Quick Answer

Build one linked workbook with an input sheet for invoice ID, due date, expected collection date, currency, processor, and fee assumptions. Then separate earned revenue from collection timing, add explicit reserve lines for taxes and disputes, and test three cases: client loss, planned time off, and FX movement. Finish each run with a trigger, owner action, and log entry so the model drives decisions instead of passive reporting.

The Solopreneur's Resilience Model: Build a Bulletproof Business, Not Just a Spreadsheet#

Use this model as an operating tool for getting paid and staying liquid, not only as a valuation exercise. If you invoice clients, your real questions are practical: when cash will arrive, what you already owe, and what happens if a client pays late, disputes a payment, or pushes unclear payment terms.

| Decision area | Question answered |

|---|---|

| liquidity | when cash actually lands and leaves |

| obligations | what you owe, even before cash goes out |

| forward planning | what likely happens next under your current billing workflow and client terms |

A 3-statement model gives you that operating view. The income statement tracks what you made and spent over a period. The balance sheet shows what you own and owe at a point in time. The cash flow statement shows how cash moves in and out.

This is where payment protection becomes concrete. Clear terms such as Net 30, Net 45, or Net 60, a thoughtful billing process, and dispute-aware planning all matter because payment timing and reversals directly affect available cash.

This guide follows that logic. First, why standard templates miss the mark. Then how to build a lean base model. Finally, how to stress-test the decisions that protect your cash flow. For a step-by-step walkthrough, see How to Build a Freelance Financial Model That Protects Cash Flow.

Why a Standard Financial Model Fails Your Business-of-One#

If you want a 3-statement model for day-to-day operations, a standard corporate template can be the wrong place to start. Many training workflows are built around reporting inputs and investor outputs. Your questions are different: when cash lands, what is already committed, and what happens if payments are delayed or reversed.

| Area | Typical 3-statement training model | Business-of-one resilience model |

|---|---|---|

| Core inputs | Historical company financials, 10-K, investor presentation | Invoices, payment terms, signed work, expected collections, reserve assumptions |

| Liability focus | Debt/equity structure and high-level expense assumptions | Cash-reserved taxes, payment fees due, dispute exposure, unpaid bills |

| Revenue logic | Trend-led forecast structure | Uneven project timing, booked work, delayed collections, uncertain pipeline |

| Asset focus | Full statement coverage, including longer-term assets | Cash, receivables, prepaid tools, near-term collectability |

| Primary output | Forecasts for valuation or investor discussion | Liquidity view, obligations coming due, downside planning |

| Main decision supported | Growth and financing narrative | Can you stay liquid if payment timing worsens? |

1. Replace hidden obligations. Generic models can underweight the liabilities that matter most to a solo operator. They may prioritize capital structure and broad expense lines over explicit cash reserves for taxes, payment fees, and possible disputes.

Make those obligations explicit reserves, not vague expense lines. Keep separate assumption lines for taxes owed, payment fees due, and dispute exposure. Add a clear note such as Reserve rule pending verification from current jurisdiction and provider terms when a numeric rule is not yet verified.

Checkpoint: the reserved amount should be visible on the balance sheet or a supporting schedule, and the cash flow should show when that cash leaves. Otherwise, the income statement can look healthy while the cash is already spoken for.

2. Forecast timing, not just revenue. One common training workflow uses company financials, a 10-K, and an investor presentation as core inputs. That setup is useful in analyst training, but it may not map cleanly to a solo business with a handful of active clients and uneven collections.

Split the forecast into booked work and uncertain work. Signed work can enter with expected invoice and collection dates. Unsigned work should stay separate until the evidence improves. If a deal is not signed, the model should not treat it as on-time cash.

Checkpoint: projected collections should match how your receivables actually behave. If they do not, your cash view is wrong even when revenue looks fine.

3. Strip out assets that do not help you decide. Version one of a business-of-one model does not need heavy balance-sheet detail. If your template asks for PP&E roll-forwards, inventory logic, or capital-structure inputs before clarifying cash and receivables, it is solving the wrong problem.

Keep assets focused on what you can use or collect soon: cash, receivables, and a short list of prepaid expenses or deposits. You should be able to open the file and answer three questions quickly: how much cash you have, what customers owe, and how much cash is already reserved. Red flag: old receivables treated as fully collectible. Aging invoices should not be modeled the same way as fresh ones.

