Quick Answer

Build a diversified investment portfolio by setting a written plan, keeping enough cash for near-term needs, and choosing a simple asset allocation across cash, bonds, and stocks. Then diversify within each bucket, use broad ETFs only when they match the exposure you want, and rebalance with simple rules so cashflow problems do not force you to sell at the wrong time.

Stop "Investing" Blindly: Build a Diversified Portfolio That Won't Break Your Cashflow#

If you run a business-of-one, you do not need vibes; you need a repeatable system you can run.

Build a diversified portfolio by writing a simple investment plan first, then making diversification serve your real-world goals instead of fighting them. The goal here is not more investing tips. The goal is fewer forced decisions.

Most investing content repeats the same slogans. One operator-focused investing essay even calls it out directly: "diversify your portfolio, play it safe, and don't put all your eggs in one basket." That advice helps, but it can stay so generic that you never translate it into rules you can actually follow.

That same essay draws a line worth taking seriously: "The strategies designed to protect a modest nest egg are fundamentally different from those used to build an empire." Translation: decide what game you are playing right now, then build portfolio rules that match.

Step 1: Put your plan in writing (so you stop improvising)#

Before you do anything else, write a Personal Investment Plan. Use it as your anchor when markets swing and emotions show up. The essay gives you the core instruction: "Define your financial goals, risk tolerance, and core beliefs in writing."

Use a simple structure:

- Goal: What this investment portfolio funds, and what it does not fund.

- Risk tolerance: What you can hold through without panic-selling.

- Core beliefs: What you will consistently do, and what you will refuse to do.

Hypothetical scenario: the market dips at the exact moment you feel pressure to "do something." If you wrote your plan, you follow it. If you did not, you will try to fix the feeling with a reactive move.

Step 2: Use diversification as protection, not decoration#

A clean operating principle beats complicated allocation math for most people: "Concentrate to Build, Diversify to Protect." You can respect growth while still prioritizing protection.

Use this translation table to keep yourself honest:

| Generic investing advice | Operator translation (what you actually do) |

|---|---|

| "Diversify" | Use a portfolio you can explain and stick to when things get noisy. |

| "Play it safe" | Choose an approach that matches your risk tolerance, not your optimism. |

| "Don't put all eggs in one basket" | Avoid single points of failure inside your investments. |

From here, the playbook is simple: define your plan, diversify intentionally, and keep your rules simple enough to execute.

Prerequisites: What to Prepare Before You Buy Anything#

Get clear on your goal, time horizon, risk tolerance, and liquidity floor before you buy investments, so you do not force a sale when cashflow gets weird. This is the unsexy setup that keeps your portfolio stable under late invoices, admin friction, and real-life liquidity needs.

Before you start (5 operator steps)#

Step 1: Write down what you are investing for and your time horizon. Write down what you are investing for, then note when you will need the money for that goal. Your time horizon is the anchor for how aggressive or conservative you can afford to be.

Verification: you can answer, "What am I trying to achieve, and when will I need this money?" in one sentence.

Step 2: Sanity-check your risk tolerance (before the market does it for you). Risk tolerance is how much investing risk feels right for you based on your emotions and financial situation. If a normal drawdown would make you panic-sell, your plan is too spicy, even if the spreadsheet looks great.

Verification: you can describe what level of ups and downs you can actually live with.

Step 3: Set your operational liquidity floor (non-negotiable cash). Define the minimum cash you refuse to invest. Bank of America frames this as "cash, or liquidity, needs," meaning whether you expect to draw on investments for regular expenses anytime soon. If bills would push you to sell ETFs during a down month, your floor sits too low.

Step 4: Build an audit-ready documentation stack. Create one folder, cloud or local, that holds brokerage statements and a simple transfer log (date, from, to, purpose). If you receive tax-related paperwork from banks, brokers, or clients, store it in the same place and save an annual export for reconciliation.

| What to store | Why it matters | Minimum habit |

|---|---|---|

| Brokerage statements | Proof of positions and activity | Save monthly PDFs |

| Transfer record | Explains money movement | Log every transfer in one line |

| Tax docs (as applicable) | Reduces year-end scramble | Drop in as received |

Step 5: Reduce transfer friction and plan for verification delays. If your income arrives inconsistently or cross-border, tighten your collection and transfer workflow so cash arrives predictably. Also assume some providers may place routine holds or require extra verification before transfers clear. Treat that lead time like operations, not an emergency.

Hypothetical scenario: a platform holds a payout for review the same week the market drops. Your liquidity floor keeps you from liquidating stocks or ETFs at the worst time.

Quick risk note: If you're considering leveraged products like CFDs or forex (FX), be aware they're described as complex instruments with a high risk of losing money rapidly due to leverage.

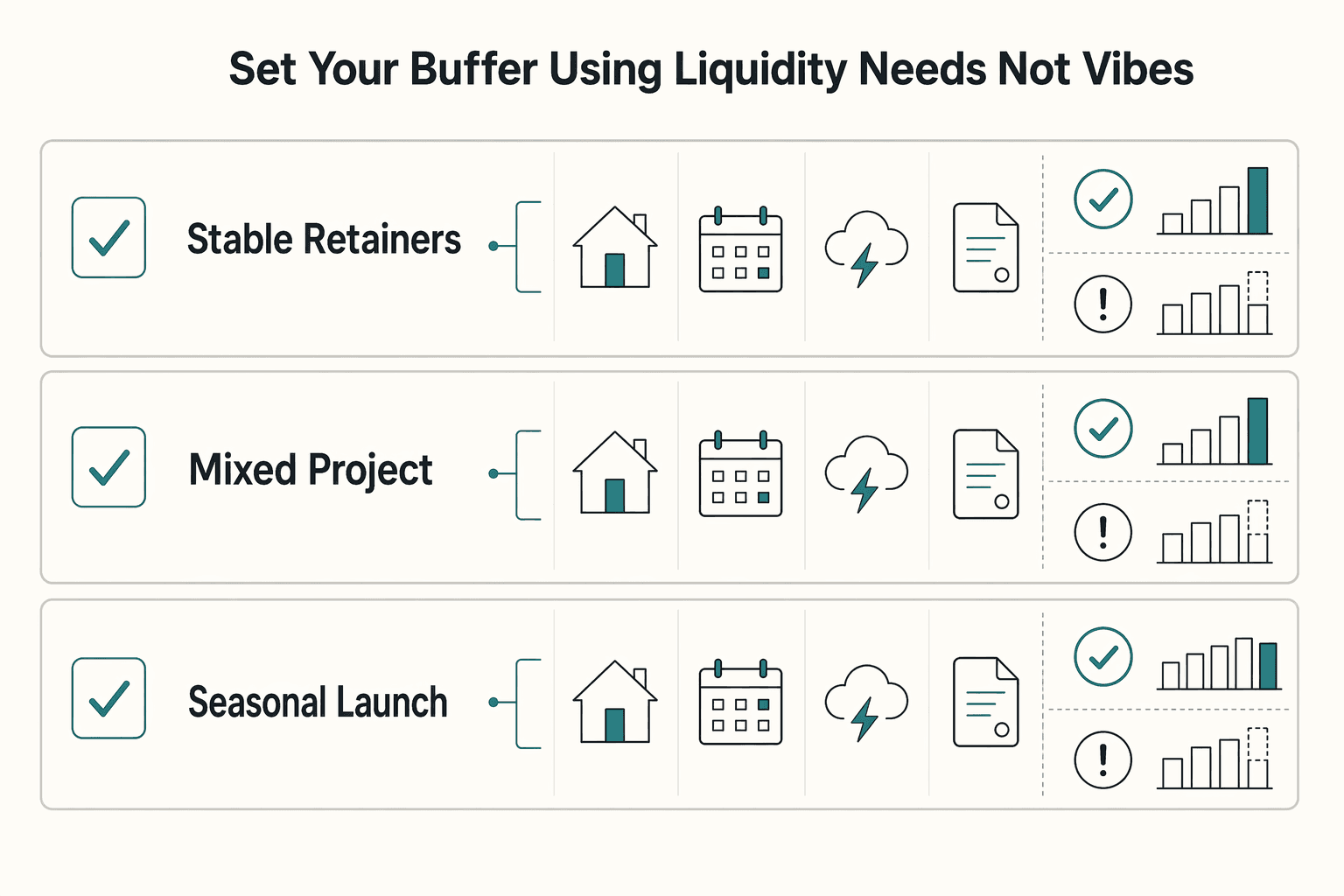

How Much Cash Buffer Should You Keep Before Investing?#

Keep enough cash to cover your real liquidity needs so you do not have to sell ETFs, or other investments, at a bad time just to pay bills. Your asset allocation starts with a cash floor, not with picking ETFs.

Step-by-step: Set your buffer using liquidity needs (not vibes)#

Step 1: Set a baseline runway in cash. Start with the smallest buffer that lets you run your life without touching your investment portfolio. Pearler puts the core principle plainly: "Holding cash alongside an ETF portfolio can smooth out life's financial bumps without forcing you to sell investments at the wrong time."

Verification: you can clearly name what this cash must cover (bills, near-term obligations, and room for unexpected costs).

Step 2: Size up when your income adds timing risk. Increase the buffer if your cashflow has more timing uncertainty or a higher chance of income disruptions.

- Variable income: payouts swing month to month.

- Delayed receipts: you are waiting on invoices even when revenue looks "booked."

- Client concentration: one client delay becomes your entire cashflow problem.

Step 3: Use the buffer ladder to choose the first line that matches reality. You will formalize exact numbers in your checklist. For now, choose the tier that matches your business model.

| Your income pattern | Buffer stance | Why this is the safe default |

|---|---|---|

| Stable retainers + low variance | Smaller cash buffer | Fewer timing shocks, easier forecasting |

| Mixed project income | Mid-level cash buffer | More gaps, more invoice variance |

| Seasonal or launch-based income | Larger cash buffer | Longer dry spells, higher disruption risk |

Step 4: Run the down-month test before you invest more. If paying monthly bills would require selling ETFs during a down month, your cash buffer is too small. Raise it first. Pearler also flags the tradeoff: "Hold too little, and you risk dipping into your ETFs in a downturn. Hold too much, and you might miss out on the returns..."

Hypothetical scenario: a top client pays late right after a market drop. Your cash buffer lets you keep your ETF plan intact instead of liquidating at the worst moment.

