Quick Answer

Build credit as a freelancer by running a repeatable system, not by chasing the “perfect” product. Start with one account you can manage reliably, automate on-time payments from a cash buffer, and keep balances controlled. Document your income with a simple proof stack, then review reporting accuracy and reconcile monthly so progress continues even when client payment timing is uneven.

You're not "bad with money" - you're missing a credit-building operating system#

To build credit as a freelancer, stop relying on motivation and start running a simple, repeatable system that still works when income is uneven. You run a business-of-one, and credit is part of your operating model, not a personality test. If you've ever blamed your "money habits," you probably just lacked a workflow that turns irregular cashflow into consistent credit behavior. Start thinking like an operator: controls first, then tools.

Erica Alini (personal finance reporter at the Globe and Mail and author of Money Like You Mean It) puts the core problem in plain language: "economic, social and technological changes have complicated personal finance for everybody," especially for Millennials and Gen Z. Freelancing can make that complexity feel even sharper because you manage both revenue timing and financial health.

Step 1: Adopt the operator mindset (system beats willpower)#

Run credit like you run client work: define inputs, set guardrails, measure outcomes.

- Input: one small, predictable payment you will never miss.

- Guardrails: autopay, reminders, and a buffer so you never "hope" a client pays in time.

- Outcome: a clean on-time track record and balances you can actually control.

In practice, if a client drifts past the due date, you do not panic-apply for new credit. You follow the system. The buffer covers the payment, you send the reminder, and your credit activity stays boring.

Step 2: Use safe defaults (pick one tool, then execute)#

The point is not to find the "perfect" product. It's to choose one path you can stick with long enough to prove consistency.

| Starter option | When it fits | What the article says to verify |

|---|---|---|

| Secured credit card | When you want spending behavior to stay small and predictable | Check the credit limit, statement close date, due date, and how the account is reported |

| Credit-builder loan | When you want one recurring payment you can plan around | Terms vary by lender, so confirm the payment schedule, fees, and conditions before you commit |

| Unsecured credit card | When you already qualify | Add only after consecutive on-time payments and controlled utilization |

Common starting points are a secured credit card, a credit-builder loan, or an unsecured credit card if you already qualify.

If you want a deeper tool breakdown later, use: The Best Business Credit Cards for Freelancers.

Step 3: Keep your credit routine resilient to client timing#

Client payment timing can be unpredictable. Your job is to design around that reality so your credit routine does not depend on a single invoice landing on the "right" day.

- Keep billing details and approvals organized so disputes do not become delays.

- Avoid cutting due dates close when you can choose timing.

- If one client dominates your income, structure work in milestones so cash comes in stages.

That is how you keep credit progress from being held hostage by one late payment cycle.

Before you start: set your credit baseline + prep your freelancer "proof stack"#

Set a baseline snapshot and assemble your "proof stack" before you apply for anything. This keeps you from guessing, rushing, or tripping your cashflow. The goal is simple: turn "irregular income" into "documented income," and start from a clean, measurable point.

Prerequisites (once): a notes doc or spreadsheet, a cloud folder, and calendar reminders for "check-in" and "statement date."

Step 1: Capture a baseline "before" snapshot (then freeze it in writing)#

Use whatever credit and account info you already rely on, and write down a dated "before" log. The point is not perfection. It's having a clear starting line you can refer back to instead of vibe-checking where you stand.

| Baseline item | What to log | Why to log it |

|---|---|---|

| Current credit picture | What you believe your current credit picture looks like based on the source you use | Creates a clear starting line you can refer back to |

| Open accounts | Which accounts you have open and which ones you actually use | Shows which accounts are open and actually used |

| Patterns to change | Any patterns you want to change, for example paying late or letting balances creep up | Highlights what needs to improve first |

| Possible inaccuracies | Anything you think might be inaccurate and want to double-check | Marks items to verify instead of guessing |

Verification point: you can answer, in one sentence, "What exactly needs to improve first?"

Step 2: Build your freelancer proof stack (one folder, boring labels)#

Create a folder called Underwriting - Self-Employed and drop in only what you can keep current. Do not overbuild this. You want fast retrieval under pressure.

| Folder | What goes in it (examples) | Why it helps |

|---|---|---|

Work + Payment | Work agreements, scopes, invoices, payment confirmations (whatever you already have) | Makes your income story easier to follow |

Banking / Payouts | Records you can export or screenshot from the systems you use | Helps connect work to deposits |

Taxes / Filings | Any filed documents you're comfortable sharing (if applicable) | Adds continuity to your story |

Identity / Business Info | Basic identity info and business details (if applicable) | Reduces back-and-forth during review |

If an issuer asks for clarification on income, you should not have to scramble through email. Pull a clean bundle from this folder and keep momentum.

