Quick Answer

Calculate how to calculate customer acquisition cost with a layered approach: first divide total acquisition spend by new clients in one period, then add the value of non-billable time, and finally adjust for hidden service burden and proposal-stage risk. Use Tier 1 for the baseline, Tier 2 for complexity, jurisdiction, and tooling load, and Tier 3 for payment and scope uncertainty. Keep LTV:CAC as a guardrail, with around 3:1 used as a common reference point.

--- Standard corporate metrics often break down for independent professionals. Customer Acquisition Cost, or CAC, is a good example. The textbook formula - total sales and marketing spend divided by new customers - leaves out your most valuable asset: your time.

If you want to protect profitability and keep the work sustainable, you need a better model. This three-tier framework replaces the standard formula with one that matches how you actually win work. It takes you from a simple calculation to a practical filter for identifying, pricing, and winning the right clients.

Tier 1: Your Foundational CAC (The True Cost of Time and Money)#

Start with one clean measurement window and put every cost and every new client into that same period. If you mix March spend with April wins, or count old pipeline work against new contracts, your baseline stops being useful.

For a business-of-one baseline, use the standard CAC numerator: total sales and marketing costs in that window. Define your inclusion rules upfront and apply them consistently, or your CAC becomes unreliable.

Choose one measurement window#

Pick a period you can actually audit, usually one month or one quarter. Then count only new clients acquired in that same window.

Before you calculate, document what you are including as acquisition cost and keep that definition stable over time. Include both marketing and sales costs in the same period so the result reflects the full acquisition cost pool.

Checkpoint: You should be able to tie each included cost and each new client to the same dated window.

Build your total acquisition cost#

Build one total numerator for that same window: all sales and marketing costs tied to acquiring new customers.

| Cost type | Include in CAC? | Common misclassification |

|---|---|---|

| Marketing spend (for example, ads, content, events) | Yes | Tracked in marketing reports but left out of CAC |

| Sales spend (for example, team costs, tools, commissions) | Yes | Treated as general overhead instead of acquisition cost |

A common failure mode is unclear cost-inclusion rules. Decide what is in and out before you calculate, then use that same rule set each period.

Calculate per-client CAC and handle thin periods#

Once the numerator is clean, use this formula: CAC = (Total Sales & Marketing Costs) / (Number of New Customers Acquired).

Example: if you spend $1,000 and gain 100 new customers in that period, CAC is $10.

If your new-customer count is very low, treat the result as directional, not precise. If you won zero new customers, you cannot compute per-customer CAC for that window; track the costs and reassess in the next review period.

Use that number to drive three immediate decisions. Your pricing floor has to cover acquisition and still leave margin. Your channel priorities should shift toward sources with better return. Your cost definitions should stay consistent so trend comparisons remain useful.

If you want a deeper dive, read How to Calculate Your Billable Rate as a Freelancer. For a quick next step, try the free invoice generator.

From Cost to Context: The LTV:CAC Ratio#

Use LTV:CAC to decide whether your acquisition spend is economically healthy, not just whether you are winning clients. The check is simple: LTV:CAC = LTV / CAC. If lifetime value does not stay above acquisition cost, growth becomes hard to sustain.

Estimate LTV by client segment#

Start with separate segments, then compare them: project-based, retainer, and hybrid. This keeps stronger performance in one segment from masking weak economics in another.

Use the contribution-based LTV structure as your anchor: LTV = m x T, where m is customer contribution margin and T is customer lifetime. If your cost-to-serve data is still limited, treat segment LTV as a provisional estimate and label it clearly.

Practical inputs to gather by segment:

- Project-based: average project value, expected repeat projects, and any usable cost-to-serve signal.

- Retainer: monthly revenue or contribution margin, plus average months retained.

- Hybrid: kickoff value, recurring value across expected months, and typical add-on value.

Checkpoint: tie each input to records you can inspect (invoices, scopes, renewals, start/end dates). If an input is assumed rather than observed, mark it as provisional.

