sacrificing delivery quality.

What's your 10-minute client onboarding risk check (before you accept the work)?#

Run a quick pre-contract scan that forces a decision: accept, accept after you tighten the basics, or decline.

Protect your cash flow by preventing avoidable nonpayment and dispute problems at intake. This check keeps your system honest because you stop volunteering for messy invoices.

Before you start (2-minute setup)#

Put three things within reach: your contract template, your invoice template, and a single place to store written proof you can find later.

| Item | What to have ready | Why it matters |

|---|---|---|

| Contract template | Your contract template | Helps you have a contract or written agreement in place |

| Invoice template | Your invoice template | Helps you issue a clean invoice with a written trail |

| Proof storage | A folder or thread you can find later | Keeps written proof you can find later if things go sideways |

One freelancer put it bluntly: "Make sure when you sign your next customer, you have a contract in place, otherwise it is just 'he said she said'..." They also reported they "didn't get paid until 6 months after [they] had completed the work" when they skipped that step.

Step 1: Run the 4-check scan (8 minutes total)#

Use this as a pass/fix/decline checklist. Aim for clarity, not perfect risk prediction.

| Check | What you're verifying | Green flag | Red flag |

|---|---|---|---|

| 1) Payer reliability | They can pay on purpose, not by accident | Clear billing owner, clear approval path, straightforward vendor setup | Vague "AP will handle it," shifting owners, endless setup friction |

| 2) Terms clarity | The agreement defines deliverables and "done" | Written scope, written acceptance criteria, written change process | "We'll know it when we see it," fuzzy ownership, moving goalposts |

| 3) Payment path reality | You understand the actual collection path | They can explain how payment happens, who initiates it, and what you must submit | They cannot describe how payment happens, they insist "we'll figure it out later" |

| 4) Documentation readiness | You can prove what you delivered and what they owe | You can issue a clean invoice with a written trail | Work lives in calls and DMs only, no written confirmations |

Verification point: If you cannot produce (a) a contract or written agreement and (b) a clean invoice trail, you do not have much protection. You have hope.

Step 2: Make the decision (and document it) Pick one outcome and write it down in the client folder:

- Accept as-is: All four checks pass.

- Accept after fixes: You secure the missing pieces in writing before you start. Save everything. As one freelancer described in a nonpayment situation, "he was emailing me all of this so I simply saved all the emails," which gave them documentation when things went sideways.

- Decline: You see persistent confusion, refusal to document, or inability to explain how payment works.

Hypothetical scenario: a client loves your proposal but dodges written acceptance criteria. You pause, send a one-page "definition of done," and only start once they confirm it in writing. That protects cash flow now and preserves runway for longer-term plans later.

The per-invoice allocation playbook (exact rules to run every time you get paid)#

Split each invoice into Tax Reserve, Freedom Fund, and Operating using the same order every time.

Freelance income "often comes in fits and spurts and is so unpredictable," as The Wordling puts it. A simple routine helps keep those swings from turning into financial whiplash.

Step-by-step: your "payment event" routine (copy/paste rules)#

Before you start: name three buckets somewhere you can actually separate and track: Operating, Tax Reserve, Freedom Fund. These can be accounts, sub-accounts, wallet buckets, or a ledger with categories.

Step 1: Pick a trigger you can stick to. Choose the moment your routine runs, for example when a payment hits, when it clears, or when you close out a billing period, and stay consistent. The goal is to stay anchored to reality, not wishful numbers.

Step 2: Split in this order (Tax, then Freedom Fund, then Operating). Quality Tax Plus frames why this matters: "Proper bookkeeping is not just a legal requirement; it's a fundamental practice that can make or break your freelance career." You're building a system you can explain later.

| Bucket | Rule you set once | Why it protects you |

|---|---|---|

| Tax reserve | Save a fixed slice of each invoice into a separate bucket (you pick the slice based on your situation). | Helps prevent tax time from raiding operating cashflow. |

| Freedom Fund | Contribute a fixed slice, plus a temporary "catch-up" amount until you hit your floor. | Builds slack so one weird month doesn't derail the plan. |

| Operating | Use what remains for payroll, tools, and delivery. | Forces you to run lean after you fund the non-negotiables. |

Step 3: Add a timing rule that matches reality. Only allocate money you can actually access. If the cash is not really there yet, treat it as unallocated.