Protect the buffer with account separation (so it stays a buffer)#

Step 5: Separate buffer cash from investing cash. Use one account for buffer cash and another for investing transfers, so money meant for bills does not get swept into investments by accident.

Verification: you cannot "accidentally invest" money that should cover next month's obligations.

Want a quick next step for "build a diversified portfolio"? Try the free invoice generator.

What's the Difference Between Asset Allocation and Diversification (and Why You Need Both)?#

Asset allocation sets how much goes into stocks, bonds, and cash. Diversification reduces single-point failure risk inside and across those buckets. This is how you build a diversified portfolio without turning it into a spreadsheet hobby.

FINRA puts the definitions plainly: "Usually expressed on a percentage basis, your asset allocation is what portion of your total portfolio you'll invest in different asset classes." It also says: "Diversification is the spreading of your investments both among and within different asset classes."

FINRA also calls asset allocation, diversification, and rebalancing "important tools in managing investment risk." Treat that as your operator mandate.

Step-by-step: Separate the "big levers" from the "spread"#

Step 1: Write your asset allocation in one sentence. Use a simple template: "I hold X% stocks, Y% bonds, Z% cash (or cash equivalents)." If you cannot explain it in one sentence, you built something too complex for your current ops maturity.

Verification: you can map every holding to a bucket (stocks, bonds, cash) without debate.

Step 2: Define diversification as "blast radius control." Diversification answers: "If one company, one sector, one country, or one issuer has a bad year, do I still stay in the game?" You diversify among asset classes (stocks vs. bonds vs. cash) and within them (not all stocks in one theme, not all bonds from one issuer).

| Decision | You're choosing... | Primary job | Common operator mistake |

|---|---|---|---|

| Asset allocation | How much in stocks, bonds, cash | Set your portfolio's overall risk exposure | Copying an allocation you cannot maintain |

| Diversification | How spread out within and across buckets | Reduce concentration risk | Owning "different" funds that hold the same exposures |

| Rebalancing | How you return to target over time | Keep the plan intact | Letting winners run until the portfolio drifts |

Step 3: Use a safe-default mental model to pick holdings.

