Quick Answer

Calculate taxable worldwide income by first totaling your worldwide gross income from all sources in U.S. dollars, then testing whether you must file before applying exclusions or credits. Include earned income, investment income, and taxable non-cash compensation. After the filing test, sort income into FEIE-eligible earned income, FTC categories, and separate reporting items such as FBAR-related accounts.

What Really Constitutes Your 'Worldwide Income'?#

Start with the broadest number, not the most favorable one. If you are a U.S. citizen or resident alien, the analysis begins with your worldwide gross income from all sources, before exclusions or credits. First total what belongs in gross income. Then determine what may later be excluded, credited, or reported separately.

Build your worldwide gross income total#

Classify income by type, not by where it was paid or deposited. Your first-pass total will usually include earned income such as salary, freelance fees, bonuses, and tips. It also includes investment or passive income such as interest, dividends, and capital gains, plus non-cash compensation such as lodging, meals, or use of a car when those benefits are treated as compensation.

Where the account is located, where the money landed, and what currency you were paid in do not control inclusion by themselves. You still report the amount on your U.S. return in U.S. dollars.

| Usually included in worldwide gross income | Potentially excluded or handled separately |

|---|---|

| Salary, wages, freelance/consulting fees, tips, bonuses | Some foreign earned income may later qualify for FEIE if you are a qualifying individual and file claiming it |

| Interest, dividends, capital gains, other investment income | Foreign taxes paid may later support an FTC, but they do not reduce gross income upfront |

| Employer-provided lodging, meals, or use of a car treated as compensation | Cross-border compensation packages may need careful classification before filing |

| Interest from foreign accounts | FBAR (FinCEN Form 114) is separate reporting if aggregate foreign account value exceeded $10,000 at any time in the year |

Test whether you must file#

Do this before you model FEIE or FTC. After you total worldwide gross income, verify the current IRS filing threshold for your filing status in the official IRS instructions or with a tax advisor before you use it. If you have self-employment income, also check the separate filing trigger: generally $400 in net earnings from self-employment. That order matters because filing requirement is tested first, including income you may later exclude under FEIE.

Apply FEIE, FTC, and separate reporting after the filing test#

Once filing is on the table, decide which relief actually fits. FEIE is not automatic. You must qualify and file a return reporting that income to claim it. FTC is meant to reduce double taxation on foreign-source income taxed by both countries, but you cannot claim FTC on the same income you exclude under FEIE.

If your income is split across countries, flows through an entity you own, involves investment structures, or includes a complex compensation package, get professional help before filing. This pairs well with our guide on How to handle 'royalty income' on your US tax return.

Pillar 1: Strategically Excluding Income with the FEIE#

FEIE works best when your income mostly comes from services you personally perform abroad and your records clearly support one qualification path. It is usually a poor fit if most of your income is unearned. It is also a poor fit if you expect it to reduce self-employment tax, or if your travel pattern makes qualification hard to prove.

Confirm FEIE matches your income#

Start by checking the income itself. FEIE applies to foreign earned income such as wages, salaries, professional fees, and similar pay for services you performed. It does not apply to unearned income such as dividends, interest, capital gains, pensions, annuities, or Social Security.

For tax year 2026, the maximum exclusion is $132,900 per qualifying person, and $130,000 for 2025. FEIE can reduce regular income tax, but it does not reduce self-employment tax.

FEIE is never automatic. You must file a U.S. return and claim it on Form 2555. If the form is incomplete or inaccurate, the exclusion or deduction can be disallowed.

Choose your qualification path#

Pick the path that matches your actual facts, not the one that looks easier on paper.

| Path | When it usually fits | What to document |

|---|---|---|

| Bona fide residence test | You are genuinely settled abroad for an uninterrupted period that includes a full tax year (for calendar-year taxpayers, Jan 1-Dec 31). | Tax home date(s), bona fide residence date(s), and records that support your residence pattern. |

| Physical presence test | You are mobile, newly abroad, or moving between countries. | Day-count log proving 330 full days in foreign countries during any 12 consecutive months, plus U.S. presence tracking. |

For physical presence, the qualifying days do not need to be consecutive. Each day must be a full midnight-to-midnight 24-hour day, and time on or over international waters does not count. If you miss 330 days, that test fails regardless of the reason.