4. Keep the model aligned and decision-ready. This is where standard modeling discipline actually helps. Separating statement-linking from model checks is useful because any mismatch across the income statement, balance sheet, and cash flow weakens forecast reliability.

Keep the build lean, too. Setup can take at least 30 minutes to several hours, and imbalances are a known Excel failure mode. One source lists 10 common causes, including circular references. If the balance sheet breaks, fix the links before adding more scenarios. A smaller model you can troubleshoot is more useful than a larger one that looks polished but is unreliable.

Once you have stripped the model down to decision-useful parts, build the base file cleanly. If you want a deeper dive, read Hiring Your First Subcontractor: Legal and Financial Steps.

The Foundation: Building Your Core 3-Statement Model in Under an Hour#

Build the core file first, then add reserves, downside cases, and dashboards. For payment operations, start with one reporting currency, a short invoice log, and clean links across the income statement, balance sheet, and cash flow statement.

| Build step | Main inputs or focus | Key output or check |

|---|---|---|

| Income statement | signed invoices or earned work by month, processor fees, operating expenses, optional separate line for uncertain work | calculates gross revenue, processor-fee impact, and net income |

| Balance sheet | cash, accounts receivable, short prepaids or deposits, accounts payable, explicit reserve lines, equity as the residual from cumulative results | shows period-end position under Assets = Liabilities + Equity |

| Cash flow statement | net income link, working-capital movements, especially A/R and A/P changes, payout timing lag, processor fees and FX effects once | calculates operating cash flow and ending cash |

| Link and test | net income should flow to both the balance sheet and cash flow statement, and ending cash on the cash flow must equal balance-sheet cash | fix the links before adding taxes, scenarios, or charts |

Before you start, create one input sheet and keep every assumption auditable.

Enter:

- invoice ID

- client

- invoice currency

- reporting currency

- invoice date

- due date

- expected collection date

- settlement currency

- receivables status

- processor

- fee assumption

- notes

For any unverified fee, FX rule, tax reserve, or payout delay, label the assumption as pending source, advisor, or business verification. Track receivables status as an operating field. A simple aging view, for example current, 1-30, 31-60, 61-90, >90, can help prioritize collection actions. If invoice or charge currency differs from settlement currency, add a conversion assumption instead of treating them as the same.

1. Build the income statement. Start with earned revenue by period, not cash receipts. Keep accrual timing and collection timing separate from day one.

What you enter:

- signed invoices or earned work by month

- processor fees

- operating expenses

- optional separate line for uncertain work, not merged into the signed forecast

What it calculates:

- gross revenue

- processor-fee impact

- net income

Why it matters:

- net income must link into both the balance sheet and cash flow statement

Quick check: run a month with high collections but no new earned work. Revenue should stay low while cash can still rise.

2. Build the balance sheet. Keep the balance sheet point-in-time and limited to accounts that help you decide.

What you enter:

- assets: cash, accounts receivable, short prepaids or deposits if relevant

- liabilities: accounts payable and explicit reserve lines you already use

- equity as the residual from cumulative results

What it calculates:

- period-end position under

Assets = Liabilities + Equity

Why it matters:

- receivables are customer amounts owed and are often the main gap between profit and liquidity

- mixed invoice and settlement currencies need translation logic, not mixed balances

Quick check: ending A/R should follow opening A/R + credit invoiced - collections. If old >90 balances never change but you still assume full collection, your cash forecast may be overstated.

3. Build the cash flow statement. This is where timing becomes visible. Start from net income and reconcile to cash.

What you enter:

- net income link

- working-capital movements, especially A/R and A/P changes

- payout timing lag between customer payment and bank availability

- processor fees and FX effects once, with consistent treatment

What it calculates:

- operating cash flow

- ending cash

Why it matters:

- collection timing and payout timing can diverge, and payout availability varies by country and industry

- if you use Stripe, verify current payout timing for your account, country, and industry before modeling cash availability

Quick check: if collections improve, operating cash flow should improve even when revenue is flat. If payout timing slips, cash should shift later without changing earned revenue.

