Quick Answer

Start with compliance, then execution: for how to buy us stocks in australia, confirm tax status, file W-8BEN correctly, choose a broker only after verifying full landed costs and custody disclosures, and run a repeatable records process. Keep parcel-level data for each buy and sell, including commissions, foreign tax, and AUD conversion inputs. If U.S.-person status may apply, check FBAR triggers at the $10,000 aggregate account level and filing dates (April 15, with automatic extension to October 15) before trading.

Buying US stocks from Australia is straightforward when you place the trade. What usually erodes the result later is the admin. Set up your tax status first, choose a broker you can verify on cost and custody, and keep a record system you can repeat from the first trade.

Get that structure right before you place the first order. These three pillars turn a one-off trade into a process you can run cleanly over time.

Pillar 1: Build Your Compliance Fortress#

Start with your tax status before you compare brokers. If you get that wrong, every later choice gets messier.

Before you start: have your tax residency facts, tax file numbers, and a folder ready for broker statements and trade confirms.

- Confirm your status first. Work through the ATO residency tests before assuming you are only an Australian tax resident. If your facts are messy, start with A Guide to Tax Residency in Australia for Digital Nomads.

Checkpoint: you should be able to say, in one sentence, whether you are only an Australian tax resident or whether you may also be a U.S. person.

| Your situation | Likely filings to prepare for | Who to confirm with before lodging |

|---|---|---|

| Only Australian tax resident | Australian return reporting Australian and overseas income; possible FITO claim | Australian tax agent or accountant |

| You may also be a U.S. person | Australian return plus possible U.S. filings, including FBAR on FinCEN Form 114 if triggers apply | Cross-border tax adviser |

- Complete Form W-8BEN correctly. Give it to the withholding agent or payer when requested. This form supports foreign status and, if you are treaty eligible, can support reduced U.S. withholding instead of the default 30% on U.S. source income.

Avoid these mistakes: claiming treaty benefits without being treaty resident, using mismatched residency details, omitting the required TIN information, or forgetting that a change in circumstances can invalidate the form before the end of the third succeeding calendar year. Set two reminders: one for renewal and one for any address or residency change.

- Capture ATO records at parcel level from day one. For each parcel and each disposal, record at least the purchase date and purchase amount, sale price, commissions, and the foreign-tax and AUD-conversion details needed for Australian reporting and any FITO claim. Separately acquired parcels are separate CGT assets. Keep records for 5 years after disposal.

Failure mode: relying only on year-end summaries. They often miss the parcel-level detail you need for capital gains, the 12-month CGT discount test, and FITO calculations.

- Escalate if U.S.-person status is possible. FBAR is not for every Australian investor. It applies to U.S. persons if aggregate foreign financial accounts exceed $10,000 at any time during the year, with filing due April 15 and an automatic extension to October 15. Civil and criminal penalties may apply, so if your status is unclear, get specialist advice before you place trades.

If you want a deeper dive, read A Deep Dive into Form 5472 for Foreign-Owned US LLCs.

Pillar 2: Select a Broker Like a CFO#

Choose your broker with a pre-funding workflow, not a promo page. If cost, custody, and reporting are all verifiable before you deposit, you are usually choosing the safer long-term option, even when the headline trading fee is not the lowest.

1) Build a landed-cost sheet before opening the account#

Use the broker's current fee schedule, PDS, FSG, and account terms. Only enter figures you can trace back to those documents.

| Cost item | Broker 1 | Broker 2 | Broker 3 |

|---|---|---|---|

| Brokerage fee per US trade | Current brokerage fee pending platform verification | Current brokerage fee pending platform verification | Current brokerage fee pending platform verification |

| FX spread disclosure over benchmark rate | Current FX spread pending platform verification | Current FX spread pending platform verification | Current FX spread pending platform verification |

| Deposit or funding fee | Current deposit or funding fee pending platform verification | Current deposit or funding fee pending platform verification | Current deposit or funding fee pending platform verification |

| Withdrawal or wire transfer fee | Current withdrawal or wire fee pending platform verification | Current withdrawal or wire fee pending platform verification | Current withdrawal or wire fee pending platform verification |

| Inactivity or platform fee | Current inactivity or platform fee pending platform verification | Current inactivity or platform fee pending platform verification | Current inactivity or platform fee pending platform verification |

| Transfer-out fee | Current transfer-out fee pending platform verification | Current transfer-out fee pending platform verification | Current transfer-out fee pending platform verification |

| Final landed cost for your typical use case | Current landed cost pending platform verification | Current landed cost pending platform verification | Current landed cost pending platform verification |

Do not look at commission alone. Include transfer, inactivity, wire, and other non-obvious fees, and treat vague FX pricing as a cost risk.