- Cash (or cash equivalents) is its own sleeve in your allocation.

- Bonds are a different asset class than stocks and cash.

- Stocks are a different asset class than bonds and cash.

- ETFs can be one way to implement diversification, because a single fund can hold many underlying securities. You still need to check what it actually holds.

Hypothetical scenario: a client pays late during a market drop. If you need cash and you do not have enough of it, you can end up forced to sell investments at the wrong time. If you sized cash and other sleeves intentionally, you bought time instead of negotiating with the market.

Step 4: Pick your rebalancing anchor now. Your allocation is the target. Rebalancing is the discipline. FINRA defines it like this: "rebalancing means making regular adjustments to make sure you're still hitting your target allocation over time." Write down how you will handle rebalancing ahead of time, so you do not negotiate with yourself later.

Step 1 (Layer One): Stabilize "Getting Paid" So Investing Doesn't Turn Into Forced Selling#

The goal is simple: do not invest money you might need soon, because that is how "investing" turns into forced selling. This is basic liquidity discipline for the part nobody glamorizes: making sure cash arrives when you expect it to.

Step 1: Map your inflows and timing (no spreadsheets, just clarity)#

Start with a one-page "cash timing map" you can review monthly:

| Map line | What to write | Handling |

|---|---|---|

| Cash you expect to come in | Write down what cash you expect to come in and roughly when | Review monthly |

| Cash you must send out | Write down what cash you must send out and roughly when | Review monthly |

| Timing uncertainty | Note where timing is uncertain | Treat that uncertainty as a real risk, not a rounding error |

Keep it that simple: expected inflows, required outflows, and anywhere timing is uncertain.

Hypothetical scenario: a payment arrives later than you thought, and markets drop at the same time. If you invested every spare dollar, you now face a choice you do not want: sell while prices are down, or miss an obligation.

Step 2: Reduce timing surprises with a repeatable "get paid" process#

Pick a process you can execute consistently, even when you get busy:

- Make it easy for someone to pay you correctly.

- Follow up in a way you will actually do, not a way you wish you did.

- Keep a record you can trust so you are not relying on memory.

You do not need a perfect system. You need a repeatable one.

Step 3: Define what is investable (one rule you can follow)#

Run your money like an operator: decide, in advance, when cash becomes investable.

Use a simple gate: "If I cannot cover near-term obligations in cash, I do not invest this cycle."

Verification (ready for Layer Two): you can explain your buffer rule in one sentence, you can estimate your next expected inflows from your own records, and you can reconcile what came in versus what you expected using your transaction history.

Step 2 (Layer Two): Build Your Baseline Asset Allocation (Stocks/Bonds/Cash) With a Safe Default#

Asset allocation is the high-level decision about what percentage of your portfolio or net worth goes into different asset classes. For most investors, that mix matters more than individual stock selection, and balancing across multiple asset classes can sharply reduce risk across different market conditions.

Step 1: Translate "risk tolerance" into freelancer reality#

Risk tolerance is not just a personality trait. For freelancers, it often shows up as a liquidity question: "How long can my revenue dip before I feel forced to sell?" Answer that in plain language, then align your asset allocation to it.

Use these prompts:

- If a top client pays late, can you cover obligations using cash, and other lower-volatility holdings, without selling stocks?

- Do you lose sleep when markets drop, or do you keep executing your plan?

- Do you treat your business income like a volatile asset, because it can be?

Lyn Alden puts the priority in the right place: "For most investors, a smart approach to asset allocation is a lot more important than individual stock selection." The operator move is to set a mix you can stick with.

Step 2: Use a simple three-bucket structure you can explain in one sentence#

You do not need complexity to start. You need clarity and risk control. One simple way to think about your mix is in three buckets: cash, bonds, and stocks.

| Bucket | Job in your portfolio | What can fit | Operator rule to keep it clean |

|---|---|---|---|

| Cash | Covers runway and near-term obligations | Checking, savings, money market (if you use it) | If spending needs rise, refill cash before adding risk |

| Bonds | Adds stability alongside stocks | Bonds or bond funds/ETFs | Treat this as shock absorption, not a return-maximizer |

| Stocks | Drives long-term growth | Stocks, stock funds/ETFs, diversified holdings | Size it so you can stay invested through drawdowns |

Implementation note: some investors use funds or ETFs to express these buckets; others pick individual securities. If you pick individual stocks, keep sizing and concentration risk in check so one mistake cannot break the plan.

Simple guardrails to keep you honest:

- Be clear about what you count as "cash" for your liquidity needs.

- Have a rough sense of how you want to balance cash, bonds, and stocks.

- Have a consistent approach to keeping your mix from drifting too far.

Practical stress test: imagine stocks drop sharply the same week a large invoice stalls. If you cannot cover your next stretch of obligations without selling your growth assets, you may have taken on more volatility than your situation can handle.

If you still need to sort your tax identity rails, use ITIN vs. EIN vs. SSN: What's the Difference?.

How Do You Diversify Within Each Asset Class Without Overcomplicating It?#

Diversify inside each bucket by spreading exposure across sectors and geographies, using as few holdings as you can while still avoiding concentration. The goal stays simple: fewer single points of failure, fewer moving parts.

Portfolio diversification means spreading exposure across different investments rather than concentrating all capital in a narrow set of holdings. Keep that in mind while you choose what sits inside each sleeve. Done well, diversification can smooth outcomes and reduce downside volatility over time, but it still may not guarantee positive returns in every period.

Step 1: Diversify stocks with clean exposure (and avoid overlap you cannot explain)#

Treat your stock sleeve as your growth engine, then spread risk across sectors and geographies so one industry or one country does not dominate outcomes. The point is not to collect more tickers. It is to avoid concentrating all your equity risk in a narrow set of holdings.

Use this operator check to prevent accidental duplication:

| Check | What you do | What "clean" looks like |

|---|---|---|

| Sector spread | Review your stock holdings by sector | No single sector obviously drives most of your equity risk |

| Geographic spread | Confirm whether you hold only one country or many | You can explain your country exposure in one sentence |

| Overlap control | Compare holdings that sound different | You do not hold multiple positions that end up concentrated in the same names |

Hypothetical scenario: you add a tech-focused stock position, then later add a growth-focused stock position. If both end up concentrated in the same few large companies, you did not meaningfully increase diversification. You just added moving parts.

Step 2: Diversify your "stability" sleeve without guessing#

If you hold bonds or any other stability-focused holdings, keep the same rule: avoid building a sleeve that depends on one narrow exposure or one product you do not understand. Make sure what you hold matches your risk tolerance, meaning your ability and willingness to handle swings in investment returns.

Verification point: you can state what job your stability sleeve does, and you can describe what you are exposed to without hand-waving.

Final practical check: open your brokerage view and look at your biggest exposures (companies, issuers, sectors, geographies). If you cannot explain what is driving your risk, you likely cannot control concentration.

Rebalancing + Review Cadence: The Simple Schedule That Keeps You in Control#

Treat rebalancing as a rule-based maintenance task so your asset allocation stays intentional instead of drifting over time. Rebalancing your financial portfolio can be a smart investment strategy, especially when you treat it like process, not prediction.

Step 1: Set rule-based rebalancing triggers (calendar + drift bands)#

Pick two triggers and write them into your portfolio policy. You want set rules, not vibes.

| Trigger | When it applies | What you do |

|---|---|---|

| Calendar trigger | On the cadence you choose and will actually follow | Check current vs target asset allocation and decide whether you need to trade, shift new contributions, or leave it alone |

| Drift bands trigger | When a sleeve moves outside acceptable ranges around cash, bonds, or stocks | Consider action if a sleeve moves outside its band |

| Material-change trigger | When liquidity needs or constraints change | Do an off-cycle review to confirm your plan still fits |

- Calendar trigger (scheduled review): choose a cadence you will actually follow. On that date, you check current vs target asset allocation and decide whether you need to trade, shift new contributions, or leave it alone.

- Drift bands trigger (unscheduled review): use simple bands so you stop guessing. Cadence Wealth Partners describes the idea plainly: "When to rebalance, using simple bands instead of guessing." You define acceptable ranges around each sleeve (cash, bonds, stocks), then consider action if a sleeve moves outside its band.

You can also add a third category: material-change triggers. Not market news. Real life. If your liquidity needs or constraints change, it can be worth doing an off-cycle review to confirm your plan still fits.

Hypothetical scenario: your cashflow goes from steady to lumpy. You revisit your cash rules and stability sleeve so you do not force selling.

Step 2: Run a one-page review you can repeat#

Use one page, every time. Keep it boring.

One-page review template (copy/paste):

| Field | What you write |

|---|---|

| Target allocation | Your intended split across cash, bonds, stocks (and the ETFs you use) |

| Current allocation | What you hold today |

| Drift note | What changed (contributions, market movement, withdrawals) |

| Next action | "Do nothing," "rebalance using contributions," or "trade to restore targets" |

| Ops notes | Any transfers to reconcile, including references from ledger journals if you track them |

Complexity check: if you cannot complete this review quickly without spreadsheets and detective work, simplify. Go back to broad ETFs, clearer cash rules, and fewer moving parts.

If "where you live and bank" changes, treat it as an ops change, and consider whether it also affects how and where you hold money. If you are planning a move, start here: Japan Digital Nomad Visa: A Guide to the New 2025 Program.

Common Mistakes + How to Recover When Things Go Wrong (Late Invoices, Market Drops, and Admin Chaos)#

Recover by rebuilding your cash buffer, tightening your ops, and only then returning to your long-term plan. This is your failure plan for the real world: late invoices, market drops, and admin chaos.

Step 1: Stabilize the business layer first (cashflow beats theory)#

Treat every mistake as a systems signal, not a moral failure. The Economic Times puts it bluntly: "Don't let a financial mistake go wasted." Use the mistake to "modify your financial life." That means you change policy, not your mood.

Use this recovery table as your default playbook:

| What broke | The common mistake | Recovery move you can execute this week | "Back to normal" check |

|---|---|---|---|

| Late invoices or lumpy income | Investing before stabilizing operations | Rebuild your cash buffer first. Put contributions on pause until your liquidity needs clear without selling investments | You can cover near-term obligations from cash (not investment sales) |

| Admin or account setup friction | Ignoring onboarding and paperwork early | Finish any required account and tax paperwork before you need speed. Start with: ITIN vs. EIN vs. SSN: What's the Difference? | You can access accounts and move money without last-minute scrambles |

| Revenue risk plus portfolio risk | One client dominates, plus a concentrated portfolio | Reduce business concentration (pipeline) and portfolio concentration (diversification). Consider dialing down risk temporarily if you need stability | No single client or single holding can break your month |

Hypothetical scenario: a key client pays late right as stocks slide. You do not "buy the dip" with bill money. You rebuild cash, then resume contributions.

Step 2: Restore portfolio discipline (records + guardrails)#

Market narratives change fast. You cannot control that. You can control your documentation and your rules.

| Practice | Core action | Supporting detail |

|---|---|---|

| Minimal audit trail | Export statements on a cadence you will follow | Add short notes on transfers and keep the tax documents you receive organized |

| Standardize money movement | Use the same transfer path every time | Label it consistently and confirm each move lands before you schedule the next one |

| Re-enter with conservative principles | Aim to protect capital first, then pursue consistent progress | Keep your asset allocation clear and your risk management boring enough to repeat |

Conclusion: Your Two-Layer Diversification System (Copy/Paste Checklist)#

Build your portfolio by choosing an asset allocation that fits your goals, time horizon, and risk tolerance, then diversifying across different asset classes (like stocks, bonds, and real estate). The win is consistency. You make the same high-quality decision on a calm day and on a chaotic day.

Layer 1: Practical guardrails (so your investing plan stays executable)#

Treat this as your "can I follow through?" layer. You do not need perfect. You need stable defaults you can repeat.

- Define what money must stay available for near-term needs before you invest.

- Keep your plan simple enough that you can follow it without guesswork.

- Keep basic records so you can explain what you did and why later, even if it is just a straightforward transaction log.

Layer 2: Portfolio construction (asset allocation, then diversification)#

Asset allocation is your split across stocks, bonds, and cash, based on your goals, time horizon, and risk tolerance. eToro states: "Consider your financial goals, time horizon and risk tolerance to determine your right asset allocation." Diversification then spreads your investment portfolio across different asset classes so you do not rely on only one bucket. eToro also notes: "diversify your investments across different asset classes, such as stocks, bonds and real estate."

One described approach to diversification is to "purchase disparate assets" across "unrelated and uncorrelated sectors."

If you use ETFs, use them intentionally. Name the exposure you want (asset class, region, style), then verify each fund actually provides it so you do not stack overlapping funds by accident.

If you want to tighten ops further, evaluate tools and providers carefully. Features and coverage can vary by market and program, so confirm what is actually supported before you design around it.

Copy/paste checklist (save this and reuse it):

- I know my baseline near-term cash needs before I invest.

- My portfolio policy states target asset allocation across stocks, bonds, and cash based on my goals, time horizon, and risk tolerance.

- I can explain my diversification in one sentence (including the asset classes I'm using, such as stocks, bonds, and real estate).

- If I use ETFs, I can name the exposure each one is meant to provide.

- I have a simple, repeatable way to review my plan without improvising in the moment.

Frequently Asked Questions

How do I build a diversified portfolio if my freelance income is irregular?

Treat investing as a sweep, not a fixed monthly bill. First fund bills, taxes, and buffer cash, then sweep a percentage of what is left into broad ETFs that match your target asset allocation across stocks, bonds, and cash. If income comes in waves, invest on paid invoice days, not on the calendar.

How much cash buffer should I keep before investing?

Keep enough cash that you can avoid selling ETFs in a bad month. If a late invoice would force you to liquidate holdings to cover near-term obligations, your buffer is too small. Keep buffer cash separate from your investing account so the buffer stays a buffer.

What is the difference between diversification and asset allocation?

Asset allocation is how you split your portfolio across big buckets like stocks, bonds, and cash. Diversification is how you spread risk within each bucket, such as using broad ETFs instead of a few individual stocks. Use allocation to set the risk level you can live with, and diversification to avoid single-point failures inside that level.

How often should I rebalance a small portfolio?

Rebalance on a cadence you will actually follow, then add a drift trigger. A common approach is a calendar check at least annually plus rebalancing if a sleeve drifts beyond your preset threshold. If the review keeps turning into a project, reduce holdings until it stops.

Should I pay down high-cost debt before diversifying investments?

Yes. Treat high-cost debt as negative guaranteed return and address it before you take additional market risk. Keep building your cash buffer in parallel so you do not create new volatility by paying debt aggressively and then needing credit again. After you stabilize, resume ETF contributions aligned to your asset allocation.

How do I reduce risk when one or two clients drive most of my income?

Reduce risk in two places: business concentration and portfolio concentration. On the business side, tighten collections and build pipeline so you are not dependent on one payer. On the investing side, keep a higher cash allocation while concentration is high, and favor broad ETFs over concentrated stocks.

If I work internationally, where do I start with the Foreign Earned Income Exclusion (FEIE)?

Start with FEIE eligibility basics, then work outward to any other reporting that may apply to your situation. To claim it, you must have foreign earned income, your tax home must be in a foreign country, and you must meet a listed status or test such as the physical presence test of 330 full days during any period of 12 consecutive months. You still file a U.S. return reporting the income to claim the exclusion. The IRS lists a maximum exclusion of $130,000 for tax year 2025 and $132,900 for tax year 2026.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

ITIN vs. EIN vs. SSN: What's the Difference?

As the CEO of your business-of-one, you are not here for vibes. You need a repeatable system you can run.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.