Calculate ratio by segment first, then roll up#

Calculate LTV:CAC per segment before looking at a blended total. If you cannot yet split CAC by segment, use your Foundational CAC as a temporary denominator and mark confidence as lower.

| Client type | Revenue pattern | Retention pattern | Estimated LTV method | CAC ratio outcome | Recommended action |

|---|---|---|---|---|---|

| Project-based | One-time fee, occasional repeats | Usually short, may return later | Working estimate from project value and repeat pattern; refine with contribution margin when available | LTV:CAC ratio pending source-record verification | Tighten qualification or raise minimum engagement size if weak |

| Retainer | Recurring monthly value | Ongoing until churn | Working estimate from monthly value and retained months; refine with contribution margin when available | LTV:CAC ratio pending source-record verification | Protect and prioritize channels that produce this segment if strong |

| Hybrid | Kickoff plus recurring/add-ons | Mixed retention | Working estimate from kickoff + recurring + common add-ons over expected duration | LTV:CAC ratio pending source-record verification | Split low-value vs high-value hybrid profiles and route differently |

Then roll up: compare the total estimated LTV for clients won in the period against the total CAC for that same cohort.

Interpret quality and control cashflow#

Do not treat one ratio target as universal. A "good" CAC relationship depends on business model, industry, and company size. You can treat about 3:1 as directional only, then calibrate to your model. Verify any current benchmark range against source records before using it.

Track CAC payback period as a cashflow control metric: how long it takes client contribution to recover acquisition cost. If payback is too slow, act operationally: shift channel mix toward faster-recovery sources, tighten qualification, and adjust offer or pricing to improve earlier cash recovery.

Watch the two common failure modes: CAC above lifetime value (unsustainable), and CAC/CPA confusion (different metrics, different decisions).

Related: How to Find and Secure Public Speaking Gigs as a Freelancer.

Tier 2: Your 'Fully-Loaded' CAC (The Hidden Costs of Service)#

Use Fully-Loaded CAC when Foundational CAC looks fine but certain clients still erode margin. Keep the same reporting window, same customers won, and same denominator as Tier 1. Then add only the hidden burden tied to that client type, channel, or market.

Define the boundary before you add anything#

Start by locking what Tier 1 already includes. Foundational CAC often covers sales and marketing spend such as salaries, tools, ad budgets, and other acquisition-touching expenses. Teams define CAC differently, so your edge is not a "perfect" formula. It is a written scope you apply the same way over time so comparisons stay usable across quarters, channels, and geographies.

Treat Fully-Loaded CAC as a management layer, not a universal standard. Only add costs that are observable and tied to winning and activating a specific client profile.

Use this double-counting check before you calculate:

- If a cost is already in sales or marketing spend, do not add it again.

- If a cost applies equally to all clients, keep it in Foundational CAC.

- If a cost appears only in one channel, cohort, market, or client type, add it only to that slice.

- If you cannot trace it to a calendar record, invoice, software bill, consultant fee, or admin log, mark it as provisional.

Checkpoint: Use one period (for example, a quarter or year) and divide spend by customers acquired in that same period.

Convert each hidden burden into a per-client cost#

Use the same three buckets every cycle: Complexity, Jurisdiction, and Tooling. Measure the extra burden, record the evidence source, and allocate it either directly to one client or across the relevant segment.

| Hidden cost driver | How to measure | Where the data comes from | How to allocate to one client | Operational response |

|---|---|---|---|---|

| Complexity | Extra unbillable hours for calls, revisions, onboarding, coordination | Calendar, timesheets, PM notes, email threads | Convert hours using the same internal hourly value from Tier 1; assign directly if unique, or spread across similar clients in that cohort | Tighten qualification, cap revisions, simplify onboarding, narrow proposal options |

| Jurisdiction | Extra admin time and external fees for market-specific paperwork, invoicing requirements, tax review, payment setup | Admin logs, accountant invoices, onboarding checklists, payment records | Assign directly when client-specific; otherwise spread across clients won in that market during the same period | Limit market coverage, standardize templates, require simpler payment rails, raise minimum deal size |

| Tooling | Software seats, portal fees, consultancy, setup work required only for this client type | Vendor invoices, subscription receipts, implementation notes | Assign directly if one-client only; otherwise amortize across expected clients in that channel or cohort | Bundle setup into first contract, avoid low-value one-offs, renegotiate requirements |

If hour estimates are rough but ad spend is exact, flag that gap. Update estimates after onboarding so the next cycle uses stronger inputs.

Stress-test cross-border admin burden and use the result#

Cross-border work is where hidden CAC often spikes. Run a repeatable screen before you price:

| Check | What to review | Possible burden |

|---|---|---|

| Documentation | Extra tax, vendor, or withholding documentation for their market and your entity type | Added time and outside-advisor cost |

| Invoice requirements | Invoice format, fields, language, numbering, or supporting details | Manual work |

| Payment and approvals | Required payment method or approval flow | Fees, FX friction, or delay |

Log added time, outside-advisor cost, and market. Then segment results by geography or market so decisions are practical.