Step 4: Make it auditable (you, your bookkeeper, future-you)#

Every split gets a memo. Use: Client + invoice number + a short note on anything relevant.

Beam Content models the right humility here: "This is not financial advice, just a collection of opinions and experiences." Treat this playbook the same way, then adapt it to your situation.

If you use wallet or ledger-style tooling, treat the ledger as your source of truth. Keep transfers traceable end-to-end. That's what keeps your routine grounded in reconcilable numbers.

Where should the Freedom Fund sit for liquidity and control (without creating a mess)?#

Specific guidance on where to keep a Freedom Fund for liquidity, control, or auditability is not established here. Anything more specific here - two-tier setups, separate buckets, invoice-level memo rules, and similar details - would go beyond what is supported.

What we can verify from the sources you provided is limited to page metadata and a site-wide stat:

- The Get Rich Slowly article "Mastering your money: 12 steps to financial freedom" is published 01 October 2016 and updated 06 December 2024.

- The Wealth Without Wall Street Podcast page displays "1,500,000 Downloads and Counting!".

What do you do when clients pay late, a payout gets held, or a chargeback hits? (the exception workflow)#

Handle late pays, holds, and disputes with a written SOP that logs the issue, protects cashflow, and assembles proof fast.

Once you have a cash buffer you can access and reconcile cleanly, you need a repeatable response plan for the moments that actually test freelance finance. Late payments, payout delays, and disputes happen. Your system decides whether they become a crisis.

Step 1: Triage the exception and open a single "case file"#

Treat every issue as a trackable case, not a Slack spiral.

- Create one log entry (doc, note, CRM, whatever you will actually maintain).

- Record: client, invoice number, amount, due date, payment rail, and the exact failure mode (late, payout delay, dispute).

- Start a comms log immediately (date, channel, summary, next follow-up).

Verification point: you can answer "What exactly do I want next, and by when?" in one sentence.