2) Run custody and insolvency due diligence#

Work through this checklist before you fund the account:

| Check | Where to confirm | Pass if... |

|---|---|---|

| Australian licensing/registration scope | ASIC professional registers + broker legal entity details | The entity and service scope match what is being offered to you |

| Custodian/clearing identity | Broker PDS/FSG/custody or account terms | Named parties are explicit, not implied |

| Client asset segregation | Broker custody/client money disclosures | Segregation approach is clearly described |

| Insolvency handling | Broker legal disclosures/terms | Process is explained, including claims/liquidation pathway |

| US-side firm background (if used) | FINRA BrokerCheck | Firm/person records are consistent with broker disclosures |

| SIPC claim (if made) | Official SIPC membership context + broker disclosure | Coverage scope is clearly stated; you understand it is for broker failure, not market losses |

Treat an AFS licence as a gate, not a quality badge. If custody language is marketing-heavy but the legal structure is unclear, do not proceed.

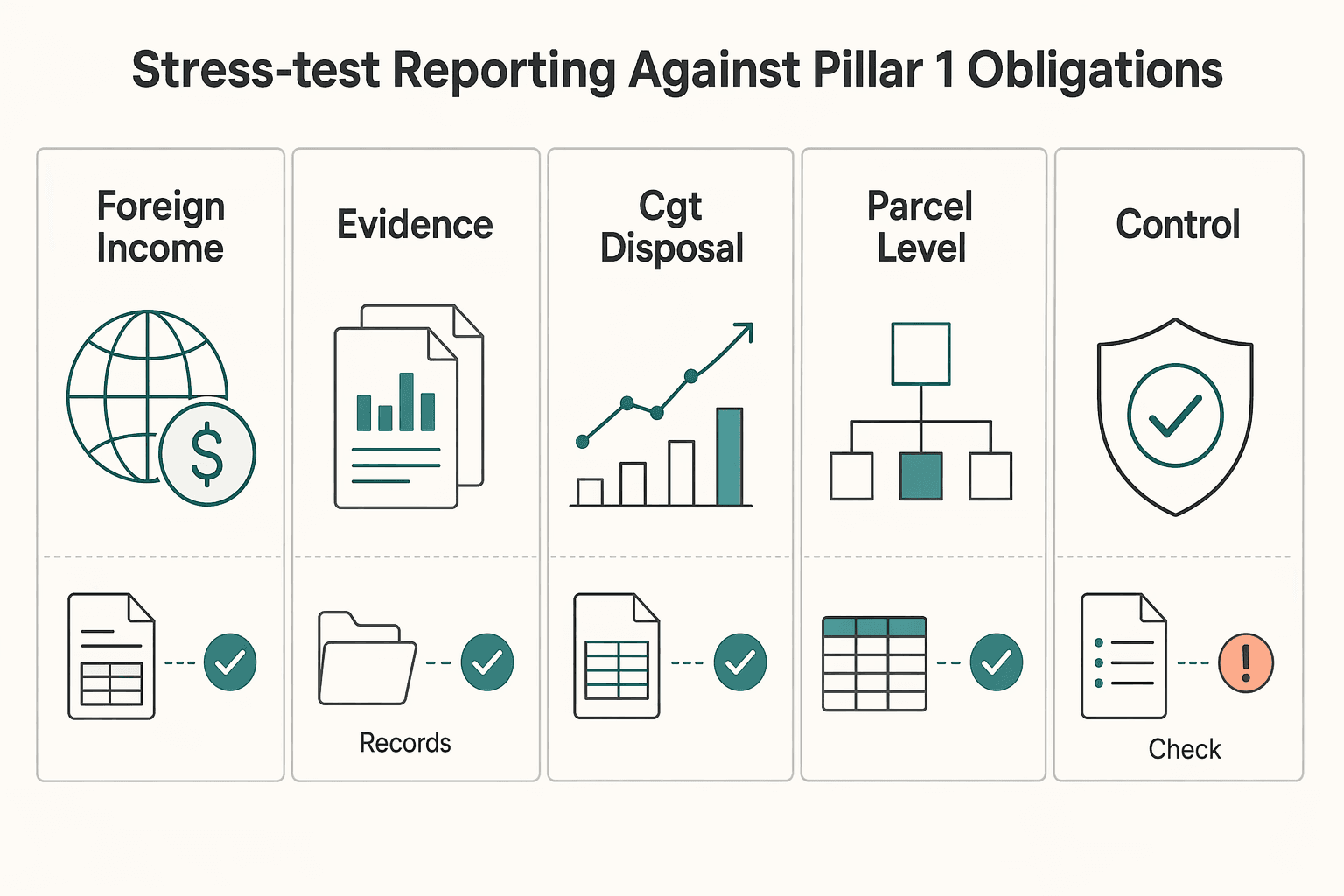

3) Stress-test reporting against Pillar 1 obligations#

A broker is tax-ready only if its exports support your actual filing workflow.

| Requirement tied to Pillar 1 | Pass test |

|---|---|

| Foreign income and foreign tax must be translated to AUD for return prep | Export includes fields you can convert to AUD consistently |

| Dividend reporting and FITO support | Records show gross dividend and foreign tax withheld (not net cash only) |

| CGT disposal and cost tracking | Exports include trade date, quantity, sale price, and commissions |

| Parcel-level CGT history | Separate parcels are preserved, not blended into one rolling position |

| Record retention readiness | You can retain usable records for at least 5 years after the relevant CGT event |

| W-8BEN operational control | Onboarding/maintenance supports setup and renewal before validity lapses, and updates after change in circumstances |