4. Link the statements and test them. Link first, then add detail. Net income should flow to both the balance sheet and cash flow statement, and ending cash on the cash flow must equal balance-sheet cash.

| Linkage | Formula logic | Common setup error | Quick validation check |

|---|---|---|---|

| Net income | Income statement net income flows to equity and starts cash flow reconciliation | Separate hardcoded profit in cash flow | Change one expense input; net income updates everywhere |

| Accounts receivable | Ending A/R = Opening A/R + credit invoiced - collections | Treating all revenue as same-period cash | Run invoicing with no collection; A/R rises, cash does not |

| Accounts payable | Ending A/P = Opening A/P + unpaid expenses - cash paid | Wrong sign in operating cash flow | Delay one vendor payment; A/P rises and operating cash improves temporarily |

| Ending cash | Cash flow ending cash equals balance-sheet cash | Counting processor-held funds as bank cash too early | Both statements show exactly the same ending cash |

If the model does not tie, stop there and fix the links before adding taxes, scenarios, or charts. We covered this in detail in A Guide to Creating a 'Pro Forma' Financial Statement.

The Fortification: Forging a True Resilience Model#

Once the file ties, fortify it for disruption, not presentation. Add a few operating schedules that show where cash is most exposed, then review them on a fixed cadence.

1. Add a tax schedule you can verify and update. Build a separate tax tab, and label every unverified rule as pending advisor or business verification. Keep the structure simple and auditable.

| Input block | What to enter |

|---|---|

| Tax base inputs | Tax base definition pending advisor verification |

| Rule set | Threshold or rate pending advisor verification |

| Payments already made | Estimated/actual prepayments |

| Open items | Uncertain treatments marked for follow-up |

Use a provisional flow and mark each step for verification before relying on it: draft your forecast tax base, apply only verified rules, subtract payments already made, and flag any remaining amount for follow-up.

Link it across all three statements as a draft map, then confirm each linkage before finalizing.

- map tax assumptions to the income statement, balance sheet, and cash flow statement

- keep any unverified linkage marked for follow-up

Add a short revision log on the same tab: date, assumption changed, verification status.

2. Build runway as an operating framework, not one number. Runway is more useful when it is tied to actions, not just a headline figure. Start by splitting cash into:

- available bank cash

- pending or processor-settling cash

- reserved cash

- unavailable or held cash

Then map committed outflows before variable spend. You rarely have time for a full redesign under budget pressure, so predefine a short list of variable cuts you can make quickly if runway weakens.

Set trigger-based actions with trigger states pending business verification:

| Trigger state | Immediate action | Owner |

|---|---|---|

| Runway trigger pending business verification | Pause lowest-priority variable spend | You |

| Receivables trigger pending business verification | Tighten collection follow-up cadence | You |

| Commitment trigger pending business verification | Re-sequence noncritical commitments | You |

3. Monitor client concentration with clear ownership. Client concentration can become harder to manage when it combines with weak payment behavior, so track both together. Use a compact table that updates from your forecast and forces a response when concentration risk rises.

| Client | Share of forecast revenue | Payment behavior | Contract risk signals | Mitigation owner |

|---|---|---|---|---|

| Client A | [enter %] | on-time / delayed / disputed | renewal uncertainty / scope drift / weak payment terms | You |

| Client B | [enter %] | on-time / delayed / disputed | renewal uncertainty / scope drift / weak payment terms | You |

| Client C | [enter %] | on-time / delayed / disputed | renewal uncertainty / scope drift / weak payment terms | You |

Review this alongside receivables aging. If concentration and payment friction worsen at the same time, treat it as an operating trigger, not just a reporting note.

4. Add a payment-risk layer that flows into cash stress tests. This layer should be scenario-driven. Test the disruption that would hurt most and the control that would reduce the impact, even when you do not have precise probabilities.

Route these stressors explicitly:

| Stressor | Model input | Cash-flow impact |

|---|---|---|

| Delayed payment | Shift expected collection timing later | Cash arrives later |

| Dispute/chargeback | Reduce or reverse expected collections | Cash decreases in affected periods |

| Processor hold | Move funds to unavailable cash bucket | Spendable cash drops even if revenue was recognized |

With that layer in place, a delayed payment, dispute, or processor hold changes spendable cash in a visible way. You can see where cash is most exposed, what control to apply first, and who owns the response.

Related: The Best Bank Accounts for Freelancers in Germany.