Run a quick eligibility checklist#

Before you claim FEIE, make sure the basic pieces line up:

| Requirement | What to confirm | Article note |

|---|---|---|

| Tax home | Your tax home is in a foreign country, meaning your main place of business, employment, or post of duty. | Basic piece that must line up before you claim FEIE. |

| Income type | The income you want to exclude is earned from services you performed. | Basic piece that must line up before you claim FEIE. |

| Qualification path | You qualify under one path, either bona fide residence or physical presence. | Basic piece that must line up before you claim FEIE. |

| Travel records | Your travel records reconcile to your chosen path and the details you will report on Form 2555. | If your records do not support each item, fix that before you file. |

If your records do not support each item, fix that before you file.

Separate excludable vs non-excludable income#

This is where FEIE claims often go wrong. Sort the income before you calculate anything.

| Income bucket | FEIE status | Immediate next action |

|---|---|---|

| Salary/wages for services performed abroad | Can be excludable up to the annual FEIE limit if you qualify | Report on return and compute on Form 2555 |

| Freelance/consulting fees for services performed abroad | Can be excludable up to the annual FEIE limit if you qualify | Compute on Form 2555 and separately account for self-employment tax |

| Dividends, interest, capital gains | Not FEIE income | Keep in taxable-income workflow; do not place in FEIE bucket |

| Pensions, annuities, Social Security, other unearned income | Not FEIE income | Report under their own rules; do not place in FEIE bucket |

If you also qualify for housing relief, use the right version based on how the expense was funded:

- Foreign housing exclusion applies only to employer-provided amounts.

- Foreign housing deduction applies only to amounts paid with self-employment earnings.

- Base housing amount uses the 16% formula prorated by qualifying days.

- General housing expense limitation is generally 30% of the FEIE maximum, $39,870 for 2026; $39,000 for 2025.

- Verify the applicable IRS housing limits for your tax year and facts before finalizing the calculation.

Escalate early in complex cases#

Some FEIE issues are not worth guessing through. Consider bringing in a cross-border tax professional before filing if you have a split-year move, frequent U.S. travel that affects day counts, mixed employee and self-employed income, or uncertainty about which test you meet. Do the same if you previously revoked FEIE and want to use it again, because re-choosing within 5 tax years requires IRS approval. Related: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Pillar 2: When the Foreign Tax Credit is Your Smarter Financial Move#

If you already pay meaningful foreign income tax, test the Foreign Tax Credit before you default to FEIE. IRS guidance says a credit is usually better than a deduction. A credit reduces U.S. tax liability dollar for dollar, while a deduction only reduces taxable income. For a given tax year, you generally choose either the credit or the deduction for all qualified foreign taxes, and you can change that choice year to year. In practice, FTC can be a steadier starting point when you have mixed income types or want flexibility across years.

| Choice | Practical effect on your U.S. return | Placeholder example |

|---|---|---|

| Foreign tax credit | Reduces U.S. income tax liability dollar for dollar, subject to the FTC limitation | If creditable foreign tax is $Y, U.S. tax on foreign-source income can be reduced by up to $Y |

| Foreign tax deduction | Reduces taxable income, not tax liability directly | If deductions increase by $Y, tax savings are your marginal rate x $Y |

| FEIE | Excludes qualifying foreign earned income; taxes tied to excluded income are not creditable | If salary is excluded on Form 2555, foreign taxes on that excluded salary cannot also be claimed for FTC |

-

Use this decision default first. FTC is often a practical starting point when local taxes apply to wages, freelance income, dividends, or interest. FEIE may still be the better fit in some earned-income situations when your Form 2555 qualification is solid. A blended approach can make sense when part of your earned income is excluded but other foreign-source income remains in FTC categories.

-

Run an include/exclude check before you calculate. Include foreign income taxes, war profits taxes, excess profits taxes, or taxes in lieu of those taxes. Exclude VAT, sales taxes, property taxes, and amounts you did not legally owe or can recover by refund. For each included item, keep records showing the foreign country (or U.S. possession), related foreign income, and your share of foreign taxes paid. Keep excluded levies in a separate folder so they do not get pulled into Form 1116 support.

-

Follow a clean FTC process. Categorize income by Form 1116 basket, prepare separate Form 1116s by category, map each foreign tax amount to the matching category, convert and report in U.S. dollars, apply the FTC limitation, then validate carryback and carryforward treatment. Verify current rule details in the official IRS instructions or with a tax advisor before you rely on them. If you use the simplified path for no more than $300 of foreign taxes, or $600 if filing jointly, confirm all eligibility conditions first because that election does not allow carrybacks or carryovers for that year.