If the platform gives you dashboard summaries but not exportable transaction-level data, fail it.

4) Compare execution and operating fit#

Once cost, custody, and reporting pass, compare the factors that affect day-to-day results: limit-order control, product access, funding and transfer rails, execution-quality disclosure (such as Rule 605 summaries where relevant), and support responsiveness.

Decision rule: if one option is slightly cheaper but weaker on W-8BEN handling, tax exports, or verifiable custody disclosures, choose the lower-friction compliant option.

You might also find this useful: How to Buy US Stocks as a Canadian Resident.

Pillar 3: Implement Your Operational Playbook#

After you choose a broker, execution discipline is what protects your results. Use the same funding cadence, the same trade checks, and the same record routine every time.

Set your funding rhythm and wait for landed USD#

Pick a transfer rhythm you can repeat without guesswork. There is no universal "best" cadence, so use one that fits your cash flow while limiting repeated FX conversion friction, transfer costs, and admin.

| Factor | What to compare | Note |

|---|---|---|

| Deposit method | Compare the available deposit methods | Some Australian workflows are AUD-first |

| Conversion cost | Compare total conversion friction | FX fees can apply when you convert |

| Withdrawal friction | Compare the withdrawal path and cost | Do not compare speed alone |

| Time to tradable balance | Compare time to tradable balance | Balance updates can lag, including after close or on weekends |

| USD funds available | Confirm your account shows USD funds available to trade before you place any order | A transfer receipt is not enough |

Look at the full path from deposit to tradable USD, not speed alone. Some Australian workflows are AUD-first, some brokers offer multiple rails (for example wire, check, or ACH), and FX fees can apply when you convert.

Before you place any order, confirm your account shows USD funds available to trade. A transfer receipt is not enough.