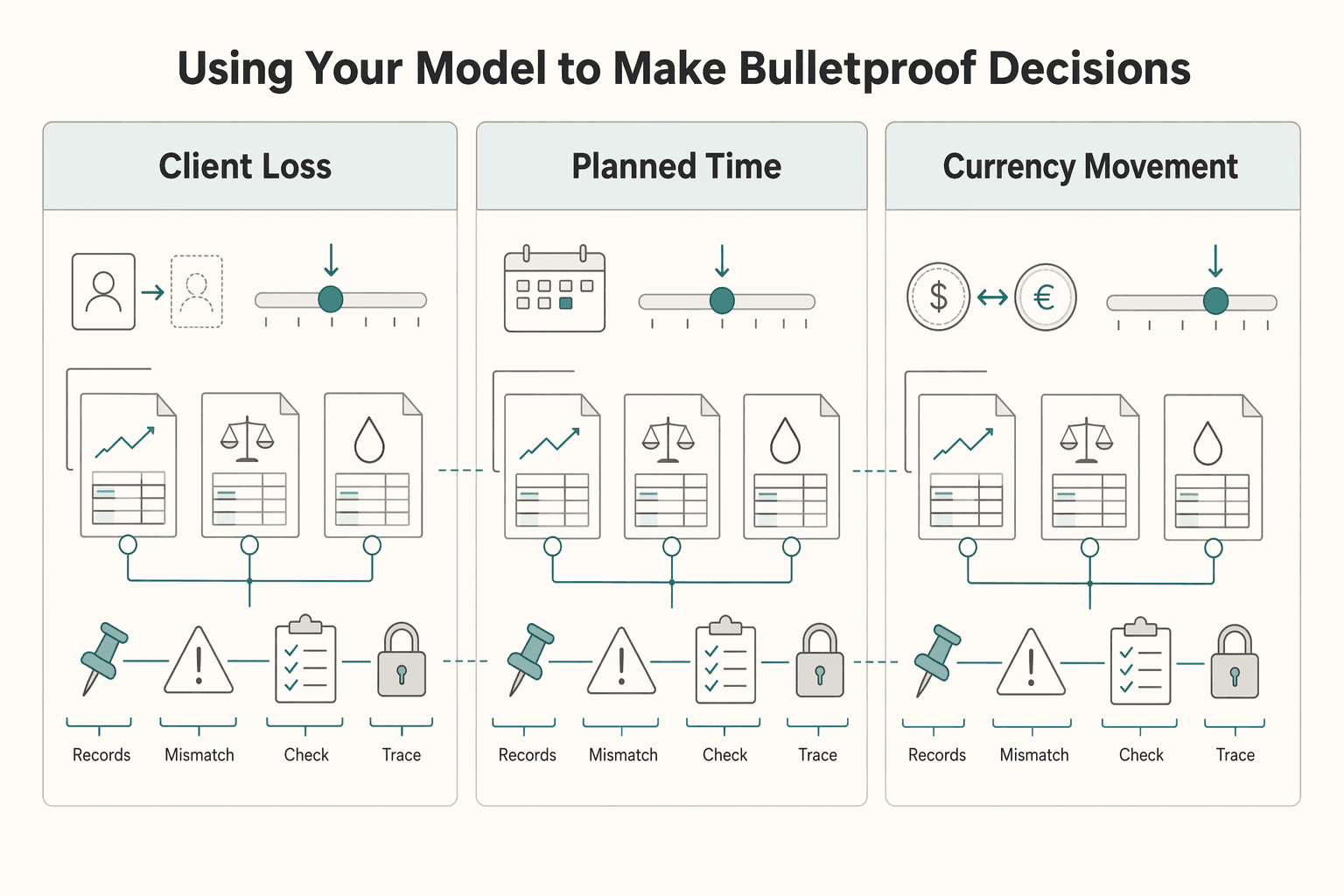

The War Room: Using Your Model to Make Bulletproof Decisions#

Use this part of the model to turn uncertainty into a decision. Change a few assumptions, trace the impact across all three statements, and choose the next move. If a scenario does not end with a trigger, an action, and a logged decision, it is only a forecast.