Step 3: Don't make new credit responsible for a tight timeline#

Approvals, reviews, and verification steps can take time. Avoid stacking "must-pay" obligations on top of a plan that only works if new credit arrives immediately.

What's the fastest safe way to build credit as a freelancer? The 90-day sequence you can actually execute#

There is no guaranteed "fastest" timeline. A safer approach is to run one controllable tradeline cleanly for roughly 90 days, then add complexity only if it genuinely reduces risk for you. Build around what you can control: on-time payments and accurate reporting.

Ellen Johnson (TradelineSupply, published 12/07/2023) puts the timeline reality plainly: "Getting results from credit repair can take months, and it takes years to build or rebuild a solid credit history." Use the sequence below as a practical framework, not a promise.

Step 1 (First week): Open one starter tradeline you can control#

Pick one on-ramp and commit to operating it cleanly:

| Before applying | What to confirm | Why it matters |

|---|---|---|

| Reporting | Ask whether and how the account is reported to consumer credit bureaus | Build around accurate reporting, not guesses |

| Costs and terms | Confirm fees, interest, and any key conditions around closing the account early | Terms can vary, especially on credit-builder loans |

| Funding source | Confirm you can make payments from your buffer, not from your next invoice | Keeps the plan from depending on a client paying on time |

- Secured credit card: You control spending behavior and can keep activity small and predictable.

- Credit-builder loan: Terms vary by lender, so confirm the exact schedule, fees, and conditions before you commit.

Practical checks before you apply:

- Ask whether and how the account is reported to consumer credit bureaus (read the disclosure, ask directly).

- Confirm fees, interest, and any key conditions around closing the account early.

- Confirm you can make payments from your buffer, not from your next invoice.

Verification point: you can explain, in one sentence, why this account fits your current self-employed cashflow.

Step 2 (Roughly the next 11 weeks): Stabilize, then expand only with a clear reason#

Treat the next stretch like operations, not motivation.

Step 2A: Keep usage boring and payments flawless. Use the account for a small, predictable expense you already pay anyway, and make sure every payment is on time. If you use any "set it and forget it" features, still check periodically that payments actually post.

Step 2B: Add a second account only if it clearly lowers risk. If your cashflow is stable and you have a specific reason, you can consider adding a second line. Do not stack applications impulsively. Add complexity only when you can clearly explain the benefit for your situation, for example separating spending, adding redundancy, or smoothing cashflow.

Step 2C: Verify accuracy. Review your statements and, when your credit reports update, check that the information shown looks accurate. If something is wrong, follow the provider's stated process to get it corrected.

If a client pays late, you still make your credit payment on time because you funded it from your buffer, not from "incoming invoices." That is the whole point.

If you plan to move toward business credit later, bookmark this for your next phase: The Best Business Credit Cards for Freelancers.

Secured credit card vs credit-builder loan: which should you start with (and why)?#

Start with the product you can pay on time, every time, while keeping your balances under control. Focus on what gets rewarded: one source flags payment history as the most significant factor (35%), and another highlights credit utilization (30%) with a practical target to keep it under 30%. Another source also sums it up plainly: keep balances under 30% and pay bills on time.

Before you start (two non-negotiables to verify)#

You can build credit as a freelancer with either tool, but the basics still matter.

- Confirm how it shows up: Ask the issuer or lender what gets reported to the credit bureaus (and what does not), so you are not guessing about impact.

- Confirm the full cost: Read the cardholder agreement or loan disclosures for fees and payment terms. Do not rely on marketplace roundups alone. You need the primary documents.