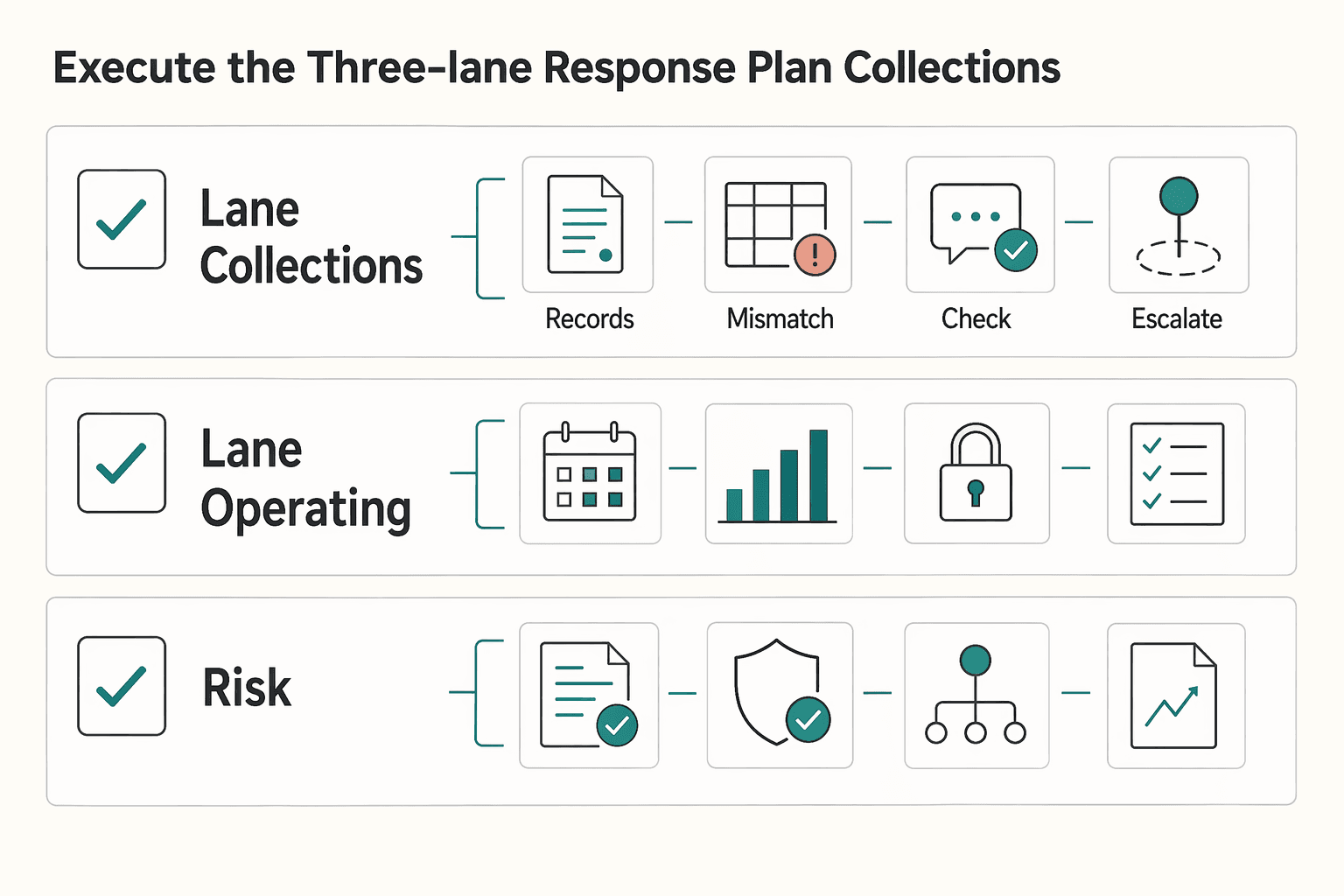

Step 2: Execute the three-lane response plan (collections, continuity, risk reduction)#

Run all three lanes in parallel so you protect today and your long-term planning.

| Lane | Goal | Actions you can run today |

|---|---|---|

| Lane A: Collections | Get the invoice paid | Follow your reminder approach based on your payment terms. Escalate from polite reminder to direct "payment required to continue work." |

| Lane B: Operating continuity | Keep delivery stable | Use your own cash buffer plan to decide what you can cover temporarily (subscriptions, contractors, critical tools). Keep a note in the case file for every transfer so your savings goals stay auditable. |

| Lane C: Risk reduction | Prevent repeats | Tighten payment terms next round (deposit, milestones, shorter net terms). Consider switching rails for future invoices if your current rail creates delays or dispute exposure. |

Hypothetical scenario: a platform says it "needs review" before releasing funds. You log the case, continue only the work you can sustain, and tighten terms for the next project so you never depend on a single payout event.

Step 3: Build an audit-ready proof bundle (this saves time, even when you can't "win") You cannot control every outcome, but you can control your documentation.

Your proof bundle should include:

- Contract or written agreement (including payment terms)

- The invoice

- Proof of delivery or acceptance (files, links, screenshots, sign-off message)

- Comms log (email thread exports help)

- Any dispute evidence you can provide quickly

If you work through a freelance platform, one Quora answer described a pattern where "payment is released three days after delivery, unless the buyer says they aren't happy." It also suggested: "You can try raising a dispute with the freelance provider." Use that as a practical escalation option when a platform, not the client, blocks release.

Pass/fail operator test: if you can't assemble your proof bundle quickly, your dispute process is still too fragile. Fix the storage, naming, and logging before the next dispute tests your financial freedom.