Run assumption-driven scenarios, not single-point guesses. Change the input tied to the risk, such as pipeline close probability, receivables timing, owner draw treatment, or currency conversion timing. Then confirm that the income statement, balance sheet, and cash flow statement remain linked.

| Scenario | Inputs You Change | Primary Metrics to Watch | Decision Trigger | Immediate Action |

|---|---|---|---|---|

| Client loss | Set affected client revenue to zero or lower close probability by stage; extend receivables timing for delayed or disputed invoices | Revenue, accounts receivable, tax liability line, operating cash runway | Runway falls below your verified threshold or replacement pipeline does not cover the gap | Freeze low-priority spend, adjust owner draw where appropriate for your entity, shift sales effort to replacement work |

| Planned time off | Zero new revenue for leave period; keep fixed costs; model owner draw separately from operating expense where relevant | Net cash burn, ending cash, tax payments due, runway | Required reserve exceeds available bank cash plus planned collections | Shorten leave, pre-fund the gap, or move leave after collections land |

| Currency movement | Change FX assumptions at transaction-date spot rates; test conversion timing for foreign receipts and tax funding | Home-currency margin, spendable cash after conversion, tax funding gap | Spendable cash or tax funding falls below your verified threshold | Convert earlier, hold a buffer in the payment currency, or tighten pricing and terms |

1. Remove one client and trace the gap. Start with the simplest hard test: remove one client. Take that client out of forecast revenue, or set the pipeline probability to zero if the work is still unsigned, and push receivables timing later if collections may slip.

Then trace the effect across the statements. Revenue and profit fall on the income statement. Receivables and the tax liability shift on the balance sheet. The cash flow shows fewer or later collections, which reduces runway.

Decision: if runway or replacement pipeline misses your trigger, execute your pre-set spend and pipeline actions immediately.

2. Model planned time off as a cash event. Time off is not just a calendar choice. It is a cash timing event, so model it that way. Zero out new revenue during leave months, keep fixed expenses in place, and model owner draw based on entity treatment rather than as a default operating cost.

Then trace what happens. Collections may still come in from existing receivables even while new sales pause, but cash outflows and tax obligations continue. For US estimated tax planning, keep the four payment periods in view: April 15, June 15, Sept. 15, and Jan. 15 (following year). Underpayment can create penalties.

Decision: if reserve coverage comes up short, choose now between shortening leave, pre-funding the gap, or shifting leave timing.

3. Test currency movement where conversion timing matters. If you invoice or settle across currencies, conversion timing can create a real funding gap. Use transaction-date spot rates for initial recording, then test how conversion timing changes cash and tax funding instead of relying on a single blended rate unless that is your explicit method.

Then check the knock-on effects: profit in home currency, receivables value, cash available after conversion, and tax funding needs.

Decision: if conversion timing creates a funding gap, set a conversion rule and buffer policy now.

4. Run cadence and decision log. The model is only useful if it gets used at the right moments. Set a simple cadence and keep a decision log.

- run weekly when pipeline stages or close probabilities are moving

- re-run immediately after a major client delay, a leave decision, or a change in invoicing or conversion practice

- log each run in a scenario tab: date, assumptions changed, outputs reviewed, decision, owner, next review date

- if any metric crosses its verified threshold, record it and execute the action the same day

You might also find this useful: How to Create a Financial Forecast for a Funding Round.

After you run your downside scenarios, lock in payment timing and scope assumptions in your next client agreement with the SOW Generator.

From Anxious Operator to Confident CEO#

Your model is only useful if each review ends with a decision. Built this way, a 3-statement model can turn income volatility, uneven payment timing, and tax set-aside pressure into specific next actions.

| Statement | Clear job | Main focus |

|---|---|---|

| Income statement | profit levers | revenue, costs, and profit over time |

| Balance sheet | resilience | assets, liabilities, equity, and whether obligations are outpacing available cash |

| Cash flow statement | timing | how cash moves in and out, and how payment delays change your position |

1. Give each statement one clear job. The income statement is for profit levers across revenue, costs, and profit over time. The balance sheet is for resilience: assets, liabilities, equity, and whether obligations are outpacing available cash. The cash flow statement is for timing: how cash moves in and out, and how payment delays change your position.

Verification point: after any assumption change, all three statements should move together. If profit changes but cash or liabilities do not, fix the linkage before making a call.