Run the same pre-trade checklist every time#

Use this checklist before each order.

| Check | Why it matters | Action if it fails |

|---|---|---|

| Confirm tradable USD cash | You need available funds before placing a trade | Wait until the broker shows funds available to trade |

| Confirm ticker and venue | Wrong-symbol orders are costly to unwind | Recheck issuer name, ticker, and exchange in-platform |

| Check market session context | Prices can move sharply outside normal U.S. hours (9:30 a.m. to 4 p.m. ET) | If outside hours, tighten price control or wait |

| Choose order type and time-in-force | Market orders prioritize execution, not exact price; limit orders may not fill | Default to a day limit order unless you intentionally want a standing GTC order |

| Set slippage control | Quotes can move between review and submit | Set your max buy or min sell price; if it runs away, do not switch to a market order impulsively |

Order types and trading instructions vary by broker, so use what your platform actually supports.

Keep a lightweight documentation system#

Keep files in one place so tax prep is routine, not a reconstruction project. A simple structure is enough, for example: /Investing/US Stocks/2026/Confirmations, /Statements, /Dividends, /Tax.

| Record | Minimum detail | Article note |

|---|---|---|

| Trade confirmations | For every buy and sell | Example file name: 2026-04-15_AAPL_BUY_10_TradeConfirmation.pdf |

| Dividend records | Show gross income and foreign tax withheld | Keep records showing both the foreign tax paid and the related income included in assessable income if you plan to claim FITO |

| Broker account statements | At least quarterly for relevant active accounts | Example folder: /Statements |

| Funding and withdrawal records | Keep funding and withdrawal records | Make sure you can match them to the broker account activity |

| W-8BEN acknowledgement | Keep acknowledgement and validity tracking | Check whether your W-8BEN is still valid |

Use one naming rule so files stay searchable: YYYY-MM-DD_TICKER_Action_Qty_DocType (example: 2026-04-15_AAPL_BUY_10_TradeConfirmation.pdf).

At minimum, keep the following:

- Trade confirmations for every buy and sell.

- Dividend records that show gross income and foreign tax withheld.

- Broker account statements (at least quarterly delivery is the minimum standard for relevant active accounts).

- Funding and withdrawal records.

- W-8BEN acknowledgement and validity tracking.

This is what keeps you ATO-ready: foreign income, deductions, and foreign tax paid must be converted to AUD before lodging, and investment records generally need to be kept for 5 years after your return is processed. If you plan to claim FITO, keep records showing both the foreign tax paid and the related income included in assessable income.

Prevent common execution mistakes#

| Mistake | Prevent | Detect | Fix |

|---|---|---|---|

| Wrong ticker | Final issuer-name and ticker check before submit | Review same-day trade confirmation | Contact broker promptly and decide whether to unwind |

| Stale order | Use day orders unless you intentionally want persistence | Review open orders before placing a new order | Cancel stale order before re-entering |

| Duplicate order | Wait for order ID and status after submit | Check open orders and confirmations | Cancel extra open order immediately |

| Missing statement | Set a recurring statement-download reminder | Month-end document check | Pull missing file from broker portal right away |

Run a simple weekly and monthly cadence#

| Cadence | Task |

|---|---|

| Weekly | Check open orders |

| Weekly | Check cash balances |

| Weekly | Check unsettled activity |

| Weekly | Verify the next business day that trades and cash posted as expected because U.S. settlement is T+1 |

| Monthly | Reconcile confirmations to statements |

| Monthly | File missing documents |

| Monthly | Log dividend withholding |

| Monthly | Check whether your W-8BEN is still valid |

Keep it simple: weekly for orders, cash, and unsettled activity; monthly for reconciliation, filing, dividend withholding, and W-8BEN checks.

Related: How to Buy US Stocks as a UK Resident.

From Anxiety to Asset: Your Path to Confident Global Investing#

You are aiming for a repeatable system: clean compliance setup, disciplined broker selection, and a routine that keeps records audit-ready.

Build one clean compliance file#

Set up compliance, account opening, and document storage as one workflow before you fund anything. You should be able to show your accepted tax-status setup in the platform, the key account disclosures, and the exact folder where confirmations and statements are saved.

If you also run a business, keep that admin separate from your investing records. The ATO says you need an Australian business number before standard GST registration, and if GST registration becomes required, you must register within 21 days. That is not a rule for buying shares, but it shows why mixed records create avoidable risk.

