Quick Answer

To create a buy-sell agreement for partnership, run a structured playbook: define trigger events, choose who buys first, lock valuation and funding rules, and align enforceability clauses before signing. Start by reconciling your current partnership documents, then choose a structure such as cross-purchase or redemption, and finish with legal and tax review in each relevant jurisdiction.

Build a partnership safety net before a partner exit becomes a legal fight#

Treat your buy-sell agreement for partnership as core operating infrastructure, not paperwork for later. Freelancers and consultants move fast on client delivery, but shared ownership risk keeps running in the background until one partner leaves, becomes disabled, goes bankrupt, or goes through a divorce.

Even when you share ownership, you are the CEO of a business-of-one, and your job is to make exits predictable before they become personal. If you wait for the triggering moment, you negotiate under pressure and hand control to whoever reacts fastest.

A buy-sell agreement (also called a buyout agreement) sets pre-agreed rules for what happens when ownership changes. It can support business continuity, not just document an exit. The practical goal is simple: support planning for cash flow, control, and succession decisions while client work keeps moving.

Run the Partnership Buy-Sell Playbook in one session#

- Name your operating risk. List where your current legal document set stays silent on exits, transfers, and decision rights. Expected outcome: one page of unresolved ownership risks you can act on now.

- Define trigger events before emotion takes over. Agree on plain language for departure, death, disability, bankruptcy, divorce, and retirement. Expected outcome: a shared trigger list that removes improvisation during stress.

- Set your first-response rules. Decide how transfer approvals, purchase options, and dispute decisions will be handled. Expected outcome: a clear decision path that supports continuity and control planning.

- Convert intent into a signed drafting brief. Capture the terms in writing, assign owners, and schedule legal and tax review in each relevant market. Expected outcome: a draft-ready brief your counsel can translate into enforceable terms.

Picture a small consultancy with two partners. One suddenly wants out while a major client renewal sits in review. If triggers, transfer rights, and approvals are already defined, you are better positioned to execute a handoff instead of pausing delivery to improvise ownership terms.

| What this session gives you | Why it matters now |

|---|---|

| Clear continuity rules | Supports client work continuity when partner status changes |

| Cash flow planning inputs | Helps you plan buyout timing with less operational disruption |

| Control guardrails | Makes ownership shifts more likely to follow pre-agreed rules, not only pressure |

Use this framework for education and alignment first, then have local legal and tax professionals review and finalize terms for your jurisdictions. If you want a deeper dive, read Germany Freelance Visa: A Step-by-Step Application Guide.

What to prepare before you draft anything#

Prepare a complete, conflict-free input pack first, then draft your buy-sell agreement for partnership from that pack. The fastest way to get a "signed but unusable" agreement is to draft before you reconcile what already governs you. This prep step keeps your buy-sell terms from clashing with your current legal document set and helps you catch cross-border tax issues early.

Before you start#

Treat this as a short pre-draft sprint. Your goal is to align your partnership agreement, confirm current ownership and notice details, and collect the records that support approvals and payouts. Do this upfront and your buy-sell agreement stays coherent instead of drifting into conflicting clauses.

| Document or record | Why you need it now | Verify before drafting |

|---|---|---|

| Current Partnership Agreement | Sets baseline control and governance terms | Flag clauses that conflict with transfer rules |

| Prior Buy-Sell Agreement or Succession Agreement | Reveals legacy terms you may still rely on | Mark what to keep, replace, or retire |

| Current ownership schedule | Anchors transfer mechanics | Confirm each partner interest and notice details |

| Approval and payout records | Creates an auditable trail | Confirm you can trace approvals, evidence, and reconciliation |

Build your draft pack in one session#

| Step | What to do | Verification point |

|---|---|---|

| Step 1 | Reconcile document hierarchy: compare your foundational agreements and decide which transfer terms control if language conflicts | You can state one clear hierarchy rule that counsel can codify in the draft |

| Step 2 | Build a partner facts sheet: list ownership splits, notice contacts, and where the partnership has its principal place of business | Every partner profile includes ownership and notice details |

| Step 3 | Define record trail requirements: set minimum evidence for ownership changes, including written notices, approvals, payout support, and reconciliation logs | Your team can show who approved what, when, and with which supporting records |

| Step 4 | Create a counsel handoff pack: summarize assumptions, open questions, and market-specific tax issues, especially if a foreign partner may trigger withholding obligations on an interest transfer | Counsel receives a focused list of decisions, not a blank-page request |

- Step 1. Reconcile document hierarchy. Compare your foundational agreements and decide which transfer terms control if language conflicts. Verification point: you can state one clear hierarchy rule that counsel can codify in the draft.