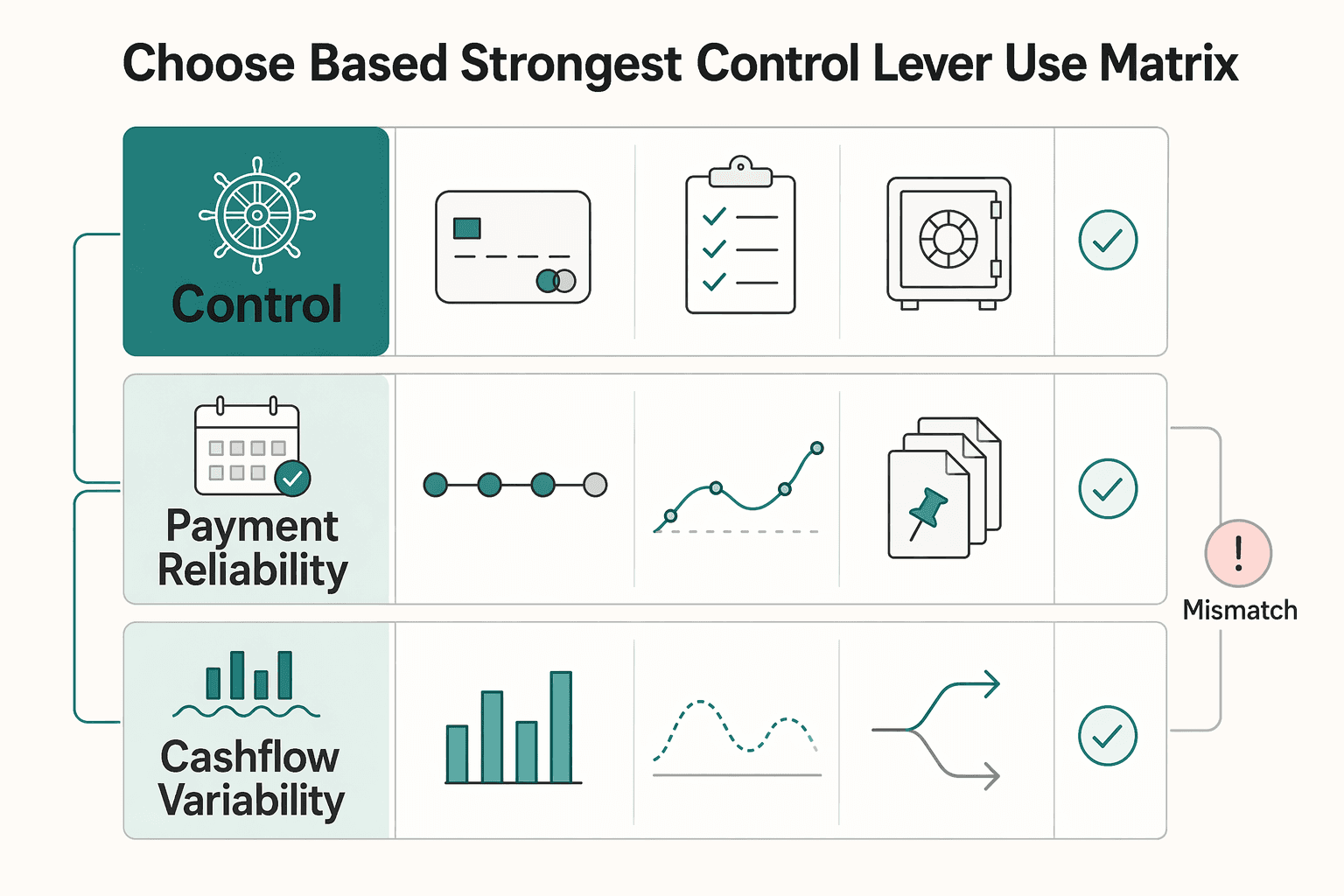

Step 1: Choose based on your strongest control lever (use this matrix)#

Use the table to pick the option that best supports your self-employed system.

| Decision factor | Choose a secured credit card when... | Choose a credit-builder loan when... | What to check in writing |

|---|---|---|---|

| Utilization control | You can keep spending small and pay it down so you stay under 30% utilization. | You would rather prioritize consistent on-time payments without needing to track utilization month to month. | Card: credit limit, statement close date, due date. Loan: payment amount, due date, total fees. |

| Payment reliability | You can set up a repeatable payment routine and review each statement so nothing surprises you. | You want one recurring payment you can plan around. | Payment options, late fee policy, any grace or processing details listed. |

| Cashflow variability | You can route a few predictable expenses through the account and pay them off without waiting on client invoices. | You can commit to the stated payment schedule even when a client pays late. | Allowed payment methods, processing time, cutoff times. |

If one slow-paying client would push you to carry a high card balance, pick the option that makes balances easier to keep low, even if it feels less "fun."

Step 2: Add an unsecured card only after stability shows up consistently. Do not chase rewards while you are still stabilizing your financial health. Add an unsecured credit card only after you can point to consecutive on-time payments and controlled utilization across your recent statements.

Safe default decision rule: Pick one primary product first, operate it perfectly for multiple billing cycles, then add a second tool only if it reduces risk (lower utilization pressure or simpler repayment), not because you found a new offer.

Can you build credit with inconsistent freelance income? Yes - if you package your cashflow like an underwriter#

Inconsistent freelance income can make planning harder, but you can make your cash flow easier to explain and easier to manage. You do not need perfect income. You need a verifiable story and repeatable execution.

Before you start (your "proof stack" must reconcile)#

You want your documents to tell one consistent narrative across bank deposits, invoices, and tax reporting.

Step 1: Summarize income so it reads cleanly in 2 minutes. Create a one-page monthly summary (month → total deposits → top clients). Then back it up with invoices, payouts, and signed agreements, especially retainers.

| Artifact to keep | Why it matters | Practical verification check |

|---|---|---|

| Monthly deposit summary | Makes irregular income legible fast | Totals match your bank deposits for each month |

| Invoice ledger (issued, paid, outstanding) | Shows how money was earned, not "random deposits" | Each deposit ties to an invoice or contract |

| Signed agreements (including retainers) | Helps show ongoing work, not just one-off projects | Agreement names match invoice client names |

| Payouts log (platform payouts, bank transfers) | Explains timing gaps between "paid" and "received" | Payout dates align with bank posting dates |

| Tax documents | Helps keep your story consistent year to year | Your annual totals reconcile to your records |

Step 2: Reduce perceived volatility by reducing real volatility. A freelancer respondent put it bluntly: "cut down your expenses like Netflix, eating out... focus growing your business by keeping and acquiring retainer clients." Do that. Lower fixed burn and more predictable work make it easier to stay steady when client payments swing.

Step 3: Build a simple buffer-and-bills routine so timing stops breaking your month. Irregular deposits are normal with an unsteady paycheck. What helps is separating "money that arrived" from "money you can safely spend," and planning bills around a buffer instead of around hoped-for invoice timing.

If your longer-term goal includes a major application like a mortgage, keep your records organized for that too (this helps: The Ultimate Guide to Getting a Mortgage as a Freelancer).

If one client pays early and another pays late, you still cover your scheduled payments on time because you keep expenses lean and run your month off a buffer, not off "hopefully cleared" invoices.

How do I build credit without hurting cashflow? Make your invoices do the risk-control work#

Protect your cashflow by making your credit payments predictable, then keep utilization low. Payment history is the biggest factor (Zintego cites 35%), and credit utilization matters too (Zintego cites 30%, and recommends keeping it under 30%). As Billcut puts it, "Freelancers don't have predictable salaries, so credit usage requires strategy, not guesswork."

Step-by-step: a cashflow-safe credit workflow#

Step 1: Lock your "credit payment money" away from your client money. Create a separate buffer account (or sub-account) that only exists to pay credit. Fund it on a schedule you control, then run autopay from that buffer. Verification: your credit autopay never pulls directly from the same pool where client payments land.

Step 2: Automate "on time" so you are not relying on memory. Autopay is the baseline. Add calendar reminders for statement close and due dates so you can spot issues before they become late payments. Verification: you can show a consistent record of on-time payments.

Step 3: Plan spend so utilization stays low (and boring). Utilization is a major piece of your score (Zintego cites 30%), and Zintego recommends keeping it under 30%. If you use credit for work expenses, set a ceiling and pay down before the statement closes when you can. Verification: your balance is kept low and you are not surprised by the statement.

Step 4: Keep billing and payment records tidy so you can reconcile fast. This is not about perfect contracts. It is about clean documentation: invoices, confirmations, and transaction records you can match up. Verification: you can point to a transaction record that matches the invoice.

Two controls do most of the work here:

- On-time autopay from a buffer: Payment history drives your score (Zintego cites 35%). Operator check: autopay still hits in a slow-pay month.

- Low, planned spend: Utilization matters (Zintego cites 30%, recommends under 30%). Operator check: you pay down before the statement closes.

If a client claims they paid but the funds have not hit your account yet, you still make your credit payment from the buffer, then reconcile the invoice and follow up without panic-spending on the card. Want a quick next step? Try the free invoice generator.

If you can't qualify yet: the fallback playbook (and how to recover from mistakes)#

If you cannot get approved today, do not force it. When you are bootstrapping and do not have external funds to fall back on, cashflow is everything, and freelancing can take patience early on. Choose the conservative Plan B: fewer moving parts, more control.