-

Check long-term fit before filing. FTC can be stronger for longer-range planning because unused credit above the limitation may be carried back one year and forward up to 10 years under IRS rules. If retirement contribution planning matters, verify IRA compensation treatment directly instead of assuming FEIE or FTC settles it by itself. Talk to a cross-border tax professional when you have multi-country income, entity structures, foreign and U.S. tax-year mismatch, treaty-dependent outcomes, or uncertainty in category allocation and Schedule B carryovers.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

The FEIE vs. FTC Decision Matrix: Which Path Optimizes Your Position?#

Once you understand each tool on its own, compare them in the same order every time: tax environment, income type, long-term impact, then election. That sequence helps you avoid claiming credits on excluded income, missing Form 1116 category issues, or locking yourself into an election that works poorly next year.

Gather decision inputs first#

You can only claim FEIE or FTC by filing a U.S. return, so build one file that supports both paths from the start.

At minimum, collect your foreign return or assessment, withholding statements, proof of payment, and a country-by-country income summary. Also keep a clean split between earned and non-earned income.

For FEIE, confirm eligibility before modeling outcomes. Your tax home must be in a foreign country, and your qualification path must be documented. If you are using the physical presence test, keep support for at least 330 full days in a 12-month period.

Compare tax environment before form mechanics#

Start with the likely result on the same income dollars, not with generic labels like high-tax or low-tax.

| What your facts look like | Path to test first | Why this can be the better first test | What to validate |

|---|---|---|---|

| Foreign income taxes on wages or self-employment income are likely to offset most or all U.S. tax on that same income | FTC | A credit reduces U.S. tax liability directly; unused credit may carry back 1 year and forward 10 years | Taxes are creditable, tied to the same foreign-source income, and mapped to the correct Form 1116 category |

| Foreign income tax is light, zero, or not usable as a credit | FEIE | Excluding qualifying foreign-earned income may give stronger immediate relief | Foreign tax home, 330-day support if applicable, and earned income compared with the 2026 FEIE cap of $132,900 per qualifying person |

| You have taxed earned income plus untaxed or differently taxed streams | Split approach | FEIE may cover part of earned income while FTC may fit the remaining or non-earned income | Map each income stream to one treatment, and do not claim FTC on taxes tied to excluded income |

Also factor in FEIE stacking. When you exclude earned income, tax on non-excluded income is computed at the rates that would have applied without the exclusion.

Classify income before choosing#

Do not choose between FEIE and FTC until the income is sorted correctly. FEIE applies to foreign-earned income from personal services, such as wages, salaries, and professional fees. Qualifying self-employment income may be excluded for regular income tax, but FEIE does not reduce self-employment tax.

FTC can be more flexible on mixed-income returns because Form 1116 is category-based, and passive income sits in a separate category. You may need separate Form 1116 filings by category.

A practical hybrid is FEIE for qualifying earned income up to the allowable amount. FTC can then apply to foreign taxes tied to foreign-source income that is not excluded, including passive income where applicable. The guardrail is simple: do not claim FTC on taxes tied to excluded income. Doing that can cause one or both FEIE elections to be treated as revoked.

Check long-term impact, then elect#

This year's answer is not always next year's, so test the choice against likely changes before you file.

Use this decision checklist:

- Retirement contribution implications: Apply required add-back adjustments for excluded FEIE and housing amounts when determining compensation for IRA limits.

- Multi-year flexibility: FTC may create carryback or carryforward value. FEIE continuity and revocation rules can make switching less flexible.

- Recordkeeping burden: FEIE needs strong tax-home and day-count records. FTC needs payment proof, category mapping, and clean Form 1116 support.

- Expected profile changes: Re-test if you may move countries, add passive income, or exceed the FEIE ceiling.

Once you elect FEIE, it continues unless revoked. If revoked, re-choosing within 5 tax years requires IRS approval.

Escalate before filing if any of these apply:

- Mixed income streams, especially earned income plus dividends, interest, royalties, or capital gains

- Tax exposure in more than one foreign country

- Uncertainty about which foreign taxes are creditable or how to classify them on Form 1116

- Unclear tracing between taxes on excluded versus non-excluded income in a hybrid approach

- Planned FEIE election changes with uncertain downstream consequences

Before you lock in FEIE or FTC, run your own scenario with the FEIE calculator.