2. Run scenarios by changing one driver, checking the next metric, then deciding.

| Scenario | Change this assumption | Check this next | Make this decision |

|---|---|---|---|

| Biggest client delays or disappears | Lower expected revenue or collection timing | Ending cash and receivables on cash flow and balance sheet | Cut optional spend, accelerate outreach, or tighten invoice terms |

| You want time off | Reduce billable work and add owner draws or fixed expenses | Cash balance, taxes owed, and reserve gap | Set a reserve target once advisor or business verification is complete, and delay the break if the gap is too wide |

| FX risk affects your work | Apply an FX shock range once source or advisor verification is complete to foreign-currency revenue or costs | Net profit on the income statement and cash timing | Reprice, convert cash sooner, or keep terms as-is |

3. Support the model with a few non-negotiable controls. A rejected invoice is not just admin friction. It can delay cash. If you invoice EU B2B clients, treat the invoice as a legal document and verify required details before sending.

If cross-border rules apply to you, keep a simple days-by-jurisdiction table. Review it against thresholds that may matter in your case, such as 183 days in one country or 90 days within a rolling 180-day Schengen window. If you hold foreign accounts, set a recurring monthly reminder to total balances in USD. That helps you spot whether FinCEN Form 114 may be triggered if aggregate value exceeds $10,000 at any point in the calendar year. That is the operator-to-CEO shift in practice: fewer guesses, faster checks, clearer decisions.

This pairs well with our guide on How to Read a Cash Flow Statement.

When your model is ready, put it into practice by issuing cleaner client invoices with the Free Invoice Generator.

Frequently Asked Questions

How do you build a 3-statement financial model for a one-person business?

Build one workbook where the income statement, balance sheet, and cash flow statement are fully linked. Keep only the lines that reflect how the business earns and spends cash so each assumption change flows through the full model. Add basic checks and balances so you catch broken links early instead of patching outputs later.

How should you forecast revenue when your work comes in projects, not subscriptions?

Use assumption-based scenarios, not one top-line guess. Track expected project value and timing assumptions, then test different cases. Confirm those assumptions flow into working capital and cash flow so the model stays connected.

How do you include tax planning without turning the model into a tax return?

Keep taxes as a planning input in the model instead of trying to replicate a full tax return. The goal is visibility inside the linked model as assumptions change, not tax-form-level precision.

What is the practical difference between a corporate valuation model and a freelancer operating model?

For this FAQ, focus on operating use: testing assumptions and seeing how changes ripple through income, balance sheet, and cash flow. Valuation-focused work can require additional assumptions that are outside this operating workflow.

How do you use the model for what-if planning without wasting time?

Change one assumption tied to one risk, then trace the effect across all three statements. If you adjust revenue or timing assumptions, income, balance sheet, and cash flow should all move in a consistent way. If one statement changes and the others do not, fix the linkage before making a decision.

What assumptions matter most in a freelancer model?

Start with the assumptions that move cash fastest: revenue, expense, and timing inputs. Make sure revenue assumptions flow through to working capital and cash outcomes. Add extra inputs only when they change a real decision.

How do you know the model still works after you update it?

Run a quick control check after each update: the balance sheet balances, ending cash ties across statements, and core outputs come from linked assumptions instead of manual patching. Broken linkage usually shows up as one statement updating while another stays stale. Catching that early keeps scenario work fast and usable.

How should you use this weekly?

Review projections against actuals on a regular cadence, and use weekly when cash movement is active. If you track 52 weekly periods, each review should update assumptions and compare projected versus actual cash results. End every review with a decision: keep plan, cut spend, accelerate collections, or revise the forecast.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- dot.ca.gov/-/media/dot-media/programs/aeronautics/docum...trusted

- ebudget.ca.gov/2026-27/pdf/BudgetSummary/FullBudgetSummary.pdftrusted

- faa.gov/documentLibrary/media/Advisory_Circular/AC_1...trusted

- federalregister.gov/documents/2025/01/15/2025-00636/framework-fo...trusted

- irs.gov/businesses/small-businesses-self-employed/es...trusted

- irs.gov/businesses/small-businesses-self-employed/pa...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC8424774trusted

- sba.gov/business-guide/manage-your-business/manage-y...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

The Best Bank Accounts for Freelancers in Germany

Pick the account that protects cashflow and keeps records clean when client behavior gets messy, not the one with the nicest app.

How to Create a Financial Forecast for a Funding Round

Treat your forecast as a system first and an investor document second. If it does not help you decide hiring pace, spending, and cash runway in the near term, it is not ready yet. Three terms matter here: