Quick Answer

To automate personal finances safely, use a risk-first system instead of a generic set-and-forget setup. Put high-consequence bills on protected autopay first, fund a buffer and tax set-asides next, and only then automate savings and investing from cleared receipts. Add pause rules, approval gates, and a monthly reconciliation check so one late or disputed payment does not destabilize your cash flow.

You don't need "better money habits" - you need a risk-first automation operating system#

Build a risk-first financial system that handles timing uncertainty first, then automates the rest. If you want to automate personal finances, the real upgrade is moving from "try harder" habits to a system that keeps working when real life gets messy. If you run a business-of-one, you want rules, triggers, and checks that still hold up when money shows up later than expected.

A common failure mode: timing mismatch, not forgetfulness#

If you invoice clients, you can do everything "right" and still feel squeezed when cash-in timing and cash-out timing do not match. That mismatch creates stress and rushed decisions you would never make on a calm Tuesday.

Say you schedule bill pay perfectly, then a client goes quiet. You start floating essentials on a card, delay a tax set-aside, and pause automatic savings you meant to keep consistent. Nothing about that chain comes from bad character. It usually comes from a setup that assumes regular pay timing.

You might even copy a checklist from a Reddit thread (even r/personalfinance), but generic advice often assumes predictable income. As an operator, you want automation that waits for confirmed cash, not optimism.

One framework: decision order + guardrails + exceptions#

Run personal finance automation like a tiny finance team.

1) Set a decision order (your default "what gets funded first"). Cover high-consequence obligations first, then stability, then growth.

| Priority | What it covers | Automation stance |

|---|---|---|

| 1 | Bills with penalties or service risk | Use automation that prioritizes these from a dedicated bills pool |

| 2 | Buffer and tax parking | Fund before discretionary transfers |

| 3 | Automatic savings and investing | Only after Priority 1 and 2 stay intact |

| 4 | Nice-to-haves | Automate last, cancel fastest |

2) Add guardrails (so automation can't surprise you).

- Keep a buffer floor and treat it like a policy, not a vibe.

- Separate "money to spend" from "money to protect."

- Trigger savings transfers from paid and cleared inflows, not from invoice send dates.

3) Plan for exceptions (so you stop improvising under stress). Create a short script for late payments, partial payments, and surprise outflows. Decide what pauses first, what stays live, and what you review manually.

If you want a concrete tool-and-workflow layer after this mindset shift, use Automating Your Freelance Finances: A Guide to Tools and Workflows.

What does "automate personal finances" mean when your income is irregular?#

When your income arrives in lumps, "automate personal finances" is less about clicks inside an app and more about setting up repeatable workflows plus a way to verify they actually ran. For founders, freelancers, and self-employed professionals with irregular income, it can feel like a second job, especially when you are juggling late invoices, partial payments, and timing weirdness.

A useful way to think about automation here is as an ops layer: decide what happens, when it happens, and how you will confirm it worked. Apps can execute steps, but your system is what keeps you safe. That "check" layer can be as simple as a spreadsheet or as structured as a double-entry ledger (for example, Beancount stores transactions in a plain-text file and requires transactions to balance).

Two kinds of automation (and why one can break freelancers)#

Treat these as different tools in your financial system, because they fail in different ways. Bill automation helps you stay on schedule. Cash-flow automation helps you avoid moving money before it has actually arrived.

| Automation type (how this guide uses the term) | What it controls | Best for | Primary failure mode |

|---|---|---|---|

| Bill automation | Recurring or scheduled payments | Rent, insurance, minimum debt payments | You schedule it, but cash arrives late, so you trigger fees or interest |

| Cash-flow automation | Transfers you run based on what has actually hit your accounts | Automatic savings, tax set-asides, investment automation | You move money too early, then you reverse transfers or scramble to cover obligations |

If you only automate bill pay, you still carry a lot of manual decision-making. With irregular income, money management often means tracking inflows from multiple sources, moving money for taxes, staying on top of bills, and deciding what is safe to spend. That "safe to spend" decision never disappears, so you have to operationalize it.