Pillar 3: Neutralizing the Single Biggest Expat Financial Risk (FBAR)#

After you choose FEIE, FTC, or a hybrid, make FBAR your next compliance check. In practice, the job is straightforward: confirm the trigger, identify the right accounts, file FinCEN Form 114 separately and on time, and escalate quickly if prior years are missing.

Start with a full-year account inventory that shows the institution, account type, ownership, joint holders, signature or transfer authority, and each account's highest value during the year.

Confirm the filing trigger (aggregate test)#

The trigger is the combined value of reportable foreign financial accounts, not the balance in any one account. You file an FBAR if the combined value of your reportable foreign financial accounts exceeded $10,000 at any point in the calendar year. Do not exclude an account just because it produced no taxable income. That does not determine FBAR reportability.

Scope accounts by control, not just account title#

FBAR review turns on interest or authority, not just whose name appears on the statement.

| If this is true | Treat as in-scope for FBAR review |

|---|---|

| You have a financial interest | Yes |

| The account is jointly held (including with a spouse) | Yes |

| You have signature or other authority over the account | Yes |

If any row is yes, include that account in your FBAR review set. For spouse filings, IRS guidance includes an authorization path using FinCEN Form 114a, but do not assume one spouse filing automatically covers both without confirming the setup requirements. For retirement-related accounts, IRS examples include certain exceptions, so verify account type before assuming treatment.

File with the right form, in the right place, on the right date#

FBAR is separate from Form 1040. You file electronically as FinCEN Form 114 through FinCEN's BSA E-Filing System.

Deadline mechanics are simple:

- Due date: April 15 for the prior calendar year

- Automatic extension: October 15

- No separate extension request required

Your last check is also simple: confirm FinCEN Form 114 was actually submitted. Filing Form 1040 or other international forms does not replace FBAR.

If prior years are missed, treat this as an escalation point#

Missed FBARs are where DIY confidence often breaks down. Penalty exposure is highly fact-specific, and willful versus non-willful is not something you should self-label casually.

| Standard | Reference point | Practical read |

|---|---|---|

| Non-willful | Up to $16,536 (table amount for penalties assessed on or after January 17, 2025; verify current table timing before filing decisions) | After Bittner, the non-willful maximum generally applies per annual FBAR form, not per account. |

| Willful | Greater of $100,000 or 50% (statutory formula); current table amount includes $165,353 (verify current table timing) | Civil penalties may apply, and IRS guidance also notes possible criminal consequences depending on facts. |

Talk to a professional now if any of these apply:

- You missed one or more prior-year FBARs

- You are unsure whether your facts are non-willful

- You have complex ownership or signature-authority facts you cannot classify confidently

- You hold foreign retirement or other account arrangements with unclear treatment

- You are considering delinquent or streamlined options and are unsure whether you meet eligibility conditions (including exam or investigation status)

For another practical international tax walkthrough, see How to Calculate Depreciation on a Foreign Rental Property.

From Anxiety to Agency: Owning Your Global Financial Strategy#

Treat this as a repeatable review cycle, not a once-a-year scramble. When you separate tax treatment, relief eligibility, and reporting risk into a simple routine, the work gets much easier to control.

Give each pillar one clear job#

FEIE is a tax-treatment election for qualifying foreign earned income on Form 2555. To qualify, you need a foreign tax home and must meet either the bona fide residence test or the physical presence test. If you are using physical presence, that means 330 full days in a 12-month period. FTC is a relief mechanism that can reduce U.S. tax when the same income is taxed by a foreign country, and you cannot claim FTC on income excluded under FEIE. FBAR is separate Treasury reporting when the aggregate value of foreign financial accounts exceeds $10,000 at any point in the year, even if the accounts do not generate taxable income.

| Pillar | Role | Key trigger or constraint |

|---|---|---|

| FEIE | Tax-treatment election for qualifying foreign earned income on Form 2555. | Requires a foreign tax home and either the bona fide residence test or 330 full days in a 12-month period under physical presence. |

| FTC | Relief mechanism that can reduce U.S. tax when the same income is taxed by a foreign country. | You cannot claim FTC on income excluded under FEIE. |

| FBAR | Separate Treasury reporting for foreign financial accounts. | Required when the aggregate value of foreign financial accounts exceeds $10,000 at any point in the year. |

Verification check: if you cannot place each item in the right bucket, pause before filing.