Common mistakes (and how to recover without derailing your cashflow)#

The biggest cashflow blowups usually come from emotional money decisions, living beyond your means, and ignoring your budget. Each one is fixable with a simple habit.

| Mistake | What breaks | Safer move |

|---|---|---|

| Budget off expected money | Late or uneven income | Plan from what's already in hand (and what you can count on) |

| Emotional money decisions | Stress shopping, fear-based moves, or celebration spending can quietly wreck your goals | Put a pause rule on non-essential spending |

| Living beyond your means | Can lead to serious debt | Separate baseline expenses from nice-to-haves |

| Overlooking the basics | Financial mistakes can come from emotional choices or overlooking duties | Keep a simple list of upcoming obligations and due dates |

| Ghost your budget | Things drift | Once a month, review your income, upcoming obligations, and current spending against your plan |

Freelance income can feel like a financial rollercoaster. If your numbers keep drifting, the goal is not perfection. It's getting back to a few steady defaults that protect your buffer and keep your planning grounded in reality.

Step 1: Budget for irregular income (stop planning like every month is your best month)#

Freelancers "often face fluctuating income and irregular paychecks," so a plan that assumes smooth, predictable pay will keep breaking. Build your baseline budget around what you can reliably cover, then treat upside as upside.

| Habit | What it assumes | What breaks | Safer default |

|---|---|---|---|

| Budget off "expected" money | "It'll probably come in" | Late or uneven income | Plan from what's already in hand (and what you can count on) |

| Budget off real cash | "Cashflow is real" | Less exciting projections | Your plan matches reality |

- Verification point: Your plan matches what's actually available, not what you hope shows up.

Step 2: Stop making emotional money decisions (so you don't blow up your plan on a bad day)#

Western and Southern puts it plainly: "Money and emotions don't mix well." Stress shopping, fear-based moves, or celebration spending can quietly wreck your goals.

- Action: Put a pause rule on non-essential spending, even a short one, so decisions are not made in the heat of the moment.

- Verification point: You can explain the "why" behind recent spending without it boiling down to mood.

Step 3: Don't live beyond your means (even when a good month tricks you)#

"Living beyond your means might impress others, but it can lead to serious debt." Strong months are real, but they are not a permanent salary. Keep your lifestyle anchored to your sustainable baseline.

- Action: Separate "baseline" expenses from "nice-to-haves," and only upgrade commitments when your baseline can carry them.

- Verification point: A slow month does not force you into panic cuts or debt.

Step 4: Stop overlooking the basics (small misses become big messes)#

Financial mistakes can come from "emotional choices or overlooking duties." The fix is boring on purpose: keep the basics visible so they do not sneak up on you.

- Action: Keep a simple list of upcoming obligations and due dates, and review it regularly.

- Verification point: Nothing "surprises" you that was actually predictable.

Step 5: Install a monthly budget check-in (stay flexible instead of avoiding your numbers)#

Don't ghost your budget. Make it a monthly reset so you can course-correct before things drift.

- Action: Once a month, review your income, upcoming obligations, and current spending against your plan.

- Action: Adjust and stay flexible ("check in monthly, adjust and stay flexible.").

- Verification point: You can say what changed this month and what you're doing about it in one sentence.

Conclusion: turn the Freedom Fund into a repeatable "get paid" system you can run on every client#

Stop treating the Freedom Fund like a savings mood and start treating it like governance you can execute on every payment event. You already know the risks: late pay, holds, disputes, fees. Now write down the rules, run them every time, and escalate exceptions without improvising.

If you do nothing else, do this four-part loop:

- Define your target. Pick a target you can defend with your real cashflow history and your current obligations. You want a clear "floor" that triggers behavior changes, and a "green zone" that lets you plan longer-term (financial freedom, long-term planning, even an investment fund) without stealing oxygen from operations.

- Enforce payment terms before you start work. You do not need fancy language; you need clarity: when you invoice, when you expect payment, what counts as acceptance, and what happens if payment slips. Use whatever structure fits your work, but you set the policy, not the internet.

- Allocate from every paid invoice. Split money when you collect it, not when you send the invoice. That one rule stops phantom cashflow and keeps your freelance finance system honest.

- Run the exception workflow when reality breaks the plan. Late invoice, payout hold, chargeback: respond with a checklist, not adrenaline.