A two-lane model (clean, repeatable, audit-friendly)#

One practical approach is to run two lanes so each lane has one job.

- Lane A (Fixed-date lane): Put predictable obligations on a schedule, and fund that lane first with a buffer so timing noise does not leak into essentials.

- Lane B (Event-trigger lane): Tie automatic savings and transfers to cash events you can verify, such as "deposit posted," not "invoice sent."

Example: a client pays, but a platform flags the transaction and delays settlement. If you already swept "savings" out of your bills lane, you force yourself into reactive card spending. If you run the two-lane model, Lane A stays boring and paid, and Lane B waits.

Build your "what if money doesn't land?" plan on day one. Assume a payment can arrive late, get held, or get reversed. Reality check: if one delayed client payment could push you into late fees or high-interest debt, install safeguards before you trust any set-and-forget flow.

If you want a deeper dive, read The Best Personal Finance Apps for Freelancers.

Prerequisites: what to prep before you automate anything (15 minutes that prevents 90% of failures)#

Prep a small, verifiable "inputs pack" before you automate anything. Automation only executes the rules you feed it, including the wrong ones. Once you separate fixed-date obligations from event-trigger transfers, clean inputs become the difference between "helpful automation" and "automated chaos."

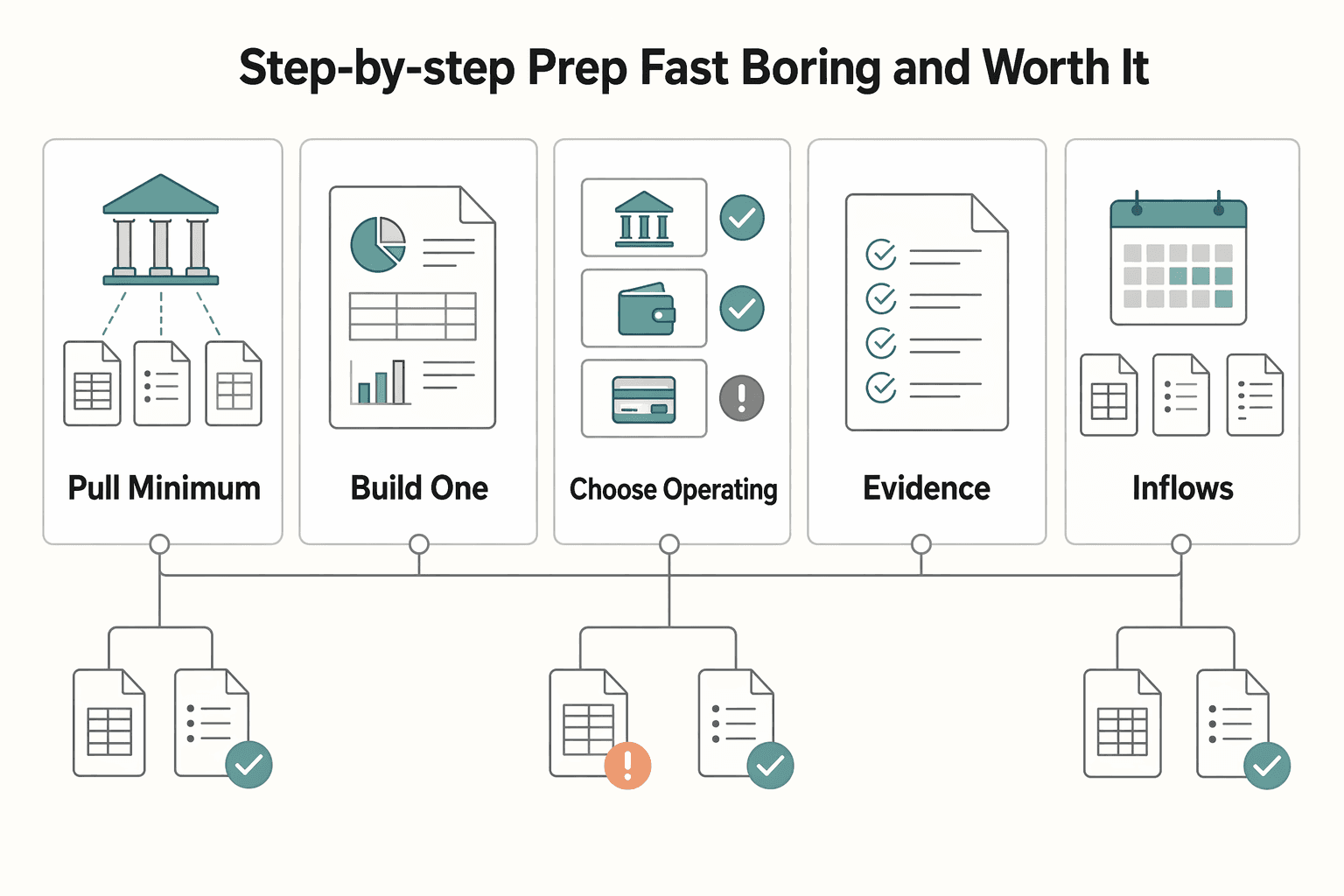

Step-by-step prep (fast, boring, and worth it)#

Step 1: Pull your minimum data set (one export beats ten guesses). Grab recent transaction history from the accounts you actually use, plus your current list of bills. Don't aim for perfection. Aim for coverage.

| Prep step | What to prepare | Why it matters |

|---|---|---|

| 1. Pull your minimum data set | Recent transaction history from the accounts you actually use, plus your current list of bills | One export beats ten guesses, and the goal is coverage |

| 2. Build a one-page money map | Inflows, outflows, and risk items | Shows which inflows you can trust quickly, which items must never miss, and what can trigger late fees or Penalty APR |

| 3. Choose your operating accounts | Bills role, buffer role, spending role, and optional landing role | Uses separation, not complexity |

| 4. Create two control documents | SOW payment schedule summary and client onboarding checklist | Keeps dates or milestones, amount due, payment method, who approves, and payment-risk flags in reusable docs |