Decision output before Tier 3:

- If Fully-Loaded CAC rises from Complexity, qualify harder and simplify scope earlier.

- If it rises from Jurisdiction, narrow accepted markets or payment requirements until the process is repeatable.

- If it rises from Tooling, raise minimum engagement size or deprioritize channels that require one-off setup.

For a step-by-step walkthrough, see How to Calculate and Manage Churn for a Subscription Business.

Tier 3: Your 'Risk-Adjusted' CAC (Pricing for Peace of Mind)#

Apply this layer before you send pricing or terms. If payment reliability, scope clarity, or decision flow is uncertain, your Fully-Loaded CAC is only a baseline, not your real exposure.

For each opportunity, keep these together in one record: Fully-Loaded CAC, working LTV estimate, and draft commercial terms. CAC is a profitability guardrail, but the decision is stronger when you evaluate CAC and LTV together.

Use risk bands, then map to action#

Start with risk bands and avoid false precision. Classify each deal as Low, Watch, or High risk from proposal-stage evidence, then map each band to your internal multiplier and term changes.

Use this decision rule: if the risk-adjusted view pushes expected LTV:CAC below your minimum floor, do not send standard terms. A 3:1 ratio is a common guide, but your floor should match your model and channel reality.

| Risk band | Evidence pattern at proposal stage | Default response |

|---|---|---|

| Low | Signals are clear and consistent across payment, scope, stakeholders, timeline | Use standard pricing and standard terms |

| Watch | Mixed or incomplete signals; one or more open risks | Keep pricing under review and tighten terms before kickoff |

| High | Multiple unresolved risks, or one issue that can materially delay payment or expand work | Do not use standard terms; reprice, restructure, or decline |