Know your fee drag (it changes what "enough buffer" means)#

Stripe notes that payment gateway fees can significantly impact profitability and cost structure because every transaction incurs a cost. Stripe also says listed costs can change, so re-check before you bake assumptions into your pricing.

| Stripe lists this as... | Fee (selected examples) | Why it matters to your system |

|---|---|---|

| Domestic card transaction | 2.9% + 30¢ | Your margin funds your buffer, not just your lifestyle. |

| Manually entered card add-on | +0.5% | Manually entered payments cost more. Price and policy should reflect it. |

| International card add-on | +1.5% | Cross-border clients increase fee drag. |

| Currency conversion add-on | +1% | FX friction compounds quietly. |

| ACH Direct Debit | 0.8% (cap $5.00) | The fee structure can change which rails you prefer. |

Hypothetical: a client pays by card, then disputes the charge. Your buffer buys time to keep operating while you gather the contract, invoice, delivery proof, and comms log.

If card costs keep eating your margin, tighten the fee side next: How to Reduce Stripe Processing Fees. If you plan to work abroad, pressure-test your recordkeeping and tax posture before you move.

Copy/paste checklist (Freedom Fund runbook)#

- Freedom Fund target set (based on your own cashflow and risk tolerance)

- Money tracked by category (operating, tax where applicable, buffer)

- Client + payment method chosen intentionally (fees, payout timing, and operational overhead)

- Contract + payment terms agreed in writing

- Allocation rule applied to every paid invoice (on collection, not on send)

- Exception workflow ready (late-payment follow-ups, payout holds, dispute response)

- Monthly reconciliation completed (invoice IDs tied to transfers; balances verified)

Frequently Asked Questions

What is a freelance freedom fund (and why is it different from “Freelance Freedom”)?

A freelance freedom fund is a label people use loosely, so you need to define it inside your own system. If you see “Freelance Freedom” elsewhere, treat it as someone else’s framing, not a standardized term, and get clear on what you want your own fund to do.

How much should a freelancer keep in a freedom fund?

Set your target by mapping your real cashflow pattern, not by copying someone else’s savings goals. As Winning Solo puts it, “Our revenue fluctuates, sometimes wildly, often unpredictably,” and Charley Locke adds, “the work comes in waves.” Build a floor you can defend, then raise it when you take on higher-risk clients, longer pay cycles, or more fixed commitments.

Is a freedom fund the same as an emergency fund or tax savings?

Not necessarily. An emergency fund usually protects your household, while a separate business buffer is often about keeping operations steady through volatility. Whatever buckets you use, keep the lines clean so you are not mixing funds in a way you cannot track. Winning Solo says it plainly: “The IRS, shall we say, frowns upon commingling.”

How do I build a freedom fund if clients pay late?

Build it from collected payments only and make it as consistent as you can. When money lands, move some of it into your buffer even if the amount feels small, because consistency beats intensity. If late pay keeps punching holes in your plan, tighten terms first, then fund the buffer from the improved collections.

Where should a freelance freedom fund sit for liquidity and control?

Prioritize clarity and separation over any one “perfect” place. Winning Solo recommends “keeping an account exclusively for business income and expenses,” and that same separation principle helps you track what is business money versus personal money. If you cannot reconcile transfers back to specific inflows, you do not control the fund, you just have a vague pile.

What rules should I use to allocate each payment to tax, operating cash, and reserve?

Use a rule you can run every time and write it down in plain language. Keep it simple enough that you will actually follow it, then review it periodically as your income swings and obligations change. Verification point: you can explain what each bucket does and why it exists without hand-waving.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- oecd.org/content/dam/oecd/en/publications/reports/200...trusted

- scstatehouse.gov/code/t12c006.phptrusted

- sec.gov/Archives/edgar/data/1627475/0001193125182675...trusted

- sec.gov/Archives/edgar/data/1451951/0001398432090001...trusted

- unc.edu/about/accessibility/well-said-transcripts-2trusted

- unc.edu/about/accessibility/well-said-transcripts-2trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

How to Reduce Stripe Processing Fees

**You can protect margin by treating fees, payout timing, and dispute exposure as one risk system.** It is easy to fixate on headline Stripe fees. In practice, margin usually leaks from three places at once:

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.