Choose the broker you can actually audit#

Pick the platform you can reconcile, not just the one with the lowest headline fee. Review the legal disclosures, the full fee schedule, and a sample statement before your first deposit.

Your test is simple: can you trace each trade, cash movement, and tax entry to a dated document? If not, you are more likely to miss withheld amounts, unexplained cash differences, or duplicate orders.

Make execution boring on purpose#

Use the same operating sequence every time: fund, place the order, save the same-day confirmation, then reconcile by event. If your statement and your log do not match, stop and fix the gap before the next trade.

What to do next:

- Confirm compliance documents and account status are complete and saved.

- Approve a broker only after reviewing disclosures, fees, and sample reporting.

- Build an event-based record set for funding, trades, dividends, and statements.

- Set a recurring review to re-check the tax rules that apply to you, broker terms and costs, any ATO thresholds relevant to any business activity, and whether your document trail is still complete.

For a step-by-step walkthrough, see How to Pay US-Based Contractors from Australia.

Frequently Asked Questions

What are the tax implications if you buy US shares from Australia?

This grounding pack does not verify the tax treatment of buying US shares from Australia, including specific withholding rates, treaty outcomes, or filing triggers. Treat those points as unconfirmed until you verify them with current official guidance or a qualified adviser.

How does the W-8BEN fit into this?

This grounding pack does not include verified W-8BEN details. Do not assume filing effects, timing, or status from this section alone; confirm the current position directly with your broker or adviser.

Will you be taxed twice on the same dividend or gain?

This grounding pack does not establish a definitive "yes" or "no" for that outcome. Verify the current rules that apply to your situation before relying on any assumption.

Do you need an ABN or GST registration to buy US stocks?

Do not assume GST excerpts determine the tax treatment of share investing. The ATO and ABR material here is about GST registration and business status, not a direct rulebook for buying shares. If you are registering for GST for a business, you need an ABN first, and if registration becomes required, you need to act within 21 days. Penalties may apply if you fail to register when required.

How should you judge whether a broker app is safe enough?

This grounding pack does not verify broker-safety specifics such as custody arrangements, protection-scheme scope, or fee-model comparisons. Treat those as due-diligence checks to confirm from current broker legal disclosures and account documents.

How should you handle records and currency conversion?

This grounding pack does not set detailed recordkeeping or FX-conversion rules for share investing. Use a consistent recordkeeping process and confirm exact requirements against current tax guidance for your situation.

When should you use a market order instead of a limit order?

This grounding pack does not provide verified order-type guidance. Use your broker’s current order definitions, risk disclosures, and execution rules before placing trades.

What is the most common operational mistake after the first trade?

This grounding pack does not support a single verified "most common" mistake. A practical approach is to run a consistent post-trade check process so records and orders are reviewed before issues compound.

Try a related tool

A financial planning specialist focusing on the unique challenges faced by US citizens abroad. Ben's articles provide actionable advice on everything from FBAR and FATCA compliance to retirement planning for expats.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

- ato.gov.au/individuals-and-families/investments-and-ass...trusted

- ato.gov.au/individuals-and-families/coming-to-australia...trusted

- federalregister.gov/documents/2024/04/15/2024-05556/disclosure-o...trusted

- investor.gov/introduction-investing/investing-basics/glos...trusted

- investor.gov/introduction-investing/investing-basics/how-...trusted

- irs.gov/instructions/iw8bentrusted

- irs.gov/forms-pubs/about-form-w-8-bentrusted

- sec.gov/newsroom/press-releases/2024-32trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints

The goal is a defensible, low-drama position the Australian Taxation Office (ATO) can follow from your records, not a clever workaround. For a digital nomad, that usually means keeping two tracks straight: residency and GST/ABN admin. Consistency is what holds up over time: use real facts, take steps in a clear order, and keep documents that still match months later.

A Deep Dive into Form 5472 for Foreign-Owned US LLCs

**Treat Form 5472 as an IRS reporting workflow, not a tax guess, and you can cut avoidable penalty risk quickly.** If you run a globally mobile single-member LLC, most uncertainty comes from definitions, not effort. You can keep clean books and still miss a trigger because the IRS focuses on entity status, related parties, and reportable transactions.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.