- Transaction history: deposits, transfers, card payments, bank fees, refunds.

- Bill list: payee, due date, minimum due (especially for credit cards), and payment method.

Step 2: Build a one-page "money map." Make this a single doc or note you can keep open while you wire automations.

| Lane | What to list | What you're looking for |

|---|---|---|

| Inflows | Client payment methods (ACH, card, international transfer) and typical clearing timing in your world | Which inflows you can trust quickly versus ones you should treat as "pending" |

| Outflows | Fixed obligations (rent, insurance, minimum debt payments) vs variable spending | Which items must never miss, and which you can pause |

| Risk items | Anything that can trigger late fees or Penalty APR | The "do not mess this up" list your system protects first |

Step 3: Choose your operating accounts (separation, not complexity). If you want simple separation, assign accounts "roles" like this:

- Bills role: pays fixed obligations.

- Buffer role: holds stability cash and tax parking.

- Spending role: daily discretionary.

- Optional landing role: receives client payments first.

If you use Mercury, note two operational details that affect automation design. Mercury states its core banking services and essential tools cost $0/mo, and it states it has no monthly overdraft fees or minimum balance requirements. Mercury also states subscription payments pull from your primary account balance, and the billing cycle begins on the first of the month, so keep your primary account funded if you rely on plan features.

Step 4: Create two control documents you will reuse#

- SOW payment schedule summary (one page): dates or milestones, amount due, payment method, and who approves.

- Client onboarding checklist: flags payment risks upfront (deposit or retainer requirement, late fee terms, dispute process).

Practical check before you move on: you should be able to point to your next four due dates and state the minimum cash you must keep available to avoid fees this month. If you cannot do that, pause automation and tighten inputs first.

Example: a client pays by card, the deposit shows up, then a refund hits. If you already automated a sweep into savings based on "money arrived," you create a scramble. If you map inflows and tag risk items first, you can wire triggers to cleared, reliable cash instead.

What should you automate first (without overdrafts) if cash is uneven?#

Start risk-first: automate on-time minimum payments first, then add a buffer, then automate savings and investing. Done right, automation reduces day-to-day decision load without setting up transfers that fail when cash timing gets weird.

Ramit Sethi frames the real benefit clearly: "Using automation to reduce choices sets you up for success with money." He also pushes you to "Think about the 50+ money decisions you have to make today." The job is to reduce choices while protecting the downside.

Step 1: Use a risk-first checklist (not aspiration-first)#

Run this list in order. Treat it like an operator's runbook, not a motivation poster.

- Minimum payments you cannot afford to miss: anything where a missed payment can trigger late fees or a hit to your credit score.

- Buffer: stabilize first because "unexpected expenses will pop up."

- Savings/investing: automate after stability.

- Nice-to-haves: subscriptions and discretionary.

Example: a client invoice slips. If you automated investing before you automated minimum bills, you just turned a timing issue into a fee problem.

Step 2: Convert the checklist into rules (so the system runs itself)#

Use rules you can audit. Skip "vibes." The Modern Savvy CPA nails the cost of sloppy setup: "One missed payment can lead to late fees or a hit to your credit score."

- Bills autopay fires only from your Bills account. Keep income landing and daily spending out of the blast radius.

- Buffer transfer runs before discretionary transfers. Fund stability before lifestyle.

- No Surprises rule: if buffer drops below your minimum threshold, pause savings and discretionary transfers and require manual approval to restart.

Step 3: Choose fixed-date vs event-trigger automation (use the right tool)

| Automation type | Best for | Trigger | Operator default |

|---|---|---|---|

| Fixed-date | Rent, utilities, minimum debt payments | Calendar date | Use dates when timing is predictable |

| Event-trigger | Set-asides and savings sweeps | When income arrives | Use triggers when income timing varies |

Confidence check: if generic advice you saw on Reddit or r/personalfinance would let one late client payment knock over your bill pay, you have not earned "set it and forget it" yet. Fix sequencing first, then add more automation.

For tool ideas once sequencing works, use Automating Your Freelance Finances: A Guide to Tools and Workflows.

The 7-step risk-first automation playbook (with checks at each step)#

Build finance automation by controlling where money lands, where obligations pull from, and when transfers trigger, then verify each link with a simple check. With sequencing in place, the next step is wiring a setup you can run calmly. This is how you manage cash flow without letting a late client payment or messy account structure create avoidable chaos.

The playbook (risk-first, operator-friendly)#

Step 1: Create a clean income landing zone. Route every client payment to one landing account so you reconcile deposits in one place. One option is Mercury, which positions itself as a fintech company (not an FDIC-insured bank) and says it offers finance automations like invoicing and bill pay. Check: In a regular review, you can match every "paid" invoice to a corresponding deposit without hunting across accounts.

| Step | Action | Check |

|---|---|---|

| 1 | Create a clean income landing zone | You can match every "paid" invoice to a corresponding deposit without hunting across accounts |

| 2 | Split obligations from discretion with a Bills account and a Spending account | The Bills account holds enough to clear upcoming minimum obligations without borrowing from Spending |

| 3 | Automate minimum viable bills first | Autopays are scheduled with enough lead time that you are not relying on last-day timing |

| 4 | Add a buffer transfer with a hard floor | If the buffer falls below the floor, your system pauses automatic savings and investing |

| 5 | Create a separate tax holding account and move a portion of cleared receipts into it | You can explain the rule and trigger in one sentence to your future self |

| 6 | Automate savings and investing last, using a portion of cleared inflows | A missed invoice does not force you to unwind a bunch of transfers |

| 7 | Install an audit loop | You can prove where money went if a payment gets reversed or a dispute hits |

Step 2: Split obligations from discretion (two-account minimum). Run a Bills account for fixed-date bill pay and a Spending account for daily use. Keep the debit card tied to Spending, not Bills. Check: the Bills account should hold enough to clear upcoming minimum obligations without borrowing from Spending.

Step 3: Automate "minimum viable bills" first. Turn on autopay for minimums (credit cards, utilities, insurance) before you automate anything that "feels productive." Check: autopays should be scheduled with enough lead time that you are not relying on last-day timing.

Step 4: Add a buffer transfer with a hard floor. Sweep money into a buffer on a steady cadence until you hit your floor (define it in terms you can actually defend, not vibes). Check: if the buffer falls below the floor, your system pauses automatic savings and investing.

Step 5: Automate taxes like a business (because you are one). Create a separate tax holding account and set a clear rule for moving a portion of cleared receipts into it (rules vary by jurisdiction and situation). Check: you should be able to explain the rule and trigger in one sentence to your future self.

Step 6: Automate savings and investing last (and conditionally). Only trigger savings and investment automation after you satisfy the buffer floor, using a portion of cleared inflows. Check: your rules should be set up so a missed invoice does not force you to unwind a bunch of transfers.

Step 7: Install an audit loop. Block time for reconciliation and periodic rules review. Check: you can prove where money went if a payment gets reversed or a dispute hits.

Your "safe default" wiring map#

| Component | Job | Automation trigger | Verification check |

|---|---|---|---|

| Income landing | Capture all inflows | Client payment clears | One place to reconcile |

| Bills account | Protect bill pay | Fixed dates | Minimum obligations covered |

| Buffer and tax | Absorb timing risk | After cleared receipts | Floor and rules still hold |

Hypothetical: you read a "set it and forget it" thread on Reddit or r/personalfinance and automate investing immediately. A client pays late, your bills pull anyway, and you spend your week unwinding transfers. Follow the playbook instead, and the system degrades gracefully.

How do you automate savings (and investing) when client payments are unpredictable?#

Automate savings around money you actually receive, not around a fixed calendar date. Many people set up automation so that each time they get paid, a portion is automatically deposited into savings or investments. If your income is irregular, build in simple guardrails so transfers do not get ahead of your cash flow.

Step-by-step: the "slice-of-receipts + pause rule" setup#

Step 1: If fixed-dollar transfers don't fit, use a percentage mindset. An automated savings plan typically withdraws a specific amount from your bank account and deposits it into a savings or investment account. If a fixed monthly number is hard with uneven income, take a consistent slice of whatever comes in, when it comes in, and translate that into your transfer amount.

| Rule | What it says | Purpose |

|---|---|---|

| Use a percentage mindset | Take a consistent slice of whatever comes in, when it comes in, and translate that into your transfer amount | Fits uneven income better than a fixed monthly number |

| Add a pause condition | Temporarily stop discretionary transfers when your buffer is under pressure | Protect essentials first, then savings, then investing |

| Use a two-stage flow | Stage 1 routes transfers to your buffer until you hit your floor; Stage 2 routes transfers toward investing once Stage 1 is consistently satisfied | Makes growth transfers conditional on stability |

If your bank lets you edit scheduled transfers, keep one on the books and adjust the amount during your regular money review so it stays anchored to recent receipts.

Step 2: Add a rule that pauses savings when stability drops. A pause condition is a rule that temporarily stops discretionary transfers when your buffer is under pressure. The point is to protect essentials first, then savings, then investing, so automation does not create a new problem you have to unwind manually.

Step 3: Use a two-stage flow (simple, durable).

- Stage 1 (stability): Route transfers to your buffer until you hit your floor.

- Stage 2 (growth): Once Stage 1 is consistently satisfied, route transfers toward investing on a cadence you can comfortably maintain.

Use this decision table as a safe default.

| Situation | Savings action | Investing action | Operator check |

|---|---|---|---|

| Buffer below floor | Pause | Pause | Bills still clear without pulling from savings |

| Buffer at or above floor | Transfer a slice to savings | Optional scheduled transfer | You can reconcile transfers to deposits in one sitting |

Cadence: match your invoice reality (not a paycheck fantasy)#

An automated savings plan can move money automatically at a frequency you choose (once a month, biweekly, weekly). Pick a cadence that matches how you actually get paid and how often you're willing to check in and adjust.

If you're still building stability, one common irregular-income strategy is to build an emergency fund sized to cover at least one to three months of expenses, and to consistently grow savings with automatic transfers. Once the cushion is there, you can also automate investing. For example, one approach is setting up an automatic weekly deposit into an investment account that requires little to no ongoing effort.

Avoid the trap where "set it and forget it" becomes the goal. Your goal is financial system reliability.

Example: a client pushes payment out unexpectedly. If you would need to pull money back out of savings to cover bills, your automation is too aggressive. Tighten the pause rule, not your willpower.

For deeper tooling workflows, see Automating Your Freelance Finances: A Guide to Tools and Workflows.

Want a quick next step for "automate personal finances"? Try the free invoice generator.

Safeguards that make automation safe: policy gates, buffers, and auditability#

Make automation safe by adding the same controls a finance team uses: approval gates, pause rules, and a paper trail you can reconcile quickly. Once your automation is event-triggered and buffer-first, guardrails are what keep one weird payment event from turning into fees, reversals, or confusion.

Step-by-step: install gates + auditability (operator-grade)#

Step 1: Set policy gates (your "CFO approval"). Pick an approval threshold where you require manual review before any transfer or bill pay happens. Do not overthink the number. You just need a line that catches mistakes and fraud.

Add pause conditions that stop discretionary moves when any of the following happens:

- Buffer drops below your floor.

- You see an unusually large outflow you did not plan.

- You spot potential chargeback exposure (for example, a large card payment from a new client).

Step 2: Standardize traceability in every transfer. Your future self cannot debug mystery transactions, so require a memo standard:

InvoiceID | Client | Purpose | Category(example:INV-104 | ClientCo | Buffer top-up | Stability)- Store the related doc (invoice, SOW, even an NDA if relevant) in the same client folder.

If you run a platform setup like Mercury plus modular money movement, insist on clean reconciliation. At minimum, use tools that let you sync transaction details into accounting software (Mercury says it supports this for free). If you bank elsewhere, keep your reconciliation workflow consistent so your weekly review stays frictionless.

Step 3: Enforce a "no duplicates" rule. Treat every trigger as a one-time instruction. When you move money, include a unique reference (invoice number and client name) so you can spot duplicates instantly and correct the right thing.

| Control | What it prevents | How you implement it |

|---|---|---|

| Approval threshold | Fat-finger transfers, fraud | Manual review above your set limit |

| Pause conditions | Overdrafts, forced reversals | Buffer floor and "unusual outflow" stops |

| Memo standards | Confusion during reconciliation | Invoice ID + client + purpose every time |

Step 4: Add a card-heavy client safety rule (chargeback-aware)#

If you accept card payments (Mercury invoices can take card and bank transfer methods), treat those funds as provisionally available. Do not sweep them aggressively into savings or investment automation until you feel confident the payment will stick. This is where "set it and forget it" advice can mislead operators.

Practical check: you should be able to answer, without guessing, "What happens if funds get held or returned?" Your default response: pause discretionary transfers, protect bill pay, document the event, and reconcile deposits against invoice IDs in your next weekly audit.

When things go wrong: late payments, holds, chargebacks, and bad terms (recovery protocols)#

Treat exceptions as normal operations, and route them through a written protocol so your personal finance automation does not collapse under stress. Safeguards prevent a lot of damage. Protocols are what you run when reality still breaks the plan, because it will.

Step-by-step: run the right protocol for the failure mode#

Step 1: Classify the problem (late, pending/failed, or disputed). Do not guess. Decide which bucket the event belongs in, then run the matching checklist.

| Failure mode | What it means operationally | Your safe default next move |

|---|---|---|

| Client pays late | Timing breaks your plan | Reforecast your next obligations, then choose what to delay (not what to "hope" for) |

| Payment pending/failed (held/returned) | You can't treat it as received yet | Confirm the payment status and next steps with your processor and the client before you rely on it |

| Chargeback | A formal dispute risk | Treat it as disputed until it's resolved |

| "Bad paper" | Contract ambiguity creates cash risk | Tighten templates so billing and dispute handling follow a clearer path |

Step 2: Late payment protocol (income timing risk). Review your SOW and invoice terms, then enforce them consistently. Set a reminder schedule you actually run (not a one-off emotional email), and keep the tone factual: amount due, due date, payment link, and the next escalation step you already agreed to in writing.

Step 3: Pending/failed payment protocol (confirmation before action). If a payment is marked pending, held, or returned, treat it as unconfirmed until you understand what happened. Follow your payment provider's guidance, confirm status with the client, and document what you learn so you can act quickly if questions come up.

Step 4: Chargeback protocol (dispute operations). Chargebacks often start with "a confused customer who doesn't recognise a transaction, or someone claiming fraud," as Airwallex notes. You win by moving fast with clean records.

Airwallex also says chargeback management software "can reduce resolution time and improve your chances of winning disputes," which matters when global chargeback volume reaches "337 million by 2026."

Recovery playbook you can run today (without heroics)#

- If a client feels higher-risk, revisit how you structure billing and payment terms so expectations are clearer. Use this as your reference: A Strategic Consultant's Guide to Structuring a Retainer Agreement.

- Reduce payment failure exposure by planning for pitfalls up front. Chargebee frames it well: "plan for the pitfalls (technical and otherwise) that might assail a payment shortens the chasm" between what you earned and what you receive.

- Fix "bad paper" by standardizing your templates. Define acceptance, payment triggers, and a clear dispute process so you do not negotiate basics under pressure.

Practical check: write one decision rule for (1) when you update your cash plan, (2) when you escalate with a client, and (3) when you require tighter payment terms next cycle.

Example: a client goes quiet after delivery. If you already defined acceptance in the SOW and you keep your records organized, you stop improvising and start executing.

Conclusion: build a "get paid" system you can trust (and reuse every month)#

Automation works for freelancers when you treat it like ops, not vibes. The catch is that many examples floating around online sell "systems" with big income numbers, not evidence-backed guidance for setting up personal finance automation safely.

In the sources reviewed for this piece, you'll see marketing-style claims like a "3-step system" tied to "$84 MRR" and tools that do "80% of the work," plus a Member-only Medium story titled around making "$47,000 in 90 days" (dated Dec 23, 2025). None of that verifies outcomes or proves which rules you should use, so keep your risk-first thinking in the driver's seat.

Your north star stays simple: obligations get handled, cash stays visible, and "growth" transfers happen only when you choose. Build something you can reuse every month and for every new client, because it runs on rules you can explain, not optimism.

If you want deeper tool and workflow ideas, pair this playbook with Automating Your Freelance Finances: A Guide to Tools and Workflows. You can also reference The Best Personal Finance Apps for Freelancers to compare features, but don't outsource judgment to an app.

Example: a client payment arrives late or gets delayed. Your system keeps essentials running from the account you use for bills, pauses optional transfers (like savings and investing), and forces a manual review before any large moves. Nothing breaks. You stay in control.

If you operate across currencies or need tighter payout traceability, look for modular infrastructure (for example, Virtual Accounts plus Payouts) that supports clean money movement, status visibility, and audit-ready records, where supported. Set compliance gates and keep exports clean so reconciliation stays straightforward.

Copy/paste checklist (use as an ops template, not something the sources above "prove"):

- Bills list updated and payment settings reviewed

- Bills account funded with a cushion you're comfortable with

- Simple pause rules defined for optional transfers when cash gets tight

- Separate set-aside for taxes (where applicable) and a clear rule for when money moves into it

- Savings/investing rules are conditional (only after essentials and your cushion are covered)

- Regular review cadence scheduled (invoices → deposits → transfers)

- Client terms verified in SOW/Retainer Agreement (payment timing, late fees, stop-work, issue resolution)

- Exception protocol written for delayed/failed payments (what pauses, what you document, who you contact)

Frequently Asked Questions

What should I automate first in personal finances if my income is irregular?

Automate the payments with the biggest downside if you miss them. Start with minimum viable bill pay (minimum debt payments, insurance, any “fee if late” obligations), and run those from a dedicated Bills account, not from wherever client money lands. Then automate your buffer and tax set-asides off cleared receipts so your personal finance automation does not outrun reality.

How do freelancers automate finances without overdrafts or missed bills?

Separate “landing” money from “bills” money, then only turn on autopay from the Bills account once it consistently holds your next set of obligations. If you use Mercury, note that Mercury states its business banking has no monthly overdraft fees, minimum balance requirements, or fees for domestic wires, ACH, or checks. Mercury also states subscription payments get withdrawn from your primary account balance, so keep that primary balance funded before you rely on anything else.

How do I automate savings when client payments are unpredictable?

Use event-trigger rules instead of calendar rules: move savings only after a client payment clears, not on the first of the month. Add a hard pause condition: if your buffer falls below your floor, stop automatic savings and investment automation until you recover. If a client pays later than expected, your system can still cover bills because savings never pulled cash out early.

What’s the difference between automating bills vs automating cash-flow management?

Bill automation is basically scheduling payments on dates. A practical way to think about cash-flow management automation is that transfers (automatic savings, taxes, investing) only fire after you confirm cash actually arrived and stays available. That distinction can matter more than app features when you automate personal finances on irregular income.

How do I set up a repeatable monthly finance workflow I can audit?

Run a simple close process: reconcile invoices to deposits, verify upcoming due dates, then review each automation rule for “should this still run?” Use a checklist and a single “money map” page you update monthly. Standardize memos (invoice ID, client name) so you can trace every move. For deeper tooling and routines, use Automating Your Freelance Finances: A Guide to Tools and Workflows.

How do I protect myself from chargebacks and payment holds as a creator or freelancer?

Treat card-funded income as higher-risk cash until you feel confident it will stick, and avoid sweeping it immediately into savings. Keep clean evidence (SOW, acceptance proof, delivery trail) and isolate disputed revenue so one dispute does not destabilize your bill pay. If you invoice through Mercury, Mercury states customers can pay invoices by credit card, Apple Pay, Google Pay, wire, ACH transfer, or ACH debit for subscribers, so match your automation rules to the risk of each rail.

Do I need multiple bank accounts (e.g., Mercury + Ally Bank) to automate safely?

You do not need a specific brand pair. You need functional separation: at minimum, one account for bills and one for spending, plus an optional buffer or tax holding account. If you use Mercury, Mercury says it offers checking and savings accounts with no monthly fees, and it describes itself as a fintech company (not an FDIC-insured bank) with banking services provided through Choice Financial Group and Column N.A., Members FDIC, plus “the protection of up to $5M in FDIC insurance” through partner banks and sweep networks.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- dartmouth.edu/finance/forms-policies-systems/training_guid...trusted

- dartmouth.edu/finance/forms-policies-systems/training_guid...trusted

- dos.ny.gov/february-25-2026vol-xlviii-issue-8trusted

- federalreserve.gov/publications/files/usb_p3.pdftrusted

- govinfo.gov/content/pkg/FR-2024-11-21/pdf/FR-2024-11-21.pdftrusted

- sec.gov/Archives/edgar/vprr/2200/22001154.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Automating Freelance Finances Without Losing Cashflow Control

You can [automate freelance finances](https://solofinancehub.com/blog/how-to-automate-freelance-finances) and still keep control over key cash decisions. The practical target is simple: automate repetitive admin, then keep human approval for higher-risk exceptions.

The Best Personal Finance Apps for Freelancers

If you are choosing among the best personal finance apps freelancers can use, start with payment risk, not popularity. The goal is simple: keep cash flow visible enough to act early when income slows or bills stay fixed.

A Strategic Consultant's Guide to Structuring a Retainer Agreement

**Build your consulting retainer agreement to control scope, stabilize cash flow, and set expectations early.** Scope creep is what happens when work quietly expands beyond what the client approved. The drift can hit your calendar, your margin, and delivery quality. As the CEO of a business-of-one, your agreement is not paperwork. It is the system that protects your time and decisions.