Run a monthly or quarterly four-part review#

Run a monthly or quarterly review with four checks:

- Income classification: mark income as earned or not earned, and record where services were performed.

- Tax-position review: decide whether FEIE or FTC is the first method to test for this year.

- Account-reporting review: update your foreign account list and each account's highest balance point.

- Documentation readiness: tie each income item and tax payment to supporting records such as an invoice, payslip, assessment, receipt, or statement.

Bank feeds alone may not be enough because they can blur transfers, reimbursements, tax payments, and income.

Use trigger-based decisions#

Use trigger-based decisions so you are not rethinking everything from scratch every filing season:

- Favor FEIE-first testing when you can substantiate foreign tax home status and FEIE qualification under either bona fide residence or the 330-day physical presence rule.

- Favor FTC-first testing when foreign income taxes may be used to reduce U.S. tax on the same income.

- Escalate FBAR cleanup immediately if foreign accounts crossed the $10,000 aggregate threshold and your maximum-balance support is incomplete.

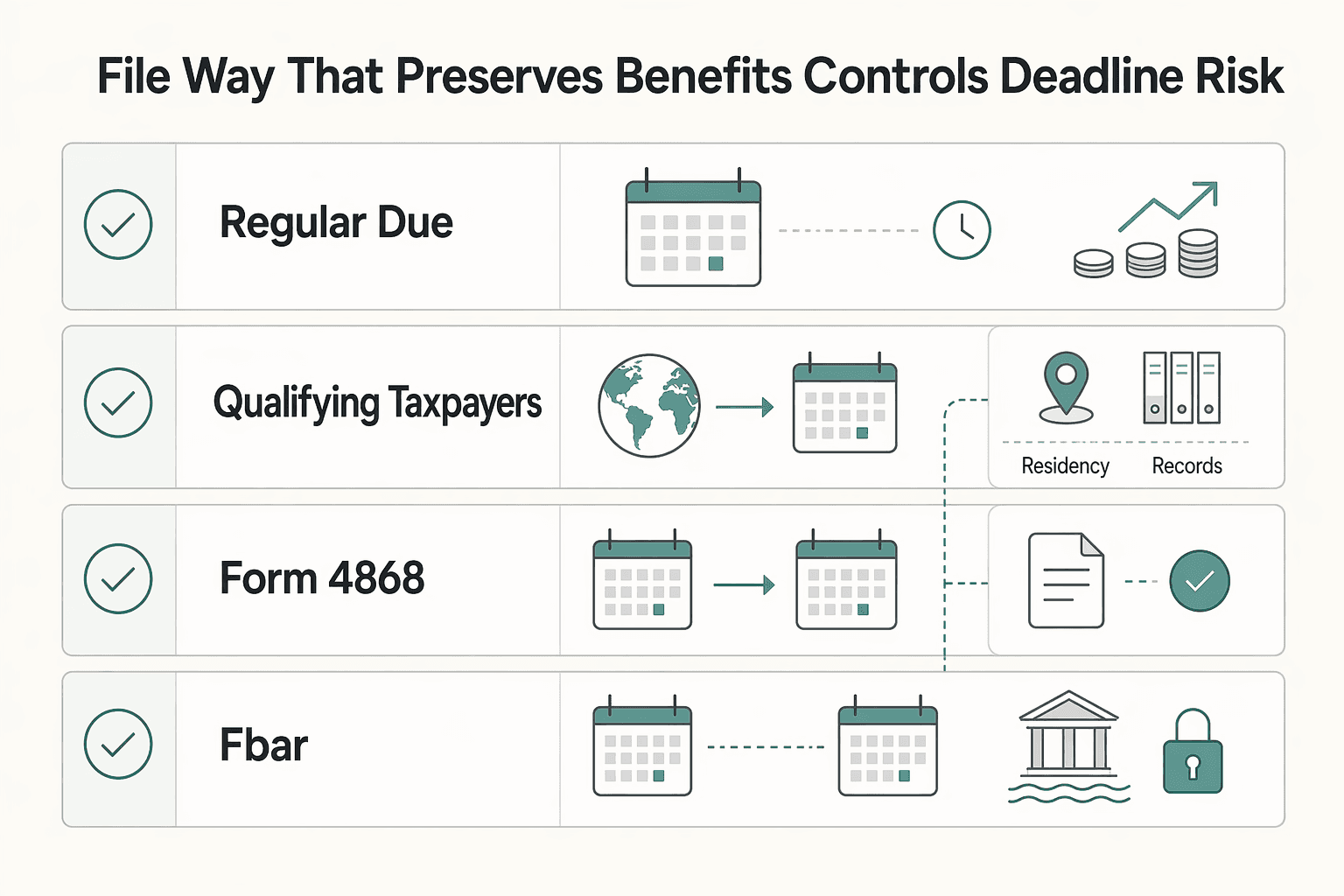

File in a way that preserves benefits and controls deadline risk#

File in a way that preserves benefits and controls deadline risk. If you want FEIE or FTC benefits, you must file a U.S. return. Qualifying taxpayers abroad generally move from the regular April 15 due date to an automatic June 15 filing date, and Form 4868 can request an extension to October 15. Interest on unpaid tax still accrues after the regular due date. FBAR is due April 15 with an automatic extension to October 15.

| Filing item | Date or timing | Note |

|---|---|---|

| Regular due date | April 15 | Interest on unpaid tax still accrues after the regular due date. |

| Qualifying taxpayers abroad | Automatic June 15 filing date | Applies to the U.S. return. |

| Form 4868 extension | October 15 | Can request an extension to this date. |

| FBAR | April 15 | Automatic extension to October 15. |

Quick execution checklist:

- Choose FEIE or FTC based on this year's facts

- Maintain one evidence pack year-round

- File required forms on time

- Confirm current filing deadlines with the IRS or a tax advisor

See A Step-by-Step Guide to Filling Out Form 2555 (Foreign Earned Income) for more detail. To keep this process low-stress year-round, track your travel and documentation in the tax residency tracker.

Frequently Asked Questions

What do FEIE, FTC, and worldwide income actually mean?

FEIE is a voluntary election on Form 2555 that lets you exclude qualifying foreign earned income from U.S. taxation. FTC reduces your U.S. tax liability using eligible foreign income taxes you paid or accrued. Worldwide income starts with income from all worldwide sources, and for earned income, where you performed the services matters more than where the money was deposited.

How do I choose between FEIE and FTC?

Start by checking your earned versus non-earned income mix, whether unused foreign tax credits could matter in other years, and whether you can meet FEIE eligibility rules. You cannot claim FTC on income you exclude under FEIE. If you revoke FEIE, re-electing it within 5 tax years requires IRS approval.

Do I still have to file a U.S. return if I live abroad?

Usually yes, if your worldwide gross income meets the filing threshold for your filing status. Check the current Form 1040 or Form 1040-SR instructions before deciding not to file. Keep a simple ledger with payer, income type, amount, currency, date earned, and your U.S. dollar conversion method.

How do I document the physical presence test for FEIE?

Use the exact rule: 330 full days in a 12-consecutive-month period. Keep one travel log and support it with passport stamps, flight confirmations, lodging receipts, and calendar entries. Each day must be a full midnight-to-midnight 24-hour day. Time on or over international waters does not count.

Does salary paid into a U.S. bank account still count as worldwide income?

Yes. Deposit location does not determine inclusion in worldwide income or whether earned income is foreign for FEIE purposes. Track where you performed the work and classify the income type first.

Can I use FEIE and FTC on the same income?

No. If you exclude foreign earned income or foreign housing costs, you cannot also claim FTC for taxes on that same excluded income. Keep excluded wages, foreign tax paid, and other foreign-source income separated before preparing Form 2555 and FTC calculations.

What records should I keep year-round so filing is not a rebuild project?

Keep one evidence pack with an income ledger, foreign tax assessments or payment receipts, a travel log, a year-end account list, and copies of filed Form 2555, FTC workpapers, and FinCEN Form 114. Make sure each foreign tax payment ties to a notice, payslip, or statement, and label each income item as earned or not earned. Bank feeds alone are not enough because they can blur revenue, reimbursements, transfers, and tax payments.

When do I need an FBAR, and when should I stop DIYing it?

You generally need an FBAR when the aggregate value of foreign financial accounts exceeds $10,000 at any point during the calendar year. You file it separately as FinCEN Form 114, so filing Form 1040 does not satisfy that requirement. Get professional help if your facts are complex, you cannot substantiate maximum balances, or you missed prior-year FBARs.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

Build a Freelance Media Kit That Reduces Client Friction

Treat your media kit as a buyer decision tool, not a design exercise. If a prospect can spot fit, proof, and the next action quickly, you cut a lot of avoidable back and forth before a call is scheduled. That is this document's job.