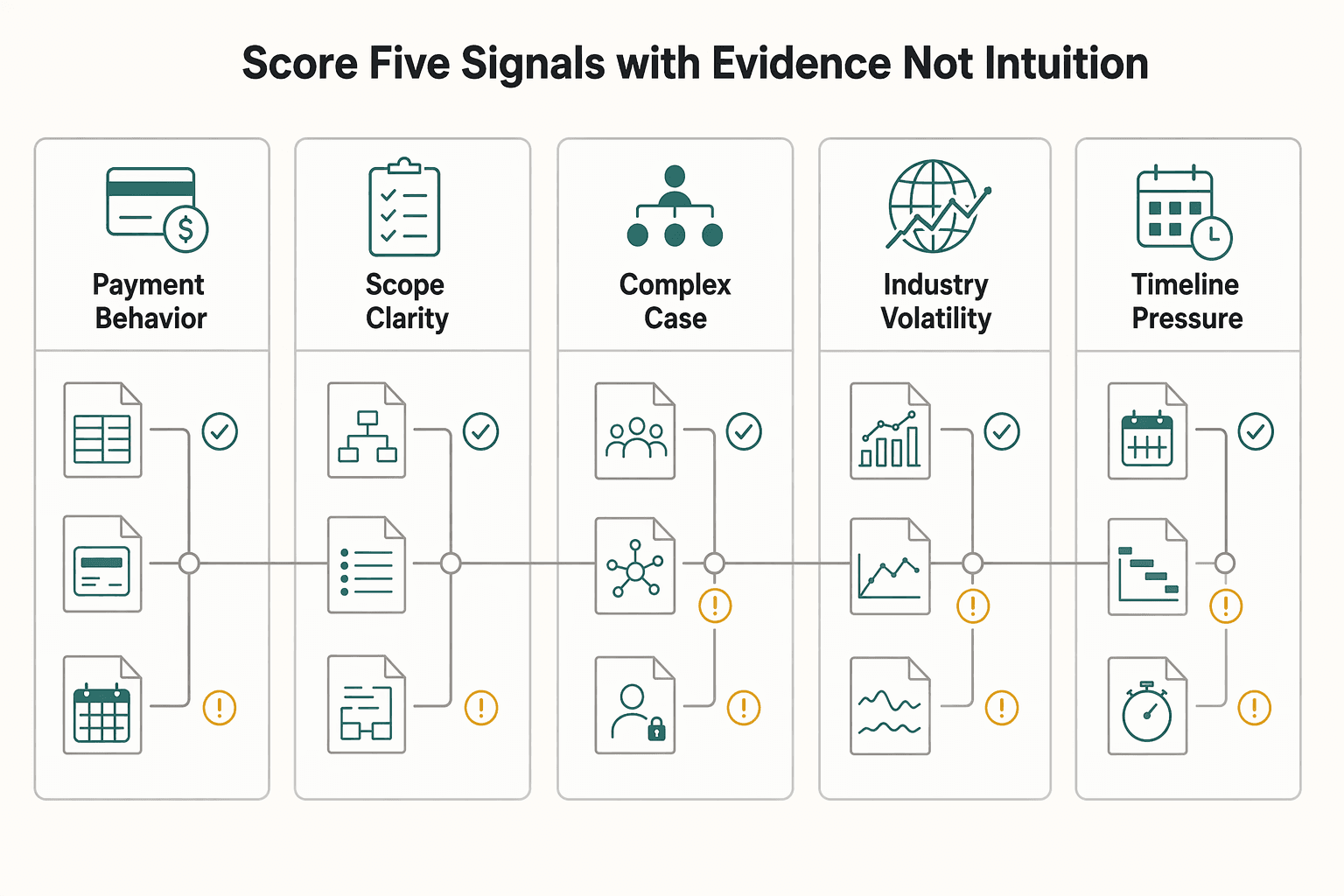

Score five signals with evidence, not intuition#

Use the same five signals every time: payment behavior, scope clarity, stakeholder complexity, industry volatility, and timeline pressure.

| Risk signal | How to verify | Impact on Risk-Adjusted CAC | Contract or pricing response |

|---|---|---|---|

| Payment behavior | Check requested terms, prior invoice aging for repeat clients, procurement steps, and willingness to discuss deposits | Higher collection risk raises carrying cost and erodes CAC efficiency | Set deposit trigger (current threshold pending source-record verification), shorten billing cycle (current interval pending source-record verification), pause work at unpaid threshold (current threshold pending source-record verification) |

| Scope clarity | Count unresolved deliverables, assumptions, dependencies, and revision points in proposal/SOW | Ambiguity increases rework risk and makes CAC understate total effort | Lock scope baseline, require written change orders, pre-price out-of-scope paths |

| Stakeholder complexity | Count approvers, teams, legal/procurement reviews, and external sign-offs named pre-kickoff | More handoffs increase coordination time and approval drag | Name decision owner, set explicit approval gates, align timeline to review cycle |

| Industry volatility | Review how often budgets, demand, or priorities change in that segment | Lower predictability reduces confidence in expected LTV | Shorten commitment window, bill earlier, tighten cancellation language |

| Timeline pressure | Compare requested turnaround with your normal lead time and required dependencies | Rush conditions increase coordination load and revision risk | Apply rush logic where justified, phase delivery, define exclusions in writing |

If you cannot tie a signal to real artifacts (email, SOW draft, payment-term request, invoice history, procurement notes), mark it as provisional.

Use a protection playbook for Watch and High deals#

Do not rely on price alone. Add operating controls before kickoff:

- Design milestones around decision points and written approvals.

- Apply your deposit policy using internal triggers (current threshold pending source-record verification).

- Enforce a change-order workflow: no out-of-scope start until fee, timing, and owner are confirmed in writing.

- Set invoice follow-up cadence up front (reminder/escalation cadence pending source-record verification).

This is where payment-delay and scope-creep risk gets contained in advance, not after margin is already lost.

Make go/no-go decisions from a reusable checklist#

Use one qualification checklist per lead. Green-light when the expected profile is High LTV, Low Fully-Loaded CAC, and Low Risk-Adjusted CAC. Move carefully when one area is weak. Treat as no-go when two areas are weak and terms cannot close the gap.

| Decision | Condition |

|---|---|

| Green-light | Expected profile is High LTV, Low Fully-Loaded CAC, and Low Risk-Adjusted CAC |

| Move carefully | One area is weak |

| No-go | Two areas are weak and terms cannot close the gap |

Then review this by channel. If one source repeatedly fails your risk-adjusted threshold, do not scale it until it clears your written gate and expected LTV:CAC floor.

Related: How to Set and Track KPIs for Your Freelance Business.

From Metric to Mindset: Building a Resilient Business#

Use CAC as a weekly decision filter, not just a reporting metric. Your goal is to decide who to pursue, how to scope and price, which payment terms to set, and when to decline work before margin or cashflow gets damaged.

| Tier | When to use | Focus |

|---|---|---|

| Tier 1 | First gate | Calculate CAC the same way every time and include the full acquisition picture |

| Tier 2 | Before you quote | Pressure-test service complexity and operational load |

| Tier 3 | Before you say yes | Treat payment friction as part of the acquisition reality |

Use Tier 1 as your first gate#

Start by calculating CAC the same way every time: total acquisition costs divided by new customers in the same period. Include the full acquisition picture, not just ad spend, so the number is usable for decisions. If you cannot show what counts as a CAC expense, pause and fix that policy before acting on the metric.

Use Tier 2 to scope before pricing#

Before you quote, pressure-test service complexity and operational load so you do not underprice a hard-to-serve client. Then check whether the deal still clears your sustainability test; a common reference point is an LTV:CAC ratio of at least 3:1. If it does not, re-scope, re-price, or pass.

Use Tier 3 to protect collection risk#

Before you say yes, treat payment friction as part of the acquisition reality. If approval chains, payment timing, or similar risk signals increase effort and uncertainty, tighten terms or walk away instead of accepting thin-margin work.

What changes in practice:

- Qualify lead fit using your Tier 1 CAC method.

- Scope the offer and workload risk with Tier 2.

- Set payment terms and controls with Tier 3.

- Decline deals that still fail your margin and collection checks after adjustments.

| Lens | Metric-only CAC thinking | Resilience mindset CAC thinking |

|---|---|---|

| Focus | Lower acquisition cost | Profitable, collectable customers |

| Behavior | Optimize lead cost in isolation | Qualify, scope, price, and terms together |

| Likely outcome | More wins, volatile cashflow | Fewer bad-fit wins, steadier margins |

Weekly review checklist:

- Confirm your CAC expense policy is documented and data capture is complete.

- Flag channels or leads below your LTV:CAC floor (

[verify your current floor]; 3:1 is a common reference point). - Recheck quotes where scope complexity increased after discovery but pricing did not.

- Validate payment terms against your current risk triggers (

[verify deposit rule],[verify approval-chain limit],[verify late-pay trigger]). - Separate any large one-time acquisition cost and review it across the period it is expected to support.

Related: How to Calculate the All-In Cost of an International Payment.

Frequently Asked Questions

How do you calculate customer acquisition cost for a service business?

For a service business, divide your total acquisition spend in a defined period by the number of new paying clients won in that same period. Include marketing and advertising costs, sales salaries or equivalent selling labor, and related overhead. Do not divide by leads, trials, or calls instead of actual new customers.

What is the difference between CAC and CPA?

CAC is the cost to win a paying customer. CPA is the cost to get a non-customer action such as a lead or trial. If you are comparing channels, use CPA for early funnel efficiency and CAC for actual revenue decisions, and do not treat cheap leads as proof that a channel is profitable.

What is a good CAC?

There is no single good dollar figure that fits every business. Judge it against your LTV:CAC ratio and your channel economics. A commonly cited strong relationship is around 3:1, but it is not a universal rule.

What if you win zero new clients in a period?

Using the standard formula, CAC is not interpretable for that period because there are no new customers in the denominator. Keep that period’s spend logged and evaluate performance over a longer comparable window; these sources do not define a separate validated CAC method for zero-acquisition periods.

How do you reduce CAC without increasing payment risk?

Use analytics to identify which channels actually convert, then shift effort toward those channels and keep testing new ones. Evaluate channel performance with CAC alongside LTV so you can avoid channels that hurt profitability over time. The grounding here does not establish payment-term or contract controls as a proven CAC-reduction method.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 6 external sources outside the trusted-domain allowlist.

- acquisition.gov/sites/default/files/page_file_uploads/RFO.pdftrusted

- online.hbs.edu/blog/post/ltv-cactrusted

- adapty.io/blog/customer-acquisition-costexternal

- andrewchen.com/how-to-actually-calculate-cacexternal

- bloomreach.com/en/blog/cac-vs-cpa-how-to-cut-marketing-cost...external

- buildwithtoki.com/blog-post/calculating-cost-of-customer-acqui...external

- chartmogul.com/blog/customer-acquisition-cost-cacexternal

- commonthreadco.com/blogs/coachs-corner/customer-acquisition-cos...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Calculate a Freelance Rate You Can Actually Get Paid On

A workable rate is not the neat number a calculator produces. It is the number that still works after you account for real billable capacity, non-client time, scope drift, and the gap between sending an invoice and receiving cleared cash. Start with hourly math even if you do not plan to bill hourly, then turn that number into a quote with clear `payment terms`.

How to Set and Track KPIs for Your Freelance Business

Better decisions matter more than more metrics. The practical goal is to finish each review knowing what to change next, who owns that change, and when you will verify whether it worked.

How to Find and Secure Public Speaking Gigs as a Freelancer

---