- Step 2. Build a partner facts sheet. List ownership splits, notice contacts, and where the partnership has its principal place of business so you can localize governing-law review early. Verification point: every partner profile includes ownership and notice details.

- Step 3. Define record trail requirements. Set minimum evidence for ownership changes, including written notices, approvals, payout support, and reconciliation logs. Verification point: your team can show who approved what, when, and with which supporting records.

- Step 4. Create a counsel handoff pack. Summarize assumptions, open questions, and market-specific tax issues, especially if a foreign partner may trigger withholding obligations on an interest transfer. Verification point: counsel receives a focused list of decisions, not a blank-page request.

If a foreign partner is involved while the partnership's principal office is local, flag that split before drafting terms. It affects governing-law review, tax review scope, and your final legal document workflow.

Which buy-sell structure fits your partnership right now?#

Pick the structure that matches your owner count, administrative capacity, and control goals, then document it clearly in your buy-sell terms. With your prep documents aligned, you can choose an ownership transfer model with less guesswork. This decision determines who buys, who signs, and how smoothly exits are handled in practice.

Compare the core structures with a practical grid#

Cross-Purchase Agreement means the remaining owners buy the departing owner's interest directly. Redemption Agreement means the business buys back that interest itself. Both can be drafted inside a buy-sell agreement, but they create different workflows in your agreement stack.

| Decision factor | Cross-Purchase Agreement | Redemption Agreement |

|---|---|---|

| Buyer of departing interest | Remaining partners buy directly | Business entity buys back interest |

| Best fit by owner count | Usually strongest with a smaller owner group | Often easier when owner count grows |

| Admin burden | Rises as partners increase | Centralizes process inside the entity |

| Insurance complexity | Can become harder to manage as ownership expands | Often simpler to administer through the entity |

| Control objective | Keeps ownership inside the existing partner group | Supports stable, standardized buyback operations |

The tradeoff is operational. Cross-purchase can stay tight and partner-controlled in smaller groups. Redemption can be easier to run consistently as the owner group grows.

Use a safe default rule for mixed and edge cases#

- Step 1. Define your primary goal. Rank goals in order: control retention, administrative simplicity, and transaction speed. Verification point: partners agree on one top priority in writing.

- Step 2. Choose a base model. Select cross-purchase when you want tight partner-level control in a smaller group. Select redemption when you need cleaner administration across more owners. Use a hybrid when you want the entity to buy first and owners to buy if needed. Verification point: your draft states who buys first and what happens next if that first path is not used.

- Step 3. Draft with entity flexibility. Frame the terms as a broader Buyout Agreement that can stand alone or sit inside the partnership agreement, so the structure can adapt if your entity form changes later. Verification point: your draft explains where buy-sell terms live and which document controls conflicts.

- Step 4. Pause on edge cases and escalate. Stop and route to local counsel when your facts are jurisdiction-specific or ownership terms are nonstandard. Verification point: counsel confirms governing law and tax treatment before signature.

What events should trigger a forced or optional buyout?#

Define trigger events and response paths now so every Partnership Interest transfer follows rules, not emotion. Build this as an execution matrix so your team knows what happens when death, disability, divorce, retirement, bankruptcy, or partner departure triggers a buy/sell process.

Build your trigger matrix before you draft clauses#

Map each event to a forced or optional buyout path, then assign buyer priority and restrictions in the same row. Keep this matrix tied to your legal document workflow so your buy-sell agreement and partnership agreement stay aligned.

| Trigger event | Forced or optional path | First buyer right | Restricted buyer outcome | Action path |

|---|---|---|---|---|

| Death | Forced or optional based on agreement terms | Entity or remaining partners | Spouse/heir transfer risk managed through purchase rights in the agreement | Start valuation, issue transfer notice, execute buyout |

| Disability | Forced or optional based on agreement terms | Entity or remaining partners | Third-party transfer can be restricted unless the agreement permits it | Confirm trigger definition, start valuation, close transfer |

| Retirement | Optional path with written notice, then buyout process per agreement | Entity or remaining partners | Outsider sale limited unless agreement allows | Collect written notice, run purchase option sequence |

| Bankruptcy | Forced or optional based on agreement terms | Entity or remaining partners | External creditor-driven control can be limited where permitted | Trigger mandatory offer, execute purchase rights |

| Divorce | Forced or optional based on agreement terms | Entity or remaining partners | Former spouse ownership exposure managed by purchase rights | Trigger transfer review, run buyout at defined method |

| Partner departure | Voluntary path with notice, or mandatory path for for-cause termination if drafted | Entity or remaining partners | Outside buyer access limited by consent rules | Start notice process, run timeline to closing |

Separate termination paths and lock dispute steps#

| Step | Rule | Verification point |

|---|---|---|

| Step 1 | Split voluntary and for-cause exits: define voluntary resignation with a written notice window and define for-cause termination separately with a mandatory buyout route | Each exit type has its own timeline and obligations |

| Step 2 | Set buyer priority clearly: state who buys first, who buys next, and when outsiders may participate | Spouse and heir scenarios follow one predictable rule set |

| Step 3 | Tie triggers to dispute resolution: pre-assign mediation, arbitration, or litigation order for valuation or process disputes | The team can point to a pre-agreed escalation path in one paragraph |

| Step 4 | Run a scenario check: use one real scenario such as a resignation, a disputed price, or a divorce-driven transfer risk | Your matrix shows trigger type, notice path, buyer order, and dispute route without fresh negotiation |

- Step 1. Split voluntary and for-cause exits. Define voluntary resignation with a written notice window (often 60 to 90 days where used). Define for-cause termination separately and allow a mandatory buyout route. Verification point: each exit type has its own timeline and obligations.

- Step 2. Set buyer priority clearly. State who buys first, who buys next, and when outsiders may participate. Verification point: spouse and heir scenarios follow one predictable rule set.

- Step 3. Tie triggers to dispute resolution. Pre-assign mediation, arbitration, or litigation order for valuation or process disputes. Verification point: the team can point to a pre-agreed escalation path in one paragraph.

- Step 4. Run a scenario check. Use one real scenario (a resignation, a disputed price, or a divorce-driven transfer risk). Your matrix should show trigger type, notice path, buyer order, and dispute route without fresh negotiation.

How do you set price and fund the buyout without freezing operations?#

Set a clear valuation rule and a funded payment path in your buy-sell agreement for partnership so a trigger event does not stall operations. Triggers tell you when the buyout starts. Valuation and funding determine whether the buyout can actually close while the work continues.

Choose valuation mechanics your team can execute#

Use one of the common valuation provision types in your buy-sell agreement, then tie review timing to business milestones so price stays current.

| Valuation method | How it works | Good fit | Key control |

|---|---|---|---|

| Fixed value | Partners agree a value and attach it as an exhibit | Stable businesses with aligned owners | Set review dates so value does not go stale |

| Formula | Agreement applies a pre-set mathematical formula | Teams that want repeatable pricing logic | Define inputs clearly and keep inputs auditable |

| Process | Agreement defines a valuation process at trigger | Teams that want flexibility at event time | Lock the process steps before conflict |

- Step 1. Select the base valuation method. Choose fixed, formula, or process based on how often partners update financials. Verification point: one method appears in the draft with no conflicting alternatives.

- Step 2. Set a review cadence. Tie valuation refreshes to milestones your team already tracks, such as annual planning or material scope changes. Verification point: your legal document names who initiates each review.

Build funding rails and payment controls#

- Step 3. Map funding paths in priority order. Set an agreed funding sequence, such as available cash, life insurance for death-trigger liquidity, and a promissory-note fallback when liquidity is tight. In a cross-purchase setup, each owner can hold policies on co-owners. Verification point: the agreement states which path activates first. If you want a practical primer, see A Guide to Key Person Insurance for Small Agencies.

- Step 4. Define execution controls. Define payment terms and transfer steps, including approval checkpoints and evidence requirements before money moves. Record approvals, payout proof, and reconciliation logs so finance workflows stay traceable. Verification point: your team can reconstruct the full payment trail from one folder.

- Step 5. Write a no-freeze fallback. If liquidity tightens, allow staged payments under defined promissory-note terms so ownership transfer continues without a fire-sale decision. Verification point: both buyer and seller obligations stay explicit.

If you want a quick next step for "buy-sell agreement for partnership," Try the SOW generator.

Which clauses keep the agreement enforceable when pressure hits?#

Prioritize governing law, jurisdiction, dispute resolution, liability limits, and transfer controls in your partnership buy-sell agreement so conflicts follow a pre-set path. Price and funding solve the economics. Enforceability clauses solve the "what happens when someone refuses" problem.

Build the enforceability stack in draft order#

| Clause area | Draft instruction | Verification point |

|---|---|---|

| Governing Law and Jurisdiction | State which law controls interpretation, then state which court or ADR forum handles the dispute | Your draft answers both questions in plain language |

| Dispute Resolution | Define one path for mediation, arbitration, or litigation so valuation and transfer fights do not become ad hoc escalation | Your legal document shows one clear escalation route |

| Limitation of Liability | Cap exposure where appropriate and write specific carveouts your operating model needs | Each partner can explain the cap and exceptions in one minute |

| Indemnification | Assign who covers which losses, under what trigger, and with what process | Claims, notice, and reimbursement steps match your partnership agreement workflows |

- Step 1. Separate Governing Law from Jurisdiction. State which law controls interpretation, then state which court or ADR forum handles the dispute. Treat these as distinct decisions, not one combined sentence. Verification point: your draft answers both questions in plain language.

- Step 2. Preselect a Dispute Resolution path. Define your path for mediation, arbitration, or litigation so valuation and transfer fights do not become ad hoc escalation. Verification point: your legal document shows one clear escalation route.

- Step 3. Set Limitation of Liability boundaries. Cap exposure where appropriate and write specific carveouts your operating model needs. A cap manages risk allocation, but it does not erase all liability. Verification point: each partner can explain the cap and exceptions in one minute.

- Step 4. Define Indemnification scope. Assign who covers which losses, under what trigger, and with what process. Verification point: claims, notice, and reimbursement steps match your partnership agreement workflows.

Lock transfer control and future proof ownership terms#

- Step 5. Restrict Partnership Interest transfers. Where local law allows, require consent rules and give the entity or existing partners purchase rights before any outside transfer. Verification point: outsider ownership cannot bypass your consent process.

- Step 6. Add conversion notes for entity changes. If you later change entity type, do not assume ownership terms carry over one-to-one; remap the terms so your original intent stays explicit after restructuring.

| Current clause intent | If converting entities, re-document as | Rule that should stay consistent |

|---|---|---|

| Transfer restrictions on partnership interests | Entity-specific transfer restriction language | Consent and purchase rights before outsider transfer |

| Governing law, forum, and dispute path | Entity-specific governing law, jurisdiction, and ADR language | Trigger events, valuation method, and dispute path |

Use local counsel to validate final wording because enforceability details vary by jurisdiction.

What goes wrong most often and how do you recover fast?#

Many failures in a buy-sell agreement for partnership come from four fixable gaps, and you can recover fast with a focused repair sprint. This is the operational reality check. The agreement fails when it cannot be executed cleanly with your existing documents, records, and cash movement.

-

Step 1. Reconcile governing documents before you edit language. Pull your current Partnership Agreement, Buy-Sell Agreement, and any related succession or ownership documents into one redline session. Template-first drafting often creates silent conflicts across definitions, transfer rights, and payout mechanics. Treat governing-document alignment as a control task, not a formatting task. Verification point: every ownership term and transfer rule matches across documents with no contradictory clause.

-

Step 2. Rewrite trigger events in plain action language. Define exactly which events activate the buyout path, who acts first, and the sequence for what happens next. Weak triggers force ad hoc negotiation during crisis, especially when exits turn emotional. Tight language removes ambiguity and protects business succession. Verification point: each trigger includes an owner, a required action, clear timing, and a valuation standard.

-

Step 3. Run a funding drill, then set recurring proof-of-funding checks. Life insurance can fund a death trigger, but it does not solve every trigger event. Build separate payment mechanics for non-death scenarios so the legal document stays executable under stress. Verification point: partners can show current funding evidence for death and non-death buyout paths.

-

Step 4. Align indemnification and limitation terms as one risk system. Review indemnification, limitation of liability, and governing-law language together, then redline enforceability and edge cases. Imagine one partner exits under conflict while another claims broad reimbursement rights. If these clauses drift apart, disputes accelerate and recovery slows. Verification point: your buy-sell agreement and partnership agreement allocate risk consistently for routine disputes and edge-case exits.

Use this decision rule for the final pass: if a clause cannot tell a partner what to do under pressure, rewrite it until it can.

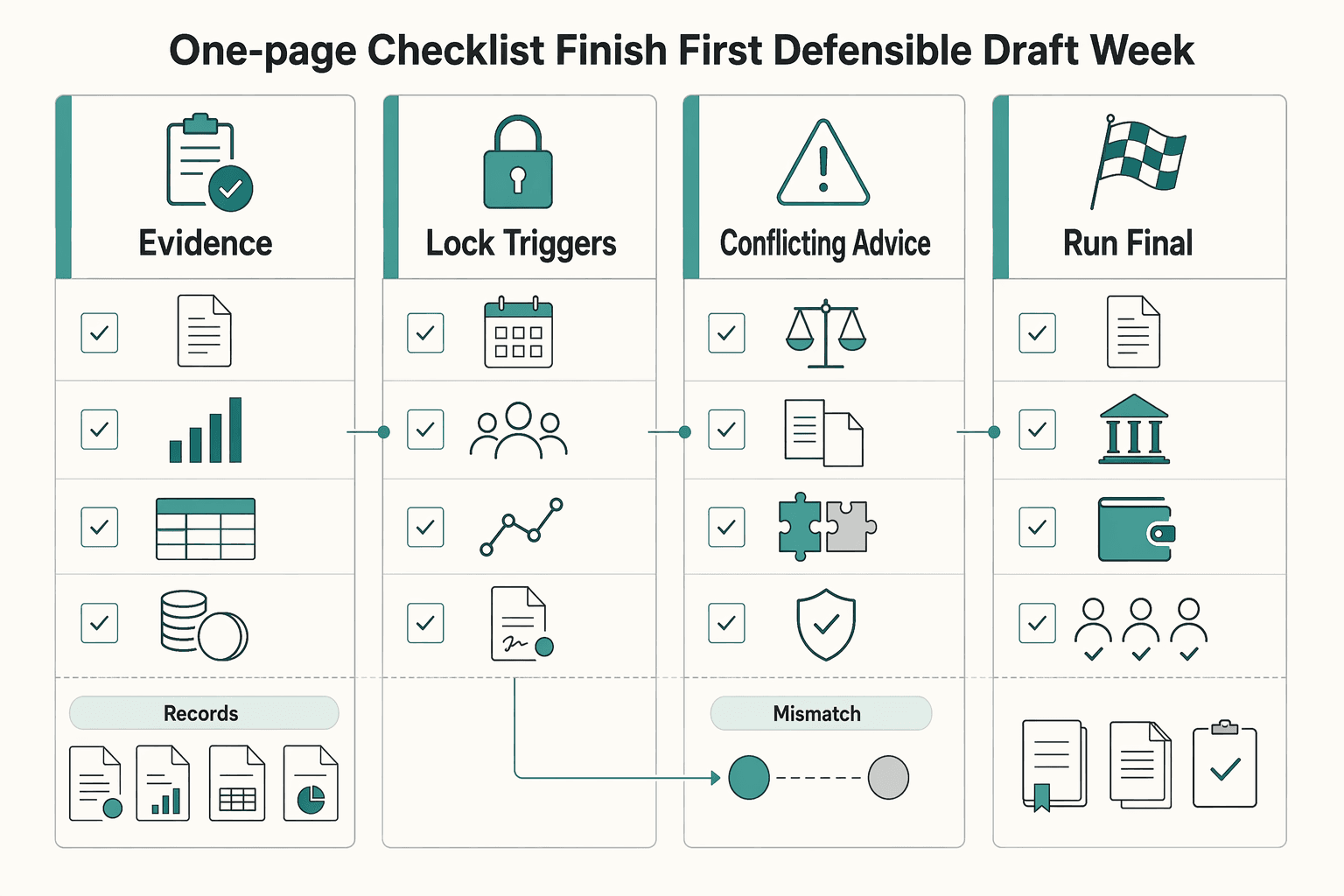

Use this one-page checklist to finish your first defensible draft this week#

Use this five-step closeout to convert a working draft into a sign-ready buy-sell agreement for a partnership without leaving legal gaps. The point is not elegance. The point is a draft your partners can execute under stress, using real records and a real payment workflow.

Before you start: open your current Partnership Agreement, draft Buy-Sell Agreement, ownership cap table, and current funding evidence in one working file.

-

Step 1. Confirm structure choice and record your reason. Decide between a Cross-Purchase Agreement and a Redemption Agreement, then write a short rationale tied to partner count, control goals, and admin load. Verification point: your draft states the selected structure, why you chose it, and what would trigger a future switch.

-

Step 2. Lock triggers, transfer rights, and termination pathways. Write trigger events in plain language, including death, disability or incapacity, retirement or resignation, and personal bankruptcy. State who can buy first and who needs consent before any transfer. Verification point: each trigger names the event, first buyer, deadline owner, and termination path.

-

Step 3. Finalize valuation and funding mechanics. Define one valuation method and keep it consistent across the buyout workflow. If you use fair market value, define it as a willing buyer and willing seller standard inside the legal document. Life insurance is commonly used for death-trigger liquidity, then add non-death payment terms so cash constraints do not freeze transfers. Verification point: finance can execute every trigger without renegotiating price or payment terms.

-

Step 4. Validate the enforceability package as one system. Align Governing Law, forum selection, dispute resolution path, Indemnification, and Limitation of Liability in a single redline pass. Treat these clauses as connected risk controls, not isolated boilerplate. Verification point: your draft names applicable law, dispute venue, ADR or litigation path, and risk allocation boundaries with no internal conflicts.

-

Step 5. Run final legal and tax review, then set refresh cadence. Ask counsel to review jurisdiction-specific legal and tax issues before signature, including whether valuation restrictions fit bona fide and arm's-length comparability expectations. Pair legal review with insurance review so funding design matches obligations. Then schedule regular refresh checkpoints as an operating discipline. Verification point: your calendar, counsel notes, and version log show a repeatable review cycle.

Frequently Asked Questions

What should a buy-sell agreement include for a partnership?

A strong buy-sell agreement for partnership defines what triggers a buyout, who can buy (and in what order), how price is set, and how payments are made. It should also clarify what happens to the business after an owner exits. The execution test is simple: it fits your live partnership agreement and your operating workflow.

What events should trigger a buy-sell agreement?

Define triggers in plain language so nobody renegotiates rules during a crisis. Common triggers include death or incapacity, bankruptcy, creditor claims, and divorce-related transfer risk. You can also define partner departure events that permit or force a buyout, as long as the agreement states buyer order and valuation method for each trigger.

Who can buy a departing partner’s share and who should be restricted?

Most teams route the purchase through remaining owners, the company, or another approved buyer. A right of first refusal keeps the departing owner from shopping the interest externally before existing owners or the entity get a shot. Restrict outside buyers or family transfers from taking control unless the agreement and consent rules allow it.

How do partners set a fair buyout price without constant disputes?

Pick one valuation standard and write it precisely. Many agreements use current value, book value, or the present value of future distributions, but the key is that partners can run the method with the records they actually keep. If valuation is vague, the disagreement will show up at the worst possible time.

How is a buyout funded if the business is cash-constrained?

Use multiple funding paths instead of betting on one payment event. Life insurance can cover a death-trigger buyout, but non-death exits usually need staged terms, such as a 20% to 30% down payment with installments over three to five years. The goal is continuity: close the ownership transfer without freezing operations.

Which is better for us right now, cross-purchase or redemption?

Neither structure wins in every case. A Cross-Purchase Agreement and a Redemption Agreement solve different needs, and wait-and-see or hybrid structures can also fit. Decide based on partner count, how much process you can realistically run, and how tightly you want ownership held at the partner level.

Can one template work across multiple states or countries?

Do not assume one template covers every jurisdiction. Without tailored terms, default state law can drive outcomes, and some states can require partnership dissolution when a partner leaves. For cross-border teams, treat templates as a starting point, then run local legal and tax review before signing because rules vary by jurisdiction.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- law.cornell.edu/wex/Partnershiptrusted

- findlaw.com/smallbusiness/incorporation-and-legal-struct...external

- freelegalforms.uslegal.com/partnership-forms/buy-sell-agreementexternal

- legalclarity.org/what-to-include-in-a-partnership-buy-sell-ag...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Germany Freelance Visa Application Path for Freiberufler and Gewerbe

Choose your track before you collect documents. That first decision determines what your file needs to prove and which label should appear everywhere: `Freiberufler` for liberal-profession services, or `Selbständiger/Gewerbetreibender` for business and trade activity.

A Guide to Key Person Insurance for Small Agencies

If one founder, rainmaker, or delivery operator drops out, your agency can lose revenue, delivery capacity, and client confidence fast. That risk is common, not an edge case. In small-business research, 71% of surveyed firms reported they were very dependent on one or two people. That makes continuity planning a core operating decision, not optional paperwork.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.