Before you start (so you do not dig a hole)#

Treat this as prep, not a shopping spree.

- Set a cash buffer you can live with. Only commit to a new recurring payment if you can cover it from cash you already control.

- Confirm credit reporting in writing (if credit-building is the goal). If a product is not reported to the bureaus that matter in your market, it may not help your credit file the way you expect. Do not assume.

- Prefer boring, transparent terms. If you cannot explain the fees, interest, and repayment schedule in one sentence, pause.

Step-by-step: choose your on-ramp without overcommitting#

Step 1: Pick one simple tool you can operate reliably. Focus less on what is "optimal" and more on what you can run cleanly: clear terms, predictable payments, and no surprises.

Step 2: Treat "alternative" products as research, not defaults. You will see product names and hacks tossed around in communities. Do not anchor on the brand name. Verify the basics for your situation: what it costs, what it requires from you, and whether it reports where you live (rules vary by market).

Step 3: If you hit a snag, reset to basics.

- If you are carrying a balance, prioritize getting it back to a level you can comfortably manage and keep new charges predictable.

- If you missed a due date, get current and simplify your process so you can repeat it consistently.

- If you have had a run of denials, slow down and stabilize before trying again.

If you decide a business credit card might fit later, remember that some business credit cards can report on personal credit, depending on the card and issuer. Read this before you apply: The Best Business Credit Cards for Freelancers.

The maintenance cadence: a monthly monitoring loop that keeps you building credit (without obsessing)#

Run one simple monthly close plus one mid-month check to keep building credit through boring consistency. At this point you have controls, tools, and a fallback plan. The maintenance loop is what keeps the system stable: fewer surprises, fewer fees, fewer panic decisions.

Step-by-step: your monthly close routine (operator-simple)#

Step 1: Reconcile money end-to-end (invoices → bank → credit payments). Pick one day each month and match three totals: invoices marked received, deposits that actually settled, and payments you made toward cards/loans. Save artifacts (invoices, payout confirmations, bank lines, card statements) in one folder so you can defend disputes and prep taxes later.

Step 2: Keep identity and tax profile docs organized. Store whatever your clients request for onboarding and tax identity in a single "Proof Stack" folder. You want zero scrambling when a lender, platform, or enterprise client asks for the same document again.

Step 3: Use one payment rule you can actually follow. Do not obsess over daily balances. Pick a simple operating rule: pay on time, avoid surprises, and do not carry more debt than you can clear without stress.

| Monthly close item | What you check | What "done" looks like |

|---|---|---|

| Invoice log | Paid status vs received cash | No invoice marked "paid" without a matching deposit |

| Bank deposits | Settled vs pending | You only count funds that actually settled |

| Credit payments | Posted vs scheduled | Every payment shows as posted before the due date |

| Document folder | Contracts, statements, tax docs | One searchable folder, no missing months |

If a client says "finance sent it," but your bank still shows nothing, you do not float expenses on your card and hope. You pay from your buffer, then chase the deposit with a clean paper trail.

Step-by-step: global work without surprise paperwork#

Step 4: Track cross-border compliance triggers early, not at filing time. If you work internationally, treat cross-border admin like operations. Keep a lightweight log of where you worked and when, and store tax profile data where platforms support it. Do not guess on FEIE or other cross-border reporting requirements that may apply.

Term: Physical presence test means you meet the test if you are physically present in a foreign country or countries 330 full days during any period of 12 consecutive months (the days do not have to be consecutive). If you plan around FEIE, remember: the IRS ties the exclusion to filing a return reporting the income. Confirm your situation with a qualified tax pro in your jurisdiction before you make financing moves based on assumptions.

Conclusion: build credit like an operator - sequence, controls, and repeatability#

Build a stronger credit profile as a freelancer by running a repeatable system: make payments predictable, keep reported balances steady, and keep your records clean. At this point you have the pieces. The win is turning "I know what to do" into "I do it the same way every time," even when client payments arrive late, partial, or messy.

Step 1: Treat credit building like operations, not motivation#

You do not win by "earning more someday." You win by consistently managing the signals that show up in credit reporting and lender reviews. What matters varies by country and lender, but an operator lens helps:

| Control | What you do | What you verify (monthly) |

|---|---|---|

| Payment timing | Put autopay on the minimum due, then manually true-up from cleared funds | No due dates missed; fewer avoidable fees |

| Reported balance | Set a target range and pay before the statement closes (when that is how your account reports) | Statement reports within your target range |

| Reporting | Keep accounts simple and track what shows up on your report | Accounts appear as expected; errors get disputed fast |

If a client says "paid," but the funds do not actually settle when you expect, you do not gamble. You cover the obligation from your buffer, then reconcile once the deposit clears.

Step 2: Tighten your "get paid" layer so credit progress does not depend on hope#

Your credit system breaks when your cash system stays ambiguous. If you want to tighten the payment workflow while you build credit, use tooling that makes it easier to run consistent processes.

If you use products like Gruv Virtual Accounts and Gruv Payouts (where enabled), evaluate them like an operator: do they give you clear status on invoices, deposits, and payouts, and make reconciliation less manual? If yes, keep them. If no, simplify.

Step 3: Copy/paste checklist (run this for every new client + every month)

- Baseline my score + report snapshot (date, open accounts)

- Chosen one starter credit product (for example, a secured card or credit-builder product, if available)

- Autopay on + calendar reminders set (due date + statement close date)

- Reported-balance rule set (target range, payment schedule, alert thresholds)

- Client terms in writing (milestones, due dates, late fees, acceptance proof)

- Payment buffer funded (a level I can sustain)

- Monthly reconciliation done (invoices → deposits → credit payments)

- Application freeze rule followed (no new credit unless my criteria says "yes")

Frequently Asked Questions

What is the fastest safe way to build credit as a freelancer?

There is no single “fastest” path that fits everyone. The safest, most repeatable path is the one you can keep consistent, because credit building comes down to consistent, reported financial behavior. Kikoff puts it plainly: “You simply need to demonstrate consistent, reported financial behavior.” Pick one starter account that reports, make on-time payments non-negotiable (automation helps), and tie your spending to predictable expenses you already pay so the system survives busy weeks.

Secured credit card vs credit-builder loan: which should a freelancer start with?

There’s no universal winner. Start with whichever option you can manage reliably month after month, because consistency matters more than the label on the product. Whichever route you choose, confirm that your activity is actually reported so it counts toward the “reported” part of consistent, reported financial behavior.

Can I build credit with inconsistent freelance income?

Yes, if you separate income volatility from payment reliability. The goal is to make payments consistent even when your cash inflow is not. Make it easier on yourself: set reminders or automation for at least the minimum, and only take on charges you can comfortably cover if a client pays late.

How do I build credit without hurting cashflow?

Use credit as a reporting tool, not as working capital. Tie the account to expenses you would pay anyway (software, phone, hosting), then pay from money you actually have, not money you expect. A simple rule that keeps you out of trouble: only charge what you can pay even if a client payout lands late.

What if I can’t qualify for standard credit yet?

Look for an on-ramp that’s designed for people who are building (or rebuilding) credit, and prioritize something that reports your activity. Then keep it simple: one account, clean payments, consistent reporting. Avoid stacking multiple new applications at once. Focus on building a track record of consistent, reported financial behavior.

Should I build personal credit first or business credit first as a freelancer?

It depends on what you’re applying for and what the issuer actually evaluates. As a freelancer, your personal and business finances can blur in early stages, so pay attention to which credit profile is being checked and reported for the specific account. If you’re exploring business-card options, you can start here: The Best Business Credit Cards for Freelancers.

How long does it usually take to see a credit score change from these steps?

Timelines vary, and you will only see change once your activity is reported and your credit report reflects it. Track what’s reported, not what you meant to do. Focus on controllables: on-time payments and consistent, accurate reporting across your accounts. A periodic check can help you spot missing items or errors without obsessing over day-to-day score movement.

Watch

How to Build Credit as a Freelancer

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Business Credit Cards for Freelancers

Pick for reliability first. For a freelancer, the right business card is usually the one that keeps recurring bills moving, keeps records clean, and avoids extra costs when income swings from month to month. Rewards still matter, but they sit on top of those basics. They do not replace them.

Getting a Mortgage as a Freelancer Without Guesswork

Start by reconciling your income file before you compare rates. For a **mortgage for freelancers**, the first gate is simple: can an underwriter read your documents cold and see one consistent income story?

IP Protection for Software Developers Using a Copyright-First Plan

Start with a copyright-first baseline, then add other protections where they reduce a specific risk. For small teams doing client work or shipping SaaS features, that makes software IP protection more usable in day-to-day operations.